The article presents an algorithmic trading strategy using Williams %R and MACD indicators to trade NVIDIA stocks, with a Python implementation and backtesting results that outperform the SPY benchmark.

Abstract

The article delves into an algorithmic trading strategy that leverages the Williams %R and Moving Average Convergence Divergence (MACD) technical indicators to trade NVIDIA (NVDA) stocks. It provides a step-by-step guide on how to implement this strategy in Python, including data retrieval, indicator calculation, and visualization. The strategy involves buying when the MACD line crosses above the signal line and selling when it crosses below. The article also includes a backtesting analysis, demonstrating that a $10,000 investment in NVDA using this strategy from January 2021 to March 2024 would have yielded a 50% profit, outperforming the SPY benchmark by 22%. The author emphasizes the bullish trend and momentum indicators for NVDA and acknowledges the importance of considering technical analysis alongside fundamentals.

Opinions

The author believes that the combination of Williams %R and MACD provides a robust technical signal for trading NVDA stocks.

There is a positive outlook on NVDA's stock performance based on the technical analysis presented.

The article suggests that algorithmic trading strategies can offer significant profits, as evidenced by the backtested results.

The author implies that the WR-MACD strategy is superior to the SPY benchmark, indicating a potentially more profitable investment approach for traders.

A disclaimer is provided, noting that technical analysis does not take into account fundamental aspects of the stock, which could be a limitation of the strategy.

The author encourages readers to explore AI-powered trading tools, recommending a cost-effective AI service as an alternative to ChatGPT Plus(GPT-4).

Algo-Trading NVIDIA with Williams %R & MACD Indicators

The focus of this article is still on the NVIDIA stock to ensure the most efficient execution of an algo-trading strategy by examining the Williams %R &MACD technical indicators.

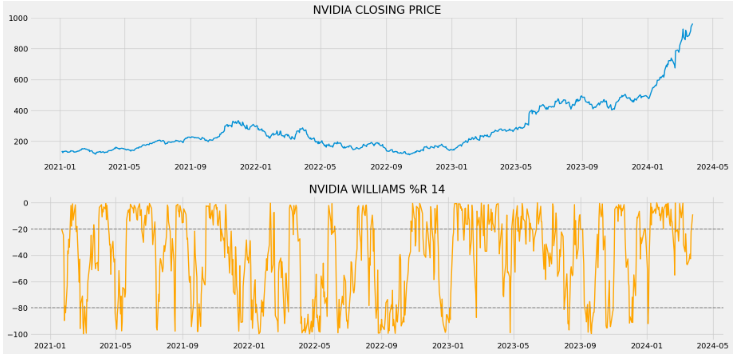

Williams %R moves between zero and -100. A reading above -20 is overbought. A reading below -80 is oversold.

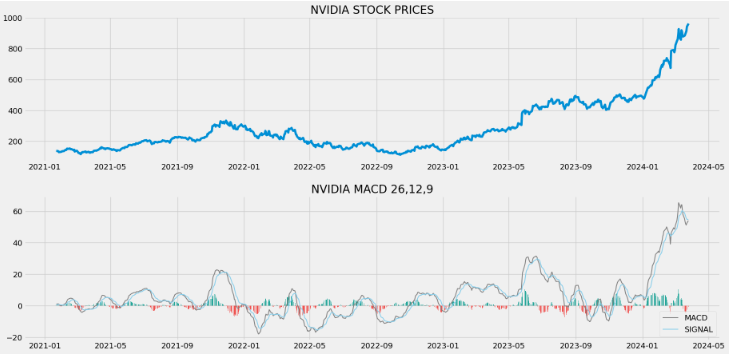

When the MACD line crosses from below to above the signal line, the indicator is considered bullish (accompanied by positive histogram bars, indicating upward momentum). The further below the zero line the stronger the signal. When the MACD line crosses from above to below the signal line, the indicator is considered bearish (accompanied by negative histogram bars, suggesting downward momentum). The further above the zero line the stronger the signal.

Let’s delve into the specifics of the algo-trading workflow in Python:

Creating the working directory YOURPATH and importing libraries

import os

os.chdir('C:/Users/adrou/OneDrive/Documents/STOCKNIKHIL') # Create working directory

os. getcwd()

import pandas as pd

import numpy as np

import requests

import matplotlib.pyplot as plt

from math import floor

from termcolor import colored as cl

plt.style.use('fivethirtyeight')

plt.rcParams['figure.figsize'] = (20,10)

Getting NVIDIA historical stock data during 01/2021–03/2024

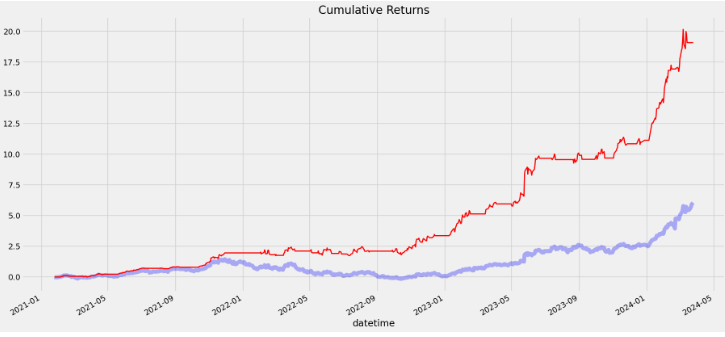

Benchmark profit by investing $10k : 2882.3

Benchmark Profit percentage : 28%

WR-MACD Strategy profit is22% higher than the Benchmark Profit

Conclusions

Considering the current trends, indicators, and patterns, the technical outlook for NVDA is bullish and overbought, with bearish momentum.

Backtesting:

Profit gained from the WR-MACD strategy by investing $10k in NVDA: 5014.22

Profit percentage of the WR-MACD strategy : 50%

Benchmark Comparison:

WR-MACD Strategy profit is22% higher than the Benchmark Profit

The MACD study has been used to identify stock buy and sell signals. When the MACD crosses above the signal line, it may be time for the longs to enter the market, whereas when a cross below the signal line occurs, it may be time for the shorts to enter the market.

As previously mentioned, the %R is used to measure momentum. %R oscillates within a fixed range between the values of 0 and -100. Williams himself set the parameters of overbought as any reading between 0 and -20.

Disclaimer: Technical Analysis is blind to the fundamentals and looks only at the trading data for NVIDIA.