Stock Time Series Forecasting in a Nutshell: AI/ML Regression/Classification, Statistical Modeling & Cross-Validation QC in Python

Zero to hero use-case examples of learning-based forecasting future stock prices based on historical financial data and various explanatory variables.

“The idea that the future is unpredictable is undermined everyday by the ease with which the past is explained.” — Daniel Kahneman

- In this post, we’ll analyze stock time-series data and build learning-based forecasting models using Python libraries [1–26].

- In the simplest terms, time-series forecasting is a technique that utilizes historical and current data to predict future values over a period of time or a specific point in the future.

- Successful forecast of the future stock price can make considerable profit. According to EMH (efficiency market hypothesis), stock prices reflect all existing information, so any price changes not based on newly released information cannot be forecast.

- The technical goal of this project is to analyze the performance of several widely used forecasting methods in predicting stock market movements: statistical modeling techniques such as Auto-ARIMA [7] and FB Prophet [8–17], supervised Machine Learning (ML) linear/nonlinear regression and binary classification algorithms [1–6, 18] with various explanatory variables or features (time dummy, lags, technical indicators, etc.), and recurrent neural networks with LSTM cells under the umbrella of deep learning as a method in AI [19–24, 26].

- While no forecasting approach can predict stock prices with absolute certainty, these methods can provide useful insights and enable investors to make informed decisions.

- Our business objective is to explore the opportunity of pair trading by predicting high growth US tech stocks (NVDA, TSLA, and AAPL) and the major cryptocurrency such as BTC-USD. Referring to the Macroaxis trading idea, can any of the company-specific risk be diversified away by investing in both tech stocks (e.g. NVDA) and Bitcoin at the same time? Let’s talk about it.

- Key Focus: Trading Strategies Based on Tech Indicators and ML. When ML is being combined with indicators to improve success rates when buying or selling stocks, you can navigate the complexities of the market with efficiency [25].

- Cross-Validation QC Visualization: MAE, MAPE, R2-Score, RMSE, yellowbrick residuals and X-plots (ML Regression); FB Prophet cross-validation metrics; expected returns of ML-based algo-trading strategies (backtesting); ARIMA Validation QC (standardized residuals, histogram plus estimated density, Normal Q-Q plot, and ACF/PACF); feature dominance, correlation matrix, mean accuracy scores, confusion matrix, ROC curve, and full classification reports of supervised ML classification algorithms; ADF/KPSS statistical testing; LSTM MSE Loss vs Epoch curve; Test Time Series Data vs LSTM Predictions.

Contents

- TSLA Linear/Nonlinear Trend Detection with Time Dummy

- TSLA Linear Regression with Lagged Variables

- BTC-USD Price Prediction & Algo-Trading Strategies using FB Prophet

- NVDA Price Prediction using Auto-ARIMA, Supervised ML & Technical Indicators

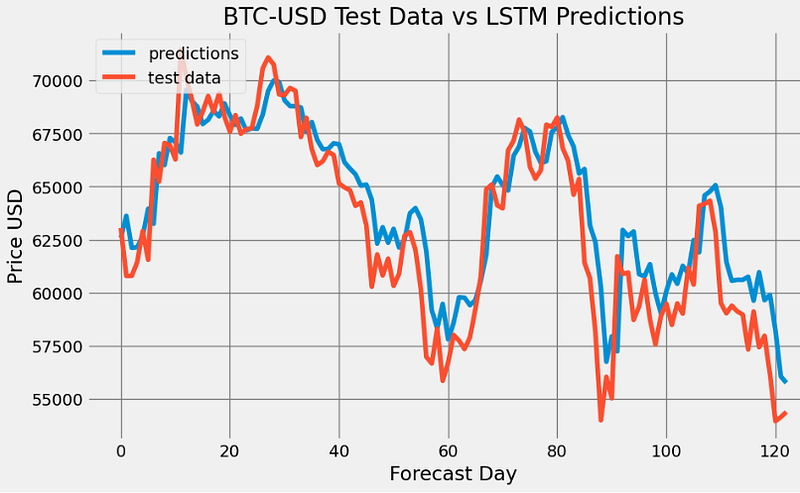

- BTC-USD Price Prediction using LSTM

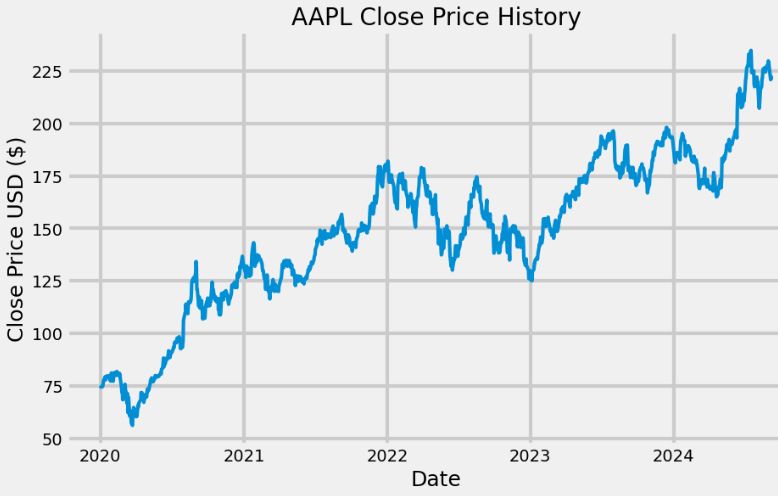

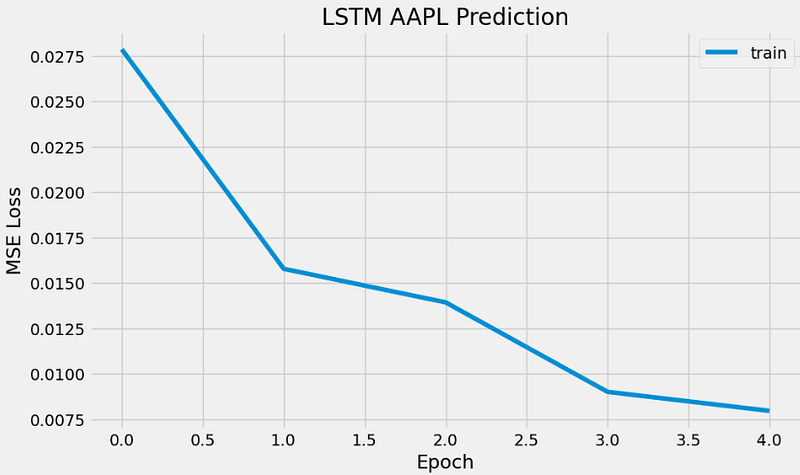

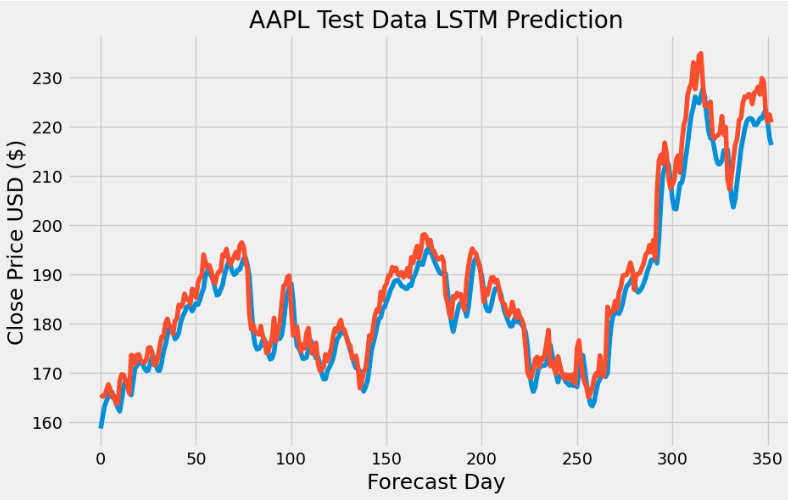

- AAPL Price Prediction using LSTM

In the sequel, we’ll delve into the specifics of the aforementioned contents.

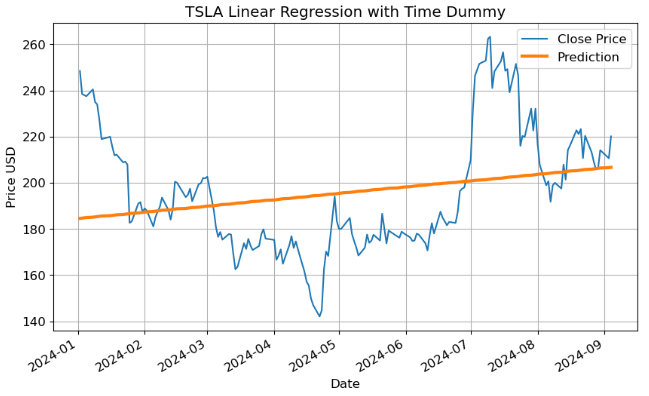

TSLA Linear Trend Detection with Time Dummy

- Let’s implement the basic linear regression algorithm using the time dummy as the most basic time-step feature, which counts off time steps in the series from beginning to end [1].

- Reading the input TSLA stock data

import pandas as pd

import yfinance as yf

df_daily = yf.download('TSLA',

start="2024-01-01",

progress=False)

df_daily.tail()

Open High Low Close Adj Close Volume

Date

2024-08-28 209.720001 211.839996 202.589996 205.750000 205.750000 64116400

2024-08-29 209.800003 214.889999 205.970001 206.279999 206.279999 62308800

2024-08-30 208.630005 214.570007 207.029999 214.110001 214.110001 63370600

2024-09-03 215.259995 219.899994 209.639999 210.600006 210.600006 76500900

2024-09-04 210.759995 220.399994 210.619995 220.080002 220.080002 29225853 - Preparing the data and training the Linear Regression (LR) model

df1 = df_daily.copy()

df1['Time'] = np.arange(len(df_daily.index))

from sklearn.linear_model import LinearRegression

# Training data

X = df1.loc[:, ['Time']] # features

y = df1.loc[:, 'Close'] # target

# Train the model

model = LinearRegression()

model.fit(X, y)

# Store the fitted values as a time series with the same time index as

# the training data

y_pred = pd.Series(model.predict(X), index=X.index)

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 12})

ax = y.plot(label='Close Price')

ax = y_pred.plot(ax=ax, linewidth=3,label='Prediction')

ax.set_title('TSLA Linear Regression with Time Dummy');

plt.legend()

plt.ylabel('Price USD')

plt.grid()

- Calculating the LR performance metrics

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

from sklearn.metrics import mean_absolute_percentage_error

# Calculate MAE, MAPE, R2-Score and RMSE

y_test=y

mae = mean_absolute_error(y_test, y_pred)

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

mape=mean_absolute_percentage_error(y_test, y_pred)

r2score = r2_score(y_test, y_pred)

print(f'Mean Absolute Error: {mae:.2f}')

print(f'MAPE: {mape:.2f}')

print(f'Root Mean Squared Error: {rmse:.2f}')

print(f'R2-Score: {r2score:.2f}')

Mean Absolute Error: 20.58

MAPE: 0.10

Root Mean Squared Error: 25.59

R2-Score: 0.06Inferences:

- Provided the time series doesn’t have any missing dates, we can create a time dummy by counting out the length of the series.

- The above model assumes a linear relationship [2] between the time variable and Close price. In the current study, this assumption is violated, leading to biased predictions of TSLA stock prices.

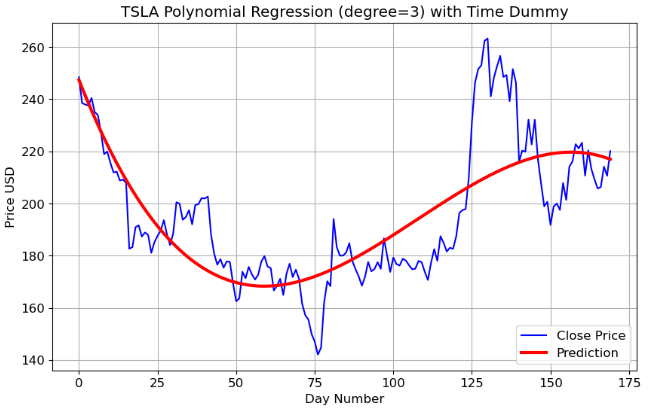

TSLA Nonlinear Trend Detection with Time Dummy

- To address the aforementioned drawback of LR, we consider Polynomial Regression (PR) [3, 4] in which the relationship between the time dummy and Close price is modeled as an nth-degree polynomial.

- Running the polynomial regression with n=3

from sklearn.preprocessing import PolynomialFeatures

poly_regressor = PolynomialFeatures(degree=3)

X_columns = poly_regressor.fit_transform(X)

from sklearn.linear_model import LinearRegression

model = LinearRegression()

model.fit(X_columns, y)

pred = model.predict(poly_regressor.fit_transform(X))

plt.figure(figsize=(10,6))

plt.rcParams.update({'font.size': 12})

plt.plot(X, y, color = 'blue',label='Close Price')

plt.plot(X, pred, color = 'red',label='Prediction',lw=3)

plt.ylabel('Price USD')

plt.xlabel('Day Number')

plt.legend(loc='lower right')

plt.title('TSLA Polynomial Regression (degree=3) with Time Dummy')

plt.grid()

- Calculating the PR performance metrics

# Calculate MAE, MAPE, R2-Score and RMSE

y_test=y

y_pred=pred

mae = mean_absolute_error(y_test, y_pred)

rmse = np.sqrt(mean_squared_error(y_test, y_pred))

mape=mean_absolute_percentage_error(y_test, y_pred)

r2score = r2_score(y_test, y_pred)

print(f'Mean Absolute Error: {mae:.2f}')

print(f'MAPE: {mape:.2f}')

print(f'Root Mean Squared Error: {rmse:.2f}')

print(f'R2-Score: {r2score:.2f}')

Mean Absolute Error: 12.37

MAPE: 0.06

Root Mean Squared Error: 16.52

R2-Score: 0.61Inferences:

- We can see that PR provides more accurate predictions of TSLA prices than LR.

- The degree of the polynomial equation determines the level of nonlinearity in the price-time relationship.

- However, PR models have poor interpolatory and extrapolatory properties. Even a single outlier in the data can seriously mess up the results. Generally, high degree polynomials (n>>2) are notorious for oscillations between exact-fit values.

TSLA Linear Regression with Lagged Variables

- Our next step is to analyze the impact of lagged features in LR [5–7]. Lagged features will be created by shifting the time series, and a simple LR model will be trained to predict TSLA Close price based on these features, viz.

- Read and explore the TSLA historical data using yfinance

- Transform the dataset to include lagged features (LF) by shifting the time series and examine LF-price correlation coefficients

- Split the input dataset into train/test sets and train a LR model

- Calculate model performance metrics for test data and visualize the regression results using yellowbrick.

- Reading the input TSLA stock data 2022–2024

import pandas as pd

import yfinance as yf

df_daily = yf.download('TSLA',

start="2022-01-01",

progress=False)

df_daily.tail()

Open High Low Close Adj Close Volume

Date

2024-08-28 209.720001 211.839996 202.589996 205.750000 205.750000 64116400

2024-08-29 209.800003 214.889999 205.970001 206.279999 206.279999 62308800

2024-08-30 208.630005 214.570007 207.029999 214.110001 214.110001 63370600

2024-09-03 215.259995 219.899994 209.639999 210.600006 210.600006 76500900

2024-09-04 210.759995 222.220001 210.619995 217.639999 217.639999 69155198

data=df_daily.copy()- Plotting PACF of the Close price

from statsmodels.graphics.tsaplots import plot_pacf

series = data['Close']

plot_pacf(series)

plt.show()

- The above PACF is helpful for identifying lags of the time variable that might be useful predictors of prices.

- Adding LF to the input DataFrame and dropping NaN values [7]

# Adding lag features to the DataFrame

for i in range(1, 6): # Creating lag features up to 5 days

data[f'Lag_{i}'] = data['Close'].shift(i)

# Drop rows with NaN values resulting from creating lag features

data.dropna(inplace=True)

data.tail()

Open High Low Close Adj Close Volume Lag_1 Lag_2 Lag_3 Lag_4 Lag_5

Date

2024-08-28 209.720001 211.839996 202.589996 205.750000 205.750000 64116400 209.210007 213.210007 220.320007 210.660004 223.270004

2024-08-29 209.800003 214.889999 205.970001 206.279999 206.279999 62308800 205.750000 209.210007 213.210007 220.320007 210.660004

2024-08-30 208.630005 214.570007 207.029999 214.110001 214.110001 63370600 206.279999 205.750000 209.210007 213.210007 220.320007

2024-09-03 215.259995 219.899994 209.639999 210.600006 210.600006 76500900 214.110001 206.279999 205.750000 209.210007 213.210007

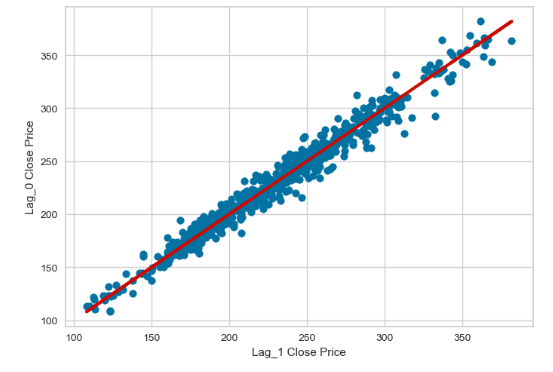

2024-09-04 210.759995 222.220001 210.619995 218.779999 218.779999 67416126 210.600006 214.110001 206.279999 205.750000 209.210007- Examining the Pearson’s correlation coefficient (CC) between LF (Lag_n, n>0) and Close price (Lag_0)

x=data['Lag_1']

y=data['Close']

r = np.corrcoef(x, y)

print(r[0, 1])

0.9862943483049603

plt.scatter(x,y)

plt.plot(x,x,c='r',lw=3)

plt.xlabel('Lag_1 Close Price')

plt.ylabel('Lag_0 Close Price')

plt.show()

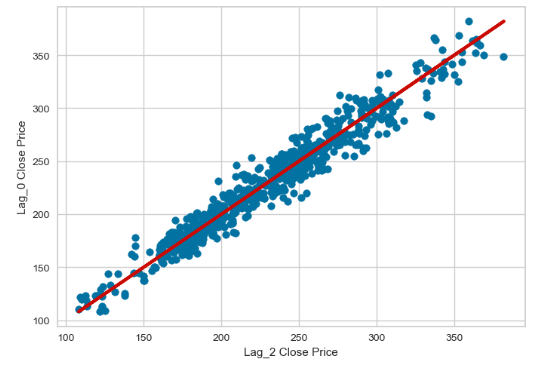

x=data['Lag_2']

y=data['Close']

r = np.corrcoef(x, y)

print(r[0, 1])

0.9738195265814875

plt.scatter(x,y)

plt.plot(x,x,c='r',lw=3)

plt.xlabel('Lag_2 Close Price')

plt.ylabel('Lag_0 Close Price')

plt.show()

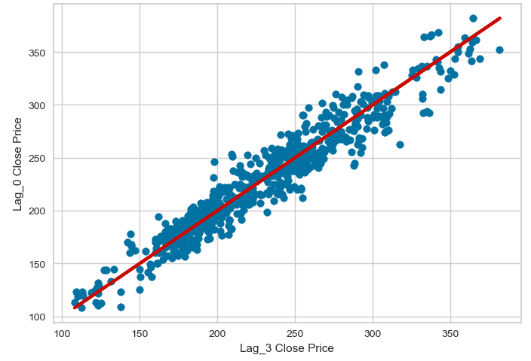

x=data['Lag_3']

y=data['Close']

r = np.corrcoef(x, y)

print(r[0, 1])

0.960646796452951

plt.scatter(x,y)

plt.plot(x,x,c='r',lw=3)

plt.xlabel('Lag_3 Close Price')

plt.ylabel('Lag_0 Close Price')

plt.show()

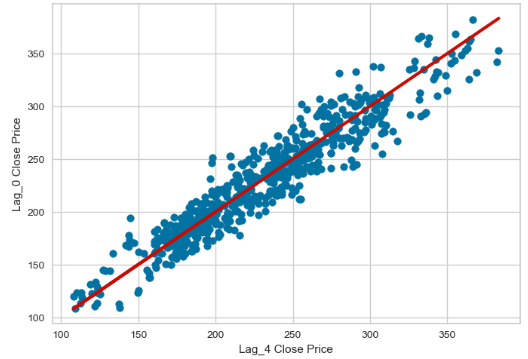

x=data['Lag_4']

y=data['Close']

r = np.corrcoef(x, y)

print(r[0, 1])

0.9486244863366714

plt.scatter(x,y)

plt.plot(x,x,c='r',lw=3)

plt.xlabel('Lag_4 Close Price')

plt.ylabel('Lag_0 Close Price')

plt.show()

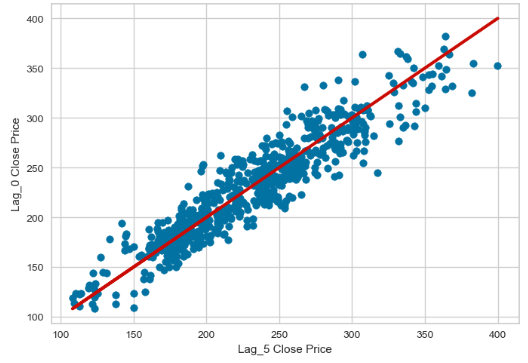

x=data['Lag_5']

y=data['Close']

r = np.corrcoef(x, y)

print(r[0, 1])

0.9335105839215305

plt.scatter(x,y)

plt.plot(x,x,c='r',lw=3)

plt.xlabel('Lag_5 Close Price')

plt.ylabel('Lag_0 Close Price')

plt.show()

- All five lags are statistically significant with CC>90%.

- Defining the explanatory and dependent variables

X = data[['Lag_1','Lag_2','Lag_3','Lag_4','Lag_5']] # Features

y = data['Close'] # Target variable - Splitting the dataset into train/test sets with split_ratio = 0.8

split_ratio = 0.8

split_index = int(len(data) * split_ratio)

X_train, X_test = X[:split_index], X[split_index:]

y_train, y_test = y[:split_index], y[split_index:]- Training the LR model and making test predictions

from sklearn.linear_model import LinearRegression

# Train the linear regression model

model = LinearRegression()

model.fit(X_train, y_train)

# Make predictions

predictions = model.predict(X_test)- Calculating the key LR model performance metrics

from sklearn.metrics import mean_absolute_error, mean_squared_error, r2_score

from sklearn.metrics import mean_absolute_percentage_error

mae = mean_absolute_error(y_test, predictions)

mape=mean_absolute_percentage_error(y_test, predictions)

mse = mean_squared_error(y_test, predictions)

r2 = r2_score(y_test, predictions)

MAE: 5.59

MAPE: 0.03

MSE: 56.30

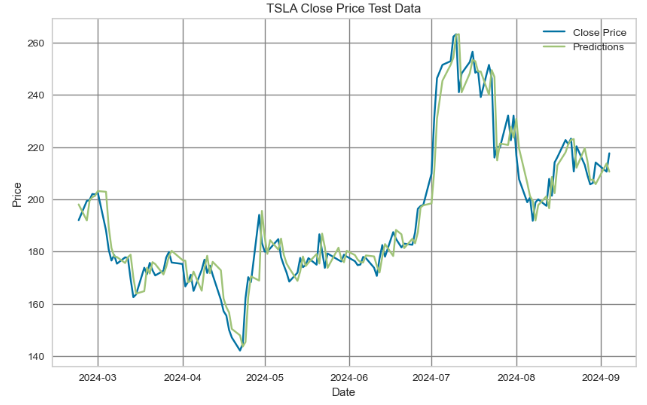

R^2 Score: 0.92- Directly comparing test LR predictions vs Close price

plt.figure(figsize=(10, 6))

plt.plot(y_test,label='Close Price')

plt.plot(y_test.index,predictions,label='Predictions')

plt.xlabel('Date')

plt.ylabel('Price')

plt.title('TSLA Close Price Test Data')

plt.legend()

plt.grid(color='grey')

- The above plot shows the actual values of the real time series compared to the predicted values from the LR model. We can see that the predicted values do not deviate significantly from the actual test values.

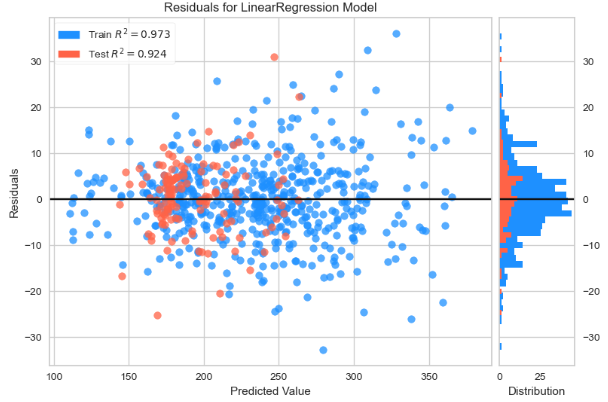

- Plotting train/test data residuals for the LR model

!pip install yellowbrick

from yellowbrick.regressor import ResidualsPlot

viz = ResidualsPlot(model,

train_color="dodgerblue",

test_color="tomato",

fig=plt.figure(figsize=(9,6))

)

viz.fit(X_train, y_train)

viz.score(X_test, y_test)

viz.show();

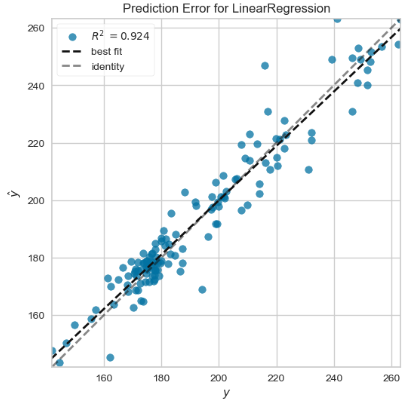

- Plotting test data prediction errors for the LR model

from yellowbrick.regressor import PredictionError

viz = PredictionError(model,

fig=plt.figure(figsize=(6,6))

)

viz.fit(X_train, y_train)

viz.score(X_test, y_test)

viz.show();

Inferences:

- We have evaluated the LR model that captures the dynamic causal link between an observed stock price and several lagged observations (previous time steps). The core idea is that the current value of a time series can be expressed as a linear combination of its past values, with some random noise [5–7].

- Direct comparisons of the actual time series (i.e. test values against the test predictions), train/test data residuals for the LR model, and X-plots predictions vs test data predicted values do not deviate significantly from the actual test values.

- The following performance metrics give us a quantitative measure of how well the LR model predicts the time series data based on its lagged features

MAE: 5.59

MAPE: 0.03

MSE: 56.30

R^2 Score: 0.92- This result suggests that the LR model fits the Close price quite well and is a good predictor for the TSLA dataset.

BTC-USD Price Prediction & Algo-Trading Strategies using FB Prophet

- In this section, we’ll discuss the BTC-USD price prediction using FB Prophet [8–17], including hyperparameter optimization (HPO), cross-validation QC & modified algo-trading strategies.

- Installation:

!pip install prophet

- Objective: This study focuses on using the FB Prophet framework to forecast BTC-USD prices accurately. By analyzing historical BTC-USD price data, the study aims to capture patterns and dependencies to provide valuable predictive models and profitable algo-trading strategies for investors, traders, and analysts in the volatile cryptocurrency market.

- Challenge: The price of BTC-USD is known for its volatility, which means it can experience significant and rapid fluctuations in a short period. This volatility is characteristic of many cryptocurrencies and is influenced by various factors, such as market friction, regulatory developments, global economic conditions, and investor sentiment.

- Why FB Prophet: A native handling of trend and seasonality features, that makes Prophet a good baseline model if the time series follows business cycles [14]. A great advantage compared to autoregressive models (eg. ARIMA) is that Prophet doesn’t require stationary time series: a trend component is generated natively.

- Let’s delve in further to the matter.

2022–2025 Time Horizon

- Importing the necessary Python libraries

import pandas as pd

import plotly.express as px

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

import requests

import numpy as np

import matplotlib.pyplot as plt

from math import floor

from termcolor import colored as cl

plt.rcParams['figure.figsize'] = (12, 6)

plt.style.use('fivethirtyeight')

import pandas as pd

import yfinance as yf

import datetime

from datetime import date, timedelta

from plotly.subplots import make_subplots

import plotly.graph_objects as go

from datetime import datetime

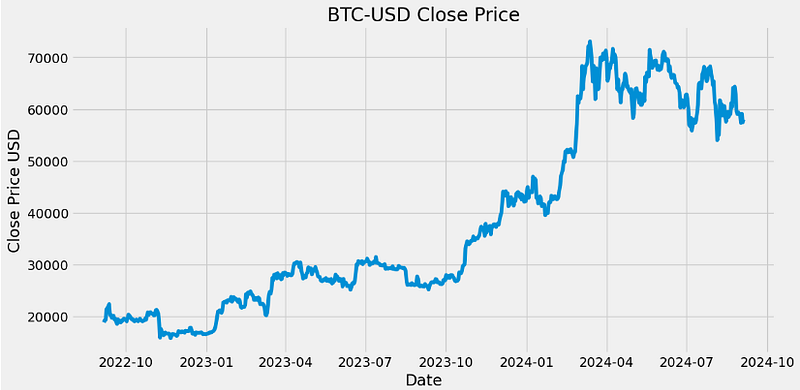

today = date.today()- Reading and plotting the BTC-USD historical data

d1 = today.strftime("%Y-%m-%d")

end_date = d1

d2 = date.today() - timedelta(days=730)

d2 = d2.strftime("%Y-%m-%d")

start_date = d2

data = yf.download('BTC-USD',

start=start_date,

end=end_date,

progress=False)

data["Date"] = data.index

data = data[["Date", "Open", "High", "Low", "Close", "Adj Close", "Volume"]]

data.reset_index(drop=True, inplace=True)

data.tail()

Date Open High Low Close Adj Close Volume

725 2024-08-31 59,117.48 59,432.59 58,768.79 58,969.90 58,969.90 12403470760

726 2024-09-01 58,969.80 59,062.07 57,217.82 57,325.49 57,325.49 24592449997

727 2024-09-02 57,326.97 59,403.07 57,136.03 59,112.48 59,112.48 27036454524

728 2024-09-03 59,106.19 59,815.06 57,425.17 57,431.02 57,431.02 26666961053

729 2024-09-04 57,430.35 58,511.57 55,673.16 57,971.54 57,971.54 35627680312

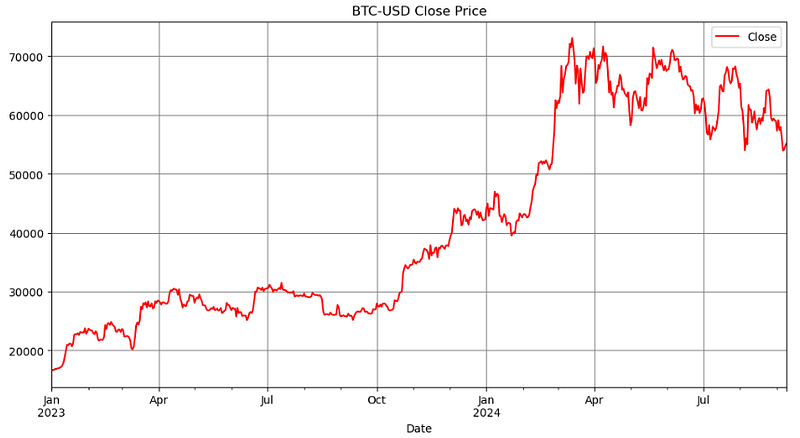

plt.plot(data['Date'],data['Close'])

plt.xlabel('Date')

plt.ylabel('Close Price USD')

plt.title('BTC-USD Close Price')

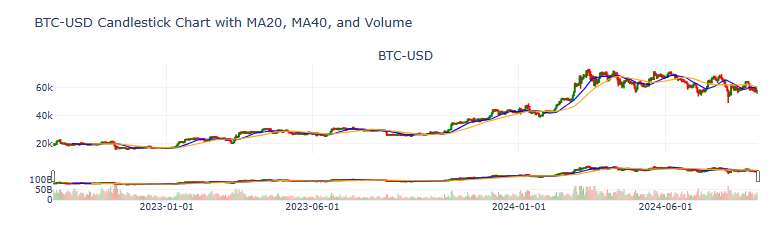

- Plotting the BTC-USD candlesticks with the 20-, 40-day simple moving averages, volume and the volatility histogram in Plotly [15]

class StockAnalysis:

def __init__(self, symbol, source, start, end=datetime.today().strftime('%Y-%m-%d')):

self.symbol = symbol

self.source = source

self.start = start

self.end = end

self.data = None

def fetch_prepare_data(self):

"""

Fetch historical data from the specified source, filter out days without trading activity,

and calculate moving averages. Currently, supports Yahoo Finance via yfinance.

"""

try:

if self.source.lower() == 'yahoo':

data = yf.download(self.symbol, start=self.start, end=self.end)

else:

raise ValueError("Currently, only 'yahoo' source is supported.")

except ValueError as e:

print(f"Error: {e}")

return

except Exception as e:

print(f"An error occurred while fetching data: {e}")

return

self.data = data

return data

def generate_plot(self):

"""

Generate and display a candlestick chart with MA20, MA40, and volume.

"""

self.data['MA20'] = self.data['Close'].rolling(window=20).mean()

self.data['MA40'] = self.data['Close'].rolling(window=40).mean()

try:

# Initialize a figure with subplots

fig = make_subplots(rows=2, cols=1,

shared_xaxes=True,

vertical_spacing=0.15,

subplot_titles=(f'{self.symbol}', ''),

row_width=[0.2, 0.7]

)

# Add Candlestick plot

fig.add_trace(go.Candlestick(x=self.data.index, open=self.data['Open'], high=self.data['High'],

low=self.data['Low'], close=self.data['Close'], name="Candlestick",

increasing_line_color='green', decreasing_line_color='red'), row=1, col=1)

# Add MA20 and MA40

fig.add_trace(go.Scatter(x=self.data.index, y=self.data['MA20'], mode='lines',

line=dict(color='blue', width=1.5), name='MA 20'), row=1, col=1)

fig.add_trace(go.Scatter(x=self.data.index, y=self.data['MA40'], mode='lines',

line=dict(color='orange', width=1.5), name='MA 40'), row=1, col=1)

# Add Volume plot

colors = ['green' if row['Close'] > row['Open'] else 'red' for index, row in self.data.iterrows()]

fig.add_trace(go.Bar(x=self.data.index, y=self.data['Volume'], name='', marker_color=colors), row=2,

col=1)

# Find the first available dates in January and June

tickvals = []

ticktext = []

for year in range(int(self.start[:4]), int(self.end[:4]) + 1):

for month in [1, 6]: # January and June

month_data = self.data[(self.data.index.month == month) & (self.data.index.year == year)]

if not month_data.empty:

first_date = month_data.index[0]

tickvals.append(first_date)

ticktext.append(first_date.strftime('%Y-%m-%d'))

# Set x-axis type to 'category' and specify tickvals and ticktext

fig.update_xaxes(type='category', tickvals=tickvals, ticktext=ticktext)

# Update layout and show the figure as before...

fig.update_layout(title=f'{self.symbol} Candlestick Chart with MA20, MA40, and Volume',

xaxis_title='', yaxis_title='',

template='plotly_white', showlegend=False,

margin=dict(b=80))

return fig

except Exception as e:

print(f"An error occurred during plot generation: {e}")

def generate_volatility_histogram(self):

"""

Generate and display a histogram of daily volatility.

"""

try:

# Calculate daily returns

self.data['Daily Return'] = self.data['Close'].pct_change()

# Compute daily volatility (standard deviation of daily returns)

daily_volatility = self.data['Daily Return'].std()

# Plot histogram of daily volatility

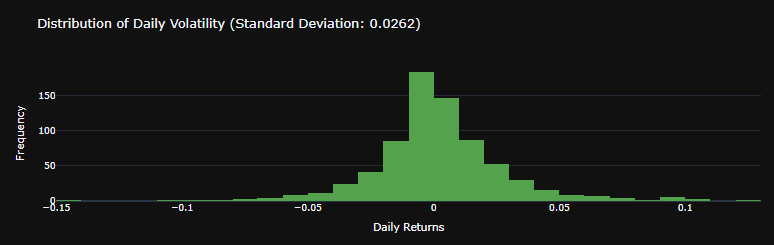

fig = go.Figure(data=[go.Histogram(x=self.data['Daily Return'], nbinsx=50, marker_color='#54A24B')])

fig.update_layout(title=f'Distribution of Daily Volatility\n(Standard Deviation: {daily_volatility:.4f})',

xaxis_title='Daily Returns',

yaxis_title='Frequency',

template='plotly_dark')

return fig

except Exception as e:

print(f"An error occurred during plot generation: {e}")

analysis = StockAnalysis(symbol='BTC-USD', source = 'yahoo', start =d2)

data = analysis.fetch_prepare_data()

fig_candelestick = analysis.generate_plot()

fig_candelestick.show()

fig_volatility = analysis.generate_volatility_histogram() fig_volatility.show()

- Let’s apply the Box-Cox transformation that transforms Close price so that our time series closely resembles a normal distribution

### Boxcox transformation

from statsmodels.base.transform import BoxCox

bc= BoxCox()

data["Close"], lmbda =bc.transform_boxcox(data["Close"])- Making our data Prophet compliant [16]

data=data.reset_index(drop=False)

data1=data[["Date", "Close"]]

data1.columns=["ds", "y"]

data1.tail()

ds y

725 2024-08-31 61.44

726 2024-09-01 60.97

727 2024-09-02 61.48

728 2024-09-03 61.00

729 2024-09-04 61.16- Training, fitting the Prophet model and making out-of-sample predictions with periods=365 [12, 16]

## Creating model parameters

model_param ={

"daily_seasonality": False,

"weekly_seasonality":True,

"yearly_seasonality":True,

"seasonality_mode": "multiplicative",

"growth": "logistic"

}

# Import Prophet

from prophet import Prophet

model = Prophet(**model_param)

data1['cap']= data1["y"].max() + data1["y"].std() * 0.05

# Setting a cap or upper limit for the forecast as we are using logistics growth

# The cap will be maximum value of target variable plus 5% of std.

model.fit(data1)

# Create future dataframe

future= model.make_future_dataframe(periods=365)

#future= model.make_future_dataframe(periods=60)

future['cap'] = data1['cap'].max()

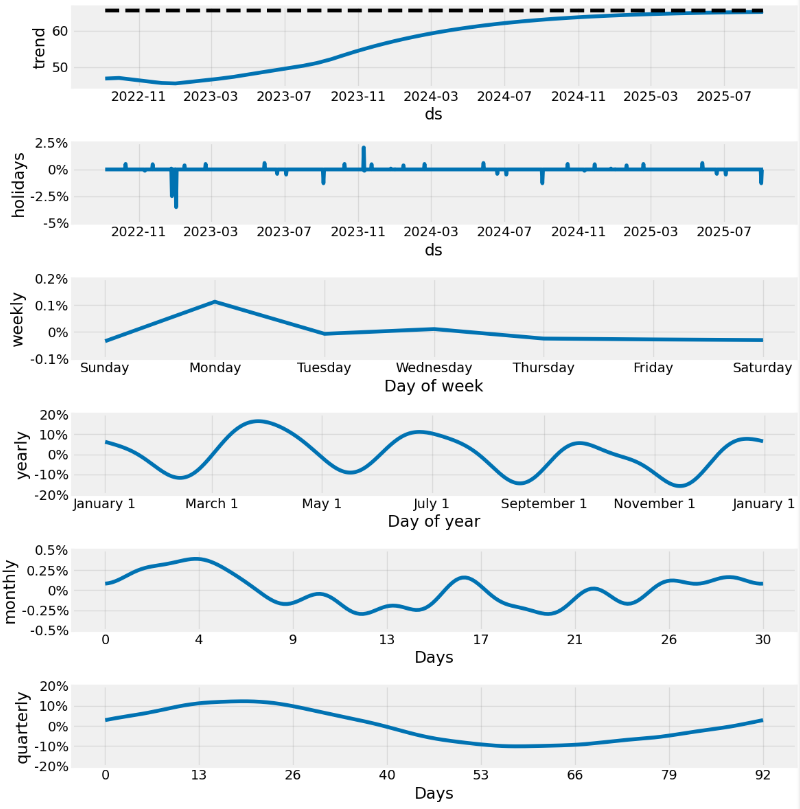

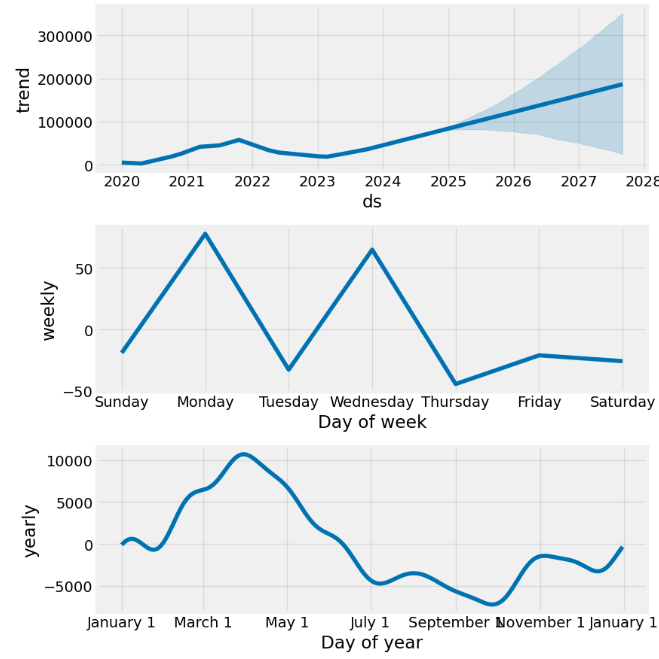

forecast= model.predict(future)- Plotting the Prophet trend, weekly and yearly components

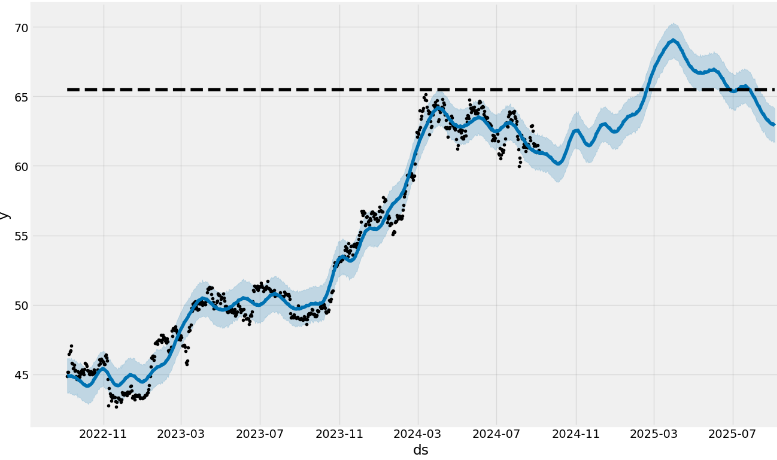

model.plot_components(forecast,figsize=(16, 10));

- Plotting the forecast vs actual values of BTC-USD prices

model.plot(forecast,figsize=(14, 8));# block dots are actual values and blue dots are forecast

- Here, the dashed line indicates a cap or upper limit for the forecast.

- We should remember that the out-of-sample forecast was built using all of the data prior to the forecast period. As an example, the forecast for 2025 was built using using data up to and including September 4, 2024.

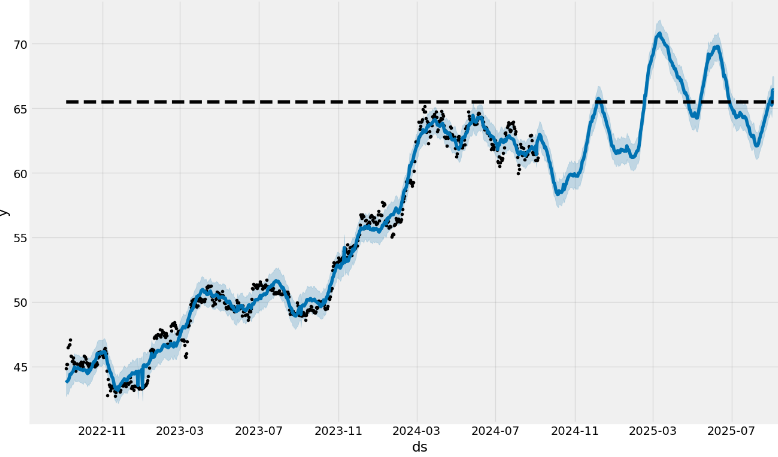

- Adding the monthly/quarterly seasonality and US events

## Adding parameters and seasonality and events

model = Prophet(**model_param)

model= model.add_seasonality(name="monthly", period=30, fourier_order=10)

model= model.add_seasonality(name="quarterly", period=92.25, fourier_order=10)

model.add_country_holidays("US")

model.fit(data1)

# Create future dataframe

future= model.make_future_dataframe(periods=365)

future['cap'] = data1['cap'].max()

forecast= model.predict(future)

from prophet.plot import plot

plot(model, forecast, figsize=(14, 8))

- Notice a somewhat increased frequency content and a narrow confidence interval (CI) of the above out-of-sample predictions as compared to the forecast without monthly/quarterly seasonality and US events.

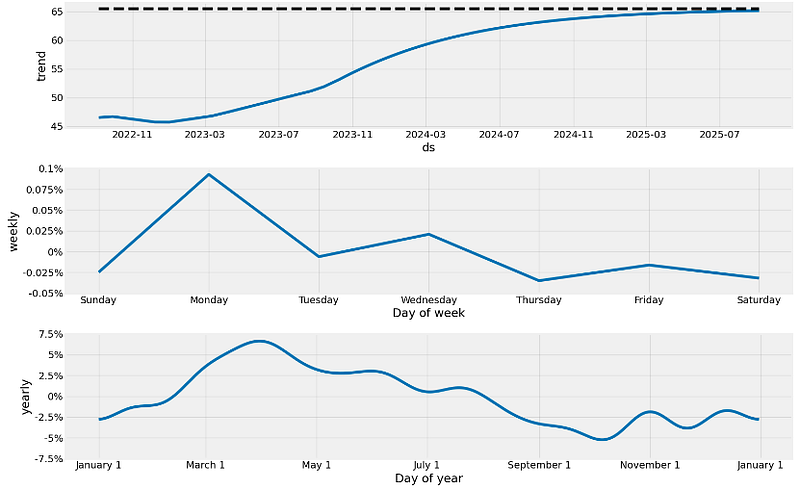

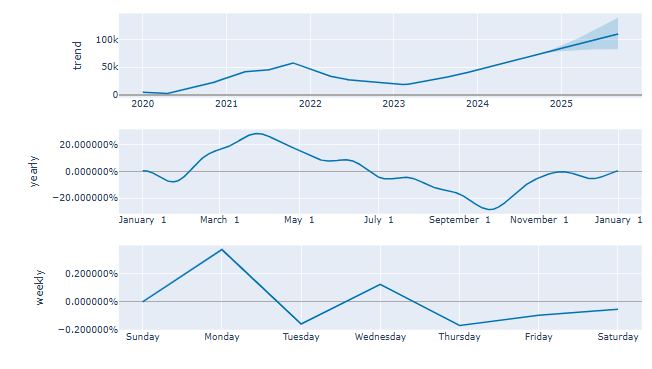

- Plotting the Prophet trend, US holidays, and seasonality

from prophet.plot import plot_components

plot_components(model, forecast, figsize=(12, 12))

We see a few features in the above components:

- A strong upward trend with a change in the rate of increase somewhere between 2023–11 and 2024–06

- Fairly strong yearly seasonality

- Variable monthly seasonal effect.

The generated forecast will have many columns as shown in the below output. We will go over the significant ones:

- yhat: This column has the predictions for the number of transactions for the future timestamps.

- yhat_lower: Prophet also takes into account the uncertainty levels while making predictions. This represents the lower bound of the uncertainty interval for each forecasted value.

- yhat_upper: This column represents the upper bound of the uncertainty interval for each forecasted value.

- trend: This represents the estimated trend component of the forecast, the overall direction of growth.

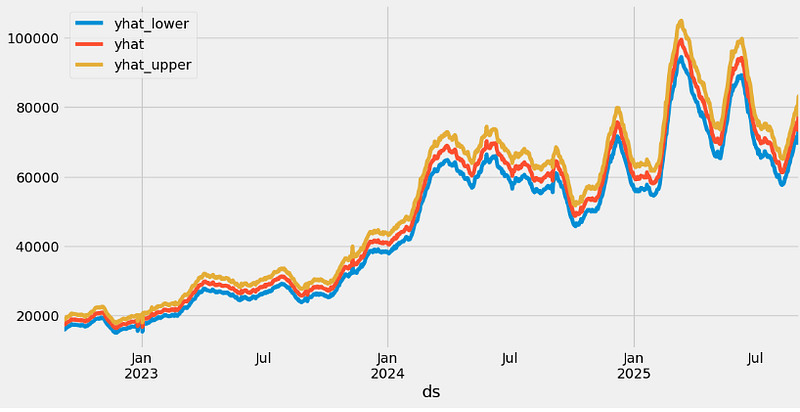

Performing a reverse Box-Cox transformation and plotting yhat, yhat_lower, and yhat_upper

forecast["yhat"]=bc.untransform_boxcox(x=forecast["yhat"], lmbda=lmbda)

forecast["yhat_lower"]=bc.untransform_boxcox(x=forecast["yhat_lower"], lmbda=lmbda)

forecast["yhat_upper"]=bc.untransform_boxcox(x=forecast["yhat_upper"], lmbda=lmbda)

forecast.plot(x="ds", y=["yhat_lower", "yhat", "yhat_upper"])

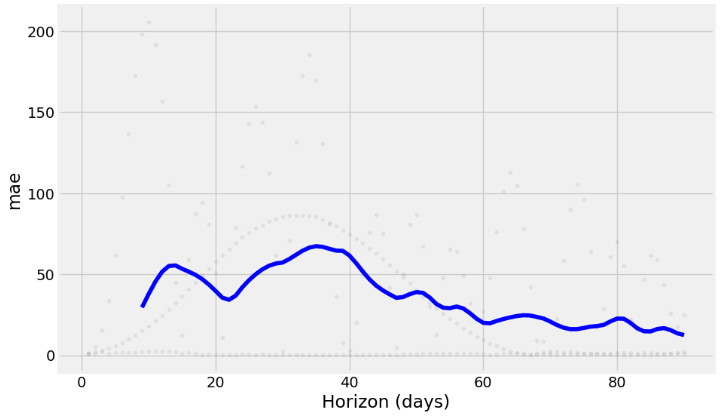

- Examining the Prophet cross-validation metrics with horizon=’90 days’

from prophet.diagnostics import cross_validation, performance_metrics

from prophet.plot import plot_cross_validation_metric

df_cv = cross_validation(model, initial="600 days", period="30 days", horizon="90 days")

cutoffs = pd.to_datetime(['2022-09-01', '2023-05-01', '2024-03-01'])

df_cv2 = cross_validation(model, cutoffs=cutoffs, horizon='90 days')

fig = plot_cross_validation_metric(df_cv2, metric='mae')

- One cool feature is that we can see the error metric per day.

- Performing the Prophet hyperparameter optimization (HPO) [12]

## Hyper parameter Tuning

import itertools

import numpy as np

from prophet.diagnostics import cross_validation, performance_metrics

param_grid={

"daily_seasonality": [False],

"weekly_seasonality":[True],

"yearly_seasonality":[True],

"growth": ["logistic"],

'changepoint_prior_scale': [0.001, 0.01, 0.1, 0.5], # to give higher value to prior trend

'seasonality_prior_scale': [0.01, 0.1, 1.0, 10.0] # to control the flexibility of seasonality components

}

# Generate all combination of parameters

all_params= [

dict(zip(param_grid.keys(), v))

for v in itertools.product(*param_grid.values())

]

rmses= list ()

# go through each combinations

for params in all_params:

m= Prophet(**params)

m= m.add_seasonality(name= 'monthly', period=30, fourier_order=5)

m= m.add_seasonality(name= "quarterly", period= 92.25, fourier_order= 10)

m.add_country_holidays(country_name="US")

m.fit(data1)

df_cv= cross_validation(m, initial="500 days", period="180 days", horizon="90 days")

df_p= performance_metrics(df_cv, rolling_window=1)

rmses.append(df_p['rmse'].values[0])

# find teh best parameters

best_params = all_params[np.argmin(rmses)]

print("\n The best parameters are:", best_params)

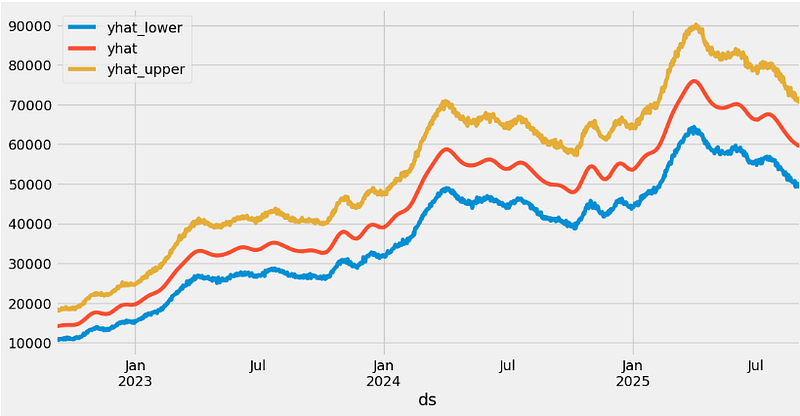

The best parameters are: {'daily_seasonality': False, 'weekly_seasonality': True, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 0.01}- After HPO: performing a reverse Box-Cox transformation and plotting yhat, yhat_lower, and yhat_upper

forecast["yhat"]=bc.untransform_boxcox(x=forecast["yhat"], lmbda=lmbda)

forecast["yhat_lower"]=bc.untransform_boxcox(x=forecast["yhat_lower"], lmbda=lmbda)

forecast["yhat_upper"]=bc.untransform_boxcox(x=forecast["yhat_upper"], lmbda=lmbda)

forecast.plot(x="ds", y=["yhat_lower", "yhat", "yhat_upper"])

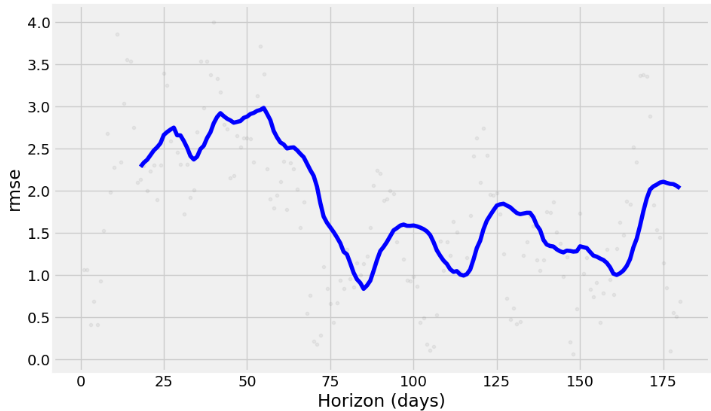

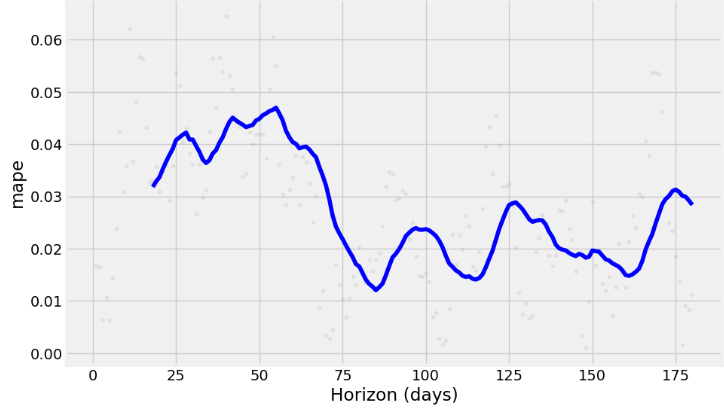

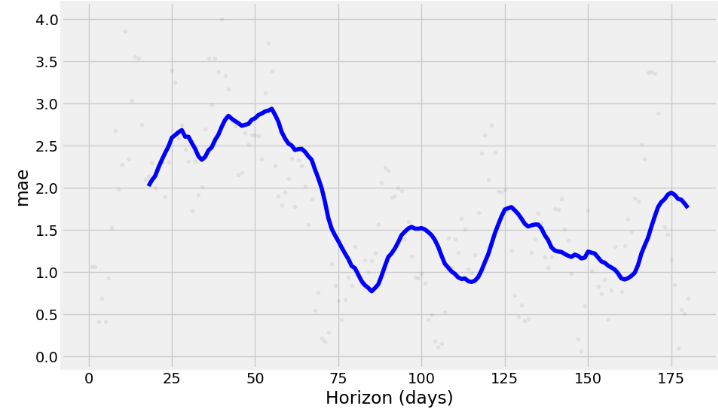

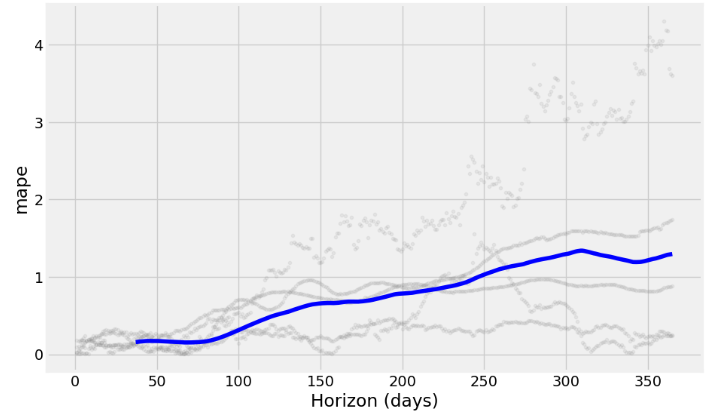

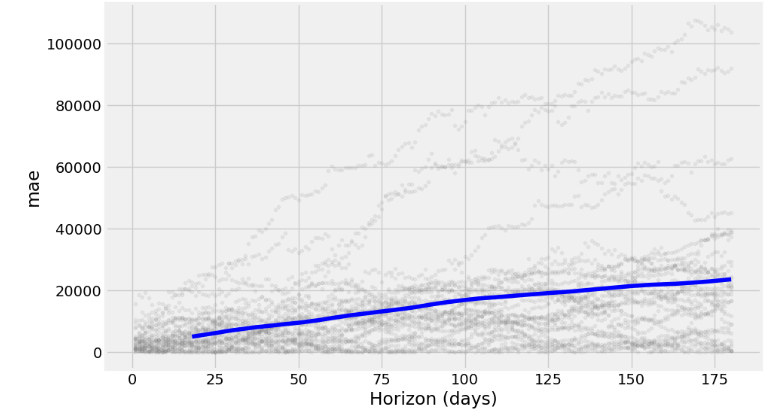

- Running the cross-validation and use a range of built-in metrics to evaluate the performance of our model, such as mean absolute error (MAE), mean squared error (MSE), mean average percentage error (MAPE), or root mean squared error (RMSE) with horizon=’180 days’, viz.

df_cv2 = cross_validation(model1, horizon='180 days')

fig = plot_cross_validation_metric(df_cv2, metric='rmse')

fig = plot_cross_validation_metric(df_cv2, metric='mape')

fig = plot_cross_validation_metric(df_cv2, metric='mae')

- The charts above show how reliable the forecast is over a specific time horizon. The above built-in metrics give us a good enough estimation of the model’s performance.

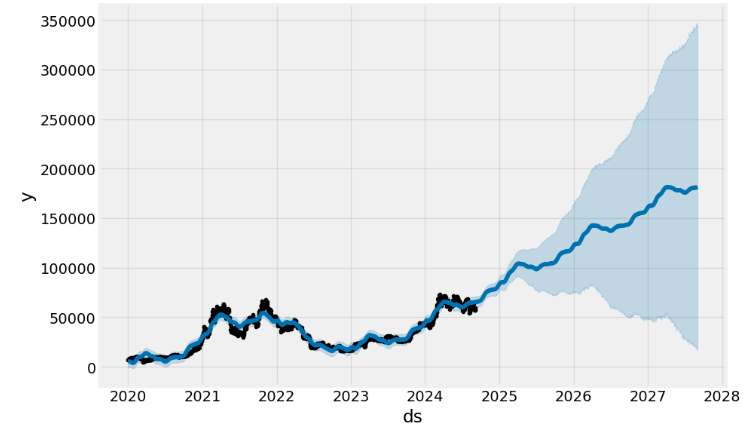

2020–2027 Time Horizon

- Next, let’s create a 3 year Prophet forecast [13] until 2027–09–03 using the historical daily BTC-USD adjusted close price data from 2020–01–01 to 2024–09–05.

- Reading the input BTC-USD stock data and preparing a dataframe with two columns — ds and y

import pandas as pd

import numpy as np

from prophet import Prophet

import matplotlib.pyplot as plt

from functools import reduce

%matplotlib inline

import warnings

warnings.filterwarnings('ignore')

pd.options.display.float_format = "{:,.2f}".format

import yfinance as yf

ticker = 'BTC-USD'

start_date = '2020-01-01'

stock_price = yf.download(ticker, start=start_date)

stock_price["Date"] = stock_price.index

stock_price.tail()

Open High Low Close Adj Close Volume Date

Date

2024-09-01 58,969.80 59,062.07 57,217.82 57,325.49 57,325.49 24592449997 2024-09-01

2024-09-02 57,326.97 59,403.07 57,136.03 59,112.48 59,112.48 27036454524 2024-09-02

2024-09-03 59,106.19 59,815.06 57,425.17 57,431.02 57,431.02 26666961053 2024-09-03

2024-09-04 57,430.35 58,511.57 55,673.16 57,971.54 57,971.54 35627680312 2024-09-04

2024-09-05 57,969.75 58,280.16 56,441.49 56,816.75 56,816.75 31623784448 2024-09-05

stock_price = stock_price[['Date','Adj Close']]

stock_price.columns = ['ds', 'y']

stock_price.tail()

ds y

Date

2024-09-01 2024-09-01 57,325.49

2024-09-02 2024-09-02 59,112.48

2024-09-03 2024-09-03 57,431.02

2024-09-04 2024-09-04 57,971.54

2024-09-05 2024-09-05 56,816.75- Fitting the above stock price and making predictions for future dates

model = Prophet()

model.fit(stock_price)

future = model.make_future_dataframe(1095, freq='d')

future_boolean = future['ds'].map(lambda x : True if x.weekday() in range(0, 5) else False)

future = future[future_boolean]

future.tail()

ds

2798 2027-08-30

2799 2027-08-31

2800 2027-09-01

2801 2027-09-02

2802 2027-09-03

forecast = model.predict(future)

forecast.tail()

ds trend yhat_lower yhat_upper trend_lower trend_upper additive_terms additive_terms_lower additive_terms_upper weekly weekly_lower weekly_upper yearly yearly_lower yearly_upper multiplicative_terms multiplicative_terms_lower multiplicative_terms_upper yhat

1998 2027-08-30 186,397.72 17,078.78 342,504.45 25,330.76 349,736.48 -5,418.98 -5,418.98 -5,418.98 77.78 77.78 77.78 -5,496.76 -5,496.76 -5,496.76 0.00 0.00 0.00 180,978.73

1999 2027-08-31 186,503.42 18,938.28 343,364.67 25,153.02 350,048.12 -5,602.41 -5,602.41 -5,602.41 -32.66 -32.66 -32.66 -5,569.75 -5,569.75 -5,569.75 0.00 0.00 0.00 180,901.01

2000 2027-09-01 186,609.12 16,790.94 346,802.89 24,995.28 350,535.01 -5,574.97 -5,574.97 -5,574.97 64.88 64.88 64.88 -5,639.84 -5,639.84 -5,639.84 0.00 0.00 0.00 181,034.16

2001 2027-09-02 186,714.83 20,909.35 347,787.00 24,837.54 351,021.90 -5,751.63 -5,751.63 -5,751.63 -44.32 -44.32 -44.32 -5,707.31 -5,707.31 -5,707.31 0.00 0.00 0.00 180,963.20

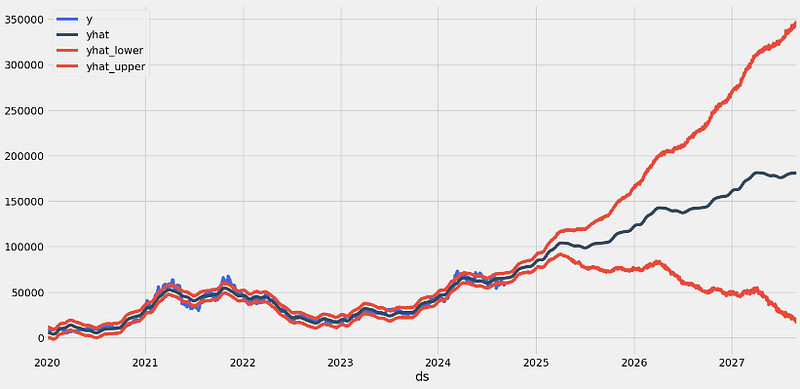

2002 2027-09-03 186,820.53 18,715.76 344,767.13 24,487.82 351,508.79 -5,793.51 -5,793.51 -5,793.51 -21.00 -21.00 -21.00 -5,772.52 -5,772.52 -5,772.52 0.00 0.00 0.00 181,027.02- Plotting the 3Y forecast with CI

model.plot(forecast);

- Plotting the key components: trend and seasonality

model.plot_components(forecast);

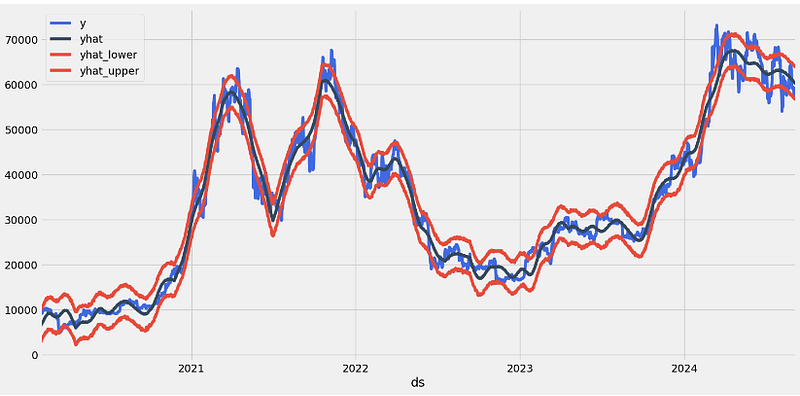

- Plotting the 3Y forecast in terms of yhat, yhat_lower, and yhat_upper

stock_price_forecast = forecast[['ds', 'yhat', 'yhat_lower', 'yhat_upper']]

df = pd.merge(stock_price, stock_price_forecast, on='ds', how='right')

df.set_index('ds').plot(figsize=(16,8), color=['royalblue', "#34495e", "#e74c3c", "#e74c3c"], grid=True);

- Splitting the date index [13] and making the Prophet forecast

stock_price['dayname'] = stock_price['ds'].dt.day_name()

stock_price['month'] = stock_price['ds'].dt.month

stock_price['year'] = stock_price['ds'].dt.year

stock_price['month/year'] = stock_price['month'].map(str) + '/' + stock_price['year'].map(str)

stock_price = pd.merge(stock_price,

stock_price['month/year'].drop_duplicates().reset_index(drop=True).reset_index(),

on='month/year',

how='left')

stock_price = stock_price.rename(columns={'index':'month/year_index'})

loop_list = stock_price['month/year'].unique().tolist()

max_num = len(loop_list) - 1

forecast_frames = []

for num, item in enumerate(loop_list):

if num == max_num:

pass

else:

df = stock_price.set_index('ds')[

stock_price[stock_price['month/year'] == loop_list[0]]['ds'].min():\

stock_price[stock_price['month/year'] == item]['ds'].max()]

df = df.reset_index()[['ds', 'y']]

model = Prophet()

model.fit(df)

future = stock_price[stock_price['month/year_index'] == (num + 1)][['ds']]

forecast = model.predict(future)

forecast_frames.append(forecast)

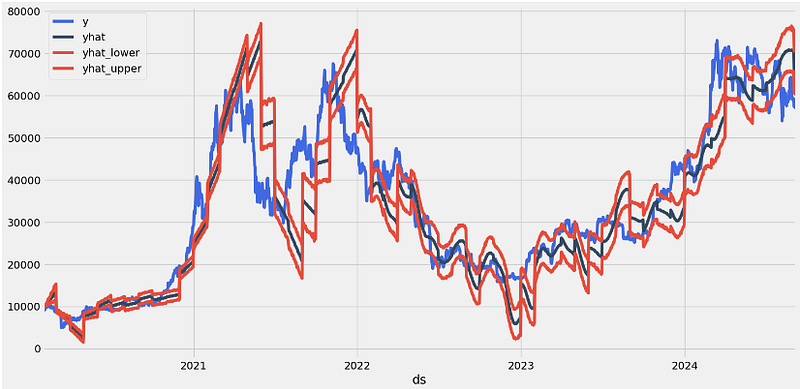

stock_price_forecast = reduce(lambda top, bottom: pd.concat([top, bottom], sort=False), forecast_frames)

stock_price_forecast = stock_price_forecast[['ds', 'yhat', 'yhat_lower', 'yhat_upper']]

df = pd.merge(stock_price[['ds','y', 'month/year_index']], stock_price_forecast, on='ds')

df['Percent Change'] = df['y'].pct_change()

df.set_index('ds')[['y', 'yhat', 'yhat_lower', 'yhat_upper']].plot(figsize=(16,8), color=['royalblue', "#34495e", "#e74c3c", "#e74c3c"], grid=True)

- Running the Prophet cross-validation QC diagnostics

from prophet.diagnostics import cross_validation

df_cv = cross_validation(model, initial='600 days', period='180 days', horizon = '365 days')

from prophet.diagnostics import performance_metrics

df_p = performance_metrics(df_cv)

df_p.head()

horizon mse rmse mae mape mdape smape coverage

0 37 days 37,926,228.96 6,158.43 5,078.86 0.16 0.14 0.17 0.41

1 38 days 39,286,966.57 6,267.93 5,205.29 0.16 0.14 0.17 0.40

2 39 days 40,986,172.18 6,402.04 5,344.08 0.16 0.15 0.18 0.39

3 40 days 42,315,522.99 6,505.04 5,454.70 0.17 0.15 0.18 0.38

4 41 days 43,420,106.74 6,589.39 5,544.55 0.17 0.15 0.18 0.37

from prophet.plot import plot_cross_validation_metric

fig = plot_cross_validation_metric(df_cv, metric='rmse')

fig = plot_cross_validation_metric(df_cv, metric='mape')

fig = plot_cross_validation_metric(df_cv, metric='mae')

- Running HPO [17] by defining the hyperparameter grid

from sklearn.metrics import mean_absolute_error

param_grid = {

'seasonality_mode': ['additive', 'multiplicative'],

'changepoint_prior_scale': [0.01, 0.1, 1, 10],

'seasonality_prior_scale': [0.01, 0.1, 1, 10],

}

# Helper function to evaluate the model

def evaluate_model(model, metric_func):

df_cv = cross_validation(model, initial='1125 days', period='180 days', horizon='365 days')

return metric_func(df_cv['y'], df_cv['yhat'])

# Grid search

best_params = {}

best_score = float('inf')

for mode in param_grid['seasonality_mode']:

for cps in param_grid['changepoint_prior_scale']:

for sps in param_grid['seasonality_prior_scale']:

# Create a model with the current hyperparameters

m = Prophet(seasonality_mode=mode, changepoint_prior_scale=cps, seasonality_prior_scale=sps)

m.fit(stock_price)

# Evaluate the model using Mean Absolute Error (MAE)

score = evaluate_model(m, mean_absolute_error)

# Update best parameters if necessary

if score < best_score:

best_score = score

best_params = {

'seasonality_mode': mode,

'changepoint_prior_scale': cps,

'seasonality_prior_scale': sps

}

print(best_params)

print(best_score)

{'seasonality_mode': 'multiplicative', 'changepoint_prior_scale': 1, 'seasonality_prior_scale': 0.01}

13078.117877655675- Defining the HPO-updated Prophet model and making 1Y predictions

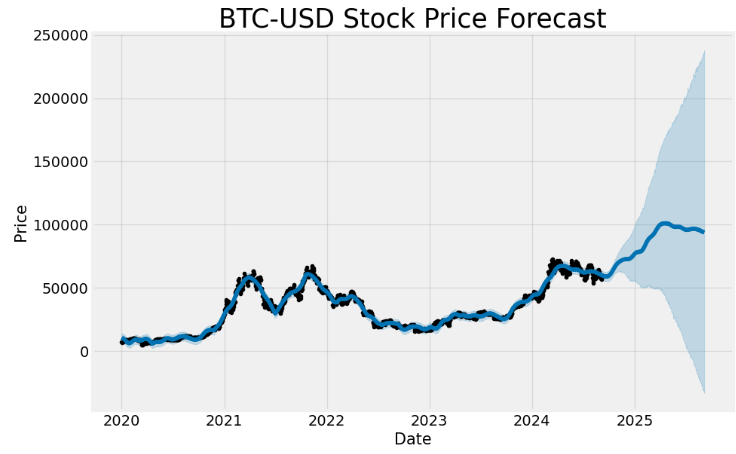

#Model with best parameters

m_best = Prophet(seasonality_mode= 'additive', changepoint_prior_scale = 1, seasonality_prior_scale = 0.01)

m_best.fit(stock_price)

#dataframe for the forecast(with 365 days)

future_best = m_best.make_future_dataframe(periods=365)

forecast_best = m_best.predict(future_best)

#plot the graph with the forecast data

fig1 = m.plot(forecast_best)

ax = fig1.gca()

ax.set_title("BTC-USD Stock Price Forecast", size=25)

ax.set_xlabel("Date", size=15)

ax.set_ylabel("Price", size=15)

- Performing cross-validation QC

# Perform cross-validation

from sklearn.metrics import mean_squared_error

df_cv = cross_validation(m_best, initial='1125 days', period='180 days', horizon='365 days')

# Calculate performance metrics

df_metrics = performance_metrics(df_cv)

# Calculate MAE, MSE, and RMSE

mae = mean_absolute_error(df_cv['y'], df_cv['yhat'])

mse = mean_squared_error(df_cv['y'], df_cv['yhat'])

rmse = np.sqrt(mse)

print(f'Mean Absolute Error: {mae:.2f}')

print(f'Mean Squared Error: {mse:.2f}')

print(f'Root Mean Squared Error: {rmse:.2f}')

Mean Absolute Error: 13879.24

Mean Squared Error: 279497823.66

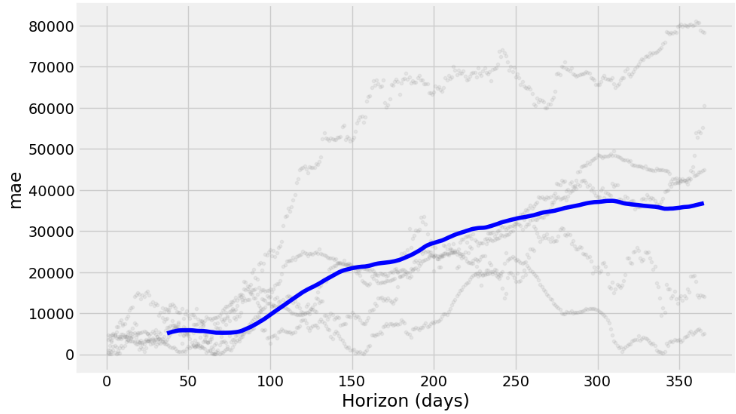

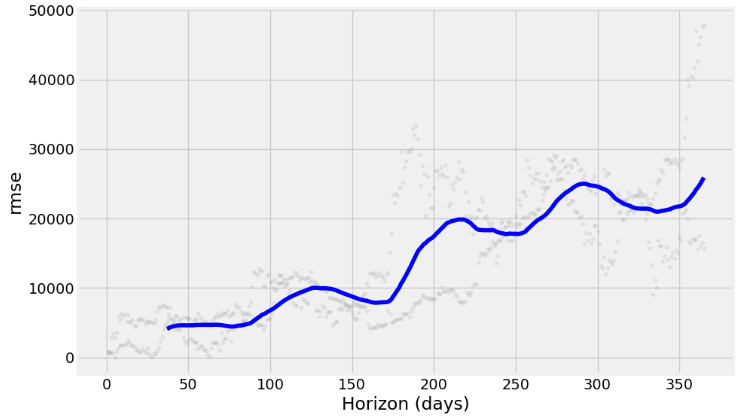

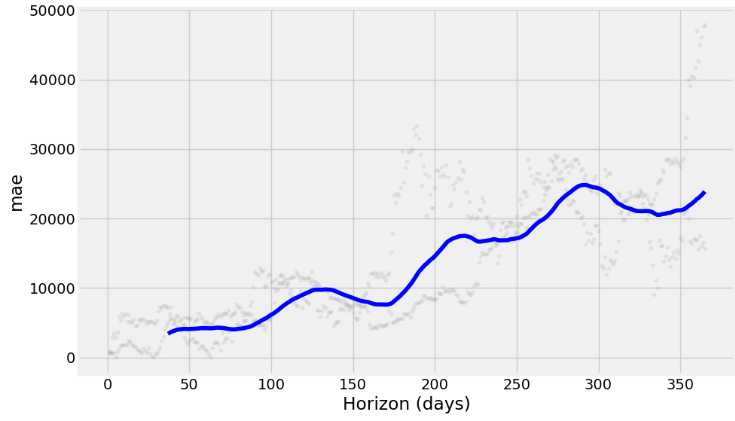

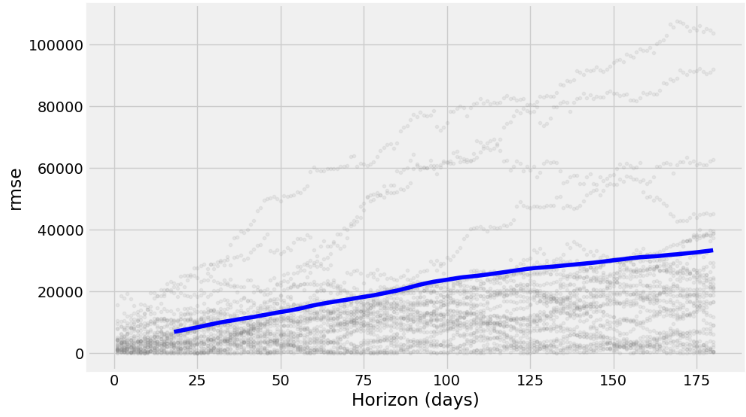

Root Mean Squared Error: 16718.19- Plotting RMSE, MAPE, and MAE vs Horizon (days)

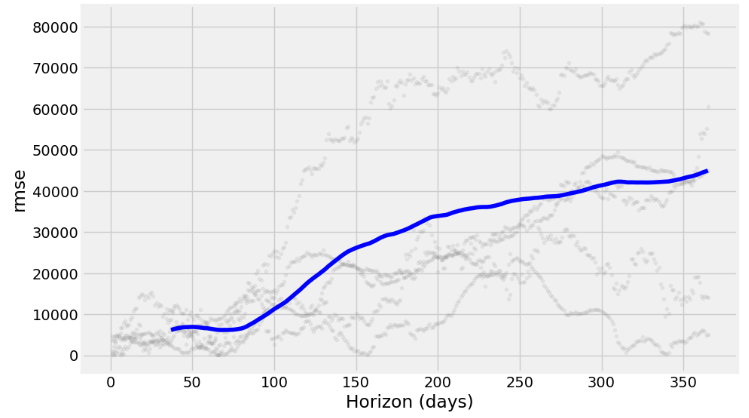

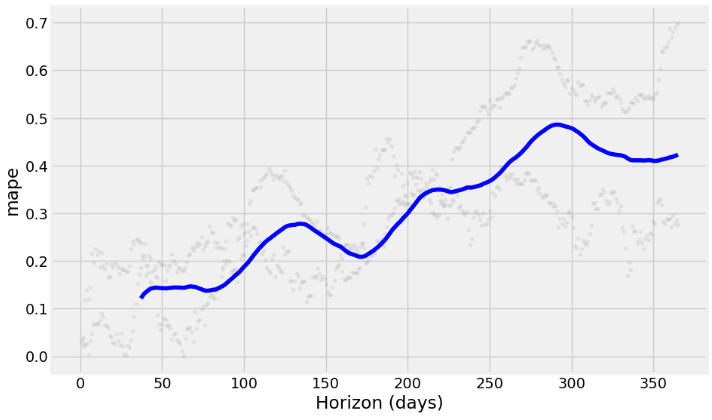

from prophet.plot import plot_cross_validation_metric

df_cv = cross_validation(m_best, initial='1125 days', period='180 days', horizon='365 days')

fig = plot_cross_validation_metric(df_cv, metric='rmse')

fig = plot_cross_validation_metric(df_cv, metric='mape')

fig = plot_cross_validation_metric(df_cv, metric='mae')

- Splitting the date index [13] and making the Prophet in-sample forecast

loop_list = stock_price['month/year'].unique().tolist()

max_num = len(loop_list) - 1

forecast_frames = []

for num, item in enumerate(loop_list):

if num == max_num:

pass

else:

df = stock_price.set_index('ds')[

stock_price[stock_price['month/year'] == loop_list[0]]['ds'].min():\

stock_price[stock_price['month/year'] == item]['ds'].max()]

df = df.reset_index()[['ds', 'y']]

future = stock_price[stock_price['month/year_index'] == (num + 1)][['ds']]

forecast = m_best.predict(future)

forecast_frames.append(forecast)

stock_price_forecast1 = reduce(lambda top, bottom: pd.concat([top, bottom], sort=False), forecast_frames)

stock_price_forecast1 = stock_price_forecast1[['ds', 'yhat', 'yhat_lower', 'yhat_upper']]

df1 = pd.merge(stock_price[['ds','y', 'month/year_index']], stock_price_forecast1, on='ds')

df1['Percent Change'] = df1['y'].pct_change()

df1.set_index('ds')[['y', 'yhat', 'yhat_lower', 'yhat_upper']].plot(figsize=(16,8), color=['royalblue', "#34495e", "#e74c3c", "#e74c3c"], grid=True)

Prophet Algo-Trading Strategies [13]

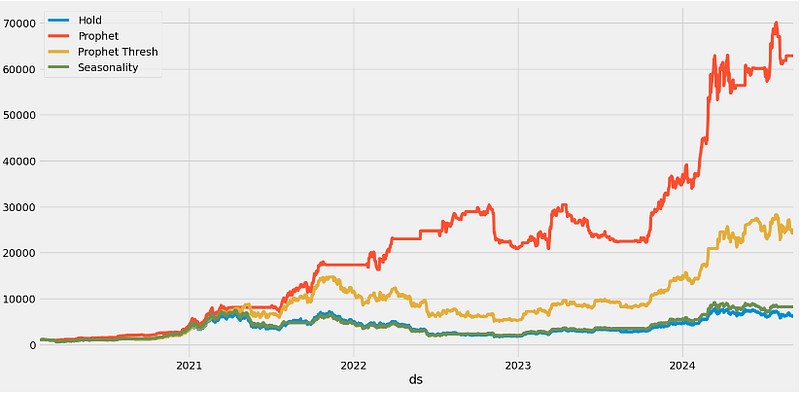

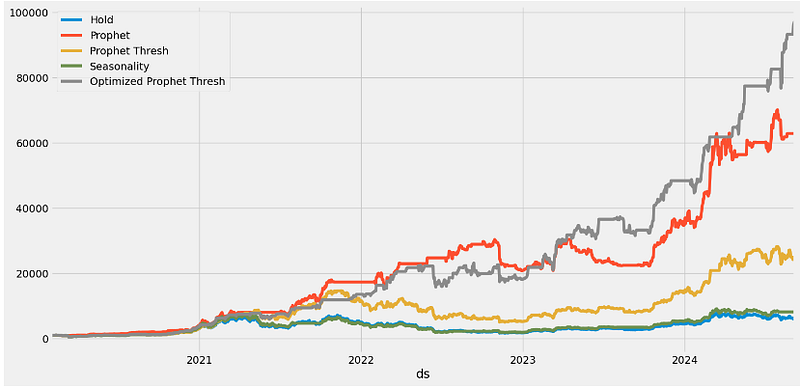

- Backtesting the BTC-USD HPO-updated Prophet algo-trading strategy

#Trading Algorithms

df=df1.copy()

df['Hold'] = (df['Percent Change'] + 1).cumprod()

df['Prophet'] = ((df['yhat'].shift(-1) > df['yhat']).shift(1) * (df['Percent Change']) + 1).cumprod()

df['Prophet Thresh'] = ((df['y'] < df['yhat_upper']).shift(1)* (df['Percent Change']) + 1).cumprod()

df['Seasonality'] = ((~df['ds'].dt.month.isin([8,9])).shift(1) * (df['Percent Change']) + 1).cumprod()

(df.dropna().set_index('ds')[['Hold', 'Prophet', 'Prophet Thresh','Seasonality']] * 1000).plot(figsize=(16,8), grid=True)

print(f"Hold = {df['Hold'].iloc[-1]*1000:,.0f}")

print(f"Prophet = {df['Prophet'].iloc[-1]*1000:,.0f}")

print(f"Prophet Thresh = {df['Prophet Thresh'].iloc[-1]*1000:,.0f}")

print(f"Seasonality = {df['Seasonality'].iloc[-1]*1000:,.0f}")

Hold = 6,049

Prophet = 62,849

Prophet Thresh = 23,986

Seasonality = 8,195

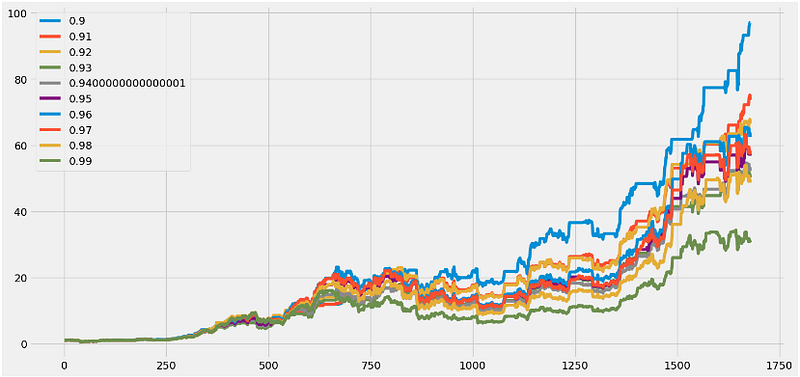

- Optimizing the Prophet threshold value in the range 0.9–1.0

performance = {}

for x in np.linspace(.9,.99,10):

y = ((df['y'] < df['yhat_upper']*x).shift(1)* (df['Percent Change']) + 1).cumprod()

performance[x] = y

best_yhat = pd.DataFrame(performance).max().idxmax()

pd.DataFrame(performance).plot(figsize=(16,8), grid=True);

f'Best Yhat = {best_yhat:,.2f}'

'Best Yhat = 0.90'

- Backtesting the BTC-USD HPO-updated Prophet algo-trading strategy with the optimized threshold value Best Yhat = 0.90

df['Optimized Prophet Thresh'] = ((df['y'] < df['yhat_upper'] * best_yhat).shift(1) *

(df['Percent Change']) + 1).cumprod()

(df.dropna().set_index('ds')[['Hold', 'Prophet', 'Prophet Thresh',

'Seasonality', 'Optimized Prophet Thresh']] * 1000).plot(figsize=(16,8), grid=True)

print(f"Hold = {df['Hold'].iloc[-1]*1000:,.0f}")

print(f"Prophet = {df['Prophet'].iloc[-1]*1000:,.0f}")

print(f"Prophet Thresh = {df['Prophet Thresh'].iloc[-1]*1000:,.0f}")

print(f"Seasonality = {df['Seasonality'].iloc[-1]*1000:,.0f}")

print(f"Optimized Prophet Thresh = {df['Optimized Prophet Thresh'].iloc[-1]*1000:,.0f}")

Hold = 6,049

Prophet = 62,849

Prophet Thresh = 23,986

Seasonality = 8,195

Optimized Prophet Thresh = 97,000

Prophet Plotly with Changepoints

- Making 1Y Prophet predictions with changepoints and Plotly visuals

stock_price.tail()

ds y dayname month year month/year month/year_index

1705 2024-09-01 57,325.49 Sunday 9 2024 9/2024 56

1706 2024-09-02 59,112.48 Monday 9 2024 9/2024 56

1707 2024-09-03 57,431.02 Tuesday 9 2024 9/2024 56

1708 2024-09-04 57,971.54 Wednesday 9 2024 9/2024 56

1709 2024-09-05 56,816.75 Thursday 9 2024 9/2024 56

mydf=stock_price[['ds','y']]

mm = Prophet()

mm.fit(mydf)

future = mm.make_future_dataframe(periods=365)

forecast = mm.predict(future)

from prophet.plot import plot_plotly

plot_plotly(mm, forecast)

- Plotting Prophet predictions with changepoints in Plotly

from prophet.plot import plot_plotly

plot_plotly(mm, forecast, changepoints=True)

- Plotting Prophet 1Y forecast: key components in Plotly

from prophet.plot import plot_components_plotly

### Using plotly

plot_components_plotly(m, forecast)

- Running cross-validation QC

from prophet.diagnostics import cross_validation

df_cv = cross_validation(mm, initial='540 days', period='31 days', horizon = '180 days')

from prophet.diagnostics import performance_metrics

df_p = performance_metrics(df_cv)

df_p.head(2)

horizon mse rmse mae mape mdape smape coverage

0 18 days 48,591,983.30 6,970.80 5,096.63 0.15 0.12 0.16 0.52

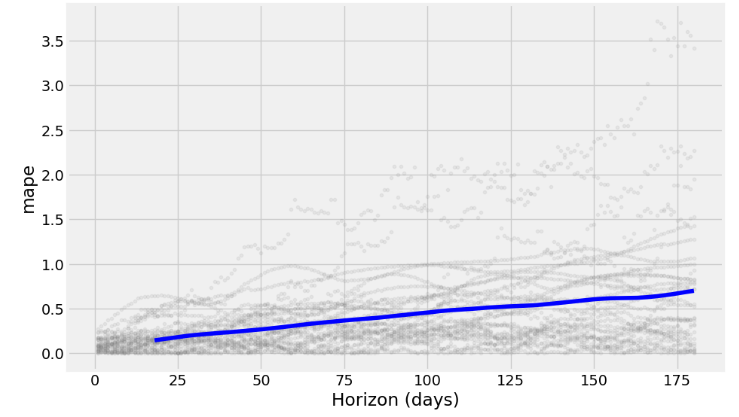

1 19 days 51,427,421.78 7,171.29 5,260.73 0.15 0.12 0.16 0.50- Plotting MAPE vs Horizon (days)

from prophet.plot import plot_cross_validation_metric

fig = plot_cross_validation_metric(df_cv, metric='mape')

- Plotting MAE vs Horizon (days)

fig = plot_cross_validation_metric(df_cv, metric='mae')

- Plotting RMSE vs Horizon (days)

fig = plot_cross_validation_metric(df_cv, metric='rmse')

Inferences:

- Prophet with the Box-Cox transformation and a cap or upper limit for the forecast yields the 1Y prediction with relatively narrow CI and can capture non-linearity in the trend of the data

- Adding the monthly/quarterly seasonality and US events reveals a fairly strong yearly seasonality and a somewhat increased frequency content with reasonable CI of the out-of-sample predictions.

- 1Y forecast (2022–2027 time interval): combining the Box-Cox transformation and HPO reduces MAE about 20 times.

- 2020–2027 Time Interval: Splitting the date index improves the in-sample goodness-of-fit of the Prophet forecast.

- The HPO-updated Prophet model and 1Y predictions yield

Mean Absolute Error: 13879.24

Mean Squared Error: 279497823.66

Root Mean Squared Error: 16718.19- Backtesting of algo-trading strategies result in the following expected returns

Hold = 6,049

Prophet = 62,849

Prophet Thresh = 23,986

Seasonality = 8,195

Optimized Prophet Thresh = 97,000- Prophet provides an interpretable decomposition of the data that is observed or forecasted into trend and multi-seasonal components.

- Different useful plotting options are available in Prophet: forecasts in terms of yhat/yhat_lower/yhat_upper, cross-validation metrics, Plotly plots with changepoints, etc.

NVDA Price Prediction using Auto-ARIMA, Supervised ML & Technical Indicators

- It is well known that ML can be used to forecast stock values in the future or find lucrative trading opportunities on the stock market [25].

- This section aims to design, train, and evaluate ML-powered NVDA price prediction algorithms in the context of quantitative finance.

- Specifically, our objective is to demonstrate how Auto-ARIMA and popular supervised ML algorithms with technical indicators [18, 19] can add value to algorithmic trading strategies in a practical yet comprehensive way.

NVDA EDA

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd() - Importing the necessary Python libraries

#Import Libraries

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

plt.style.use("fivethirtyeight")

%matplotlib inline

# For reading stock data from yahoo

import yfinance as yf

# For time stamps

from datetime import datetime

from math import sqrt

from math import sqrt

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import MinMaxScaler

#ignore the warnings

import warnings

warnings.filterwarnings('ignore')- Reading the input stock data from 2020–01–01 to 2024–09–06

symbols = ['NVDA']

start_date = '2020-01-01'

data = yf.download(symbols, start=start_date)

data.tail()

Open High Low Close Adj Close Volume

Date

2024-08-30 119.529999 121.750000 117.220001 119.370003 119.370003 333751600

2024-09-03 116.010002 116.209999 107.290001 108.000000 108.000000 474040800

2024-09-04 105.410004 113.269997 104.120003 106.209999 106.209999 372470300

2024-09-05 104.989998 109.650002 104.760002 107.209999 107.209999 306850700

2024-09-06 108.040001 108.150002 100.949997 102.830002 102.830002 411712100- Plotting the Close price history

def plot_close_val(data_frame, column, stock):

plt.figure(figsize=(10,6))

plt.title(column + ' Price History for ' + stock )

plt.plot(data_frame[column])

plt.xlabel('Date', fontsize=18)

plt.ylabel(column + ' Price USD ($) for ' + stock, fontsize=18)

plt.show()

#Test the function

plot_close_val(data, 'Close', 'NVDA')

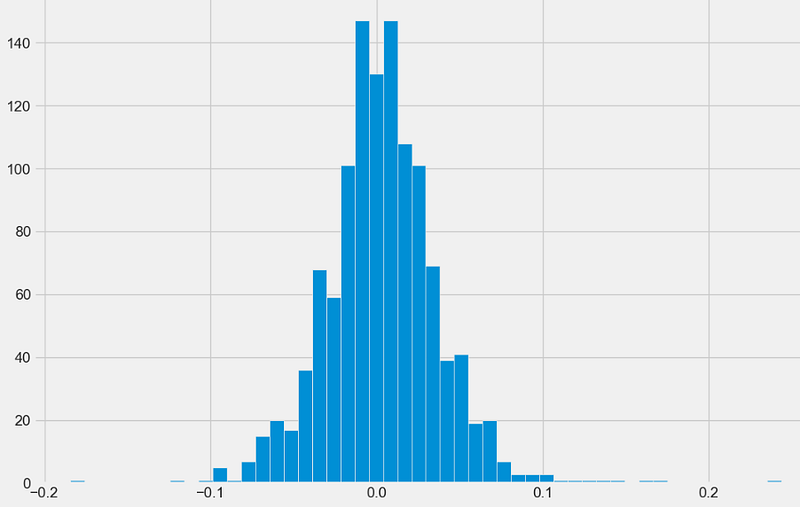

- Plotting the histogram of daily returns

#Basic EDA

daily_close_px = data[['Close']]

# Calculate the daily percentage change for `daily_close_px`

daily_pct_change = daily_close_px.pct_change()

# Plot the distributions

daily_pct_change.hist(bins=50, sharex=True, figsize=(12,8))

# Show the resulting plot

plt.show()

- Plotting the rolling STD of Close price with min_periods = 75

# Define the minumum of periods to consider

min_periods = 75

# Calculate the volatility

vol = daily_pct_change.rolling(min_periods).std() * np.sqrt(min_periods)

# Plot the volatility

vol.plot(figsize=(10, 6))

# Show the plot

plt.show()

- Plotting the NVDA candlestick chart

import plotly.graph_objects as go

data=data.reset_index()

fig = go.Figure(data=go.Ohlc(x=data['Date'],

open=data['Open'],

high=data['High'],

low=data['Low'],

close=data['Close']))

fig.show()

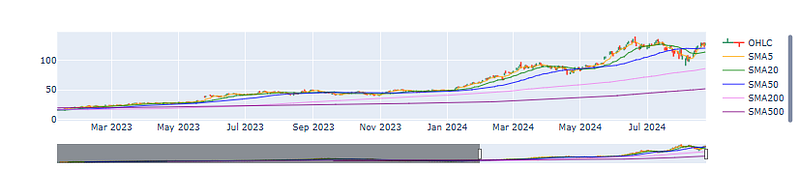

- Plotting the NVDA candlestick chart with top 5 simple moving averages (SMA 5, 20, 50, 200, 500)

data=data.reset_index()

data['SMA5'] = data.Close.rolling(5).mean()

data['SMA20'] = data.Close.rolling(20).mean()

data['SMA50'] = data.Close.rolling(50).mean()

data['SMA200'] = data.Close.rolling(200).mean()

data['SMA500'] = data.Close.rolling(500).mean()

fig = go.Figure(data=[go.Ohlc(x=data['Date'],open=data['Open'],high=data['High'],low=data['Low'],close=data['Close'], name = "OHLC"),

go.Scatter(x=data.Date, y=data.SMA5, line=dict(color='orange', width=1), name="SMA5"),

go.Scatter(x=data.Date, y=data.SMA20, line=dict(color='green', width=1), name="SMA20"),

go.Scatter(x=data.Date, y=data.SMA50, line=dict(color='blue', width=1), name="SMA50"),

go.Scatter(x=data.Date, y=data.SMA200, line=dict(color='violet', width=1), name="SMA200"),

go.Scatter(x=data.Date, y=data.SMA500, line=dict(color='purple', width=1), name="SMA500")])

fig.show()

Auto-ARIMA Modeling [18]

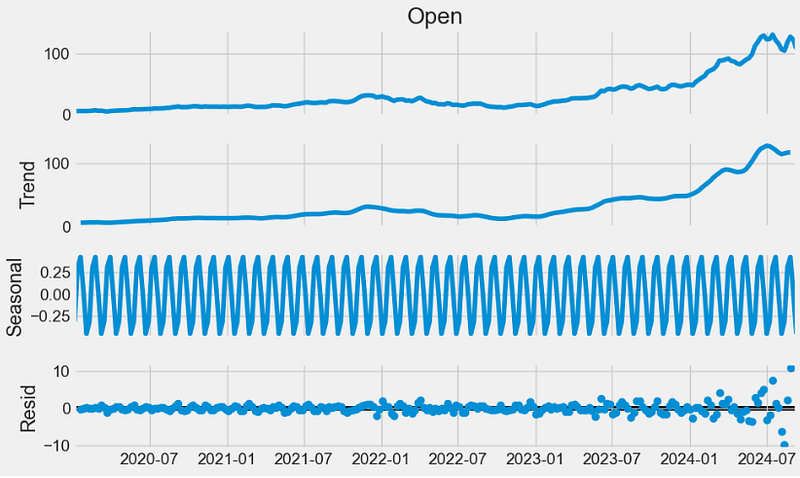

- Preparing the W-MON resampled Open price for statistical modeling

x = data['Open'].resample('W-MON').mean()

x.head()

Date

2020-01-06 5.884750

2020-01-13 6.084000

2020-01-20 6.221687

2020-01-27 6.225150

2020-02-03 6.057600

Freq: W-MON, Name: Open, dtype: float64

#visualize time series of open price

x.plot(figsize = (10,6))

plt.title("Opening Price")

plt.show()

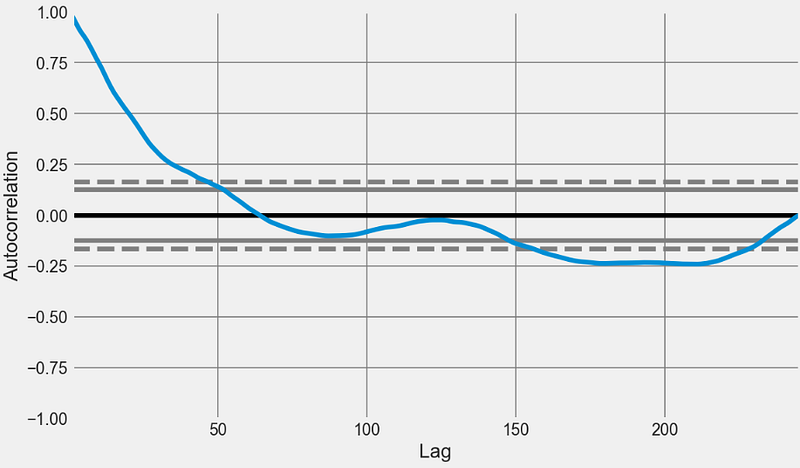

- Using statsmodels to perform the additive trend-seasonality decomposition

- Plotting the autocorrelation function

from pandas.plotting import autocorrelation_plot

from statsmodels.tsa.stattools import adfuller, kpss

plt.rcParams.update({'figure.figsize':(10,6), 'figure.dpi':120})

autocorrelation_plot(x.tolist())

plt.grid(color='grey')

- Finding an optimal parameter combination for Seasonal ARIMA without enforcing stationarity of time series

import warnings

import itertools

p = d = q = range(0, 2)

pdq = list(itertools.product(p, d, q))

seasonal_pdq = [(x[0], x[1], x[2], 12) for x in list(itertools.product(p, d, q))]

print('Examples of parameter combinations for Seasonal ARIMA...')

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[1]))

print('SARIMAX: {} x {}'.format(pdq[1], seasonal_pdq[2]))

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[3]))

print('SARIMAX: {} x {}'.format(pdq[2], seasonal_pdq[4]))

Examples of parameter combinations for Seasonal ARIMA...

SARIMAX: (0, 0, 1) x (0, 0, 1, 12)

SARIMAX: (0, 0, 1) x (0, 1, 0, 12)

SARIMAX: (0, 1, 0) x (0, 1, 1, 12)

SARIMAX: (0, 1, 0) x (1, 0, 0, 12)

#selection of parameter

for param in pdq:

for param_seasonal in seasonal_pdq:

try:

model = sm.tsa.statespace.SARIMAX(x, order = param, seasonal_order = param_seasonal, enforce_stationarity = False,

enforce_invertibility = False)

results = model.fit()

print('ARIMA{}x{}12 - AIC:{}'.format(param, param_seasonal, results.aic))

except:

continue

ARIMA(0, 0, 0)x(0, 0, 0, 12)12 - AIC:2542.1221453228754

ARIMA(0, 0, 0)x(0, 0, 1, 12)12 - AIC:2205.432369780864

ARIMA(0, 0, 0)x(0, 1, 0, 12)12 - AIC:1826.8913110661877

ARIMA(0, 0, 0)x(0, 1, 1, 12)12 - AIC:1663.0856888581307

ARIMA(0, 0, 0)x(1, 0, 0, 12)12 - AIC:1696.5162260417578

ARIMA(0, 0, 0)x(1, 0, 1, 12)12 - AIC:1678.9637064852432

ARIMA(0, 0, 0)x(1, 1, 0, 12)12 - AIC:1651.058267917132

ARIMA(0, 0, 0)x(1, 1, 1, 12)12 - AIC:1645.9164183133007

ARIMA(0, 0, 1)x(0, 0, 0, 12)12 - AIC:2210.7423692662937

ARIMA(0, 0, 1)x(0, 0, 1, 12)12 - AIC:2203.0913037562423

ARIMA(0, 0, 1)x(0, 1, 0, 12)12 - AIC:1537.3048930586983

ARIMA(0, 0, 1)x(0, 1, 1, 12)12 - AIC:1418.7522928794192

ARIMA(0, 0, 1)x(1, 0, 0, 12)12 - AIC:1451.0683837824945

ARIMA(0, 0, 1)x(1, 0, 1, 12)12 - AIC:1441.0113195138251

ARIMA(0, 0, 1)x(1, 1, 0, 12)12 - AIC:1423.0785411142224

ARIMA(0, 0, 1)x(1, 1, 1, 12)12 - AIC:1413.039982679135

ARIMA(0, 1, 0)x(0, 0, 0, 12)12 - AIC:1178.8567047336762

ARIMA(0, 1, 0)x(0, 0, 1, 12)12 - AIC:1126.9339211643753

ARIMA(0, 1, 0)x(0, 1, 0, 12)12 - AIC:1187.5326512870083

ARIMA(0, 1, 0)x(0, 1, 1, 12)12 - AIC:1092.3408895368445

ARIMA(0, 1, 0)x(1, 0, 0, 12)12 - AIC:1130.2055135648625

ARIMA(0, 1, 0)x(1, 0, 1, 12)12 - AIC:1128.3271690575802

ARIMA(0, 1, 0)x(1, 1, 0, 12)12 - AIC:1115.2722911771843

ARIMA(0, 1, 0)x(1, 1, 1, 12)12 - AIC:1094.3407571819212

ARIMA(0, 1, 1)x(0, 0, 0, 12)12 - AIC:1118.7406393983258

ARIMA(0, 1, 1)x(0, 0, 1, 12)12 - AIC:1075.1495479384398

ARIMA(0, 1, 1)x(0, 1, 0, 12)12 - AIC:1148.2924924067215

ARIMA(0, 1, 1)x(0, 1, 1, 12)12 - AIC:1042.0275297094452

ARIMA(0, 1, 1)x(1, 0, 0, 12)12 - AIC:1082.485805851485

ARIMA(0, 1, 1)x(1, 0, 1, 12)12 - AIC:1076.9580429373332

ARIMA(0, 1, 1)x(1, 1, 0, 12)12 - AIC:1071.8775311784716

ARIMA(0, 1, 1)x(1, 1, 1, 12)12 - AIC:1047.8120669921664

ARIMA(1, 0, 0)x(0, 0, 0, 12)12 - AIC:1177.3490080789097

ARIMA(1, 0, 0)x(0, 0, 1, 12)12 - AIC:1129.7779287250664

ARIMA(1, 0, 0)x(0, 1, 0, 12)12 - AIC:1190.9377862978463

ARIMA(1, 0, 0)x(0, 1, 1, 12)12 - AIC:1144.8316199958667

ARIMA(1, 0, 0)x(1, 0, 0, 12)12 - AIC:1129.7478625579813

ARIMA(1, 0, 0)x(1, 0, 1, 12)12 - AIC:1131.6506276933846

ARIMA(1, 0, 0)x(1, 1, 0, 12)12 - AIC:1115.394003615538

ARIMA(1, 0, 0)x(1, 1, 1, 12)12 - AIC:1100.4886461555423

ARIMA(1, 0, 1)x(0, 0, 0, 12)12 - AIC:1122.4801077667785

ARIMA(1, 0, 1)x(0, 0, 1, 12)12 - AIC:1079.7842226451762

ARIMA(1, 0, 1)x(0, 1, 0, 12)12 - AIC:1150.1791820520716

ARIMA(1, 0, 1)x(0, 1, 1, 12)12 - AIC:1105.7635992016349

ARIMA(1, 0, 1)x(1, 0, 0, 12)12 - AIC:1083.3652726613996

ARIMA(1, 0, 1)x(1, 0, 1, 12)12 - AIC:1081.7276621247142

ARIMA(1, 0, 1)x(1, 1, 0, 12)12 - AIC:1070.9370636396125

ARIMA(1, 0, 1)x(1, 1, 1, 12)12 - AIC:1053.3290101344387

ARIMA(1, 1, 0)x(0, 0, 0, 12)12 - AIC:1133.7146929946548

ARIMA(1, 1, 0)x(0, 0, 1, 12)12 - AIC:1087.802074373154

ARIMA(1, 1, 0)x(0, 1, 0, 12)12 - AIC:1146.0764102812118

ARIMA(1, 1, 0)x(0, 1, 1, 12)12 - AIC:1052.828342174158

ARIMA(1, 1, 0)x(1, 0, 0, 12)12 - AIC:1087.058860181081

ARIMA(1, 1, 0)x(1, 0, 1, 12)12 - AIC:1088.966632778937

ARIMA(1, 1, 0)x(1, 1, 0, 12)12 - AIC:1064.0612581801736

ARIMA(1, 1, 0)x(1, 1, 1, 12)12 - AIC:1056.9832355544775

ARIMA(1, 1, 1)x(0, 0, 0, 12)12 - AIC:1119.9105858927223

ARIMA(1, 1, 1)x(0, 0, 1, 12)12 - AIC:1076.203213223961

ARIMA(1, 1, 1)x(0, 1, 0, 12)12 - AIC:1143.4263033487089

ARIMA(1, 1, 1)x(0, 1, 1, 12)12 - AIC:1042.8217518955812

ARIMA(1, 1, 1)x(1, 0, 0, 12)12 - AIC:1079.7670530248097

ARIMA(1, 1, 1)x(1, 0, 1, 12)12 - AIC:1077.960982378333

ARIMA(1, 1, 1)x(1, 1, 0, 12)12 - AIC:1063.9499867272968

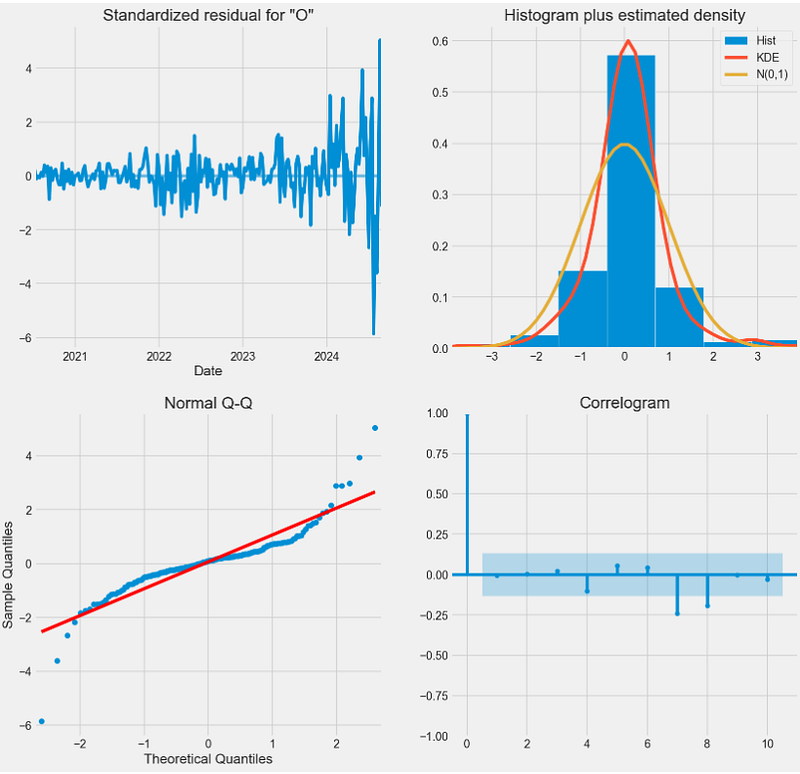

ARIMA(1, 1, 1)x(1, 1, 1, 12)12 - AIC:1048.2564843107295- Fitting the ARIMA model and plotting the QC validation diagnostics

#fitting model

model = sm.tsa.statespace.SARIMAX(x, order = (1, 1, 1), seasonal_order = (1, 1, 1, 12), enforce_stationarity = False,

enforce_invertibility = False)

result = model.fit()

print(results.summary().tables[1])

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

ar.L1 0.1853 0.063 2.932 0.003 0.061 0.309

ma.L1 0.3696 0.072 5.111 0.000 0.228 0.511

ar.S.L12 -0.1825 0.117 -1.565 0.118 -0.411 0.046

ma.S.L12 -0.6436 0.101 -6.399 0.000 -0.841 -0.446

sigma2 6.6759 0.276 24.223 0.000 6.136 7.216

==============================================================================

result.plot_diagnostics(figsize = (15, 15))

plt.show()

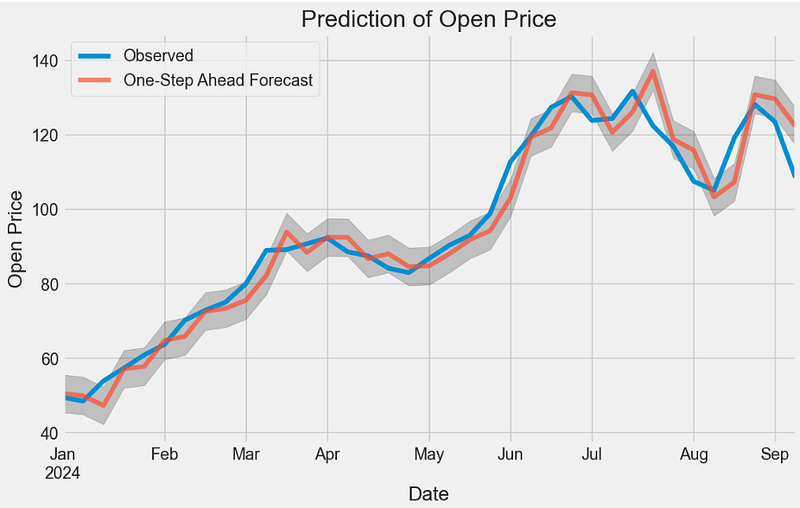

- One-step ahead ARIMA prediction of NVDA Open price in 2024

y_pred = result.get_prediction(start = pd.to_datetime('2024-01-01'), dynamic = False)

#visualize prediction of open price

pred_ci = y_pred.conf_int()

ax = x['2024':].plot(label = 'Observed')

y_pred.predicted_mean.plot(ax = ax, label = 'One-Step Ahead Forecast', alpha = .7, figsize = (10, 6))

ax.fill_between(pred_ci.index, pred_ci.iloc[:, 0], pred_ci.iloc[:, 1], color = 'k', alpha = .2)

plt.title("Prediction of Open Price")

ax.set_xlabel('Date')

ax.set_ylabel('Open Price')

plt.legend()

plt.show()

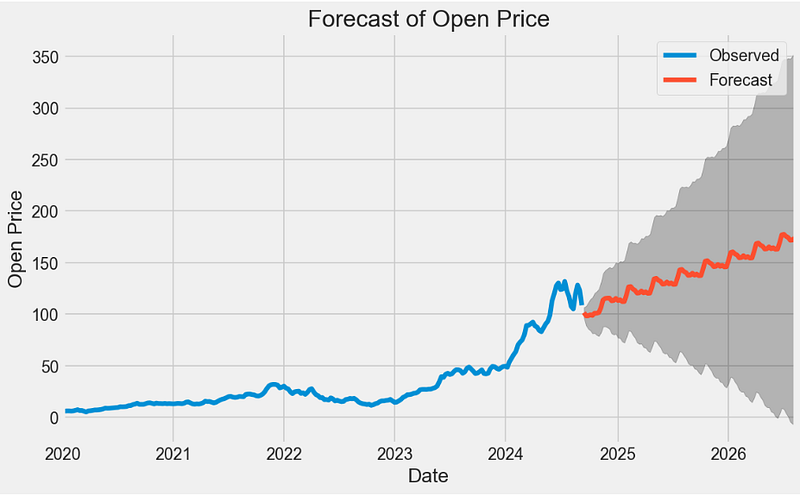

- Out-of-sample ARIMA prediction of NVDA Open price

#prediction of forecast

y_forecasted = y_pred.predicted_mean

y_truth = x['2024-03-01':]

mse = ((y_forecasted - y_truth) ** 2).mean()

print('The Mean Squared Error of our forecasts is {}'.format(round(mse, 2)))

print('The Root Mean Squared Error of our forecasts is {}'.format(round(np.sqrt(mse), 2)))

The Mean Squared Error of our forecasts is 37.26

The Root Mean Squared Error of our forecasts is 6.1

#visualize prediction of forecast

pred_uc = results.get_forecast(steps = 100)

pred_ci = pred_uc.conf_int()

ax = x.plot(label = 'Observed', figsize = (10,6))

pred_uc.predicted_mean.plot(ax = ax, label = 'Forecast')

ax.fill_between(pred_ci.index, pred_ci.iloc[:, 0], pred_ci.iloc[:, 1], color = 'k', alpha = .25)

plt.title("Forecast of Open Price")

ax.set_xlabel('Date')

ax.set_ylabel('Open Price')

plt.legend()

plt.show()

- Statistical testing of the above ARIMA forecast

# ADF Test

result = adfuller(x, autolag = 'AIC')

print(f'ADF Statistic: {result[0]}')

print(f'p-value: {result[1]}')

for key, value in result[4].items():

print('Critial Values:')

print(f' {key}, {value}')

# KPSS Test

result = kpss(x, regression = 'c')

print('\nKPSS Statistic: %f' % result[0])

print('p-value: %f' % result[1])

for key, value in result[3].items():

print('Critial Values:')

print(f' {key}, {value}')

# KPSS Test

result = kpss(x, regression = 'c')

print('\nKPSS Statistic: %f' % result[0])

print('p-value: %f' % result[1])

for key, value in result[3].items():

print('Critial Values:')

print(f' {key}, {value}')

ADF Statistic: 0.00829081706485982

p-value: 0.959212383816871

Critial Values:

1%, -3.4592326027153493

Critial Values:

5%, -2.8742454699025872

Critial Values:

10%, -2.5735414688888465

KPSS Statistic: 1.515224

p-value: 0.010000

Critial Values:

10%, 0.347

Critial Values:

5%, 0.463

Critial Values:

2.5%, 0.574

Critial Values:

1%, 0.739- The p-value obtained by the ADF test should be less than the significance level 0.05 in order to reject the null hypothesis. It appears that the ARIMA prediction is not stationary since p=0.959.

- The KPSS test yields p=0.01. We can see from the p-value and critical values that we should reject the null of stationarity because the p-value is less than 5%.

Backtesting Logistic Regression with Technical Indicators [18]

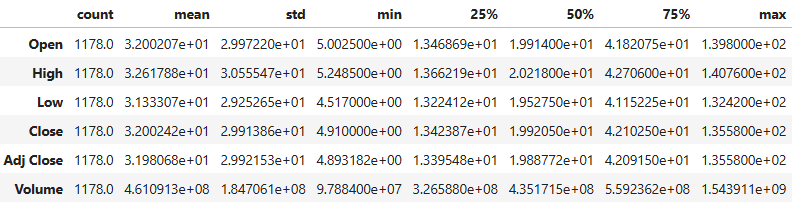

- Copying the input NVDA data

df=data.copy() df.describe().T

- Calculating the RSI, MACD, SMA, and EMA indicators with default parameters

# Calculate RSI (Relative Strength Index)

def calculate_rsi(data, window=14):

delta = data["Close"].diff(1)

gain = delta.where(delta > 0, 0)

loss = -delta.where(delta < 0, 0)

avg_gain = gain.rolling(window=window, min_periods=1).mean()

avg_loss = loss.rolling(window=window, min_periods=1).mean()

rs = avg_gain / avg_loss

rsi = 100 - (100 / (1 + rs))

return rsi

df["RSI"] = calculate_rsi(df)

#Calculate MACD & Signal_Line

def calculate_macd(data, short_window=12, long_window=26):

ema_short = data["Close"].ewm(span=short_window, min_periods=1, adjust=False).mean()

ema_long = data["Close"].ewm(span=long_window, min_periods=1, adjust=False).mean()

macd = ema_short - ema_long

signal_line = macd.ewm(span=9, min_periods=1, adjust=False).mean()

return macd, signal_line

df["MACD"], df["Signal_Line"] = calculate_macd(df)

#Calculate SMA

def calculate_sma(data, window=20):

sma = data["Close"].rolling(window=window, min_periods=1).mean()

return sma

df["SMA"] = calculate_sma(df)

#Calculate EMA

def calculate_ema(data, window=24):

ema = data["Close"].ewm(span=window, min_periods=1,

adjust=False).mean()

return ema

df["EMA"] = calculate_ema(df)

#Calculate the Trading Signal

df["Signal"] = np.where(

(df["RSI"] > 30) & (df["MACD"] > df["Signal_Line"])

& (df["Close"] > df["SMA"]) & (df["Close"] > df["EMA"]),1,0)

df = df.dropna()- Splitting the data into training and testing sets, creating and training a Logistic Regression (LR) model, generating predictions on the test data, calculating ROC curve and AUC, backtesting the trading strategy, calculate cumulative returns, and plotting ML results

def build_model():

# Split the data into training and testing sets

train_size = int(0.8 * len(X))

X_train, X_test, y_train, y_test = (

X[:train_size],

X[train_size:],

y[:train_size],

y[train_size:],

)

# Create and train a Logistic Regression model

model = LogisticRegression()

model.fit(X_train, y_train)

# Generate predictions on the test data

y_pred = model.predict(X_test)

# Calculate accuracy

accuracy = accuracy_score(y_test, y_pred)

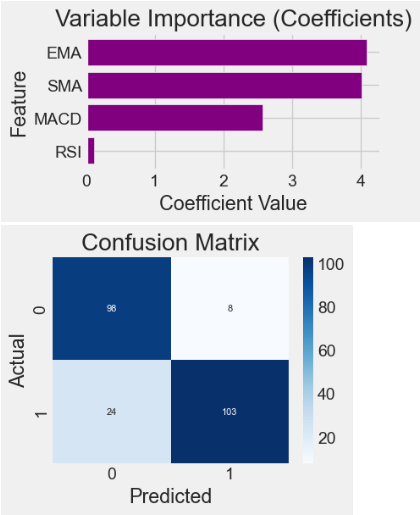

plt.figure(figsize=(4, 2))

coef_values = list(abs(model.coef_[0]))

feature_names = ["RSI", "MACD", "SMA", "EMA"]

plt.barh(feature_names, sorted(coef_values, reverse=False),

color="purple")

plt.xlabel("Coefficient Value")

plt.ylabel("Feature")

plt.title("Variable Importance (Coefficients)")

#plt.show()

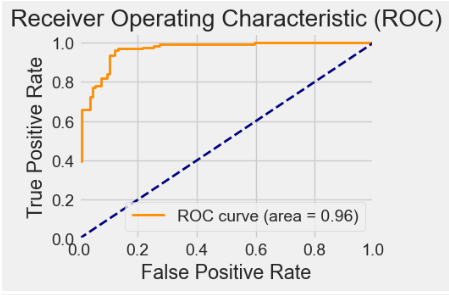

# Calculate ROC curve and AUC

y_prob = model.predict_proba(X_test)[:, 1]

fpr, tpr, _ = roc_curve(y_test, y_prob)

roc_auc = auc(fpr, tpr)

# Calculate and plot the confusion matrix

cm = confusion_matrix(y_test, y_pred)

plt.figure(figsize=(4, 3))

sns.heatmap(cm, annot=True, fmt="d", cmap="Blues", annot_kws={"size": 8})

plt.xlabel("Predicted")

plt.ylabel("Actual")

plt.title("Confusion Matrix")

plt.show()

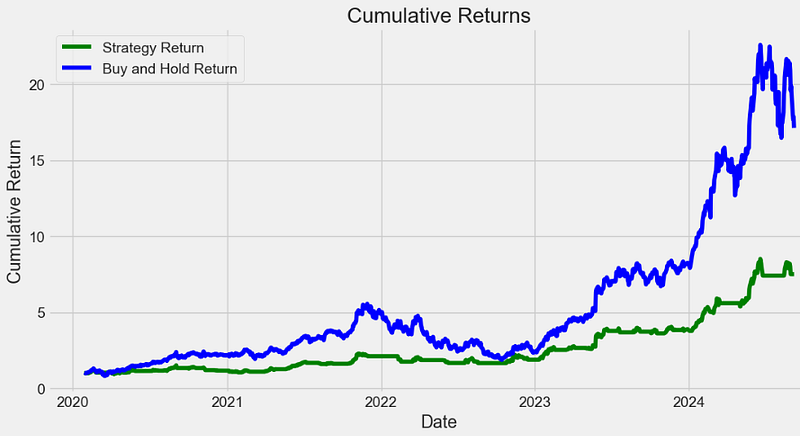

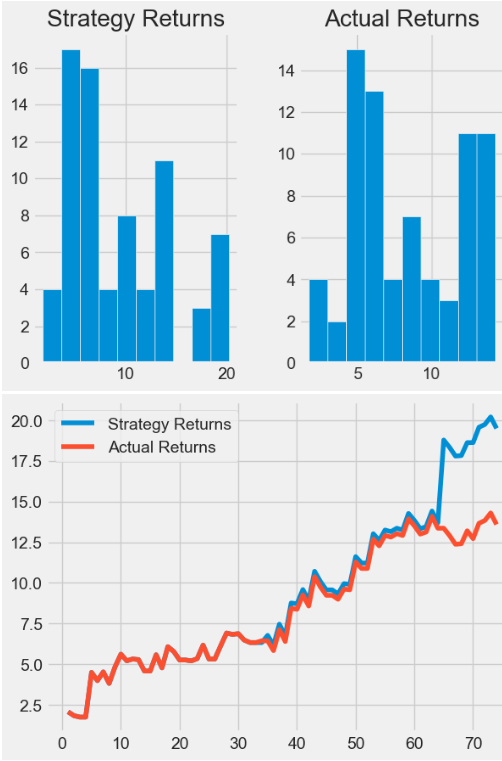

# Backtesting the trading strategy

df["Strategy_Return"] = df["Close"].pct_change() * df["Signal"].shift(1)

df["Buy_Hold_Return"] = df["Close"].pct_change()

# Calculate cumulative returns

df["Cumulative_Strategy_Return"] = (1 + df["Strategy_Return"]).cumprod()

df["Cumulative_Buy_Hold_Return"] = (1 + df["Buy_Hold_Return"]).cumprod()

# Plot the stock's closing price, RSI, MACD, SMA, and EMA

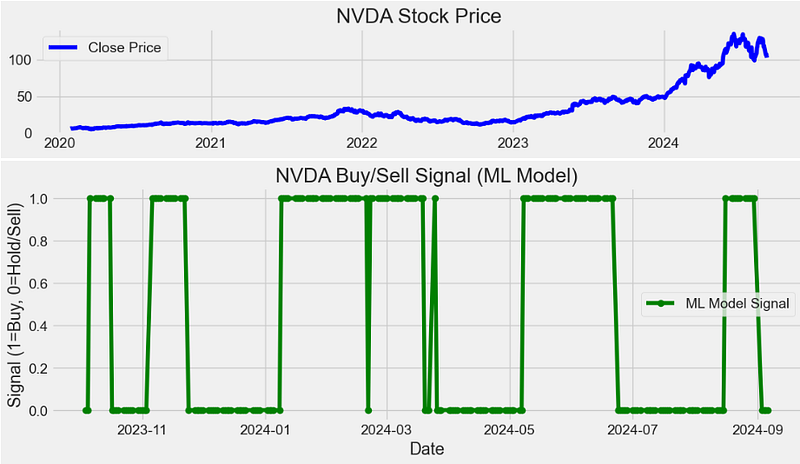

plt.figure(figsize=(12, 6))

plt.subplot(3, 1, 1)

plt.plot(df["Close"], label="Close Price", color="blue")

plt.title(f"{stock_symbol} Stock Price")

plt.legend()

# Plot the buy/sell signals generated by the machine learning model

plt.figure(figsize=(12, 4))

plt.plot(

df.index[train_size:], y_pred, label="ML Model Signal", color="green", marker="o"

)

plt.title(f"{stock_symbol} Buy/Sell Signal (ML Model)")

plt.xlabel("Date")

plt.ylabel("Signal (1=Buy, 0=Hold/Sell)")

plt.legend()

# Plot ROC curve

plt.figure(figsize=(4, 3))

plt.plot(

fpr,

tpr,

color="darkorange",

lw=2,

label="ROC curve (area = {:.2f})".format(roc_auc),

)

plt.plot([0, 1], [0, 1], color="navy", lw=2, linestyle="--")

plt.xlim([0.0, 1.0])

plt.ylim([0.0, 1.05])

plt.xlabel("False Positive Rate")

plt.ylabel("True Positive Rate")

plt.title("Receiver Operating Characteristic (ROC)")

plt.legend(loc="lower right")

# Plot cumulative returns of the strategy and buy-and-hold

plt.figure(figsize=(12, 6))

plt.plot(

df.index, df["Cumulative_Strategy_Return"], label="Strategy Return", color="green"

)

plt.plot(

df.index,

df["Cumulative_Buy_Hold_Return"],

label="Buy and Hold Return",

color="blue",

)

plt.title("Cumulative Returns")

plt.xlabel("Date")

plt.ylabel("Cumulative Return")

plt.legend()

# Display accuracy

print(f"Model Accuracy: {accuracy * 100:.2f}%")

plt.show()

X = df[["RSI", "MACD", "SMA", "EMA"]].values

y = df["Signal"].values

# call the function

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import accuracy_score

from sklearn.metrics import roc_curve

from sklearn.metrics import auc

from sklearn.metrics import confusion_matrix

stock_symbol='NVDA'

build_model()

Model Accuracy: 86.27%

- It is clear that the proposed strategy underperforms about 10% of “buy-and-hold” in terms of expected returns.

Multiple Supervised ML Classification Algorithms with Technical Indicators [19]

- Importing the necessary Python libraries and reading the input NVDA stock data from 2022–01–01 to 2024–04–18

# Load packages

import numpy as np

import pandas as pd

from pandas import read_csv, set_option

from pandas.plotting import scatter_matrix

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.tree import DecisionTreeClassifier

from sklearn.neighbors import KNeighborsClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.preprocessing import StandardScaler

from sklearn.naive_bayes import GaussianNB

from sklearn.svm import SVC

from sklearn.neural_network import MLPClassifier

from sklearn.pipeline import Pipeline

from sklearn.discriminant_analysis import LinearDiscriminantAnalysis

from sklearn.model_selection import GridSearchCV, train_test_split, KFold, cross_val_score

from sklearn.metrics import confusion_matrix, classification_report, accuracy_score

from sklearn.ensemble import GradientBoostingClassifier, AdaBoostClassifier, ExtraTreesClassifier, RandomForestClassifier

import pandas as pd

import numpy as np

symbols = ['NVDA']

start_date = '2022-01-01'

end_date = '2024-04-18'

dataset = yf.download(symbols, start=start_date, end=end_date)- Computing the following technical indicators with trading signals, excluding columns that are not needed for our prediction while dropping NaN values if any

# Create short simple moving average over a short 10-day-window

dataset['short_mvg'] = dataset['Close'].rolling(window=10, min_periods=1, center=False).mean()

# Create long simple moving average over a long 60-day-window

dataset['long_mvg'] = dataset['Close'].rolling(window=60, min_periods=1, center=False).mean()

# Create the signals

dataset['signal'] = np.where(dataset['short_mvg'] > dataset['long_mvg'], 1.0, 0.0)

#calculation of exponential moving average

def EMA(df, n):

EMA = pd.Series(df['Close'].ewm(span=n, min_periods=n).mean(), name='EMA_' + str(n))

return EMA

dataset['EMA10'] = EMA(dataset, 10)

dataset['EMA30'] = EMA(dataset, 30)

dataset['EMA200'] = EMA(dataset, 200)

dataset.head()

#calculation of rate of change

def ROC(df, n):

M = df.diff(n - 1)

N = df.shift(n - 1)

ROC = pd.Series(((M / N) * 100), name = 'ROC_' + str(n))

return ROC

dataset['ROC10'] = ROC(dataset['Close'], 10)

dataset['ROC30'] = ROC(dataset['Close'], 30)

#Calculation of price momentum

def MOM(df, n):

MOM = pd.Series(df.diff(n), name='Momentum_' + str(n))

return MOM

dataset['MOM10'] = MOM(dataset['Close'], 10)

dataset['MOM30'] = MOM(dataset['Close'], 30)

#calculation of relative strength index

def RSI(series, period):

delta = series.diff().dropna()

u = delta * 0

d = u.copy()

u[delta > 0] = delta[delta > 0]

d[delta < 0] = -delta[delta < 0]

u[u.index[period-1]] = np.mean( u[:period] ) #first value is sum of avg gains

u = u.drop(u.index[:(period-1)])

d[d.index[period-1]] = np.mean( d[:period] ) #first value is sum of avg losses

d = d.drop(d.index[:(period-1)])

rs = u.ewm(com=period-1, adjust=False).mean() / \

d.ewm(com=period-1, adjust=False).mean()

return 100 - 100 / (1 + rs)

dataset['RSI10'] = RSI(dataset['Close'], 10)

dataset['RSI30'] = RSI(dataset['Close'], 30)

dataset['RSI200'] = RSI(dataset['Close'], 200)

#calculation of stochastic osillator.

def STOK(close, low, high, n):

STOK = ((close - low.rolling(n).min()) / (high.rolling(n).max() - low.rolling(n).min())) * 100

return STOK

def STOD(close, low, high, n):

STOK = ((close - low.rolling(n).min()) / (high.rolling(n).max() - low.rolling(n).min())) * 100

STOD = STOK.rolling(3).mean()

return STOD

dataset['%K10'] = STOK(dataset['Close'], dataset['Low'], dataset['High'], 10)

dataset['%D10'] = STOD(dataset['Close'], dataset['Low'], dataset['High'], 10)

dataset['%K30'] = STOK(dataset['Close'], dataset['Low'], dataset['High'], 30)

dataset['%D30'] = STOD(dataset['Close'], dataset['Low'], dataset['High'], 30)

dataset['%K200'] = STOK(dataset['Close'], dataset['Low'], dataset['High'], 200)

dataset['%D200'] = STOD(dataset['Close'], dataset['Low'], dataset['High'], 200)

#Calculation of moving average

def MA(df, n):

MA = pd.Series(df['Close'].rolling(n, min_periods=n).mean(), name='MA_' + str(n))

return MA

dataset['MA21'] = MA(dataset, 10)

dataset['MA63'] = MA(dataset, 30)

dataset['MA252'] = MA(dataset, 200)

#excluding columns that are not needed for our prediction.

dataset=dataset.drop(['High','Low','Open','short_mvg','long_mvg'], axis=1)

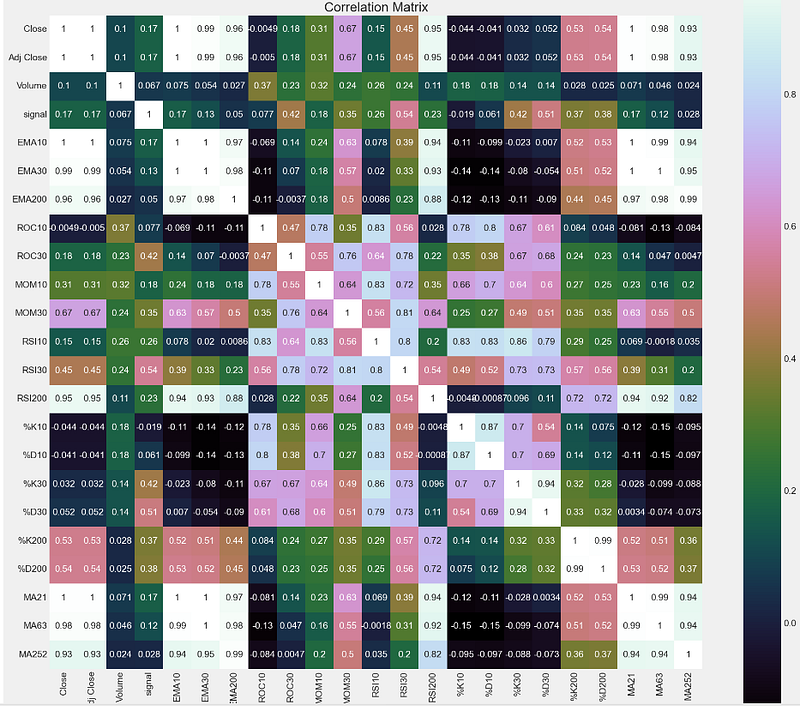

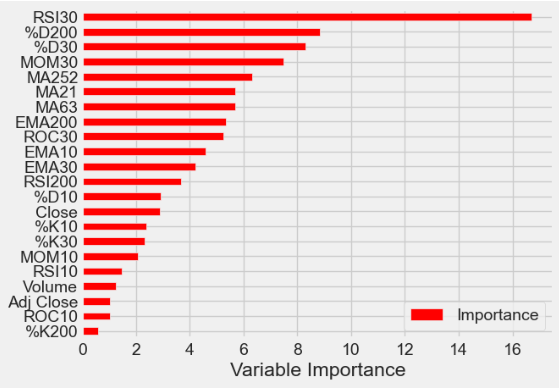

dataset = dataset.dropna(axis=0)- Plotting the correlation heatmap

# correlation

correlation = dataset.corr()

plt.figure(figsize=(20,20))

plt.title('Correlation Matrix')

sns.heatmap(correlation, vmax=1, square=True,annot=True,cmap='cubehelix')

- Splitting the input dataset into training/validation sets with validation_size = 0.2

# split out validation dataset for the end

subset_dataset= dataset.iloc[-100000:]

Y= subset_dataset["signal"]

X = subset_dataset.loc[:, dataset.columns != 'signal']

validation_size = 0.2

seed = 1

X_train, X_validation, Y_train, Y_validation = train_test_split(X, Y, test_size=validation_size, random_state=1)- Training and comparing multiple supervised ML classification algorithms

# test options for classification

num_folds = 10

seed = 7

scoring = 'accuracy'

# spot check the algorithms

models = []

models.append(('LR', LogisticRegression(n_jobs=-1)))

models.append(('LDA', LinearDiscriminantAnalysis()))

models.append(('KNN', KNeighborsClassifier()))

models.append(('CART', DecisionTreeClassifier()))

models.append(('NB', GaussianNB()))

# Neural Network

models.append(('NN', MLPClassifier()))

# Ensable Models

# Boosting methods

models.append(('AB', AdaBoostClassifier()))

models.append(('GBM', GradientBoostingClassifier()))

# Bagging methods

models.append(('RF', RandomForestClassifier(n_jobs=-1)))

results = []

names = []

for name, model in models:

kfold = KFold(n_splits=num_folds)

cv_results = cross_val_score(model, X_train, Y_train, cv=kfold, scoring=scoring)

results.append(cv_results)

names.append(name)

msg = "%s: %f (%f)" % (name, cv_results.mean(), cv_results.std())

print(msg)

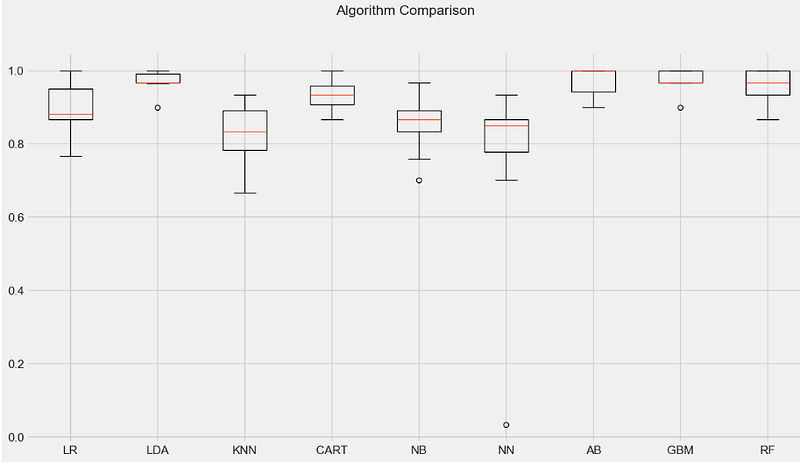

LR: 0.889655 (0.069958)

LDA: 0.969885 (0.027705)

KNN: 0.822299 (0.084645)

CART: 0.933103 (0.036521)

NB: 0.852529 (0.074317)

NN: 0.759195 (0.250235)

AB: 0.973333 (0.035901)

GBM: 0.973333 (0.029059)

RF: 0.956667 (0.047258)

# compare algorithms

fig = plt.figure()

fig.suptitle('Algorithm Comparison')

ax = fig.add_subplot(111)

plt.boxplot(results)

ax.set_xticklabels(names)

fig.set_size_inches(15,8)

plt.show()

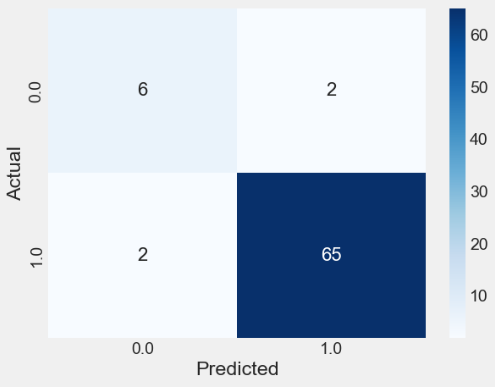

- Selecting the Random Forest (RF) classifier to perform Grid Search HPO

# Grid Search: Random Forest Classifier

'''

n_estimators : int (default=100)

The number of boosting stages to perform.

Gradient boosting is fairly robust to over-fitting so a large number usually results in better performance.

max_depth : integer, optional (default=3)

maximum depth of the individual regression estimators.

The maximum depth limits the number of nodes in the tree.

Tune this parameter for best performance; the best value depends on the interaction of the input variables

criterion : string, optional (default=”gini”)

The function to measure the quality of a split.

Supported criteria are “gini” for the Gini impurity and “entropy” for the information gain.

'''

scaler = StandardScaler().fit(X_train)

rescaledX = scaler.transform(X_train)

n_estimators = [20,80]

max_depth= [5,10]

criterion = ["gini","entropy"]

param_grid = dict(n_estimators=n_estimators, max_depth=max_depth, criterion = criterion )

model = RandomForestClassifier(n_jobs=-1)

kfold = KFold(n_splits=num_folds)

grid = GridSearchCV(estimator=model, param_grid=param_grid, scoring=scoring, cv=kfold)

grid_result = grid.fit(rescaledX, Y_train)

#Print Results

print("Best: %f using %s" % (grid_result.best_score_, grid_result.best_params_))

means = grid_result.cv_results_['mean_test_score']

stds = grid_result.cv_results_['std_test_score']

params = grid_result.cv_results_['params']

ranks = grid_result.cv_results_['rank_test_score']

for mean, stdev, param, rank in zip(means, stds, params, ranks):

print("#%d %f (%f) with: %r" % (rank, mean, stdev, param))

Best: 0.970000 using {'criterion': 'entropy', 'max_depth': 10, 'n_estimators': 20}

#6 0.953333 (0.054160) with: {'criterion': 'gini', 'max_depth': 5, 'n_estimators': 20}

#6 0.953333 (0.054160) with: {'criterion': 'gini', 'max_depth': 5, 'n_estimators': 80}

#5 0.956667 (0.053852) with: {'criterion': 'gini', 'max_depth': 10, 'n_estimators': 20}

#4 0.960000 (0.044222) with: {'criterion': 'gini', 'max_depth': 10, 'n_estimators': 80}

#8 0.950000 (0.050000) with: {'criterion': 'entropy', 'max_depth': 5, 'n_estimators': 20}

#2 0.963333 (0.043333) with: {'criterion': 'entropy', 'max_depth': 5, 'n_estimators': 80}

#1 0.970000 (0.031447) with: {'criterion': 'entropy', 'max_depth': 10, 'n_estimators': 20}

#2 0.963333 (0.043333) with: {'criterion': 'entropy', 'max_depth': 10, 'n_estimators': 80}

# prepare model

model = RandomForestClassifier(criterion='entropy', n_estimators=20,max_depth=10,n_jobs=-1) # rbf is default kernel

#model = GaussianNB()

model.fit(X_train, Y_train)

RandomForestClassifier:

RandomForestClassifier(criterion='entropy', max_depth=10, n_estimators=20,

n_jobs=-1)

# estimate accuracy on validation set

predictions = model.predict(X_validation)

print(accuracy_score(Y_validation, predictions))

print(confusion_matrix(Y_validation, predictions))

print(classification_report(Y_validation, predictions))

0.9466666666666667

[[ 6 2]