Algo-Trading NVIDIA with Donchian Channels

- NVIDIA (NASDAQ: NVDA) has come to dominate the market for chips used in AI-powered platforms, bringing its market capitalization to more than $2.28 trillion, an increase of over $1 trillion from its value at the beginning of the year.

- TradingView: Nvidia’s earnings for the current year have risen by 3.1% over the past month to $23.84. Furthermore, Nvidia is projected to experience a significant EPS growth of 84% this year.

- Indeed, NVDA stock smashed through earnings expectations, sending its shares — and the shares of adjacent AI stocks — rocketing higher. But bull runs don’t last forever. Therefore, it’s always wise to keep an eye on the exit strategy.

- The objective of this post is further validate the current NVDA technicals, trading ideas and analyst recommendations using Donchian channels.

- Donchian Channels (DC) are a technical indicator that seeks to identify bullish and bearish extremes that favor reversals, higher and lower breakouts, breakdowns, and other emerging trends.

- Why DC: Combining SMA/EMA, volume indicators, and MACD with DC can lead to a more complete picture of the market for an asset.

- Method: We take on board the algo-trading algorithm in Python that consists of the following steps (cf. Strategy 1: Donchian Middle Value Cross-Over):

- Step 1: Reading the NVDA stock historical data using yfinance

- Step 2: Create a visualization of the Donchian Channel using matplotlib

- Step 3: Implementing the Donchian Middle Value Cross-Over Strategy 1

- Step 4: Compare the cumulative returns and relevant stock Risk/Return KPIs (total/annual ROI, annual volatility, Sortino/Sharpe ratio, max drawdowns, and max drawdown durations) of Strategy 1 vs Buy-and-Hold default.

- Let’s delve into the implementation details in Jupyter Notebook!

- Setting up the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd() - Basic import and installations

!pip install yfinance

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import yfinance as yf- Invoking the DC functions that implement Strategy 1

def calcDonchianChannels(data: pd.DataFrame, period: int):

data["upperDon"] = data["High"].rolling(period).max()

data["lowerDon"] = data["Low"].rolling(period).min()

data["midDon"] = (data["upperDon"] + data["lowerDon"]) / 2

return data

def midDonCrossOver(data: pd.DataFrame, period: int=20, shorts: bool=True):

data = calcDonchianChannels(data, period)

data["position"] = np.nan

data["position"] = np.where(data["Close"]>data["midDon"], 1,

data["position"])

if shorts:

data["position"] = np.where(data["Close"]<data["midDon"], -1,

data["position"])

else:

data["position"] = np.where(data["Close"]<data["midDon"], 0,

data["position"])

data["position"] = data["position"].ffill().fillna(0)

return calcReturns(data)

def calcReturns(df):

df['returns'] = df['Close'] / df['Close'].shift(1)

df['log_returns'] = np.log(df['returns'])

df['strat_returns'] = df['position'].shift(1) * df['returns']

df['strat_log_returns'] = df['position'].shift(1) * \

df['log_returns']

df['cum_returns'] = np.exp(df['log_returns'].cumsum()) - 1

df['strat_cum_returns'] = np.exp(

df['strat_log_returns'].cumsum()) - 1

df['peak'] = df['cum_returns'].cummax()

df['strat_peak'] = df['strat_cum_returns'].cummax()

return df

def getStratStats(log_returns: pd.Series,

risk_free_rate: float = 0.02):

stats = {} # Total Returns

stats['tot_returns'] = np.exp(log_returns.sum()) - 1

# Mean Annual Returns

stats['annual_returns'] = np.exp(log_returns.mean() * 252) - 1

# Annual Volatility

stats['annual_volatility'] = log_returns.std() * np.sqrt(252)

# Sortino Ratio

annualized_downside = log_returns.loc[log_returns<0].std() * \

np.sqrt(252)

stats['sortino_ratio'] = (stats['annual_returns'] - \

risk_free_rate) / annualized_downside

# Sharpe Ratio

stats['sharpe_ratio'] = (stats['annual_returns'] - \

risk_free_rate) / stats['annual_volatility']

# Max Drawdown

cum_returns = log_returns.cumsum() - 1

peak = cum_returns.cummax()

drawdown = peak - cum_returns

max_idx = drawdown.argmax()

stats['max_drawdown'] = 1 - np.exp(cum_returns[max_idx]) \

/ np.exp(peak[max_idx])

# Max Drawdown Duration

strat_dd = drawdown[drawdown==0]

strat_dd_diff = strat_dd.index[1:] - strat_dd.index[:-1]

strat_dd_days = strat_dd_diff.map(lambda x: x.days).values

strat_dd_days = np.hstack([strat_dd_days,

(drawdown.index[-1] - strat_dd.index[-1]).days])

stats['max_drawdown_duration'] = strat_dd_days.max()

return {k: np.round(v, 4) if type(v) == np.float_ else v

for k, v in stats.items()}- Loading the NVDA historical data and calculating DC

ticker = "NVDA"

yfObj = yf.Ticker(ticker)

data = yfObj.history(start="2021-01-03", end="2024-04-03").drop(

["Volume", "Stock Splits"], axis=1)

data = calcDonchianChannels(data, 20)

data.tail()

Open High Low Close Dividends upperDon lowerDon midDon

Date

2024-03-25 00:00:00-04:00 939.409973 967.659973 935.099976 950.020020 0.0 974.0 771.213814 872.606907

2024-03-26 00:00:00-04:00 958.510010 963.750000 925.020020 925.609985 0.0 974.0 771.213814 872.606907

2024-03-27 00:00:00-04:00 931.119995 932.400024 891.229980 902.500000 0.0 974.0 783.463248 878.731624

2024-03-28 00:00:00-04:00 900.000000 913.000000 891.929993 903.559998 0.0 974.0 794.312735 884.156367

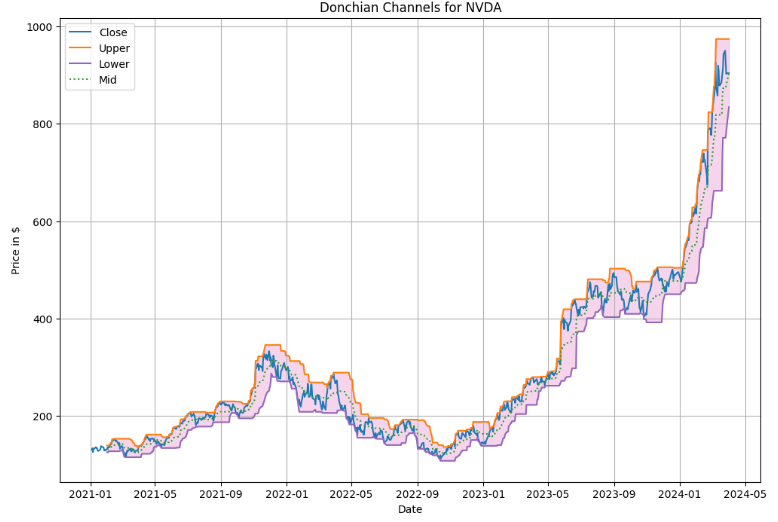

2024-04-01 00:00:00-04:00 902.989990 922.250000 892.039978 903.630005 0.0 974.0 834.169983 904.084991- Plotting DC for NVDA

colors = plt.rcParams["axes.prop_cycle"].by_key()["color"]

plt.figure(figsize=(12, 8))

plt.plot(data["Close"], label="Close")

plt.plot(data["upperDon"], label="Upper", c=colors[1])

plt.plot(data["lowerDon"], label="Lower", c=colors[4])

plt.plot(data["midDon"], label="Mid", c=colors[2], linestyle=":")

plt.fill_between(data.index, data["upperDon"], data["lowerDon"], alpha=0.3,

color=colors[6])

plt.xlabel("Date")

plt.ylabel("Price in $")

plt.title(f"Donchian Channels for {ticker}")

plt.legend()

plt.grid()

plt.show()

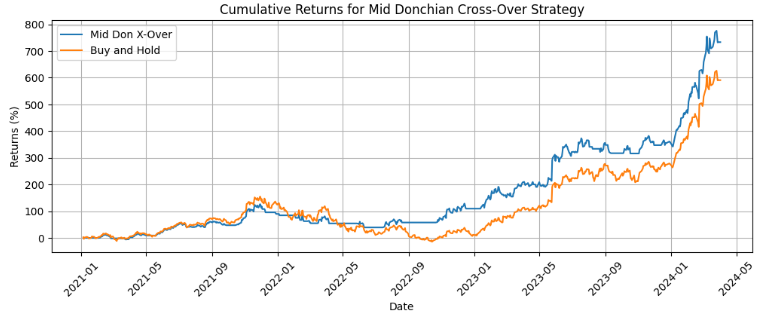

- Comparing Cumulative Returns for Mid Donchian Cross-Over Strategy vs Buy-and-Hold default

midDon = midDonCrossOver(data.copy(), 20, shorts=False)

plt.figure(figsize=(12, 4))

plt.plot(midDon["strat_cum_returns"] * 100, label="Mid Don X-Over")

plt.plot(midDon["cum_returns"] * 100, label="Buy and Hold")

plt.title("Cumulative Returns for Mid Donchian Cross-Over Strategy")

plt.xlabel("Date")

plt.ylabel("Returns (%)")

plt.xticks(rotation=45)

plt.legend()

plt.grid()

plt.show()

stats = pd.DataFrame(getStratStats(midDon["log_returns"]),

index=["Buy and Hold"])

stats = pd.concat([stats,

pd.DataFrame(getStratStats(midDon["strat_log_returns"]),

index=["MidDon X-Over"])])

stats

Conclusions

- In this study, we have performed the algo-trading technical analysis of NVDA using Donchian Channels (DC).

- Results have shown that DC can provide valuable insights into NVDA stock dynamics and offer potential opportunities for profit and exit strategies.

- It appears that NVDA Mid Donchian Cross-Over (Strategy 1) has outperformed the Buy-and-Hold default in terms of Cumulative Returns and popular Risk/Return KPIs for our selected timeframe.

Explore More

- Donchian Channel Trading Systems

- A Market-Neutral Strategy

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- NVIDIA Rolling Volatility: GARCH & XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Multiple-Criteria Technical Analysis of Blue Chips in Python

References

- NVIDIA

- Building A Simple Breakout Trading System Using Python

- Nvidia Stock Buy Hold or Sell

- NVDA Technicals

- Nvidia’s $1 Trillion Market Cap Gain This Year Is Nearly Double Tesla’s Entire Market Cap

- Nothing Goes Up Forever. This Rule Will Tell You When To Sell Nvidia Stock.

- Donchian Channels

- Donchian Channels Formula, Calculations, and Uses

- DONCHIAN CHANNELS (DC)

- Donchian Channels — Overview, Mechanics, and Calculation

- Donchian Channel Strategy — What Is It

- What Everyone Should Know About the Donchian Channel Indicator