NVDA Technical Analysis using 75 Simplified FinTA Indicators

- In this project, we’ll implement, simplify and test a technical analysis module integrating standalone Python functions available through the FinTA library [1–4] (read more here).

- Our technical challenge is three-fold:

- Firstly, the proposed technical analysis tool should not require an installation and import of FinTA.

- Secondly, algo-traders should be able to use the above functions to generate 75 popular trading indicators directly without having to match all FinTA dependencies in their projects.

- Thirdly, we’ll strengthen our message by creating powerful, yet simple data visualizations using Pandas, Matplotlib and Plotly libraries. Charts can be a great way to illustrate trends in stocks.

Business Goal:

- We’ll attempt to find patterns in charts of the NVDA stock using a huge array of different technical indicators.

- Our focus on trends in prices and trading volume. It helps traders identify areas where there may be potential opportunities for profit or risk reduction, as well as warning signs to avoid.

Why NVDA:

- The demand for GPUs is indeed massive, which provides NVDA with wide opportunities to continue capitalizing on the demand spike. Recall that NVDA dominates the GPU market with a staggering 82% market share. And NVDA’s H100 GPUs are even called the “gold standard” of generative AI workloads.

- NVDA delivered another staggering quarter on 2/21/2024, topping consensus estimates by a wide margin.

- It seems like the rapid adoption of ChatGPT in recent years opened eyes to corporate leaders on capabilities of AI, and now we are in a big “AI race”.

- It is also important that NVDA is not only a company that sells AI chipsets, but provides an ecosystem with software, tools, and libraries. Providing ecosystem instead of just selling chipsets increases switching costs for customers.

- These points express our optimism about the ability of NVDA to sustain its leadership in the tech sector.

Let’s get down to the nuts & bolts of our methodology illustrated by the in-depth NVDA technical analysis.

Imports & Settings

- Setting the working directory YOURPATH, importing the necessary libraries and ignoring warnings

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

#Import Libraries

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

plt.style.use("fivethirtyeight")

%matplotlib inline

# For reading stock data from yahoo

import yfinance as yf

# For time stamps

from datetime import datetime

from math import sqrt

from math import sqrt

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import MinMaxScaler

#ignore the warnings

import warnings

warnings.filterwarnings('ignore')Input Stock Data

- Using yfinance to read the NVDA historical data

symbols = ['NVDA']

start_date = '2023-01-01'

data = yf.download(symbols, start=start_date)

data.tail()

[*********************100%%**********************] 1 of 1 completed

Open High Low Close Adj Close Volume

Date

2024-06-21 127.120003 130.630005 124.300003 126.570000 126.570000 655484700

2024-06-24 123.239998 124.459999 118.040001 118.110001 118.110001 476060900

2024-06-25 121.199997 126.500000 119.320000 126.089996 126.089996 425787500

2024-06-26 126.129997 128.119995 122.599998 126.400002 126.400002 362975900

2024-06-27 124.099998 126.410004 122.919998 123.989998 123.989998 251669500

2024-06-28 124.574997 127.709999 122.889999 124.375000 124.375000 188174904SMA Indicator

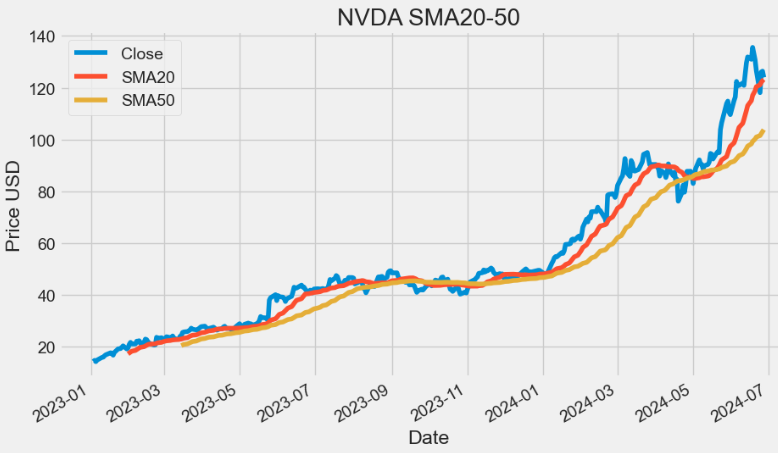

- Moving averages are one of the core indicators in technical analysis.

- Simple Moving Average (SMA) is simply the rolling average price over the specified period.

def SMA(ohlc, period= 41, column="Close"):

"""

Simple moving average - rolling mean in pandas lingo. Also known as 'MA'.

The simple moving average (SMA) is the most basic of the moving averages used for trading.

"""

return pd.Series(

ohlc[column].rolling(window=period).mean(),

name="{0} period SMA".format(period),

)

plt.figure(figsize=(10,6))

data['SMA20']=SMA(data, period=20, column="Close")

data['SMA50']=SMA(data, period=50, column="Close")

data['Close'].plot(label='Close')

data['SMA20'].plot(label='SMA20')

data['SMA50'].plot(label='SMA50')

plt.ylabel('Price USD')

plt.title('NVDA SMA20-50')

plt.legend()

- SMAs are often used to determine trend direction. If the SMA is moving up, the trend is up. If the SMA is moving down, the trend is down. A 200-bar SMA is common proxy for the long term trend. 50-bar SMAs are typically used to gauge the intermediate trend. Shorter period SMAs can be used to determine shorter term trends.

SMM Indicator

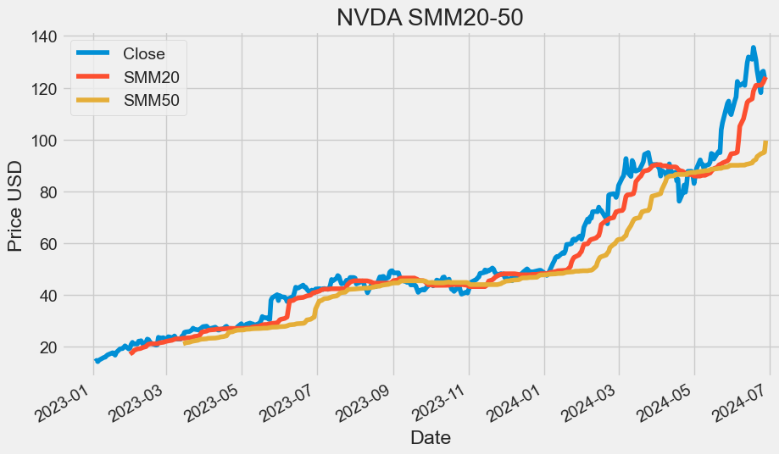

- Where a moving average filter takes the arithmetic mean of the input over a moving sample window, a median filter takes a median instead. The median filter is most-useful for removing occasional outliers from an input stream.

- The Simple Moving Median (SMM) of an array A returns an array of local k-point median values, where each median is calculated over a sliding window of length k across neighboring elements of A.

- The SMM is a central tendency which is calculated over a sliding window of price bars or indicator values. The median is the numeric value separating the higher from the lower half of the data set built from the input series over the selected window.

def SMM(ohlc, period= 9, column= "Close"):

"""

Simple moving median, an alternative to moving average. SMA, when used to estimate the underlying trend in a time series,

is susceptible to rare events such as rapid shocks or other anomalies. A more robust estimate of the trend is the simple moving median over n time periods.

"""

return pd.Series(

ohlc[column].rolling(window=period).median(),

name="{0} period SMM".format(period),

)

plt.figure(figsize=(10,6))

data['SMM20']=SMM(data, period=20, column="Close")

data['SMM50']=SMM(data, period=50, column="Close")

data['Close'].plot(label='Close')

data['SMM20'].plot(label='SMM20')

data['SMM50'].plot(label='SMM50')

plt.ylabel('Price USD')

plt.title('NVDA SMM20-50')

plt.legend()

SSMA Indicator

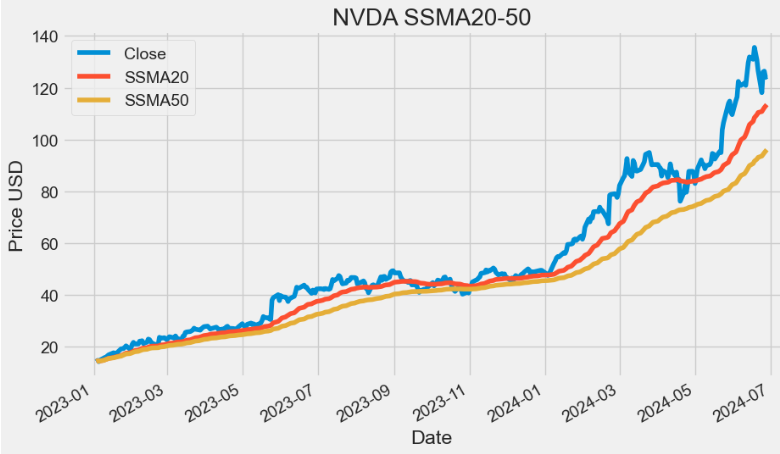

- Smoothed Simple Moving Average (SSMA) and SMA are two popular technical indicators used in technical analysis. The primary difference between the two is that SMA places equal weight on each data point, while SSMA places more emphasis on recent data points.

def SSMA(ohlc,period = 9, column = "Close",adjust = True):

"""

Smoothed simple moving average.

:param ohlc: data

:param period: range

:param column: open/close/high/low column of the DataFrame

:return: result Series

"""

return pd.Series(

ohlc[column]

.ewm(ignore_na=False, alpha=1.0 / period, min_periods=0, adjust=adjust)

.mean(),

name="{0} period SSMA".format(period),

)

plt.figure(figsize=(10,6))

data['SSMA20']=SSMA(data, period=20, column="Close",adjust=True)

data['SSMA50']=SSMA(data, period=50, column="Close",adjust=True)

data['Close'].plot(label='Close')

data['SSMA20'].plot(label='SSMA20')

data['SSMA50'].plot(label='SSMA50')

plt.ylabel('Price USD')

plt.title('NVDA SSMA20-50')

plt.legend()

- As we can see from the above plot, the main advantage of SSMA is that it removes short-term fluctuations, and allows us to view the price trends much easier, which is why they are widely used in trending markets.

- Even more than the SMA, the SMMA ensures that temporary fluctuations in price (also known as ‘noise’) are filtered out. In this way, the SMMA succeeds — better than the other MAs — in visualizing the prevailing trend.

EMA Indicator

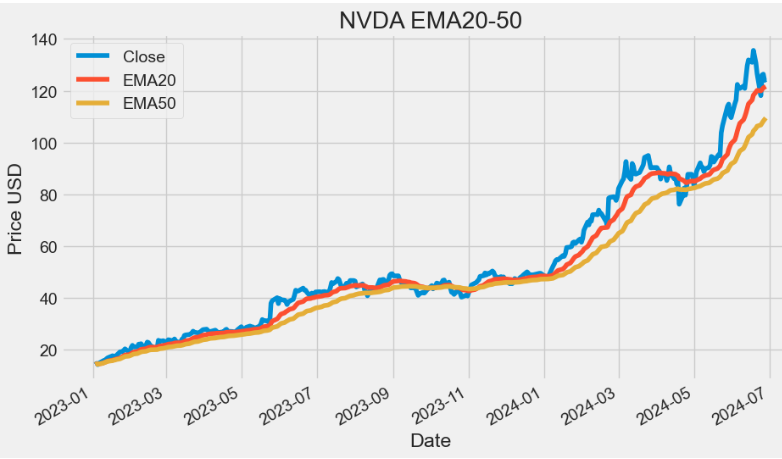

- An exponential moving average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

- Like all MA, EMA is used to produce buy and sell signals based on crossovers and divergences from the historical average.

- Traders often use several different EMA lengths, such as 20-day, 50-day, and 200-day moving averages.

def EMA(ohlc,period = 9,column = "Close", adjust = True):

"""

Exponential Weighted Moving Average - Like all moving average indicators, they are much better suited for trending markets.

When the market is in a strong and sustained uptrend, the EMA indicator line will also show an uptrend and vice-versa for a down trend.

EMAs are commonly used in conjunction with other indicators to confirm significant market moves and to gauge their validity.

"""

return pd.Series(

ohlc[column].ewm(span=period, adjust=adjust).mean(),

name="{0} period EMA".format(period),

)

plt.figure(figsize=(10,6))

data['EMA20']=EMA(data, period=20, column="Close",adjust=True)

data['EMA50']=EMA(data, period=50, column="Close",adjust=True)

data['Close'].plot(label='Close')

data['EMA20'].plot(label='EMA20')

data['EMA50'].plot(label='EMA50')

plt.ylabel('Price USD')

plt.title('NVDA EMA20-50')

plt.legend()

- The aim of EMA is to establish the direction in which the price of a security is moving based on past prices. Therefore, EMA is a lag indicator.

- EMA is not predictive of future prices; it simply highlights the trend that is being followed by the stock price.

- Advantages of Using the EMA:

- Firstly, it provides accurate signal identification by weighing recent price data more heavily than older data, reflecting the current market sentiment more accurately.

- Secondly, it reduces lag time in trend identification, allowing traders to enter and exit positions more quickly.

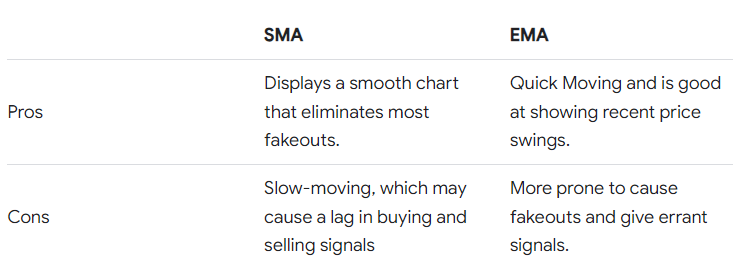

- Simple vs. Exponential Moving Averages:

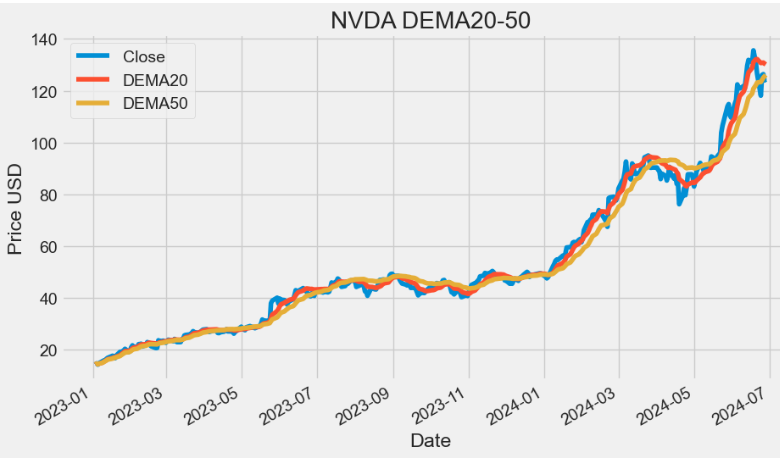

DEMA Indicator

- The double exponential moving average (DEMA) is a technical indicator devised to reduce the lag in the results produced by a traditional MA. Technical traders use it to lessen the amount of “noise” that can distort the movements on a price chart.

def DEMA(ohlc,period = 9,column = "Close",adjust = True):

"""

Double Exponential Moving Average - attempts to remove the inherent lag associated to Moving Averages

by placing more weight on recent values. The name suggests this is achieved by applying a double exponential

smoothing which is not the case. The name double comes from the fact that the value of an EMA (Exponential Moving Average) is doubled.

To keep it in line with the actual data and to remove the lag the value 'EMA of EMA' is subtracted from the previously doubled EMA.

Because EMA(EMA) is used in the calculation, DEMA needs 2 * period -1 samples to start producing values in contrast to the period

samples needed by a regular EMA

"""

DEMA = (

2 * EMA(ohlc, period)

- EMA(ohlc, period).ewm(span=period, adjust=adjust).mean()

)

return pd.Series(DEMA, name="{0} period DEMA".format(period))

plt.figure(figsize=(10,6))

data['DEMA20']=DEMA(data, period=20, column="Close",adjust=True)

data['DEMA50']=DEMA(data, period=50, column="Close",adjust=True)

data['Close'].plot(label='Close')

data['DEMA20'].plot(label='DEMA20')

data['DEMA50'].plot(label='DEMA50')

plt.ylabel('Price USD')

plt.title('NVDA DEMA20-50')

plt.legend()

- TradingView: The DEMA was developed by Patrick Mulloy for the purpose of reducing lag and increasing responsiveness. This fast-acting MA allows traders to spot trend reversals quickly, resulting in better entries into newly formed trends. The indicator is obviously based on the EMA but it follows the price more closely.

- Its calculation and usage somewhat resemble the Hull Moving Average (HMA). It helps traders spot the prevailing trend and is often used in combination with other signals and analysis techniques.

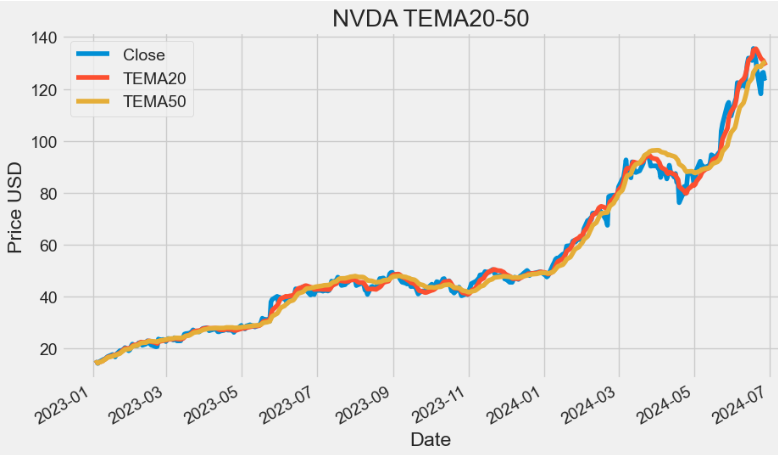

TEMA Indicator

- The triple exponential moving average, TEMA, is a trend following indicator used by analysts. It is formulated by creating multiple EMA of the original EMA to reduce some of the lag. It helps to reduce price volatility to make the trend easier to identify.

def TEMA(ohlc, period = 9, adjust = True):

"""

Triple exponential moving average - attempts to remove the inherent lag associated to Moving Averages by placing more weight on recent values.

The name suggests this is achieved by applying a triple exponential smoothing which is not the case. The name triple comes from the fact that the

value of an EMA (Exponential Moving Average) is triple.

To keep it in line with the actual data and to remove the lag the value 'EMA of EMA' is subtracted 3 times from the previously tripled EMA.

Finally 'EMA of EMA of EMA' is added.

Because EMA(EMA(EMA)) is used in the calculation, TEMA needs 3 * period - 2 samples to start producing values in contrast to the period samples

needed by a regular EMA.

"""

triple_ema = 3 * EMA(ohlc, period)

ema_ema_ema = (

EMA(ohlc, period)

.ewm(ignore_na=False, span=period, adjust=adjust)

.mean()

.ewm(ignore_na=False, span=period, adjust=adjust)

.mean()

)

TEMA = (

triple_ema

- 3 * EMA(ohlc, period).ewm(span=period, adjust=adjust).mean()

+ ema_ema_ema

)

return pd.Series(TEMA, name="{0} period TEMA".format(period))

plt.figure(figsize=(10,6))

data['TEMA20']=TEMA(data, period=20, adjust=True)

data['TEMA50']=TEMA(data, period=50, adjust=True)

data['Close'].plot(label='Close')

data['TEMA20'].plot(label='TEMA20')

data['TEMA50'].plot(label='TEMA50')

plt.ylabel('Price USD')

plt.title('NVDA TEMA20-50')

plt.legend()

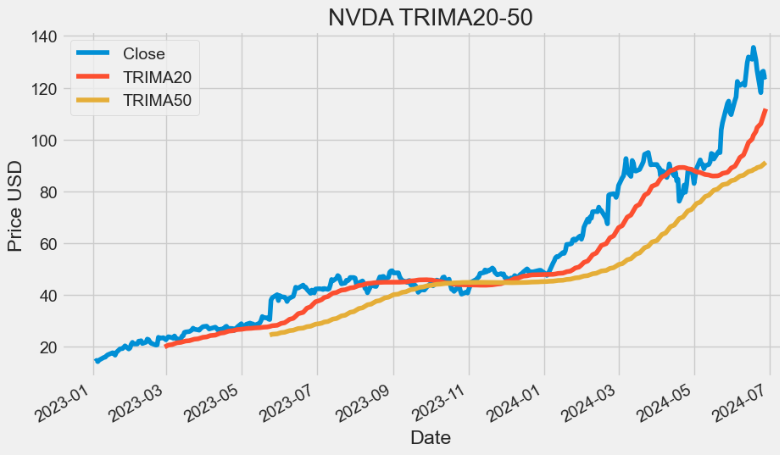

TRIMA Indicator

- The triangular moving average (TMA) is a weighted average of the last n prices (P), whose result is equivalent to a double smoothed simple moving average: SMA = (P1 + P2 + P3 + P4 + … + Pn) / n.

- The TRIMA is simply the SMA of the SMA — a double-smoothed simple moving average . The end effect of the double smoothing is that greater weight is placed on values near the middle of the lookback period. It therefore reacts relatively slowly to price changes compared to most moving averages.

def TRIMA(ohlc, period = 18):

"""

The Triangular Moving Average (TRIMA) [also known as TMA] represents an average of prices,

but places weight on the middle prices of the time period.

The calculations double-smooth the data using a window width that is one-half the length of the series.

source: https://www.thebalance.com/triangular-moving-average-tma-description-and-uses-1031203

"""

mysma=SMA(ohlc, period).rolling(window=period).sum()

return pd.Series(mysma/ period, name="{0} period TRIMA".format(period))

plt.figure(figsize=(10,6))

data['TRIMA20']=TRIMA(data, period=20)

data['TRIMA50']=TRIMA(data, period=50)

data['Close'].plot(label='Close')

data['TRIMA20'].plot(label='TRIMA20')

data['TRIMA50'].plot(label='TRIMA50')

plt.ylabel('Price USD')

plt.title('NVDA TRIMA20-50')

plt.legend()

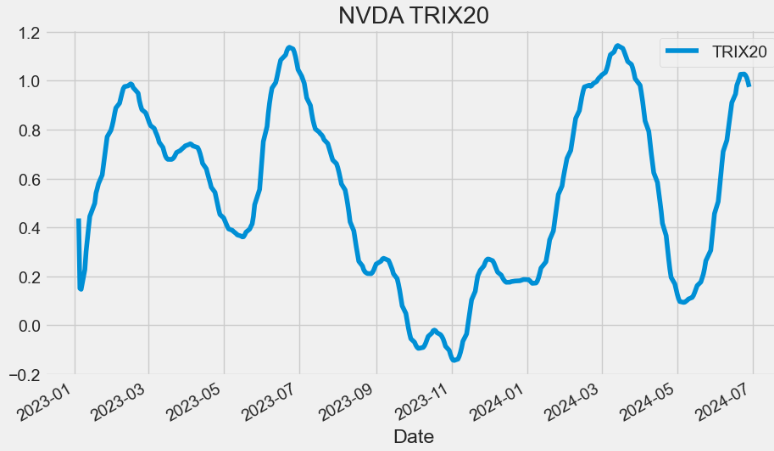

TRIX Indicator

- The triple exponential average (TRIX) is a momentum indicator used by technical traders. It shows the percentage change in a moving average that has been smoothed exponentially three times.

- Two main advantages of TRIX over other trend-following indicators are its excellent filtration of market noise and its tendency to be a leading than lagging indicator. It filters out market noise using the triple exponential average calculation, thus eliminating minor short-term cycles that indicate a change in market direction. It has the ability to lead a market because it measures the difference between each bar’s “smoothed” version of the price information. When interpreted as a leading indicator, TRIX is best used in conjunction with another market-timing indicator — this minimizes false indications.

def TRIX(ohlc,period = 20,column = "Close",adjust = True):

"""

The TRIX indicator calculates the rate of change of a triple exponential moving average.

The values oscillate around zero. Buy/sell signals are generated when the TRIX crosses above/below zero.

A (typically) 9 period exponential moving average of the TRIX can be used as a signal line.

A buy/sell signals are generated when the TRIX crosses above/below the signal line and is also above/below zero.

The TRIX was developed by Jack K. Hutson, publisher of Technical Analysis of Stocks & Commodities magazine,

and was introduced in Volume 1, Number 5 of that magazine.

"""

data = ohlc[column]

def _ema(data, period, adjust):

return pd.Series(data.ewm(span=period, adjust=adjust).mean())

m = _ema(_ema(_ema(data, period, adjust), period, adjust), period, adjust)

return pd.Series(100 * (m.diff() / m), name="{0} period TRIX".format(period))

plt.figure(figsize=(10,6))

data['TRIX20']=TRIX(data, period=20,column = "Close")

data['TRIX20'].plot(label='TRIX20')

plt.title('NVDA TRIX20')

plt.legend()

- In fact, TRIX can be used as both a trend following indicator and as an oscillator.

- As a trend following indicator, TRIX>0 values imply that an uptrend is in place whereas TRIX<0 values denote that a downtrend is in place in the market.

- When TRIX values run along the 0 value (centerline), it implies that the market stance is neutral.

- As an oscillator, TRIX is used to watch out for overbought and oversold conditions in the market. Extreme positive values denote overbought conditions, while extreme negative values denote oversold conditions in the market.

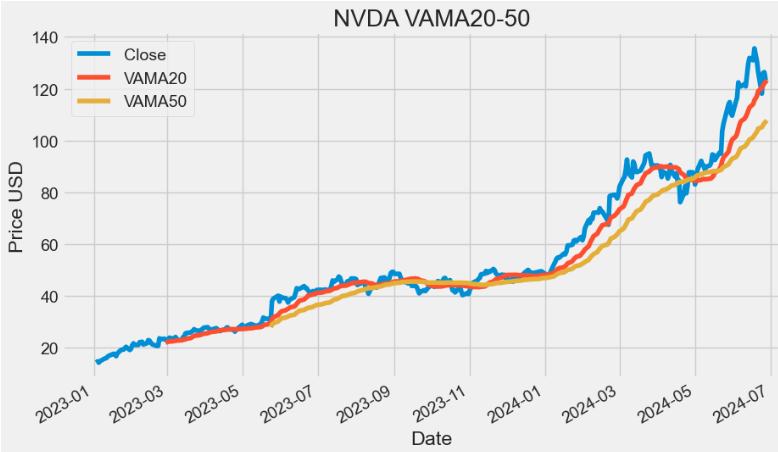

VAMA Indicator

- Volume Adjusted Moving Average (VAMA) is a technical indicator that combines price and volume when computing the average.

def VAMA(ohlcv,period = 8, column = "Close",colvol="Volume"):

"""

Volume Adjusted Moving Average

"""

vp = ohlcv[colvol] * ohlcv[column]

volsum = ohlcv[colvol].rolling(window=period).mean()

volRatio = pd.Series(vp / volsum, name="VAMA")

cumSum = (volRatio * ohlcv[column]).rolling(window=period).sum()

cumDiv = volRatio.rolling(window=period).sum()

return pd.Series(cumSum / cumDiv, name="{0} period VAMA".format(period))

plt.figure(figsize=(10,6))

data['VAMA20']=VAMA(data, period=20,column = "Close",colvol="Volume")

data['VAMA50']=VAMA(data, period=50,column = "Close",colvol="Volume")

data['Close'].plot(label='Close')

data['VAMA20'].plot(label='VAMA20')

data['VAMA50'].plot(label='VAMA50')

plt.ylabel('Price USD')

plt.title('NVDA VAMA20-50')

plt.legend()

- VAMA utilizes a period length that is based on volume increments rather than time.

- As with any MA, the VAMA can be used to detect turning points on the market. This can be done by identifying crossover points between slow and fast VAMAs for the same stock.

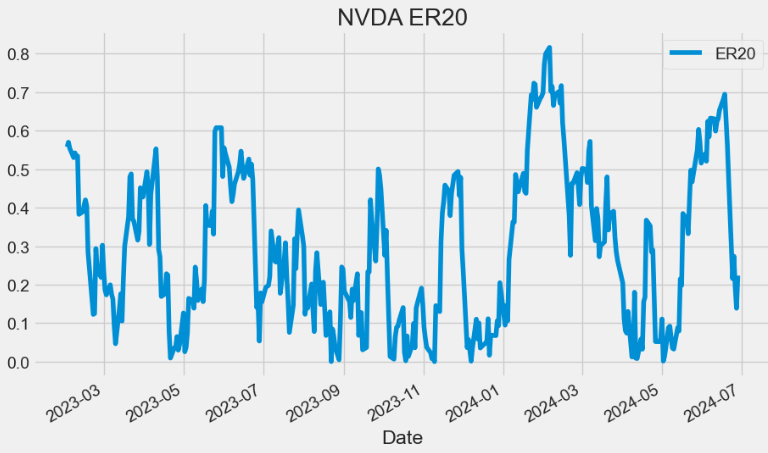

(K)ER Indicator

- The Kaufman Efficiency Ratio (ER) Indicator provides insights to assess trend efficiency and understand the speed of price movements relative to market volatility. It is used to identify bullish trends and filter out erratic entry signals.

def ER(ohlc, period = 10, column = "Close"):

"""The Kaufman Efficiency indicator is an oscillator indicator that oscillates between +100 and -100, where zero is the center point.

+100 is upward forex trending market and -100 is downwards trending markets."""

change = ohlc[column].diff(period).abs()

volatility = ohlc[column].diff().abs().rolling(window=period).sum()

return pd.Series(change / volatility, name="{0} period ER".format(period))

plt.figure(figsize=(10,6))

data['ER20']=ER(data, period=20,column = "Close")

data['ER20'].plot(label='ER20')

plt.title('NVDA ER20')

plt.legend()

- The center point is 0. +1 indicates a financial instrument with a perfectly efficient upward trend.

- A buy signal is generated after the indicator crosses above +0,6.

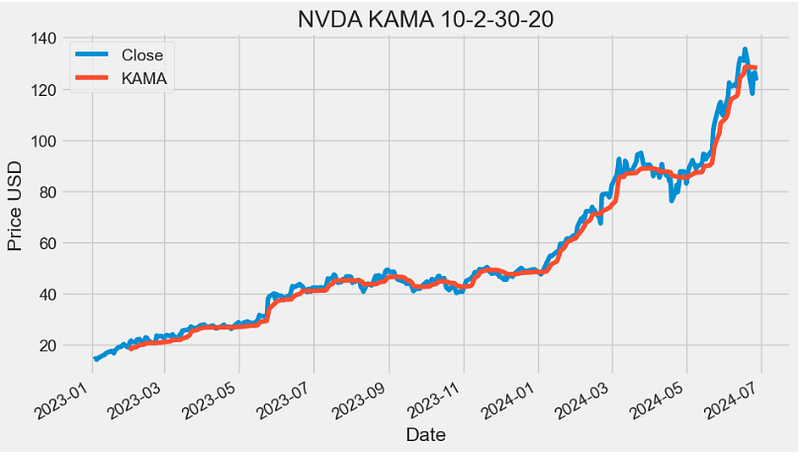

KAMA Indicator

- The Kaufman’s Adaptive Moving Average (KAMA) indicator accounts not only for price action but also for market volatility. One of the primary weaknesses of traditional MA is that when used for trading signals, they tend to generate many false signals. The KAMA indicator seeks to lessen this tendency — generate fewer false signals — by not responding to short-term, insignificant price movements.

def KAMA(ohlc,er= 10,ema_fast = 2,ema_slow = 30,period = 20,column = "Close"):

"""Developed by Perry Kaufman, Kaufman's Adaptive Moving Average (KAMA) is a moving average designed to account for market noise or volatility.

Its main advantage is that it takes into consideration not just the direction, but the market volatility as well."""

er = ER(ohlc, er)

fast_alpha = 2 / (ema_fast + 1)

slow_alpha = 2 / (ema_slow + 1)

sc = pd.Series(

(er * (fast_alpha - slow_alpha) + slow_alpha) ** 2,

name="smoothing_constant",

) ## smoothing constant

sma = pd.Series(

ohlc[column].rolling(period).mean(), name="SMA"

) ## first KAMA is SMA

kama = []

# Current KAMA = Prior KAMA + smoothing_constant * (Price - Prior KAMA)

for s, ma, price in zip(

sc.items(), sma.shift().items(), ohlc[column].items()

):

try:

kama.append(kama[-1] + s[1] * (price[1] - kama[-1]))

except (IndexError, TypeError):

if pd.notnull(ma[1]):

kama.append(ma[1] + s[1] * (price[1] - ma[1]))

else:

kama.append(None)

sma["KAMA"] = pd.Series(

kama, index=sma.index, name="{0} period KAMA.".format(period)

) ## apply the kama list to existing index

return sma["KAMA"]

plt.figure(figsize=(10,6))

data['KAMA']=KAMA(data,er= 10,ema_fast = 2,ema_slow = 30,period = 20,column = "Close")

data['Close'].plot(label='Close')

data['KAMA'].plot(label='KAMA')

plt.ylabel('Price USD')

plt.title('NVDA KAMA 10-2-30-20')

plt.legend()

- One of the uses of KAMA is to identify the general trend of current market price action. Basically, when the KAMA indicator line is moving lower, it indicates the existence of a downtrend. On the other hand, when the KAMA line is moving higher, it shows an uptrend. As compared to the SMA, the KAMA indicat\or is less likely to generate false signals that may cause a trader to incur losses.

- Read more about KAMA here.

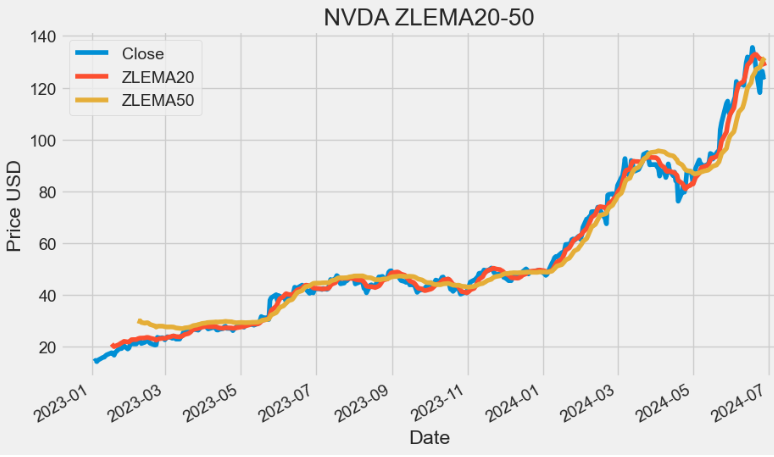

ZLEMA Indicator

- The Zero Lag Exponential Moving Average (ZLEMA) is a technical analysis indicator that is used to smoothen out price fluctuations and provide traders with a clearer view of market trends.

- Unlike traditional moving averages, the ZLEMA uses a complex formula that minimizes lag and provides traders with real-time market information.

def ZLEMA(ohlc,period = 26,adjust = True,column = "Close"):

"""ZLEMA is an abbreviation of Zero Lag Exponential Moving Average. It was developed by John Ehlers and Rick Way.

ZLEMA is a kind of Exponential moving average but its main idea is to eliminate the lag arising from the very nature of the moving averages

and other trend following indicators. As it follows price closer, it also provides better price averaging and responds better to price swings."""

lag = (period - 1) / 2

ema = pd.Series(

(ohlc[column] + (ohlc[column].diff(lag))),

name="{0} period ZLEMA.".format(period),

)

zlema = pd.Series(

ema.ewm(span=period, adjust=adjust).mean(),

name="{0} period ZLEMA".format(period),

)

return zlema

plt.figure(figsize=(10,6))

data['ZLEMA20']=ZLEMA(data,period = 20,adjust = True,column = "Close")

data['ZLEMA50']=ZLEMA(data,period = 50,adjust = True,column = "Close")

data['Close'].plot(label='Close')

data['ZLEMA20'].plot(label='ZLEMA20')

data['ZLEMA50'].plot(label='ZLEMA50')

plt.ylabel('Price USD')

plt.title('NVDA ZLEMA20-50')

plt.legend()

- Read more about ZLEMA here.

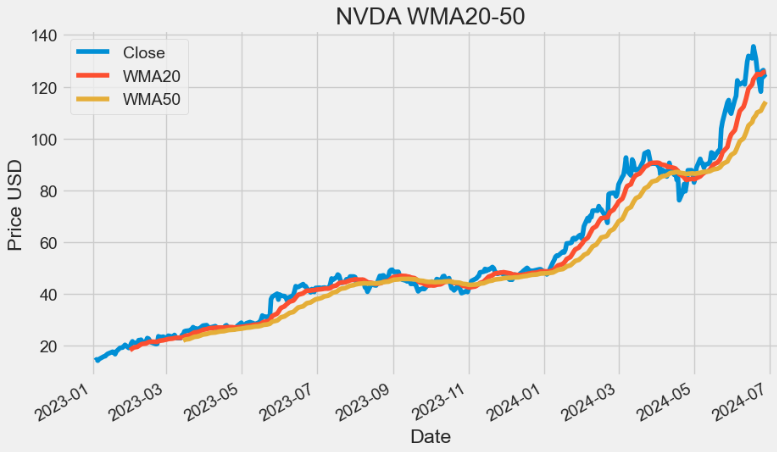

WMA Indicator

- Weighted Moving Average (WMA) assigns a heavier weighting to more current data points since they are more relevant than data points from the more remote past. The sum of the weighting should add up to one (or 100%). For SMA, the weightings are equally distributed.

def WMA(ohlc, period = 9, column = "Close"):

"""

WMA stands for weighted moving average. It helps to smooth the price curve for better trend identification.

It places even greater importance on recent data than the EMA does.

:period: Specifies the number of Periods used for WMA calculation

"""

d = (period * (period + 1)) / 2 # denominator

weights = np.arange(1, period + 1)

def linear(w):

def _compute(x):

return (w * x).sum() / d

return _compute

_close = ohlc[column].rolling(period, min_periods=period)

wma = _close.apply(linear(weights), raw=True)

return pd.Series(wma, name="{0} period WMA.".format(period))

plt.figure(figsize=(10,6))

data['WMA20']=WMA(data,period = 20,column = "Close")

data['WMA50']=WMA(data,period = 50,column = "Close")

data['Close'].plot(label='Close')

data['WMA20'].plot(label='WMA20')

data['WMA50'].plot(label='WMA50')

plt.ylabel('Price USD')

plt.title('NVDA WMA20-50')

plt.legend()

- The WMA method is a form of technical analysis that is used by traders to identify trends. Additionally, it can be used as a filter for price action and as an indicator of trend direction. It can also be used as a way to identify support and resistance levels on a chart.

- The WMA can be used in conjunction with other indicators such as the Moving Average Convergence Divergence (MACD) and Relative Strength Index (RSI) to help traders make more informed trading decisions.

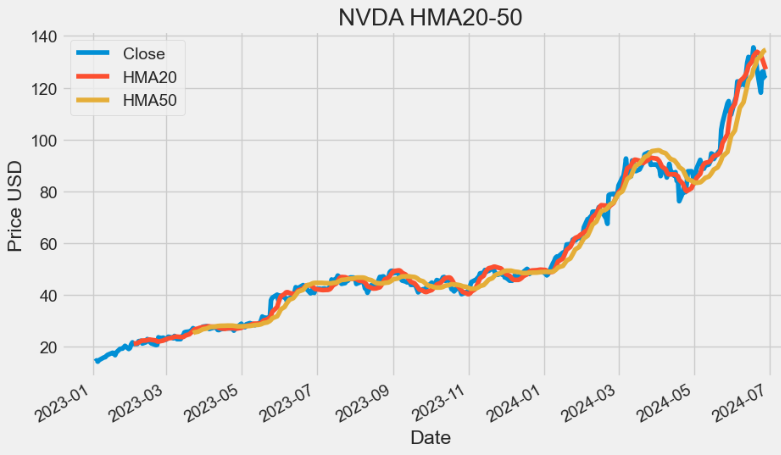

HMA Indicator

- The Hull Moving Average (HMA) is a technical analysis tool that measures the average price of an asset over a period of time. In contrast to traditional moving averages (MA), the indicator aims to minimize the noise and smooth price fluctuations.

def HMA(ohlc, period = 16):

"""

HMA indicator is a common abbreviation of Hull Moving Average.

The average was developed by Allan Hull and is used mainly to identify the current market trend.

Unlike SMA (simple moving average) the curve of Hull moving average is considerably smoother.

Moreover, because its aim is to minimize the lag between HMA and price it does follow the price activity much closer.

It is used especially for middle-term and long-term trading.

:period: Specifies the number of Periods used for WMA calculation

"""

import math

half_length = int(period / 2)

sqrt_length = int(math.sqrt(period))

wmaf = WMA(ohlc, period=half_length)

wmas = WMA(ohlc, period=period)

ohlc["deltawma"] = 2 * wmaf - wmas

hma = WMA(ohlc, column="deltawma", period=sqrt_length)

return pd.Series(hma, name="{0} period HMA.".format(period))

plt.figure(figsize=(10,6))

data['HMA20']=HMA(data,period = 20)

data['HMA50']=HMA(data,period = 50)

data['Close'].plot(label='Close')

data['HMA20'].plot(label='HMA20')

data['HMA50'].plot(label='HMA50')

plt.ylabel('Price USD')

plt.title('NVDA HMA20-50')

plt.legend()

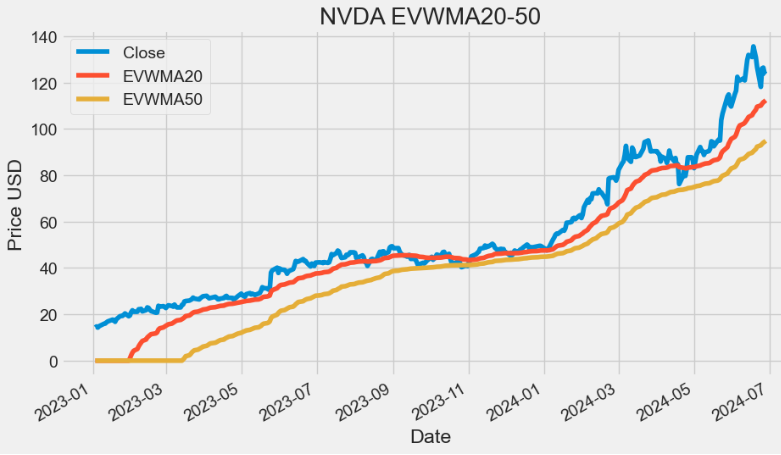

eVWMA Indicator

- Elastic Volume Weighted Moving Average (eVWMA) is a statistical measure using the volume to define the period of the moving average. It incorporates volume information in a natural and logical way. The eVWMA can be looked at as an approximation to the average price paid per share. The ability to “Use Average Volume” as your volume period, makes this indicator both symbol-independent and timeframe independent. This allows the use to switch both timeframe and symbol without having to change the volume period.

def EVWMA(ohlcv, period = 20,column = "Close",colvol="Volume"):

"""

The eVWMA can be looked at as an approximation to the

average price paid per share in the last n periods.

:period: Specifies the number of Periods used for eVWMA calculation

"""

vol_sum = (

ohlcv[colvol].rolling(window=period).sum()

) # floating shares in last N periods

x = (vol_sum - ohlcv[colvol]) / vol_sum

y = (ohlcv[colvol] * ohlcv[column]) / vol_sum

evwma = [0]

for x, y in zip(x.fillna(0).items(), y.items()):

if x[1] == 0 or y[1] == 0:

evwma.append(0)

else:

evwma.append(evwma[-1] * x[1] + y[1])

return pd.Series(

evwma[1:], index=ohlcv.index, name="{0} period EVWMA.".format(period),

)

plt.figure(figsize=(10,6))

data['EVWMA20']=EVWMA(data,period = 20,column = "Close",colvol="Volume")

data['EVWMA50']=EVWMA(data,period = 50,column = "Close",colvol="Volume")

data['Close'].plot(label='Close')

data['EVWMA20'].plot(label='EVWMA20')

data['EVWMA50'].plot(label='EVWMA50')

plt.ylabel('Price USD')

plt.title('NVDA EVWMA20-50')

plt.legend()

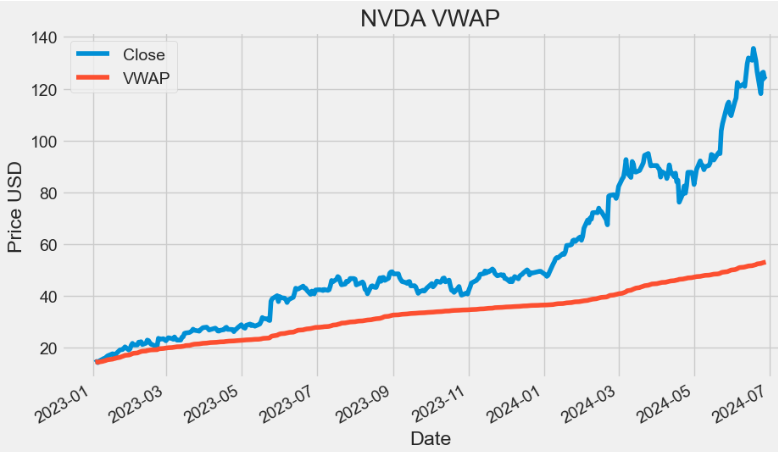

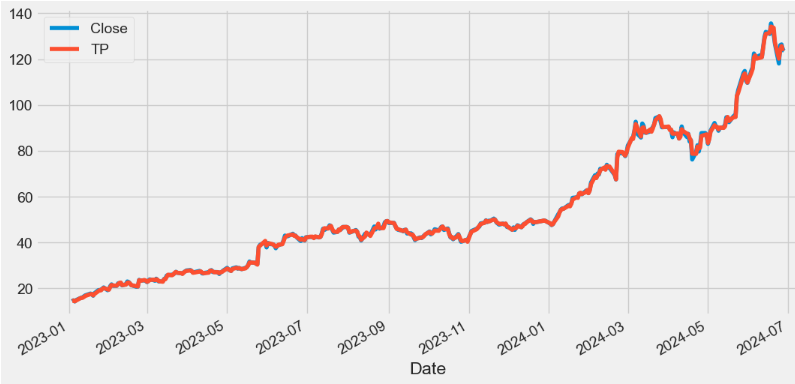

VWAP Indicator

- Volume-Weighted Average Price (VWAP) is the average price of a stock weighted by volume. By monitoring VWAP, a trader might get an idea of a stock’s liquidity and the price buyers and sellers agree is fair at a specific time. The VWAP indicator can be used by day traders to monitor intraday price movement. Institutions and algorithms might use VWAP to figure out the average price of large orders.

def TP(ohlc,open="Open",close="Close",high="High",low="Low"):

"""Typical Price refers to the arithmetic average of the high, low, and closing prices for a given period."""

return pd.Series((ohlc[high] + ohlc[low] + ohlc[close]) / 3, name="TP")

def VWAP(ohlcv,colvol="Volume"):

"""

The volume weighted average price (VWAP) is a trading benchmark used especially in pension plans.

VWAP is calculated by adding up the dollars traded for every transaction (price multiplied by number of shares traded) and then dividing

by the total shares traded for the day.

"""

return pd.Series(

((ohlcv[colvol] * TP(ohlcv,open="Open",close="Close",high="High",low="Low")).cumsum()) / ohlcv[colvol].cumsum(),

name="VWAP.",

)

plt.figure(figsize=(10,6))

data['VWAP']=VWAP(data,colvol="Volume")

data['Close'].plot(label='Close')

data['VWAP'].plot(label='VWAP')

plt.ylabel('Price USD')

plt.title('NVDA VWAP')

plt.legend()

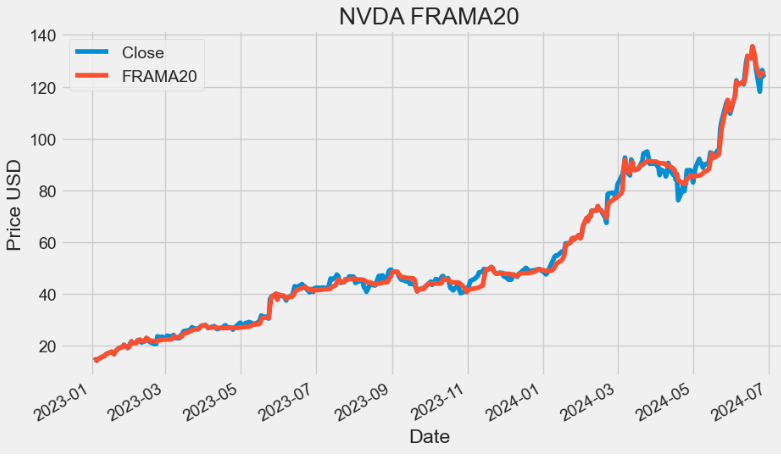

FRAMA Indicator

- Fractal Adaptive Moving Average (FRAMA) is designed to adapt to market conditions, providing traders with a versatile tool for trend identification and smoother price tracking.

def FRAMA(ohlc, period = 16, batch =10,column = "Close"):

"""Fractal Adaptive Moving Average

Source: http://www.stockspotter.com/Files/frama.pdf

Adopted from: https://www.quantopian.com/posts/frama-fractal-adaptive-moving-average-in-python

:period: Specifies the number of periods used for FRANA calculation

:batch: Specifies the size of batches used for FRAMA calculation

"""

assert period % 2 == 0, print("FRAMA period must be even")

c = ohlc[column].copy()

window = batch * 2

hh = c.rolling(batch).max()

ll = c.rolling(batch).min()

n1 = (hh - ll) / batch

n2 = n1.shift(batch)

hh2 = c.rolling(window).max()

ll2 = c.rolling(window).min()

n3 = (hh2 - ll2) / window

# calculate fractal dimension

D = (np.log(n1 + n2) - np.log(n3)) / np.log(2)

alp = np.exp(-4.6 * (D - 1))

alp = np.clip(alp, .01, 1).values

filt = c.values

for i, x in enumerate(alp):

cl = c.values[i]

if i < window:

continue

filt[i] = cl * x + (1 - x) * filt[i - 1]

return pd.Series(filt, index=ohlc.index, name="{0} period FRAMA.".format(period))

plt.figure(figsize=(10,6))

data['FRAMA20']=FRAMA(data,period = 20,column = "Close")

data['Close'].plot(label='Close')

data['FRAMA20'].plot(label='FRAMA20')

plt.ylabel('Price USD')

plt.title('NVDA FRAMA20')

plt.legend()

- TradingView:

- The practical application of MAs often involves a tradeoff between the amount of smoothness required and the amount of lag that can be tolerated. MAs have this problem because the price data is not stationary, and may have different bandwidths over different time intervals.

- FRAMA has been developed based on price statistics and the cyclic content of the price data. It rapidly follows significant changes in price but becomes very flat in congestion zones so that bad whipsaw trades can be eliminated.

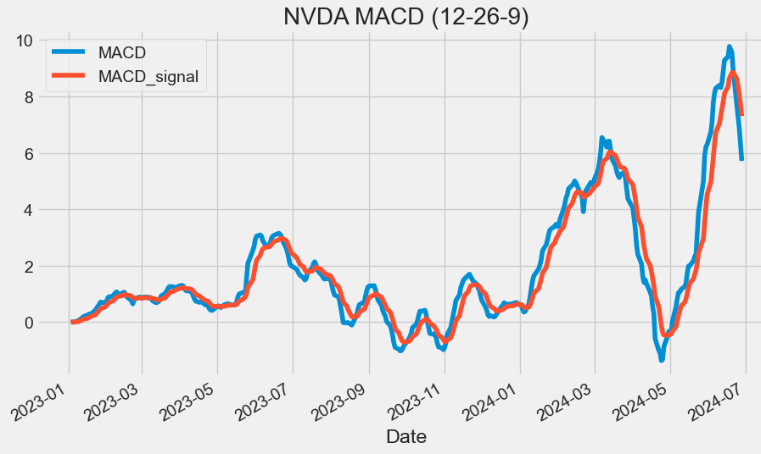

MACD Indicator

- Moving average convergence/divergence (MACD) is a trend-following momentum indicator that helps investors identify price trends, measure trend momentum, and identify market entry points for buying or selling.

def MACD(ohlc, period_fast = 12, period_slow = 26,signal = 9,column = "Close",adjust = True):

"""

MACD, MACD Signal and MACD difference.

The MACD Line oscillates above and below the zero line, which is also known as the centerline.

These crossovers signal that the 12-day EMA has crossed the 26-day EMA. The direction, of course, depends on the direction of the moving average cross.

Positive MACD indicates that the 12-day EMA is above the 26-day EMA. Positive values increase as the shorter EMA diverges further from the longer EMA.

This means upside momentum is increasing. Negative MACD values indicates that the 12-day EMA is below the 26-day EMA.

Negative values increase as the shorter EMA diverges further below the longer EMA. This means downside momentum is increasing.

Signal line crossovers are the most common MACD signals. The signal line is a 9-day EMA of the MACD Line.

As a moving average of the indicator, it trails the MACD and makes it easier to spot MACD turns.

A bullish crossover occurs when the MACD turns up and crosses above the signal line.

A bearish crossover occurs when the MACD turns down and crosses below the signal line.

"""

EMA_fast = pd.Series(

ohlc[column].ewm(ignore_na=False, span=period_fast, adjust=adjust).mean(),

name="EMA_fast",

)

EMA_slow = pd.Series(

ohlc[column].ewm(ignore_na=False, span=period_slow, adjust=adjust).mean(),

name="EMA_slow",

)

MACD = pd.Series(EMA_fast - EMA_slow, name="MACD")

MACD_signal = pd.Series(

MACD.ewm(ignore_na=False, span=signal, adjust=adjust).mean(), name="SIGNAL"

)

return pd.concat([MACD, MACD_signal], axis=1)

plt.figure(figsize=(10,6))

data[["MACD", "MACD_signal"]]=MACD(data, period_fast = 12, period_slow = 26,signal = 9,column = "Close",adjust = True)

data['MACD'].plot(label='MACD')

data['MACD_signal'].plot(label='MACD_signal')

plt.title('NVDA MACD (12-26-9)')

plt.legend()

- Let’s calculate and plot the MACD histograms

# Calculate MACD

short_term = 12

long_term = 26

signal_period = 9

# Calculate short-term and long-term EMAs

short_ema = data['Close'].ewm(span=short_term, adjust=False).mean()

long_ema = data['Close'].ewm(span=long_term, adjust=False).mean()

# Calculate MACD Line

macd_line = short_ema - long_ema

# Calculate Signal Line

signal_line = macd_line.ewm(span=signal_period, adjust=False).mean()

# Calculate MACD Histogram

macd_histogram = macd_line - signal_line

# Add MACD components to the DataFrame

data['MACD12269'] = macd_line

data['Signal12269'] = signal_line

data['Histogram12269'] = macd_histogram

import plotly.graph_objects as go

# Create a Plotly figure

fig = go.Figure()

# MACD and Signal lines

fig.add_trace(go.Scatter(x=data.index, y=data['MACD12269'], mode='lines', name='MACD'))

fig.add_trace(go.Scatter(x=data.index, y=data['Signal12269'], mode='lines', name='Signal'))

# Histogram

fig.add_trace(go.Bar(x=data.index, y=data['Histogram12269'], name='Histogram',

marker_color=['green' if val >= 0 else 'red' for val in data['Histogram12269']]))

# Customize the chart

fig.update_xaxes(rangeslider=dict(visible=False))

fig.update_layout(plot_bgcolor='#efefff', font_family='Monospace', font_color='#000000', font_size=20,width=400)

fig.update_layout(

title="NVDA MACD (12-26-9)"

)

fig.update_layout(

autosize=False,

width=1100,

height=500,

margin=dict(

l=50,

r=50,

b=100,

t=100,

pad=4

),

paper_bgcolor="LightSteelBlue",

)

fig.update_layout(

xaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey'),

yaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey')

)

# Show the chart

fig.show()

- TradingView: MACD can be used to identify aspects of a security’s overall trend. Most notably these aspects are momentum, as well as trend direction and duration.

- The MACD histogram is used as a good indication of a security’s momentum.

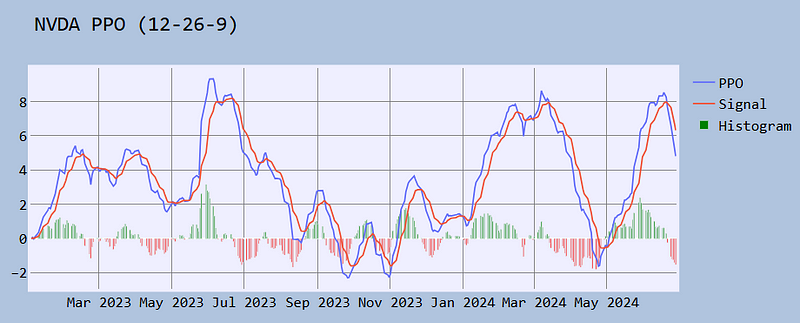

PPO Indicator

- The Percentage Price Oscillator (PPO) is a momentum indicator that gives traders and investors an idea of when the trend may change. It does this by taking the difference between two moving averages and expressing it as a percentage, which makes identifying potential entry points easier.

def PPO(ohlc,

period_fast = 12,

period_slow = 26,

signal = 9,

column = "Close",

adjust = True):

"""

Percentage Price Oscillator

PPO, PPO Signal and PPO difference.

As with MACD, the PPO reflects the convergence and divergence of two moving averages.

While MACD measures the absolute difference between two moving averages, PPO makes this a relative value by dividing the difference by the slower moving average

"""

EMA_fast = pd.Series(

ohlc[column].ewm(ignore_na=False, span=period_fast, adjust=adjust).mean(),

name="EMA_fast",

)

EMA_slow = pd.Series(

ohlc[column].ewm(ignore_na=False, span=period_slow, adjust=adjust).mean(),

name="EMA_slow",

)

PPO = pd.Series(((EMA_fast - EMA_slow) / EMA_slow) * 100, name="PPO")

PPO_signal = pd.Series(

PPO.ewm(ignore_na=False, span=signal, adjust=adjust).mean(), name="SIGNAL"

)

PPO_histo = pd.Series(PPO - PPO_signal, name="HISTO")

return pd.concat([PPO, PPO_signal, PPO_histo], axis=1)

data[["PPO", "PPO_signal","PPO_histo"]]=PPO(data, period_fast = 12, period_slow = 26,signal = 9,column = "Close",adjust = True)- Plotting the NVDA PPO (12–26–9) signal & histogram

import plotly.graph_objects as go

# Create a Plotly figure

fig = go.Figure()

# MACD and Signal lines

fig.add_trace(go.Scatter(x=data.index, y=data['PPO'], mode='lines', name='PPO'))

fig.add_trace(go.Scatter(x=data.index, y=data['PPO_signal'], mode='lines', name='Signal'))

# Histogram

fig.add_trace(go.Bar(x=data.index, y=data['PPO_histo'], name='Histogram',

marker_color=['green' if val >= 0 else 'red' for val in data['PPO_histo']]))

# Customize the chart

fig.update_xaxes(rangeslider=dict(visible=False))

fig.update_layout(plot_bgcolor='#efefff', font_family='Monospace', font_color='#000000', font_size=20,width=400)

fig.update_layout(

title="NVDA PPO (12-26-9)"

)

fig.update_layout(

autosize=False,

width=1100,

height=500,

margin=dict(

l=50,

r=50,

b=100,

t=100,

pad=4

),

paper_bgcolor="LightSteelBlue",

)

fig.update_layout(

xaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey'),

yaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey')

)

# Show the chart

fig.show()

There are two main reasons for using the PPO:

- With the PPO, it is possible to compare Price Oscillator levels from one symbol to the next. A PPO reading of +5% means that the shorter MA is 5% higher than the longer MA.

- The PPO is a better representation of the two MAs relative to each other. The difference between the two MAs is shown in relation to the shorter moving average.

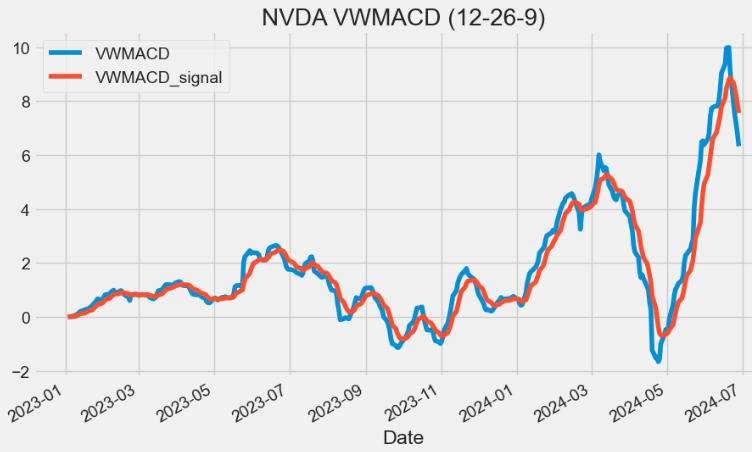

VWMACD Indicator

- The Volume-Weighted MACD (VWMACD) is an amendment to the original Moving Average Convergence Divergence (MACD) indicator discussed above. Instead of calculating the difference between two EMAs this tool uses volume-weighted moving averages.

- VWMACD represents the convergence and divergence of volume weighted average price trends. The use of volume makes this indicator more sensitive and reliable than the traditional MACD v.s.

def VW_MACD(ohlcv,period_fast = 12,period_slow = 26,signal = 9,column = "Close", colvol = "Volume", adjust = True):

""""Volume-Weighted MACD" is an indicator that shows how a volume-weighted moving average can be used to calculate moving average convergence/divergence (MACD).

This technique was first used by Buff Dormeier, CMT, and has been written about since at least 2002."""

vp = ohlcv[colvol] * ohlcv[column]

_fast = pd.Series(

(vp.ewm(ignore_na=False, span=period_fast, adjust=adjust).mean())

/ (

ohlcv[colvol]

.ewm(ignore_na=False, span=period_fast, adjust=adjust)

.mean()

),

name="_fast",

)

_slow = pd.Series(

(vp.ewm(ignore_na=False, span=period_slow, adjust=adjust).mean())

/ (

ohlcv[colvol]

.ewm(ignore_na=False, span=period_slow, adjust=adjust)

.mean()

),

name="_slow",

)

MACD = pd.Series(_fast - _slow, name="MACD")

MACD_signal = pd.Series(

MACD.ewm(ignore_na=False, span=signal, adjust=adjust).mean(), name="SIGNAL"

)

return pd.concat([MACD, MACD_signal], axis=1)

plt.figure(figsize=(10,6))

data[["VWMACD", "VWMACD_signal"]]=VW_MACD(data, period_fast = 12, period_slow = 26,signal = 9,column = "Close",colvol = "Volume",adjust = True)

data['VWMACD'].plot(label='VWMACD')

data['VWMACD_signal'].plot(label='VWMACD_signal')

plt.title('NVDA VWMACD (12-26-9)')

plt.legend()

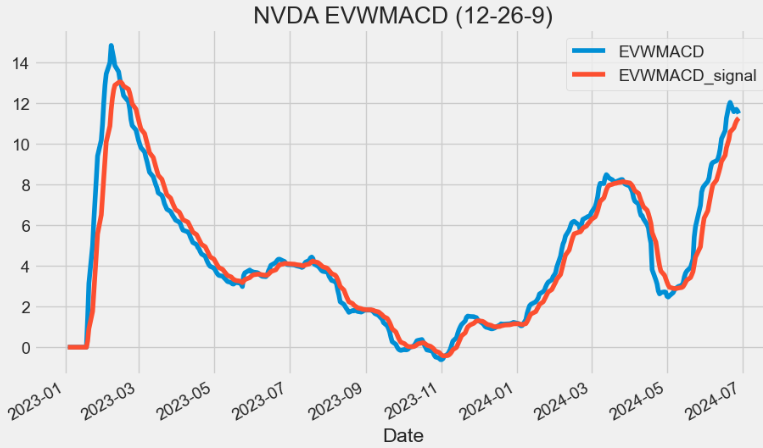

EVWMACD Indicator

- The Elastic Volume Weighted MACD (EVWMACD) is a variation of standard MACD. The Difference is that EVWMACD applies the formula of standard MACD with the eVWMA v.s.

def EV_MACD(ohlcv,period_fast = 20,period_slow = 40,signal = 9,adjust = True ):

"""

Elastic Volume Weighted MACD is a variation of standard MACD,

calculated using two EVWMA's.

:period_slow: Specifies the number of Periods used for the slow EVWMA calculation

:period_fast: Specifies the number of Periods used for the fast EVWMA calculation

:signal: Specifies the number of Periods used for the signal calculation

"""

evwma_slow = EVWMA(ohlcv, period_slow)

evwma_fast = EVWMA(ohlcv, period_fast)

MACD = pd.Series(evwma_fast - evwma_slow, name="MACD")

MACD_signal = pd.Series(

MACD.ewm(ignore_na=False, span=signal, adjust=adjust).mean(), name="SIGNAL"

)

return pd.concat([MACD, MACD_signal], axis=1)

plt.figure(figsize=(10,6))

data[["EVMACD", "EVMACD_signal"]]=EV_MACD(data, period_fast = 12, period_slow = 26,signal = 9,adjust = True)

data['EVMACD'].plot(label='EVWMACD')

data['EVMACD_signal'].plot(label='EVWMACD_signal')

plt.title('NVDA EVWMACD (12-26-9)')

plt.legend()

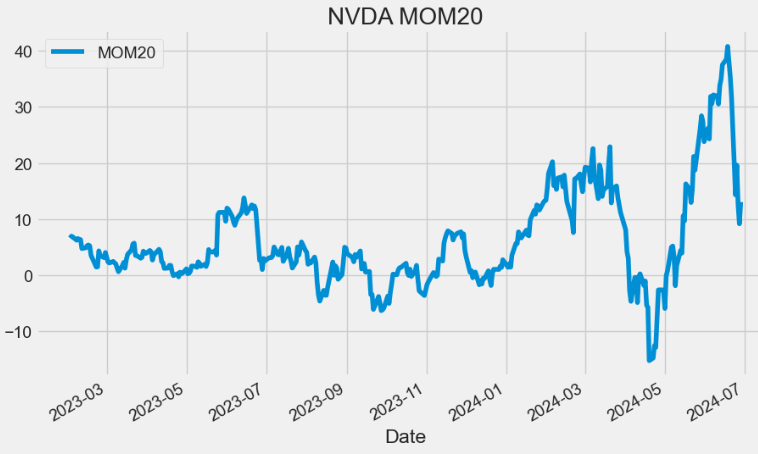

MOM Indicator

- Market Momentum (MOM) can be used as a measure of overall market sentiment that can support buying and selling with and against market trends.

def MOM(ohlc, period = 10, column = "Close"):

"""Market momentum is measured by continually taking price differences for a fixed time interval.

To construct a 10-day momentum line, simply subtract the closing price 10 days ago from the last closing price.

This positive or negative value is then plotted around a zero line."""

return pd.Series(ohlc[column].diff(period), name="MOM".format(period))

plt.figure(figsize=(10,6))

data["MOM20"]=MOM(data, period = 20, column = "Close")

data['MOM20'].plot(label='MOM20')

plt.title('NVDA MOM20')

plt.legend()

- The MOM signal indicates when an asset’s price has moved too far in one direction and is likely to reverse. For example, the above plot shows that MOM20 generates overbought signals when the reading rises above 20 and signals oversold conditions when the reading falls below 10.

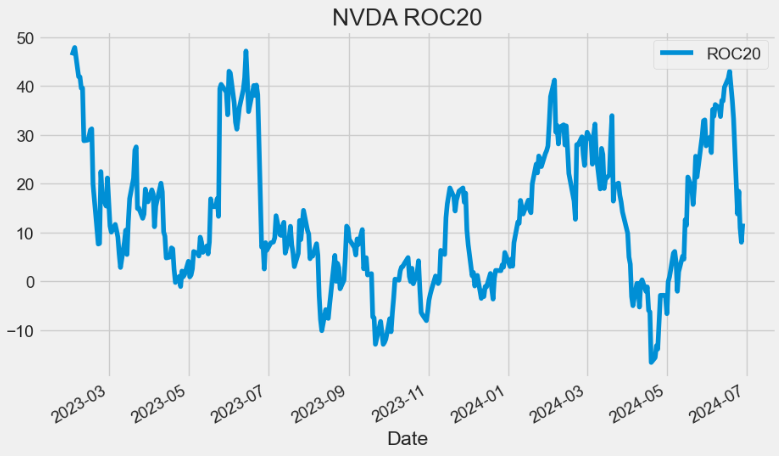

ROC Indicator

- The Price Rate of Change (ROC) is a momentum-based technical indicator that measures the percentage change in price between the current price and the price a certain number of periods ago. The ROC indicator is plotted against zero, with the indicator moving upwards into positive territory if price changes are to the upside, and moving into negative territory if price changes are to the downside.

def ROC(ohlc, period = 12, column = "Close"):

"""The Rate-of-Change (ROC) indicator, which is also referred to as simply Momentum,

is a pure momentum oscillator that measures the percent change in price from one period to the next.

The ROC calculation compares the current price with the price “n” periods ago."""

return pd.Series(

(ohlc[column].diff(period) / ohlc[column].shift(period)) * 100, name="ROC"

)

plt.figure(figsize=(10,6))

data["ROC20"]=ROC(data, period = 20, column = "Close")

data['ROC20'].plot(label='ROC20')

plt.title('NVDA ROC20')

plt.legend()

- Reading the ROC Indicator: When indicator values hover around zero, it will denote a consolidating market. A reading above zero will imply a bullish sentiment in the market; whereas a reading below zero will imply a bearish sentiment in the market.

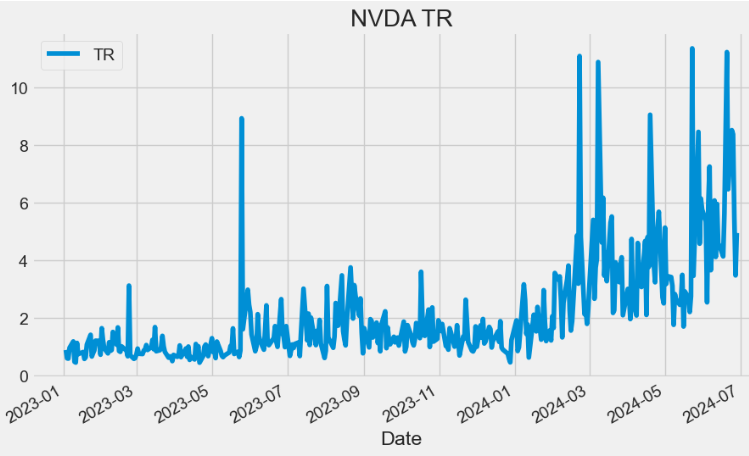

TR Indicator

- True Range (TR) measures the daily range plus any gap from the closing price of the preceding day.

- TR is defined as the largest of the following:

- The distance from today’s high to today’s low.

- The distance from yesterday’s close to today’s high.

- The distance from yesterday’s close to today’s low.

def TR(ohlc,high="High",low="Low",close="Close"):

"""True Range is the maximum of three price ranges.

Most recent period's high minus the most recent period's low.

Absolute value of the most recent period's high minus the previous close.

Absolute value of the most recent period's low minus the previous close."""

TR1 = pd.Series(ohlc[high] - ohlc[low]).abs() # True Range = High less Low

TR2 = pd.Series(

ohlc[high] - ohlc[close].shift()

).abs() # True Range = High less Previous Close

TR3 = pd.Series(

ohlc[close].shift() - ohlc[low]

).abs() # True Range = Previous Close less Low

_TR = pd.concat([TR1, TR2, TR3], axis=1)

_TR["TR"] = _TR.max(axis=1)

return pd.Series(_TR["TR"], name="TR")

plt.figure(figsize=(10,6))

data['TR']=TR(data,high="High",low="Low",close="Close")

data['TR'].plot(label='TR')

plt.title('NVDA TR')

plt.legend()

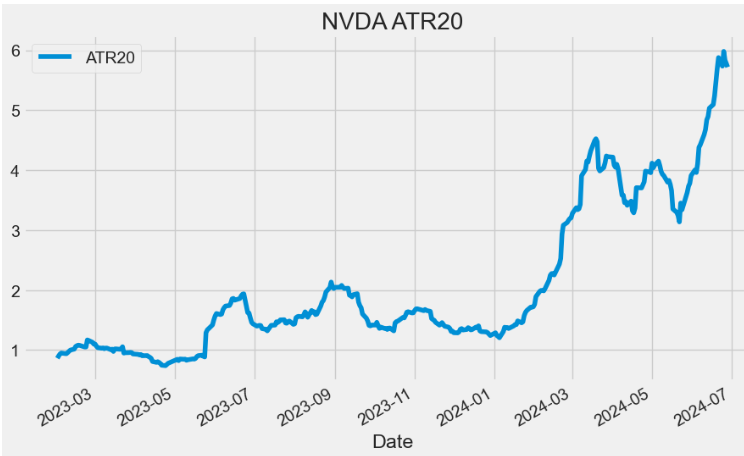

ATR Indicator

- Average True Range (ATR) is the average of TR over the specified period. ATR measures volatility, taking into account any gaps in the price movement.

def ATR(ohlc, period = 14,high="High",low="Low",close="Close"):

"""Average True Range is moving average of True Range."""

mytr=TR(ohlc,high=high,low=low,close=close)

return pd.Series(

mytr.rolling(center=False, window=period).mean(),

name="{0} period ATR".format(period),

)

plt.figure(figsize=(10,6))

data['ATR20']=ATR(data, period = 20,high="High",low="Low",close="Close")

data['ATR20'].plot(label='ATR20')

plt.title('NVDA ATR20')

plt.legend(loc='upper left')

- An expanding ATR indicates increased volatility in the market, with the range of each bar getting larger. A reversal in price with an increase in ATR would indicate strength behind that move. ATR is not directional so an expanding ATR can indicate selling pressure or buying pressure. High ATR values usually result from a sharp advance or decline and are unlikely to be sustained for extended periods.

- A low ATR value indicates a series of periods with small ranges (quiet days). These low ATR values are found during extended sideways price action, thus the lower volatility. A prolonged period of low ATR values may indicate a consolidation area and the possibility of a continuation move or reversal.

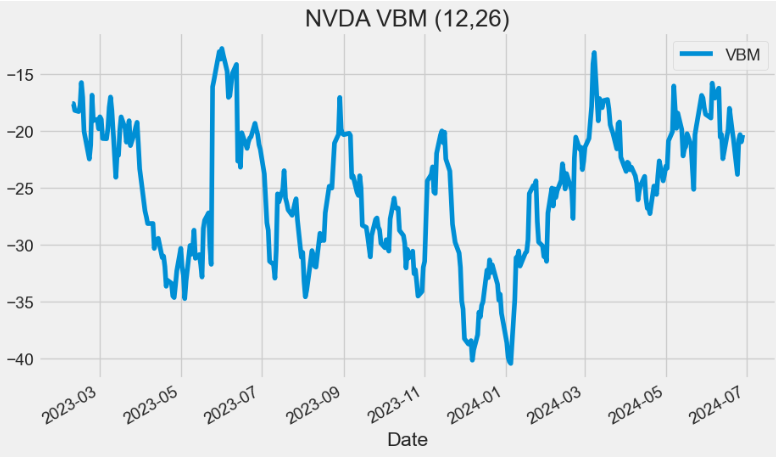

VBM Indicator

- The Volatility Based Momentum (VBM) indicator is a variation on the ROC indicator v.s.

- VBM expresses momentum in a normalized, universally applicable ‘multiples of volatility’ (MoV) unit.

def VBM(ohlc,roc_period = 12,atr_period = 26,high="High",low="Low",column = "Close"):

"""The Volatility-Based-Momentum (VBM) indicator, The calculation for a volatility based momentum (VBM)

indicator is very similar to ROC, but divides by the security’s historical volatility instead.

The average true range indicator (ATR) is used to compute historical volatility.

VBM(n,v) = (Close — Close n periods ago) / ATR(v periods)

"""

return pd.Series(

(

(ohlc[column].diff(roc_period) - ohlc[column].shift(roc_period))

/ ATR(ohlc, period = atr_period,high=high,low=low,close=column)

),

name="VBM",

)

plt.figure(figsize=(10,6))

data["VBM"]=VBM(data,roc_period = 12,atr_period = 26,high="High",low="Low",column = "Close")

data['VBM'].plot(label='VBM')

plt.title('NVDA VBM (12,26)')

plt.legend()

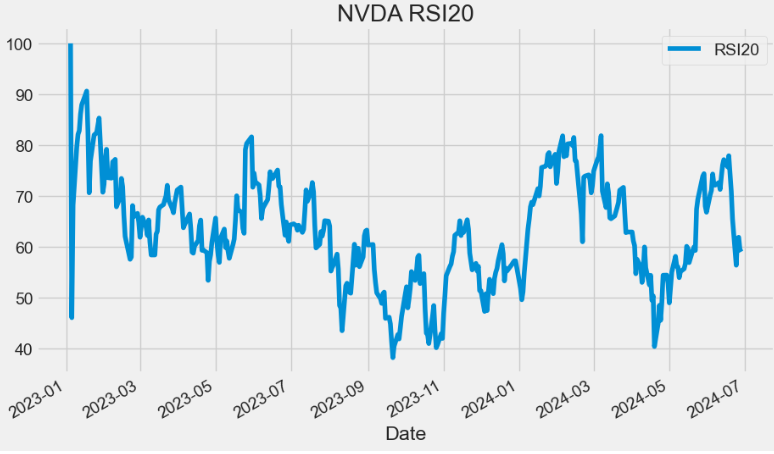

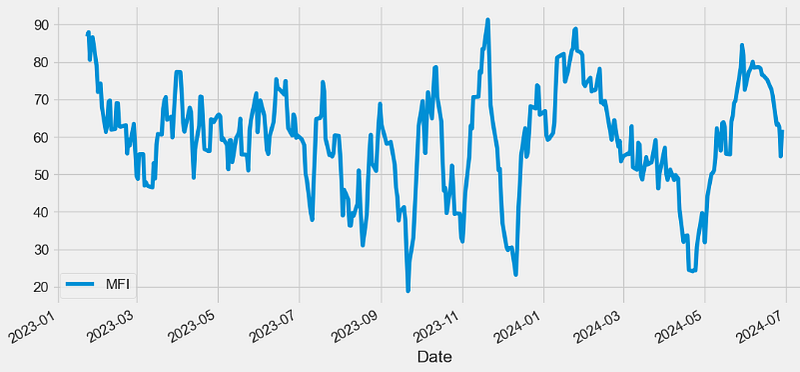

RSI Indicator

- The relative strength index (RSI) is a momentum indicator used in technical analysis. RSI measures the speed and magnitude of a security’s recent price changes to evaluate overvalued or undervalued conditions in the price of that security.

- The RSI is displayed as an oscillator (a line graph below) on a scale of zero to 100. Readings below 30 generally indicate that the stock is oversold, while readings above 70 indicate that it is overbought.

def RSI(ohlc, period = 14, column = "Close", adjust = True):

"""Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements.

RSI oscillates between zero and 100. Traditionally, and according to Wilder, RSI is considered overbought when above 70 and oversold when below 30.

Signals can also be generated by looking for divergences, failure swings and centerline crossovers.

RSI can also be used to identify the general trend."""

## get the price diff

delta = ohlc[column].diff()

## positive gains (up) and negative gains (down) Series

up, down = delta.copy(), delta.copy()

up[up < 0] = 0

down[down > 0] = 0

# EMAs of ups and downs

_gain = up.ewm(alpha=1.0 / period, adjust=adjust).mean()

_loss = down.abs().ewm(alpha=1.0 / period, adjust=adjust).mean()

RS = _gain / _loss

return pd.Series(100 - (100 / (1 + RS)), name="{0} period RSI".format(period))

plt.figure(figsize=(10,6))

data["RSI20"]=RSI(data, period = 20, column = "Close", adjust = True)

data['RSI20'].plot(label='RSI20')

plt.title('NVDA RSI20')

plt.legend()

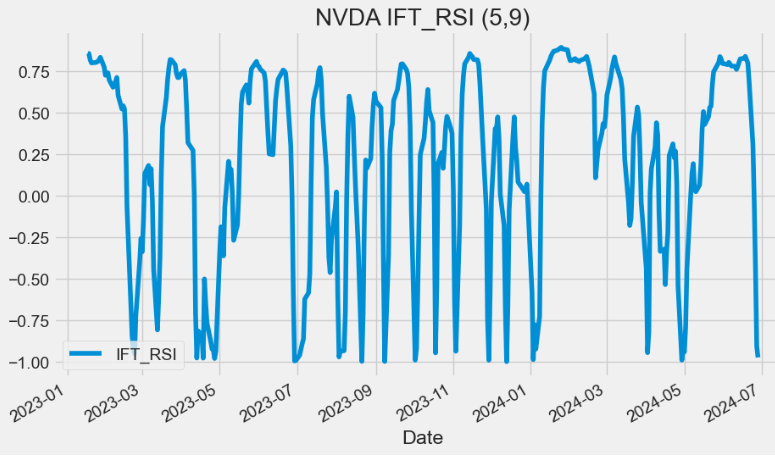

IFT RSI Indicator

- Inverse Fisher Transform with RSI (IFT RSI) is a variation of the Inverse Fisher Transform (IFT) oscillator, where the RSI indicator values are taken as intermediate values.

def IFT_RSI(ohlc,column = "Close",rsi_period = 5,wma_period = 9, adjust=True):

"""Modified Inverse Fisher Transform applied on RSI.

Suggested method to use any IFT indicator is to buy when the indicator crosses over –0.5 or crosses over +0.5

if it has not previously crossed over –0.5 and to sell short when the indicators crosses under +0.5 or crosses under –0.5

if it has not previously crossed under +0.5."""

v1 = pd.Series(0.1 * (RSI(ohlc, rsi_period,column = column, adjust = adjust) - 50), name="v1")

d = (wma_period * (wma_period + 1)) / 2 # denominator

weights = np.arange(1, wma_period + 1)

def linear(w):

def _compute(x):

return (w * x).sum() / d

return _compute

_wma = v1.rolling(wma_period, min_periods=wma_period)

v2 = _wma.apply(linear(weights), raw=True)

ift = pd.Series(((v2 ** 2 - 1) / (v2 ** 2 + 1)), name="IFT_RSI")

return ift

plt.figure(figsize=(10,6))

data["IFTRSI"]=IFT_RSI(data,column = "Close",rsi_period = 5,wma_period = 9, adjust=True)

data['IFTRSI'].plot(label='IFT_RSI')

plt.title('NVDA IFT_RSI (5,9)')

plt.legend()

- The IFT RSI gives buy and sell signals (although the sell signals are a little late). This can be used stand alone or with other indicators to add additional confirmation in either direction.

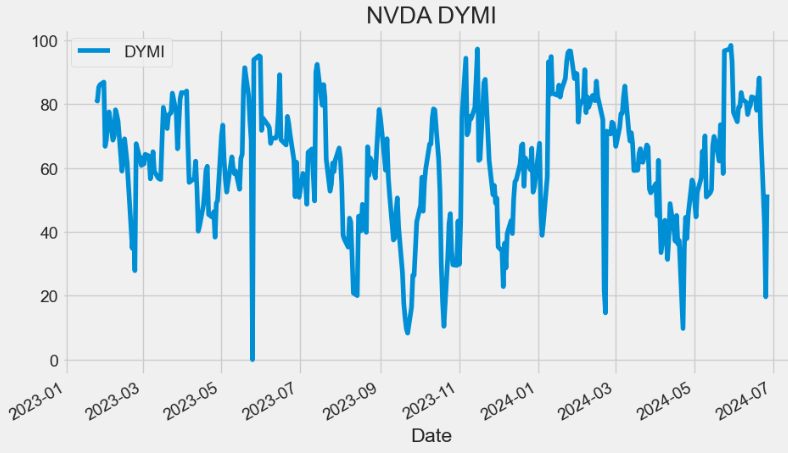

DYMI Indicator

- The dynamic momentum index (DYMI) is an overbought/oversold indicator that uses fewer periods in its calculation when volatility is high, and more periods when volatility is low.

- The indicator oscillates between 0 and 100. When the indicator is below 30 the price of the asset is considered oversold and when its above 70, the price is considered overbought.

def DYMI(ohlc, column = "Close", adjust = True):

"""

The Dynamic Momentum Index is a variable term RSI. The RSI term varies from 3 to 30. The variable

time period makes the RSI more responsive to short-term moves. The more volatile the price is,

the shorter the time period is. It is interpreted in the same way as the RSI, but provides signals earlier.

Readings below 30 are considered oversold, and levels over 70 are considered overbought. The indicator

oscillates between 0 and 100.

https://www.investopedia.com/terms/d/dynamicmomentumindex.asp

"""

def _get_time(close):

# Value available from 14th period

sd = close.rolling(5).std()

asd = sd.rolling(10).mean()

v = sd / asd

t = 14 / v.round()

t[t.isna()] = 0

t = t.map(lambda x: int(min(max(x, 5), 30)))

return t

def _dmi(index):

time = t.iloc[index]

if (index - time) < 0:

subset = ohlc.iloc[0:index]

else:

subset = ohlc.iloc[(index - time) : index]

return RSI(subset, period=time, column = column,adjust=adjust).values[-1]

dates = pd.Series(ohlc.index)

periods = pd.Series(data=range(14, len(dates)), index=ohlc.index[14:].values)

t = _get_time(ohlc[column])

return periods.map(lambda x: _dmi(x))

plt.figure(figsize=(10,6))

data["DYMI"]=DYMI(data, column = "Close", adjust = True)

data['DYMI'].plot(label='DYMI')

plt.title('NVDA DYMI')

plt.legend()

- Read more here.

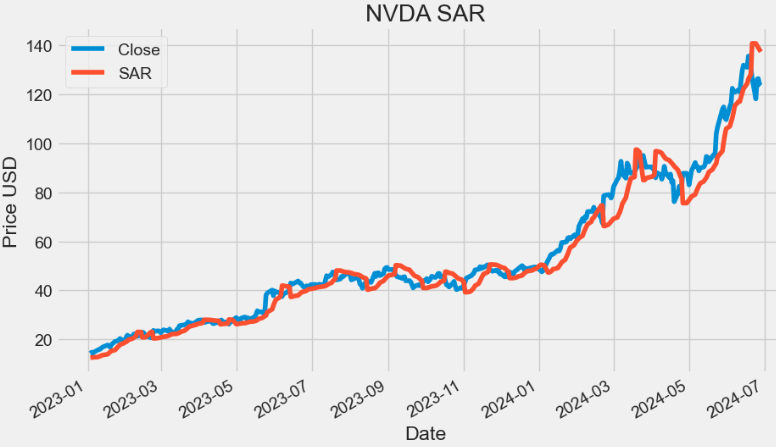

SAR Indicator

- Stop and Reverse (SAR) is a trailing stop-based trading system; it is often used as an indicator as well.

def SAR(ohlc, af = 0.02, amax = 0.2,high="High",low="Low"):

"""SAR stands for “stop and reverse,” which is the actual indicator used in the system.

SAR trails price as the trend extends over time. The indicator is below prices when prices are rising and above prices when prices are falling.

In this regard, the indicator stops and reverses when the price trend reverses and breaks above or below the indicator."""

high1, low1 = ohlc[high], ohlc[low]

# Starting values

sig0, xpt0, af0 = True, high1[0], af

_sar = [low1[0] - (high1 - low1).std()]

for i in range(1, len(ohlc)):

sig1, xpt1, af1 = sig0, xpt0, af0

lmin = min(low1[i - 1], low1[i])

lmax = max(high1[i - 1], high1[i])

if sig1:

sig0 = low1[i] > _sar[-1]

xpt0 = max(lmax, xpt1)

else:

sig0 = high1[i] >= _sar[-1]

xpt0 = min(lmin, xpt1)

if sig0 == sig1:

sari = _sar[-1] + (xpt1 - _sar[-1]) * af1

af0 = min(amax, af1 + af)

if sig0:

af0 = af0 if xpt0 > xpt1 else af1

sari = min(sari, lmin)

else:

af0 = af0 if xpt0 < xpt1 else af1

sari = max(sari, lmax)

else:

af0 = af

sari = xpt0

_sar.append(sari)

return pd.Series(_sar, index=ohlc.index)

plt.figure(figsize=(10,6))

data["SAR"]=SAR(data, af = 0.02, amax = 0.2,high="High",low="Low")

data['Close'].plot(label='Close')

data['SAR'].plot(label='SAR')

plt.ylabel('Price USD')

plt.title('NVDA SAR')

plt.legend()

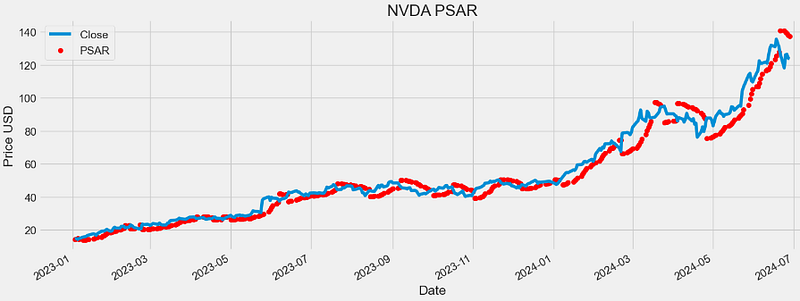

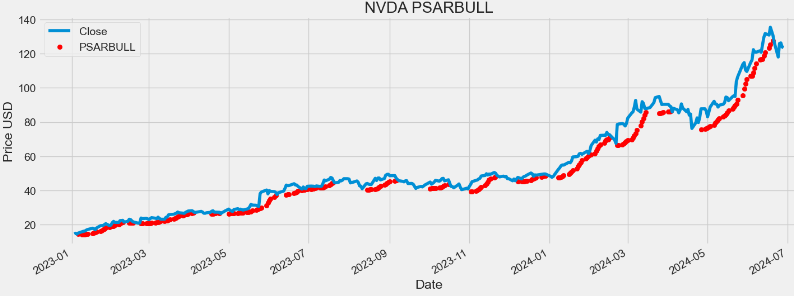

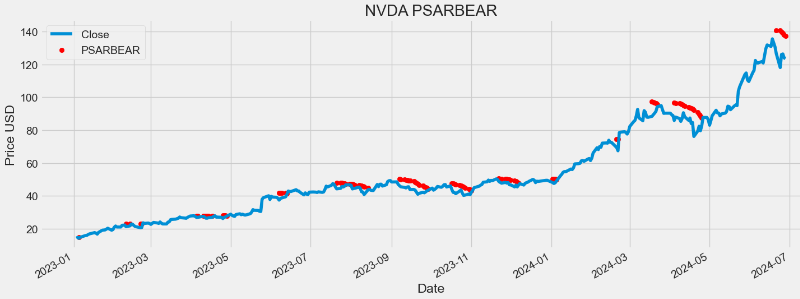

PSAR Indicator

- As a technical indicator, Parabolic SAR (PSAR) is known as a momentum indicator and used to identify potential trend reversals when the price is in a strong uptrend or downtrend.

- Parabolic SAR displays a series of dots v.i. that are placed either above or below the price, depending on the trend.

- If the dot switches its placement, a signal is generated that the current trend is most likely coming to an end, thus giving us a hint to close any open positions.

def PSAR(ohlc, iaf = 0.02, maxaf = 0.2,high="High",low="Low",close="Close"):

"""

The parabolic SAR indicator, developed by J. Wells Wilder, is used by traders to determine trend direction and potential reversals in price.

The indicator uses a trailing stop and reverse method called "SAR," or stop and reverse, to identify suitable exit and entry points.

Traders also refer to the indicator as the parabolic stop and reverse, parabolic SAR, or PSAR.

https://www.investopedia.com/terms/p/parabolicindicator.asp

https://virtualizedfrog.wordpress.com/2014/12/09/parabolic-sar-implementation-in-python/

"""

length = len(ohlc)

high1, low1, close1 = ohlc[high], ohlc[low], ohlc[close]

psar = close1[0 : len(close1)]

psarbull = [None] * length

psarbear = [None] * length

bull = True

af = iaf

hp = high1[0]

lp = low1[0]

for i in range(2, length):

if bull:

psar[i] = psar[i - 1] + af * (hp - psar[i - 1])

else:

psar[i] = psar[i - 1] + af * (lp - psar[i - 1])

reverse = False

if bull:

if low1[i] < psar[i]:

bull = False

reverse = True

psar[i] = hp

lp = low1[i]

af = iaf

else:

if high1[i] > psar[i]:

bull = True

reverse = True

psar[i] = lp

hp = high1[i]

af = iaf

if not reverse:

if bull:

if high1[i] > hp:

hp = high1[i]

af = min(af + iaf, maxaf)

if low1[i - 1] < psar[i]:

psar[i] = low1[i - 1]

if low1[i - 2] < psar[i]:

psar[i] = low1[i - 2]

else:

if low1[i] < lp:

lp = low1[i]

af = min(af + iaf, maxaf)

if high1[i - 1] > psar[i]:

psar[i] = high1[i - 1]

if high1[i - 2] > psar[i]:

psar[i] = high1[i - 2]

if bull:

psarbull[i] = psar[i]

else:

psarbear[i] = psar[i]

psar = pd.Series(psar, name="psar", index=ohlc.index)

psarbear = pd.Series(psarbear, name="psarbear", index=ohlc.index)

psarbull = pd.Series(psarbull, name="psarbull", index=ohlc.index)

return pd.concat([psar, psarbull, psarbear], axis=1)

data[["PSAR", "PSARBULL", "PSARBEAR"]]=PSAR(data, iaf = 0.02, maxaf = 0.2,high="High",low="Low",close="Close")- Reading the input stock data

symbols = ['NVDA']

start_date = '2023-01-01'

data0 = yf.download(symbols, start=start_date)

data["Close"]=data0["Close"]

data0.tail()

[*********************100%%**********************] 1 of 1 completed

Open High Low Close Adj Close Volume

Date

2024-06-24 123.239998 124.459999 118.040001 118.110001 118.110001 476060900

2024-06-25 121.199997 126.500000 119.320000 126.089996 126.089996 425787500

2024-06-26 126.129997 128.119995 122.599998 126.400002 126.400002 362975900

2024-06-27 124.099998 126.410004 122.919998 123.989998 123.989998 252571700

2024-06-28 124.580002 127.709999 122.750000 123.540001 123.540001 314945500- Plotting PSAR

plt.figure(figsize=(16,6))

data['Close'].plot(label='Close')

plt.scatter(data0.index,data['PSAR'],c='r',label='PSAR')

plt.ylabel('Price USD')

plt.title('NVDA PSAR')

plt.legend()

- Plotting PSARBULL

plt.figure(figsize=(16,6))

data['Close'].plot(label='Close')

plt.scatter(data0.index,data['PSARBULL'],c='r',label='PSARBULL')

plt.ylabel('Price USD')

plt.title('NVDA PSARBULL')

plt.legend()

- Plotting PSARBEAR

plt.figure(figsize=(16,6))

data['Close'].plot(label='Close')

plt.scatter(data0.index,data['PSARBEAR'],c='r',label='PSARBEAR')

plt.ylabel('Price USD')

plt.title('NVDA PSARBEAR')

plt.legend()

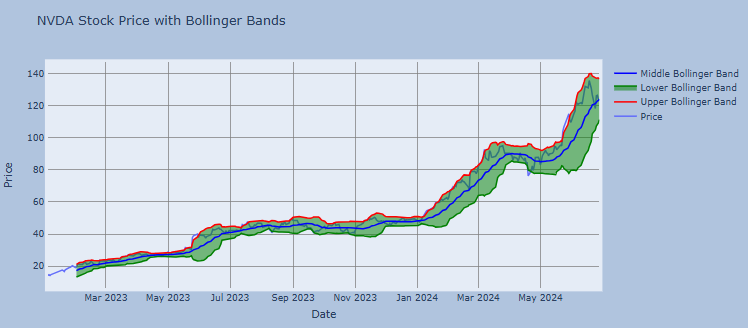

BB Indicator

- Bollinger Bands (BB) is a technical analysis tool used to determine where prices are high and low relative to each other.

- BB are composed of three lines: SMA (the middle band), upper band (UB) and lower band (LB).

- UB and LB are typically two standard deviations (2*SD) above or below SMA20.

- BB widen and narrow as the volatility of the underlying asset changes.

data0['SMA'] = data0['Close'].rolling(window=20).mean()

# Calculate the 20-period Standard Deviation (SD)

data0['SD'] = data0['Close'].rolling(window=20).std()

# Calculate the Upper Bollinger Band (UB) and Lower Bollinger Band (LB)

data0['UB'] = data0['SMA'] + 2 * data0['SD']

data0['LB'] = data0['SMA'] - 2 * data0['SD']import plotly.graph_objs as go

# Create a Plotly figure

fig = go.Figure()

# Add the price chart

fig.add_trace(go.Scatter(x=data0.index, y=data0['Close'], mode='lines', name='Price'))

# Add the Upper Bollinger Band (UB) and shade the area

fig.add_trace(go.Scatter(x=data0.index, y=data0['UB'], mode='lines', name='Upper Bollinger Band', line=dict(color='red')))

fig.add_trace(go.Scatter(x=data0.index, y=data0['LB'], fill='tonexty', mode='lines', name='Lower Bollinger Band', line=dict(color='green')))

# Add the Middle Bollinger Band (MA)

fig.add_trace(go.Scatter(x=data0.index, y=data0['SMA'], mode='lines', name='Middle Bollinger Band', line=dict(color='blue')))

# Customize the chart layout

fig.update_layout(title='NVDA Stock Price with Bollinger Bands',

xaxis_title='Date',

yaxis_title='Price',

showlegend=True)

fig.update_layout(

autosize=False,

width=1000,

height=500,

margin=dict(

l=50,

r=50,

b=100,

t=100,

pad=4

),

paper_bgcolor="LightSteelBlue",

)

# Show the chart

fig.update_layout(

xaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey'),

yaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey')

)

fig.show()

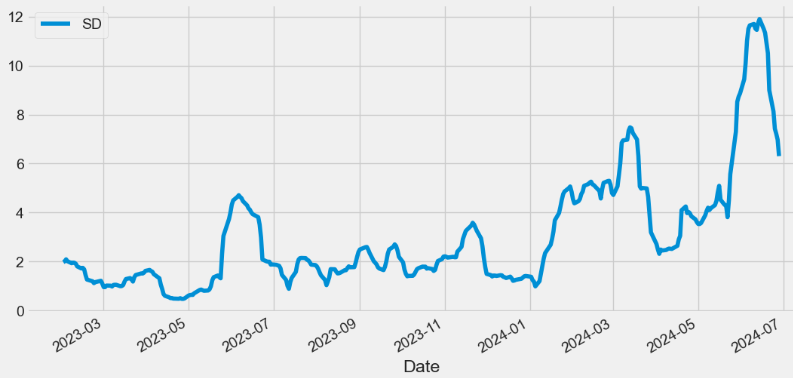

- Examining the stock volatility

data0['SD'].plot(label='SD')

plt.legend()

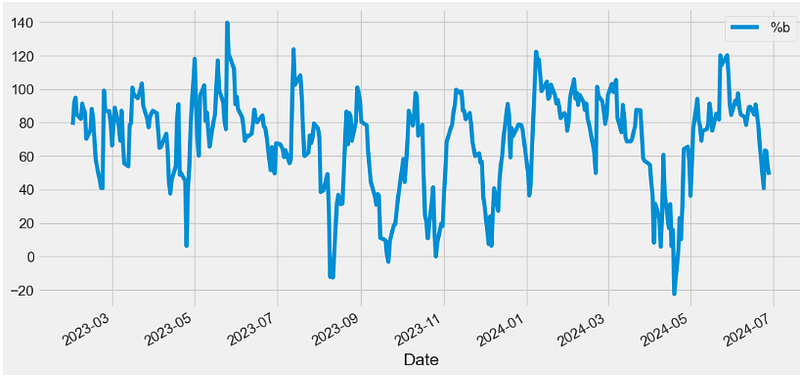

- The Percent B (%B) indicator reflects closing price as a percentage of the lower and upper BB.

percent_b = pd.Series(

100*(data0['Close'] - data0['LB']) / (data0['UB'] - data0['LB']),

name="%b"

)

percent_b.plot(label='%b')

plt.legend()

- Close=UB, %b=100

- Close>UB, %b>100

- Close=SMA, %b=50

- Close=LB, %b=0

- Close

KC Indicator

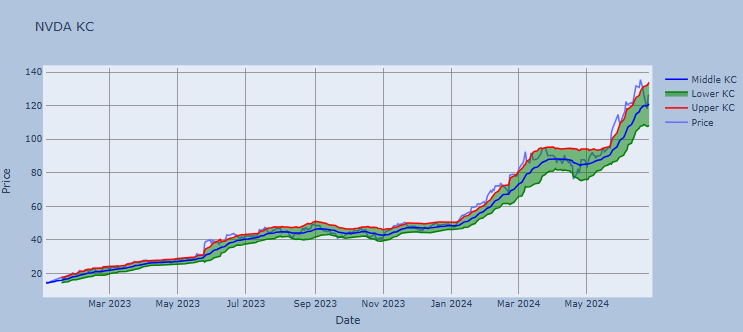

- Keltner Channels (KC) are volatility-based bands that are placed on either side of an asset’s price and can aid in determining the direction of a trend.

def KC(ohlc,period = 20,atr_period = 10,kc_mult = 2,high="High",low="Low",column="Close",adjust=True):

"""Keltner Channels [KC] are volatility-based envelopes set above and below an exponential moving average.

This indicator is similar to Bollinger Bands, which use the standard deviation to set the bands.

Instead of using the standard deviation, Keltner Channels use the Average True Range (ATR) to set channel distance.

The channels are typically set two Average True Range values above and below the 20-day EMA.

The exponential moving average dictates direction and the Average True Range sets channel width.

Keltner Channels are a trend following indicator used to identify reversals with channel breakouts and channel direction.

Channels can also be used to identify overbought and oversold levels when the trend is flat."""

middle = pd.Series(EMA(ohlc, period=period, column=column,adjust=adjust), name="KC_MIDDLE")

up = pd.Series(middle + (kc_mult * ATR(ohlc, period = atr_period,high=high,low=low,close=column)), name="KC_UPPER")

down = pd.Series(

middle - (kc_mult * ATR(ohlc, period = atr_period,high=high,low=low,close=column)), name="KC_LOWER"

)

return pd.concat([middle, up, down], axis=1)

data0[["KC_MIDDLE", "KC_UPPER","KC_LOWER"]]=KC(data0,period = 20,atr_period = 10,kc_mult = 2,high="High",low="Low",column="Close",adjust=True)- Plotting KC

import plotly.graph_objs as go

# Create a Plotly figure

fig = go.Figure()

# Add the price chart

fig.add_trace(go.Scatter(x=data0.index, y=data0['Close'], mode='lines', name='Price'))

# Add the Upper KC and shade the area

fig.add_trace(go.Scatter(x=data0.index, y=data0['KC_UPPER'], mode='lines', name='Upper KC', line=dict(color='red')))

fig.add_trace(go.Scatter(x=data0.index, y=data0['KC_LOWER'], fill='tonexty', mode='lines', name='Lower KC', line=dict(color='green')))

# Add the Middle KC

fig.add_trace(go.Scatter(x=data0.index, y=data0['KC_MIDDLE'], mode='lines', name='Middle KC', line=dict(color='blue')))

# Customize the chart layout

fig.update_layout(title='NVDA KC',

xaxis_title='Date',

yaxis_title='Price',

showlegend=True)

fig.update_layout(

autosize=False,

width=1000,

height=500,

margin=dict(

l=50,

r=50,

b=100,

t=100,

pad=4

),

paper_bgcolor="LightSteelBlue",

)

# Show the chart

fig.update_layout(

xaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey'),

yaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey')

)

fig.show()

- Price reaching KC_UPPER is bullish while reaching KC_LOWER is bearish.

- The angle of the KC also aids in identifying the trend direction. The price may also oscillate between the upper and lower KC bands, which can be interpreted as resistance and support levels.

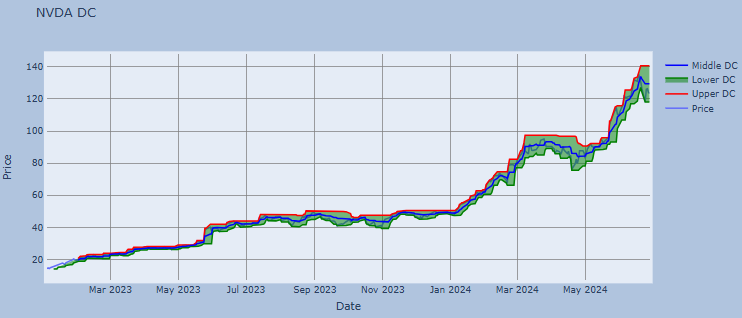

DC Indicator

- Donchian Channels (DC) are used in technical analysis to measure a market’s volatility. It is a banded indicator, similar to BB. Besides measuring a market’s volatility, DC are primarily used to identify potential breakouts or overbought/oversold conditions when price reaches either the Upper or Lower Band. These instances would indicate possible trading signals.

def DC(ohlc, upper_period = 20, lower_period = 5,high="High",low="Low"):

"""Donchian Channel, a moving average indicator developed by Richard Donchian.

It plots the highest high and lowest low over the last period time intervals."""

upper = pd.Series(

ohlc[high].rolling(center=False, window=upper_period).max(), name="UPPER"

)

lower = pd.Series(

ohlc[low].rolling(center=False, window=lower_period).min(), name="LOWER"

)

middle = pd.Series((upper + lower) / 2, name="MIDDLE")

return pd.concat([lower, middle, upper], axis=1)

data0[["DC_L", "DC_M","DC_U"]]=DC(data0, upper_period = 20, lower_period = 5,high="High",low="Low")- Plotting DC

import plotly.graph_objs as go

# Create a Plotly figure

fig = go.Figure()

# Add the price chart

fig.add_trace(go.Scatter(x=data0.index, y=data0['Close'], mode='lines', name='Price'))

# Add the Upper DC and shade the area

fig.add_trace(go.Scatter(x=data0.index, y=data0['DC_U'], mode='lines', name='Upper DC', line=dict(color='red')))

fig.add_trace(go.Scatter(x=data0.index, y=data0['DC_L'], fill='tonexty', mode='lines', name='Lower DC', line=dict(color='green')))

# Add the Middle DC

fig.add_trace(go.Scatter(x=data0.index, y=data0['DC_M'], mode='lines', name='Middle DC', line=dict(color='blue')))

# Customize the chart layout

fig.update_layout(title='NVDA DC',

xaxis_title='Date',

yaxis_title='Price',

showlegend=True)

fig.update_layout(

autosize=False,

width=1000,

height=500,

margin=dict(

l=50,

r=50,

b=100,

t=100,

pad=4

),

paper_bgcolor="LightSteelBlue",

)

# Show the chart

fig.update_layout(

xaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey'),

yaxis=dict(showgrid=True,gridwidth=1, gridcolor='Grey')

)

fig.show()

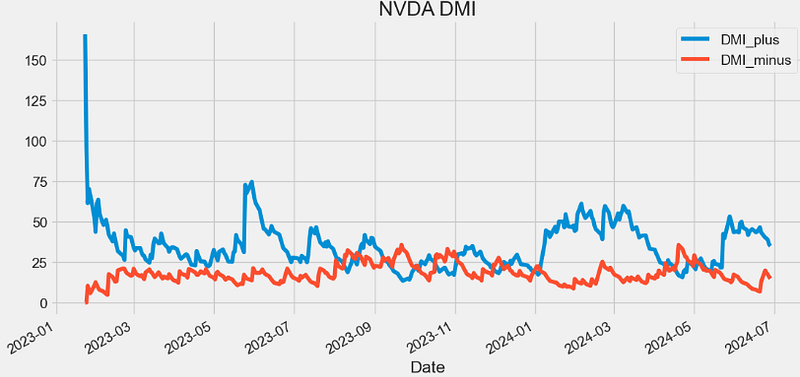

DMI Indicator

- The directional movement index (DMI) measures both the strength and direction of a price movement and is used to reduce false signals.

- The DMI employs two standard indicators, one negative (-DI) and one positive (+DI).

- The larger the spread between the two primary lines, the stronger the price trend.

- If +DI is way above -DI, the price trend is strongly up.

- If -DI is way above +DI, then the price trend is strongly down.

def DMI(ohlc, period = 14, adjust = True,high="High",low="Low",close="Close"):

"""The directional movement indicator (also known as the directional movement index - DMI) is a valuable tool

for assessing price direction and strength. This indicator was created in 1978 by J. Welles Wilder, who also created the popular

relative strength index. DMI tells you when to be long or short.

It is especially useful for trend trading strategies because it differentiates between strong and weak trends,

allowing the trader to enter only the strongest trends.

source: https://www.tradingview.com/wiki/Directional_Movement_(DMI)#CALCULATION

:period: Specifies the number of Periods used for DMI calculation

"""

ohlc["up_move"] = ohlc[high].diff()

ohlc["down_move"] = -ohlc[low].diff()

# positive Dmi

def _dmp(row):

if row["up_move"] > row["down_move"] and row["up_move"] > 0:

return row["up_move"]

else:

return 0

# negative Dmi

def _dmn(row):

if row["down_move"] > row["up_move"] and row["down_move"] > 0:

return row["down_move"]

else:

return 0

ohlc["plus"] = ohlc.apply(_dmp, axis=1)

ohlc["minus"] = ohlc.apply(_dmn, axis=1)

diplus = pd.Series(

100

* (ohlc["plus"] / ATR(ohlc, period = period,high=high,low=low,close=close))

.ewm(alpha=1 / period, adjust=adjust)

.mean(),

name="DI+",

)

diminus = pd.Series(

100

* (ohlc["minus"] / ATR(ohlc, period = period,high=high,low=low,close=close))

.ewm(alpha=1 / period, adjust=adjust)

.mean(),

name="DI-",

)

return pd.concat([diplus, diminus], axis=1)

data0[["DMI_plus", "DMI_minus"]]=DMI(data0, period = 14, adjust = True,high="High",low="Low",close="Close")

data0['DMI_plus'].plot(label='DMI_plus')

data0['DMI_minus'].plot(label='DMI_minus')

plt.title('NVDA DMI')

plt.legend()

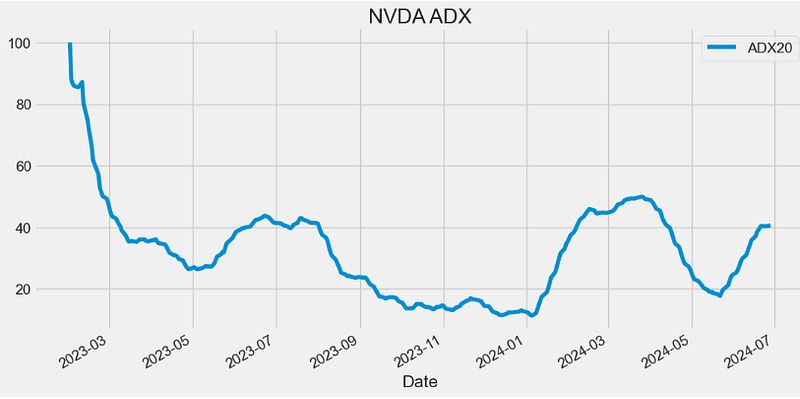

ADX Indicator

- The average directional index (ADX) is a technical indicator used by traders to determine the strength of a price trend for a financial security. Trading in the direction of a strong trend reduces risk and increases profit potential. Many traders consider the ADX to be the ultimate trend indicator because it is so reliable.

def ADX(ohlc, period = 14, adjust = True,high="High",low="Low",column="Close"):

"""The A.D.X. is 100 * smoothed moving average of absolute value (DMI +/-) divided by (DMI+ + DMI-). ADX does not indicate trend direction or momentum,

only trend strength. Generally, A.D.X. readings below 20 indicate trend weakness,

and readings above 40 indicate trend strength. An extremely strong trend is indicated by readings above 50"""

dmi = DMI(ohlc, period = period, adjust = adjust,high=high,low=low,close=column)

return pd.Series(

100

* (abs(dmi["DI+"] - dmi["DI-"]) / (dmi["DI+"] + dmi["DI-"]))

.ewm(alpha=1 / period, adjust=adjust)

.mean(),

name="{0} period ADX.".format(period),

)

plt.figure(figsize=(12,6))

data0["ADX"]=ADX(data0, period = 20, adjust = True,high="High",low="Low",column="Close")

data0['ADX'].plot(label='ADX20')

plt.title('NVDA ADX')

plt.legend()

- The ADX identifies a strong trend when the ADX is over 25 and a weak trend when the ADX is below 20.

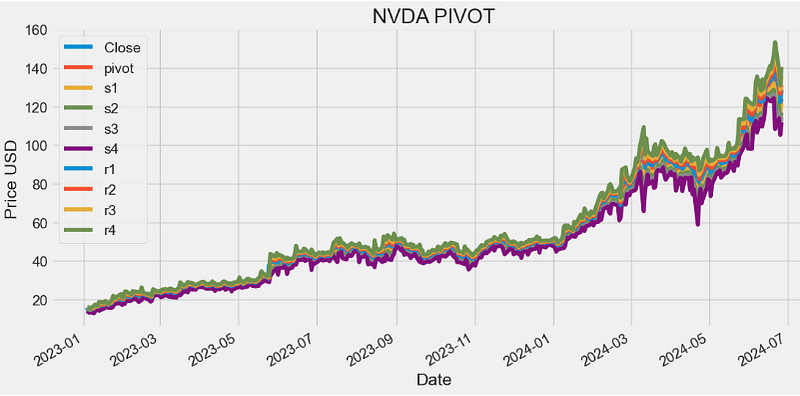

PIVOT Indicator

- Pivot Point analysis is a technique of determining key levels that price may react to. Pivot points tend to function as support or resistance and can be turning points.

def PIVOT(ohlc,open="Open",close="Close",high="High",low="Low"):

"""

Pivot Points are significant support and resistance levels that can be used to determine potential trades.

The pivot points come as a technical analysis indicator calculated using a financial instrument’s high, low, and close value.

The pivot point’s parameters are usually taken from the previous day’s trading range.

This means you’ll have to use the previous day’s range for today’s pivot points.

Or, last week’s range if you want to calculate weekly pivot points or, last month’s range for monthly pivot points and so on.

"""

df = ohlc.shift() # pivot is calculated of the previous trading session

pivot = pd.Series(TP(df,open=open,close=close,high=high,low=low), name="pivot") # pivot is basically a lagging TP

s1 = (pivot * 2) - df[high]

s2 = pivot - (df[high] - df[low])

s3 = df[low] - (2 * (df[high] - pivot))

s4 = df[low] - (3 * (df[high] - pivot))

r1 = (pivot * 2) - df[low]

r2 = pivot + (df[high] - df[low])

r3 = df[high] + (2 * (pivot - df[low]))

r4 = df[high] + (3 * (pivot - df[low]))

return pd.concat(

[

pivot,

pd.Series(s1, name="s1"),

pd.Series(s2, name="s2"),

pd.Series(s3, name="s3"),

pd.Series(s4, name="s4"),

pd.Series(r1, name="r1"),

pd.Series(r2, name="r2"),

pd.Series(r3, name="r3"),

pd.Series(r4, name="r4"),

],

axis=1,

)

datapivot=PIVOT(data0,open="Open",close="Close",high="High",low="Low")

datapivot.tail()

pivot s1 s2 s3 s4 r1 r2 r3 r4

Date

2024-06-20 134.200002 132.070002 128.560003 126.430003 124.300003 137.710002 139.840001 143.350001 146.860001

2024-06-21 133.686666 126.613337 122.446676 115.373347 108.300018 137.853327 144.926656 149.093318 153.259979

2024-06-24 127.166669 123.703334 120.836667 117.373332 113.909996 130.033335 133.496671 136.363337 139.230003

2024-06-25 120.203334 115.946668 113.783335 109.526670 105.270004 122.366666 126.623332 128.786664 130.949997

2024-06-26 123.969999 121.439997 116.789998 114.259997 111.729996 128.619998 131.149999 135.799998 140.449997

plt.figure(figsize=(12,6))

data0['Close'].plot(label='Close')

datapivot['pivot'].plot(label='pivot')

datapivot['s1'].plot(label='s1')

datapivot['s2'].plot(label='s2')

datapivot['s3'].plot(label='s3')

datapivot['s4'].plot(label='s4')

datapivot['r1'].plot(label='r1')

datapivot['r2'].plot(label='r2')

datapivot['r3'].plot(label='r3')

datapivot['r4'].plot(label='r4')

plt.ylabel('Price USD')

plt.title('NVDA PIVOT')

plt.legend()

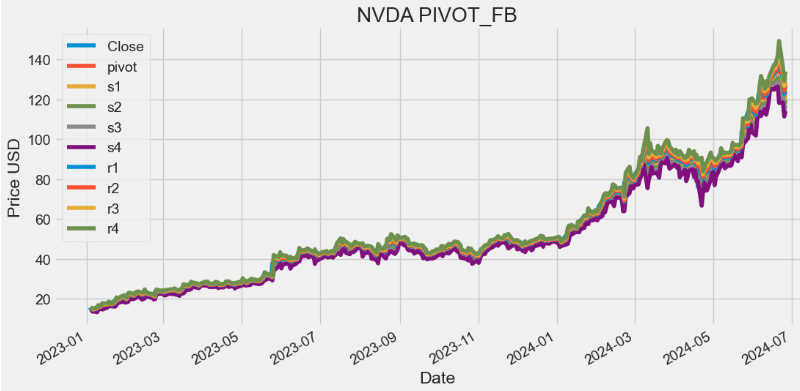

PIVOT FB Indicator

- Fibonacci Pivot Points stand tall as a powerful tool in the trader’s arsenal, offering insights into potential support and resistance levels in financial markets. Derived from the Fibonacci sequence, this indicator aids traders in making informed decisions and navigating market fluctuations with precision.

- Fibonacci Pivot Points are calculated using key levels derived from the Fibonacci sequence — typically the high, low, and close of the previous trading session. The formula involves applying specific ratios (like 0.382, 0.5, and 0.618) from the Fibonacci sequence to determine potential support and resistance levels for the current session.

def PIVOT_FIB(ohlc,open="Open",close="Close",high="High",low="Low"):

"""

Fibonacci pivot point levels are determined by first calculating the classic pivot point,

then multiply the previous day’s range with its corresponding Fibonacci level.

Most traders use the 38.2%, 61.8% and 100% retracements in their calculations.

"""

df = ohlc.shift()

pp = pd.Series(TP(df,open=open,close=close,high=high,low=low), name="pivot") # classic pivot

r4 = pp + ((df[high] - df[low]) * 1.382)

r3 = pp + ((df[high] - df[low]) * 1)

r2 = pp + ((df[high] - df[low]) * 0.618)

r1 = pp + ((df[high] - df[low]) * 0.382)

s1 = pp - ((df[high] - df[low]) * 0.382)

s2 = pp - ((df[high] - df[low]) * 0.618)

s3 = pp - ((df[high] - df[low]) * 1)

s4 = pp - ((df[high] - df[low]) * 1.382)

return pd.concat(

[

pp,

pd.Series(s1, name="s1"),

pd.Series(s2, name="s2"),

pd.Series(s3, name="s3"),

pd.Series(s4, name="s4"),

pd.Series(r1, name="r1"),

pd.Series(r2, name="r2"),

pd.Series(r3, name="r3"),

pd.Series(r4, name="r4"),

],

axis=1,

)

datapivotfb=PIVOT_FIB(data0,open="Open",close="Close",high="High",low="Low")

plt.figure(figsize=(12,6))

data0['Close'].plot(label='Close')

datapivotfb['pivot'].plot(label='pivot')

datapivotfb['s1'].plot(label='s1')

datapivotfb['s2'].plot(label='s2')

datapivotfb['s3'].plot(label='s3')

datapivotfb['s4'].plot(label='s4')

datapivotfb['r1'].plot(label='r1')

datapivotfb['r2'].plot(label='r2')

datapivotfb['r3'].plot(label='r3')

datapivotfb['r4'].plot(label='r4')

plt.ylabel('Price USD')

plt.title('NVDA PIVOT_FB')

plt.legend()

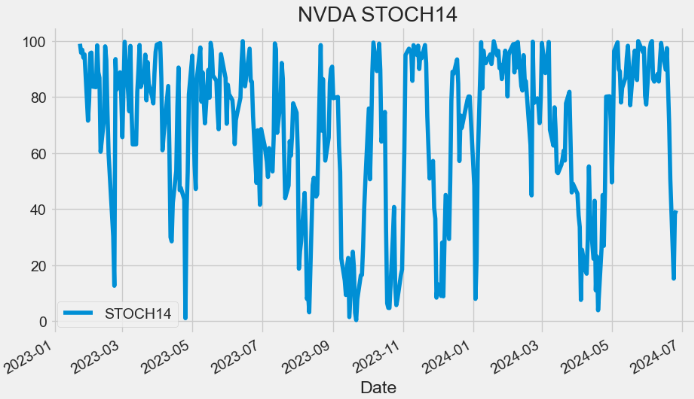

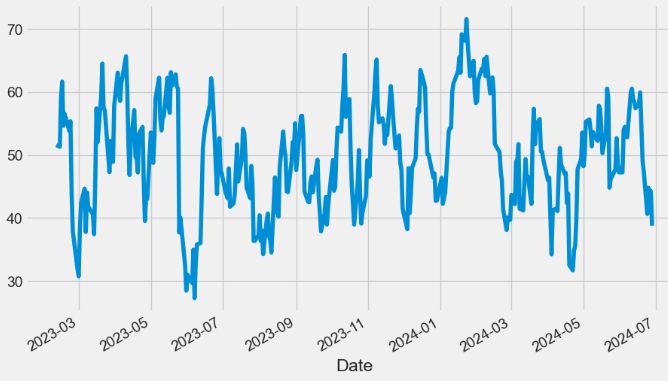

STOCH Indicator

- The stochastic indicator (STOCH) is a popular trading indicator that is useful for predicting trend reversals.

- When the stochastic indicator is at a high level, it means the instrument’s price closed near the top of the 14-period range. When the indicator is at a low level, it signals the price closed near the bottom of the 14-period range.

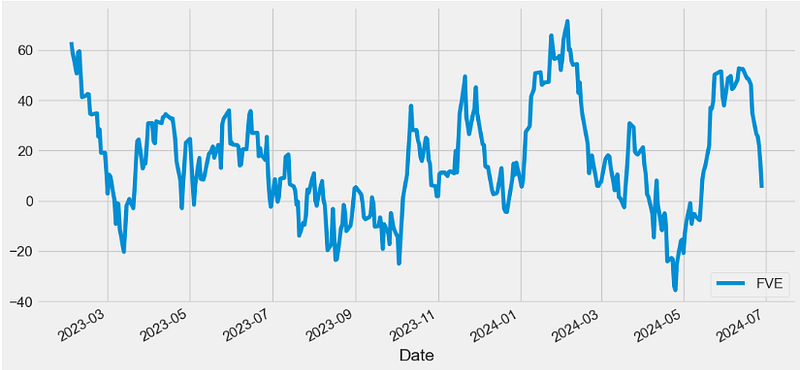

def STOCH(ohlc, period = 14,close="Close",high="High",low="Low"):

"""Stochastic oscillator %K