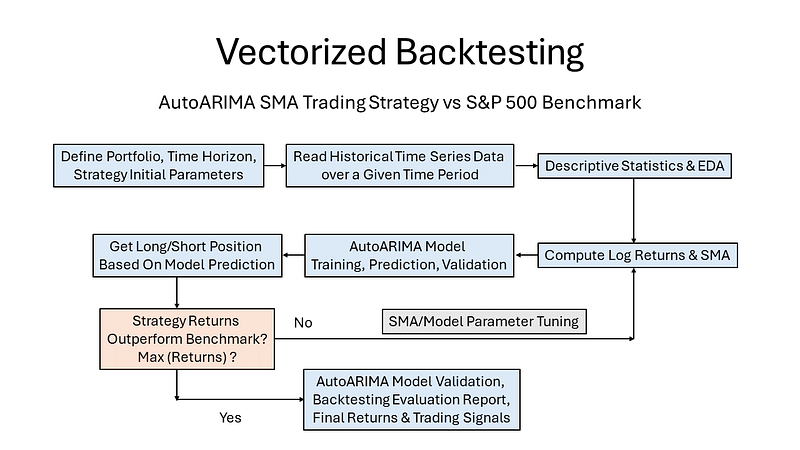

Vectorized Backtesting & Parameter Tuning of AutoARIMA SMA Strategy: BTC-Tech vs S&P 500

- This post is about the vectorized backtesting of simple moving averages (SMA) based strategies with different lengths.

- The objective is to find an optimal set of parameters by maximizing portfolio returns while outperforming the S&P 500.

- Following the ML vectorized backtesting idea, our project aims to devise stock trading strategies beyond ad hoc price forecasts.

- Specifically, the AutoARIMA model will be adopted to predict SMA trading decisions directly. We’ll provide ML SMA predictions for the optimum set of parameters by fitting the ML model to the training set.

- In the sequel, we’ll use the EODHD SMA algorithm to backtest the expected returns of BTC-USD combined with top 3 tech stocks (NVDA, AMD, and MSFT).

- The entire workflow consists of the following steps (cf. the flowchart below):

- Define our portfolio, time horizon, and strategy initial parameters

- Read historical time series data using yfinance over a specific time period

- Run the Pandas Exploratory Data Analysis (EDA) and examine the descriptive summary statistics.

- Compute Log Returns and SMA.

- Perform pmdarima AutoARIMA model training, prediction, and validation.

- Comparing Returns per Stock using ARIMA forecast.

- Comparing SPY vs ARIMA Overall Portfolio Returns (OPR).

- If OPR(SPY) > OPR(ARIMA), then go to step 4 and update both the SMA length and AutoARIMA parameters (i.e. days_to_train and days_to_predict).

- Output the full backtesting evaluation report with relevant plots.

Let’s delve into the specifics of this Python data science project.

Basic Settings, Imports & Installations

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd() - Importing/installing necessary Python libraries

!pip install pmdarima, yfinance, datetime, sklearn, tqdm, plotly,seaborn

import pandas as pd

import numpy as np

from pmdarima.arima import AutoARIMA

import plotly.express as px

import plotly.graph_objects as go

from tqdm.notebook import tqdm

from sklearn.metrics import mean_squared_error

from datetime import date, timedelta

import yfinance as yf

import seaborn as sns

#ignore the warnings

import warnings

warnings.filterwarnings('ignore')Input Historical Time Series Data

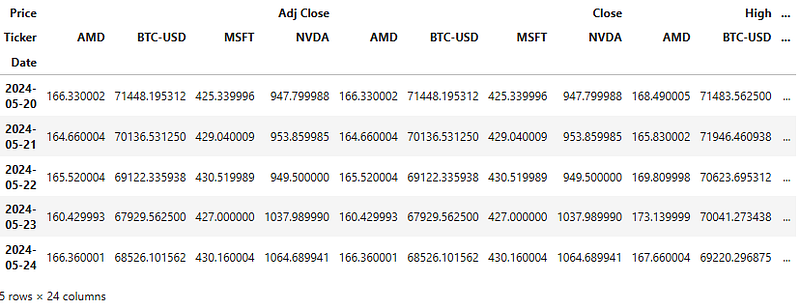

- Reading the input stock data

# Getting the time horizon

years = (date.today() - timedelta(weeks=260)).strftime("%Y-%m-%d")

# Stocks to analyze

stocks = ['NVDA', 'BTC-USD', 'AMD', 'MSFT']

# Getting the data for multiple stocks

df = yf.download(stocks, start=years).dropna()

# Storing the dataframes in a dictionary

stock_df = {}

for col in set(df.columns.get_level_values(0)):

# Assigning the data for each stock in the dictionary

stock_df[col] = df[col]- General data info

df.shape

(1254, 24)

df.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1254 entries, 2019-06-04 to 2024-05-24

Data columns (total 24 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 (Adj Close, AMD) 1254 non-null float64

1 (Adj Close, BTC-USD) 1254 non-null float64

2 (Adj Close, MSFT) 1254 non-null float64

3 (Adj Close, NVDA) 1254 non-null float64

4 (Close, AMD) 1254 non-null float64

5 (Close, BTC-USD) 1254 non-null float64

6 (Close, MSFT) 1254 non-null float64

7 (Close, NVDA) 1254 non-null float64

8 (High, AMD) 1254 non-null float64

9 (High, BTC-USD) 1254 non-null float64

10 (High, MSFT) 1254 non-null float64

11 (High, NVDA) 1254 non-null float64

12 (Low, AMD) 1254 non-null float64

13 (Low, BTC-USD) 1254 non-null float64

14 (Low, MSFT) 1254 non-null float64

15 (Low, NVDA) 1254 non-null float64

16 (Open, AMD) 1254 non-null float64

17 (Open, BTC-USD) 1254 non-null float64

18 (Open, MSFT) 1254 non-null float64

19 (Open, NVDA) 1254 non-null float64

20 (Volume, AMD) 1254 non-null float64

21 (Volume, BTC-USD) 1254 non-null int64

22 (Volume, MSFT) 1254 non-null float64

23 (Volume, NVDA) 1254 non-null float64

dtypes: float64(23), int64(1)

memory usage: 244.9 KB

df.tail()

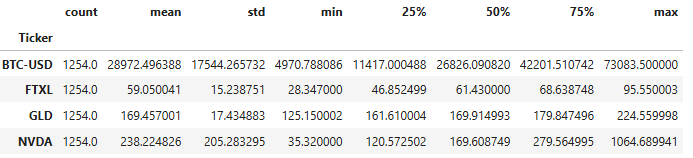

Descriptive Summary Statistics

- Examining descriptive summary statistics of the Close price

df['Close'].describe().T

- Analyzing standard deviation (std) of Close

df['Close'].std()

Ticker

AMD 37.437793

BTC-USD 17544.265732

MSFT 76.597961

NVDA 205.283295

dtype: float64- Standard deviation is the statistical measure of market volatility, measuring how widely prices are dispersed from the average price. If prices trade in a narrow trading range, the standard deviation will return a low value that indicates low volatility. Conversely, if prices swing wildly up and down, then standard deviation returns a high value that indicates high volatility.

- Analyzing kurtosis (kurt) of Close

df['Close'].kurt()

Ticker

AMD 0.153687

BTC-USD -0.706754

MSFT -0.613576

NVDA 3.033257

dtype: float64- Kurtosis measures the degree of a distribution expressed as fat tails. Most of the investors are risk-averse which means that they prefer a distribution with low kurtosis, or we can explain differently as returns that are not far away from the mean.

- Analyzing skewness (skew) of Close

df['Close'].skew()

Ticker

AMD 0.531194

BTC-USD 0.549099

MSFT 0.189534

NVDA 1.804376

dtype: float64- Skewness is the degree of asymmetry observed in a probability distribution. When data points on a bell curve are not distributed symmetrically to the left and right sides of the median, the bell curve is skewed. Distributions can be positive and right-skewed, or negative and left-skewed. A normal distribution exhibits zero skewness.

- The positive skewness of a distribution indicates that an investor may expect frequent small losses and a few large gains from the investment.

Exploratory Data Analysis (EDA)

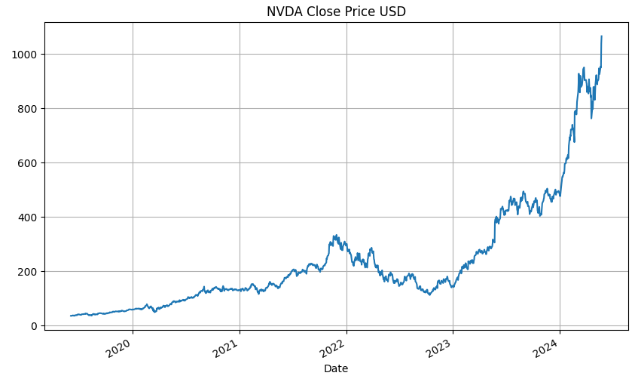

- Plotting the stock Close price

plt.figure(figsize=(10,6))

df['Close','NVDA'].plot()

plt.title('NVDA Close Price USD')

plt.grid()

plt.figure(figsize=(10,6))

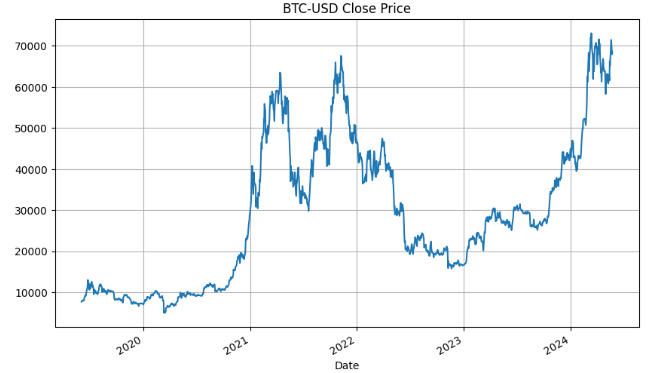

df['Close','BTC-USD'].plot()

plt.title('BTC-USD Close Price')

plt.grid()

plt.figure(figsize=(10,6))

df['Close','AMD'].plot()

plt.title('AMD Close Price')

plt.grid()

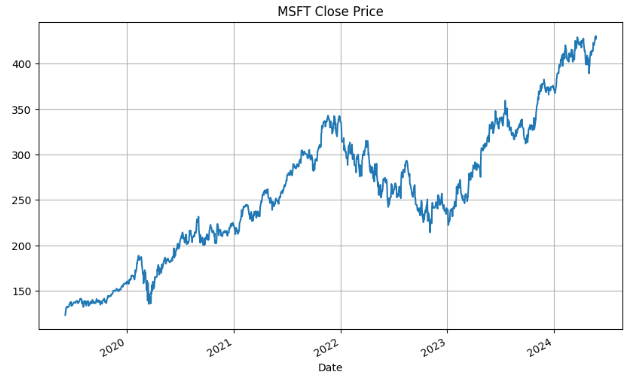

plt.figure(figsize=(10,6))

df['Close','MSFT'].plot()

plt.title('MSFT Close Price')

plt.grid()

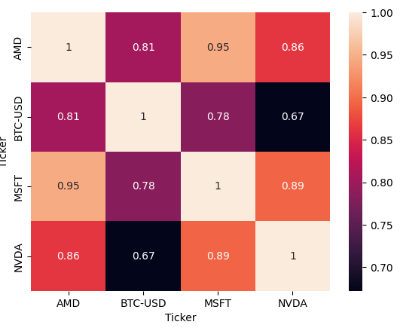

- Plotting the stock correlation matrix

# checking correlation using heatmap

#plotting the heatmap for correlation

ax = sns.heatmap(df['Close'].corr(), annot=True)

- The correlation table is a two-dimensional matrix that shows the correlation coefficient between pairs of securities. The cells in the table are color-coded to highlight significantly positive and negative relationships.

- Highly Positive Correlation Matchups: AMD — (NVDA, MSFT, BTC-USD), NVDA-MSFT, and BTC-MSFT.

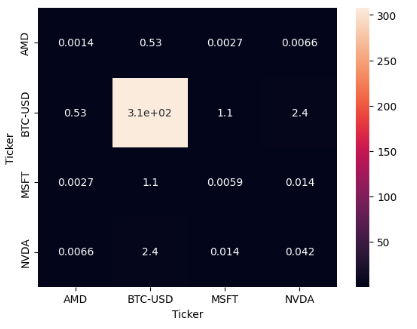

- Scaled covariance matrix

ax = sns.heatmap(df['Close'].cov()/1e6, annot=True)

- Covariance matrix and portfolio variance are essential tools that provide insights into the relationships between assets and help measure and manage portfolio risk.

Log Returns & Moving Average

- Calculating log returns and SMA with the optimal length moav=47 (after scanning over a range of moav=10–50)

# Finding the log returns

stock_df['LogReturns'] = stock_df['Adj Close'].apply(np.log).diff().dropna()

# Using Moving averages

moav=47

stock_df['MovAvg'] = stock_df['Adj Close'].rolling(moav).mean().dropna()

# Logarithmic scaling of the data and rounding the result

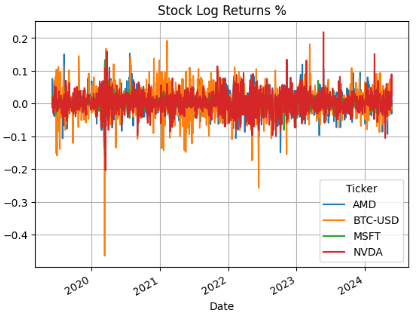

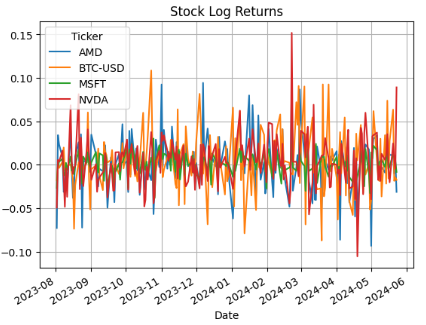

stock_df['Log'] = stock_df['MovAvg'].apply(np.log).apply(lambda x: round(x, 2))- Plotting the Stock Log Returns %

plt.figure(figsize=(10,6))

stock_df['LogReturns'].plot()

plt.title('Stock Log Returns %')

plt.grid()

AutoARIMA Model Training & Forecasting

- Setting the optimized input parameters and creating a DataFrame for predictions

# Days in the past to train on

days_to_train = 180

# Days in the future to predict

days_to_predict = 5

# Establishing a new DF for predictions

stock_df['Predictions'] = pd.DataFrame(index=stock_df['Log'].index,

columns=stock_df['Log'].columns)- AutoARIMA Model Training

# Iterate through each stock

for stock in tqdm(stocks):

# Current predicted value

pred_val = 0

# Training the model in a predetermined date range

for day in tqdm(range(1000,

stock_df['Log'].shape[0]-days_to_predict)):

# Data to use, containing a specific amount of days

training = stock_df['Log'][stock].iloc[day-days_to_train:day+1].dropna()

# Determining if the actual value crossed the predicted value

cross = ((training.iloc[-1] >= pred_val >= training.iloc[-2]) or

(training.iloc[-1] <= pred_val <= training.iloc[-2]))

# Running the model when the latest training value crosses the predicted value or every other day

if cross or day % 2 == 0:

# Finding the best parameters

model = AutoARIMA(start_p=0, start_q=0,

start_P=0, start_Q=0,

max_p=8, max_q=8,

max_P=5, max_Q=5,

error_action='ignore',

information_criterion='bic',

suppress_warnings=True)- AutoARIMA Model Forecasting

# Getting predictions for the optimum parameters by fitting to the training set

forecast = model.fit_predict(training,

n_periods=days_to_predict)

# Getting the last predicted value from the next N days

stock_df['Predictions'][stock].iloc[day:day+days_to_predict] = np.exp(forecast.iloc[-1])

# Updating the current predicted value

pred_val = forecast.iloc[-1]

# Shift ahead by 1 to compare the actual values to the predictions

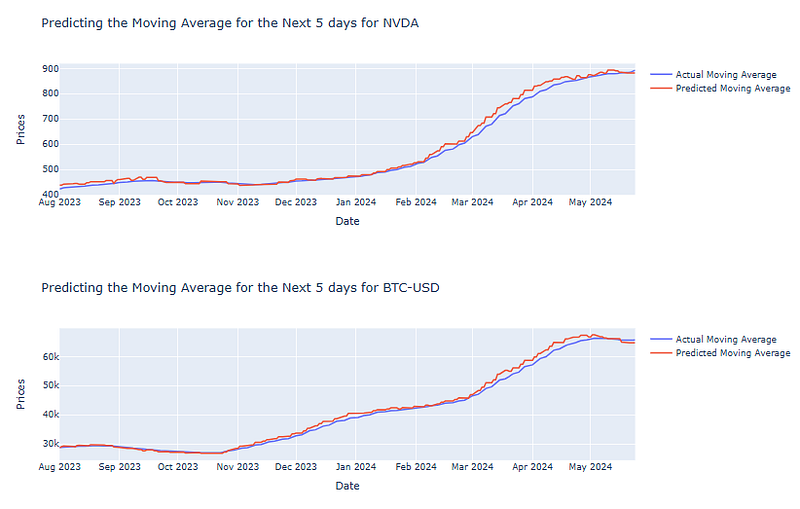

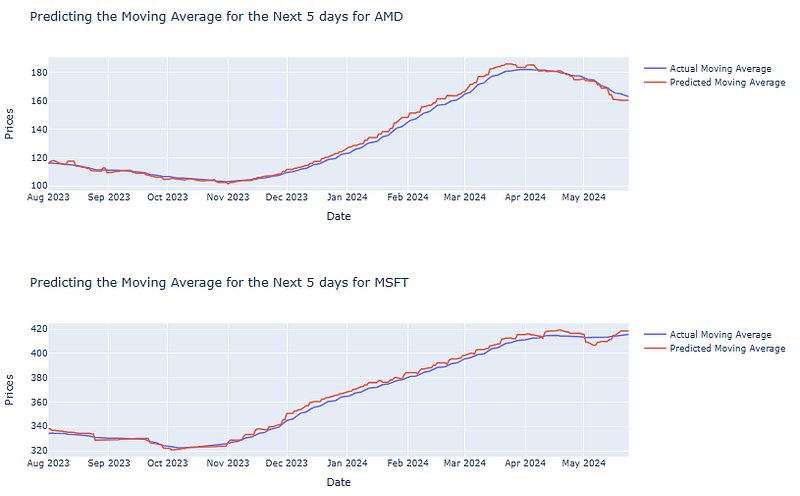

pred_df = stock_df['Predictions'].shift(1).astype(float).dropna()- Plotting Actual vs ARIMA Predicted Moving Average

for stock in stocks:

fig = go.Figure()

# Plotting the actual values

fig.add_trace(go.Scatter(x=pred_df.index,

y=stock_df['MovAvg'][stock].loc[pred_df.index],

name='Actual Moving Average',

mode='lines'))

# Plotting the predicted values

fig.add_trace(go.Scatter(x=pred_df.index,

y=pred_df[stock],

name='Predicted Moving Average',

mode='lines'))

# Setting the labels

fig.update_layout(title=f'Predicting the Moving Average for the Next {days_to_predict} days for {stock}',

xaxis_title='Date',

yaxis_title='Prices')

fig.show()

Asset-Based Model Evaluation

- Calculating RMSE for each stock

for stock in stocks:

# Finding the root mean squared error

rmse = mean_squared_error(stock_df['MovAvg'][stock].loc[pred_df.index], pred_df

[stock], squared=False)

print(f"On average, the model is off by {rmse} for {stock}\n")

On average, the model is off by 13.973533904045606 for NVDA

On average, the model is off by 1046.8465603864092 for BTC-USD

On average, the model is off by 2.617724183009069 for AMD

On average, the model is off by 2.9525237555709047 for MSFTGet Buy-Sell-Hold Positions

- Let’s formulate our SMA strategy:

- Buy — When the predicted price target shows a significant increase from the current price.

- Sell — When the predicted price target shows a significant decrease from the current price.

- Hold (or Do Nothing) — If the price target shows neither a significant increase or decrease from the current price.

def get_positions(difference, thres=3, short=True):

"""

Compares the percentage difference between actual

values and the respective predictions.

Returns the decision or positions to long or short

based on the difference.

Optional: shorting in addition to buying

"""

if difference > thres/100:

return 1

elif short and difference < -thres/100:

return -1

else:

return 0- Preparing the DataFrame trade_df for our trading strategy

# Creating a DF dictionary for trading the model

trade_df = {}

# Getting the percentage difference between the predictions and the actual values

trade_df['PercentDiff'] = (stock_df['Predictions'].dropna() /

stock_df['MovAvg'].loc[stock_df['Predictions'].dropna().index]) - 1

# Getting positions

trade_df['Positions'] = trade_df['PercentDiff'].map(lambda x: get_positions(x,

thres=1,

short=True) / len(stocks))

# Preventing lookahead bias by shifting the positions

trade_df['Positions'] = trade_df['Positions'].shift(2).dropna()

# Getting Log Returns

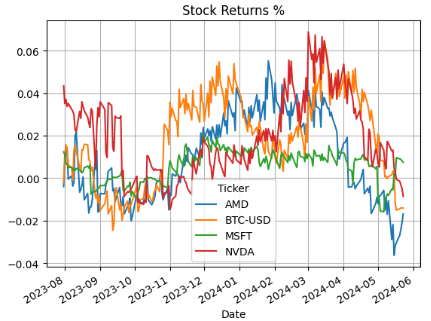

trade_df['LogReturns'] = stock_df['LogReturns'].loc[trade_df['Positions'].index] - Plotting Expected Stock Returns %

plt.figure(figsize=(10,6))

trade_df['PercentDiff'].plot()

plt.title('Stock Returns %')

plt.grid()

- Plotting Stock Positions

plt.figure(figsize=(10,6))

trade_df['Positions'].plot()

plt.title('Stock Positions')

plt.grid()

- Plotting Stock Log Returns

plt.figure(figsize=(10,6))

trade_df['LogReturns'].plot()

plt.title('Stock Log Returns')

plt.grid()

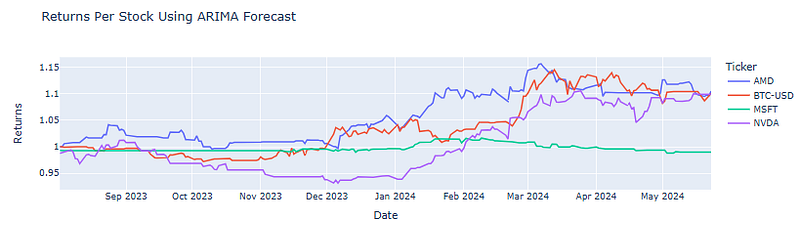

- Plotting cumulative returns per stock using ARIMA forecast

# Calculating Returns by multiplying the

# positions by the log returns

returns = trade_df['Positions'] * trade_df['LogReturns']

# Calculating the performance as we take the cumulative

# sum of the returns and transform the values back to normal

performance = returns.cumsum().apply(np.exp)

# Plotting the performance per stock

px.line(performance,

x=performance.index,

y=performance.columns,

title='Returns Per Stock Using ARIMA Forecast',

labels={'variable':'Stocks',

'value':'Returns'})

- It might be a good idea to exclude the underperforming MSFT stock from the proposed tech portfolio.

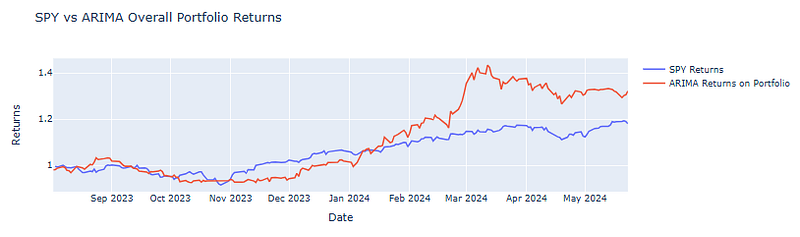

SPY vs ARIMA Overall Portfolio Returns

- Comparing the total cumulative portfolio returns against the SPY benchmark

# Returns for the portfolio

returns = (trade_df['Positions'] * trade_df['LogReturns']).sum(axis=1)

# Returns for SPY

spy = yf.download('SPY', start=returns.index[0]).loc[returns.index]

spy = spy['Adj Close'].apply(np.log).diff().dropna().cumsum().apply(np.exp)

# Calculating the performance as we take the cumulative sum of the returns and transform the values back to normal

performance = returns.cumsum().apply(np.exp)

# Plotting the comparison between SPY returns and ARIMA returns

fig = go.Figure()

fig.add_trace(go.Scatter(x=spy.index,

y=spy,

name='SPY Returns',

mode='lines'))

fig.add_trace(go.Scatter(x=performance.index,

y=performance.values,

name='ARIMA Returns on Portfolio',

mode='lines'))

fig.update_layout(title='SPY vs ARIMA Overall Portfolio Returns',

xaxis_title='Date',

yaxis_title='Returns')

fig.show()

- It is clear that the ARIMA model outperforms SPY in 2024.

Conclusions

- In this article, we have implemented and tested the vectorized backtesting & parameter tuning of AutoARIMA SMA trading strategy.

- Our portfolio combines BTC-USD with 3 tech stocks (NVDA, AMD, and MSFT).

- The backtesting strategy has been tested over a range of different SMA lengths and ARIMA parameter combinations to find the optimal set of parameters that maximize the expected return and outperforms the SPY benchmark.

- We have shown how the ARIMA SMA trading model can take into account the relationship between an observation and its lagged values, allowing traders to assess how past price movements impact future movements.

Explore More

- A Market-Neutral Strategy

- NVIDIA Rolling Volatility: GARCH & XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Blue-Chip Stock Portfolios for Quant Traders

- Top 6 Reliability/Risk Engineering Learnings

- Portfolio Optimization of 20 Dividend Growth Stocks

- A Comprehensive Analysis of Best Trading Technical Indicators w/ TA-Lib — Tesla ‘23

References

- Backtesting

- Vectorized Backtest of SMA Cross Strategy.

- Vectorized Backtest of Simple SMA Strategy

- A Guide to Vectorized Backtesting in Python for Trading Strategies

- LSTM Model Prediction for the Trading Strategy

- ML Classification Algorithms to Predict Market Movements and Backtesting

- A Beginner’s Guide to Backtesting Moving Average Crossover Trading Strategies with Python

- Dividend-NG-BTC Diversify Big Tech

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- Multiple-Criteria Technical Analysis of Blue Chips in Python

- Risk-Aware Strategies for DCA Investors

- Joint Analysis of Bitcoin, Gold and Crude Oil Prices

- BTC-USD Freefall vs FB/Meta Prophet 2022–23 Predictions