How to Swing Algo-Trade Tech Stocks using the Qullamaggie's Breakouts — 1. NVIDIA

- The objective of this post is to resolve a risk-return trade-off of a swing algo-trading strategy in Python that aims at capturing short or medium gains in a growth tech stock such as NVIDIA (NDAQ: NVDA).

- Following the Qullamaggie’s breakout strategy, we take on board a simple yet effective scanner in Python that algorithmically scans for high-growth, and sideways price actions.

- Let’s embark on the journey!

- Setting the working directory PATH, the stock ticker and importing basic libraries

import os

os.chdir('PATH') # Set working directory

os. getcwd()

import numpy as np

import pandas as pd

import yfinance as yf

import seaborn as sns

import matplotlib.pyplot as plt

ticker='NVDA'def trend_filter(prices: pd.core.series.Series,

growth_4_min: float = 25.,

growth_12_min: float = 50.,

growth_24_min: float = 80.) -> np.array:

growth_func = lambda x: 100*(x.values[-1]/x.min() - 1)

growth_4 = df['Close'].rolling(20).apply(growth_func) > growth_4_min

growth_12 = df['Close'].rolling(60).apply(growth_func) > growth_12_min

growth_24 = df['Close'].rolling(120).apply(growth_func) > growth_24_min

return np.where(

growth_4 | growth_12 | growth_24,

1,

0,

)

if __name__ == '__main__':

df = yf.download(ticker)

df.loc[:, 'trend_filter'] = trend_filter(df['Close'])

df.dropna()

df_trending = df[df['trend_filter'] == 1] - Time series smoothing using an explicit FD method and checking for consolidation

def explicit_heat_smooth(prices: np.array,

t_end: float = 5.0) -> np.array:

k = 0.1 # Time spacing, must be < 1 for numerical stability

P = prices

t = 0

while t < t_end:

P = k*(P[2:] + P[:-2]) + P[1:-1]*(1-2*k)

P = np.hstack((

np.array([prices[0]]),

P,

np.array([prices[-1]]),

))

t += k

return P

def check_consolidation(prices: np.array,

perc_change_days: int,

perc_change_thresh: float,

check_days: int) -> int:

prices = explicit_heat_smooth(prices)

perc_change = prices[perc_change_days:]/prices[:-perc_change_days] - 1

consolidating = np.where(np.abs(perc_change) < perc_change_thresh, 1, 0)

if np.sum(consolidating[-check_days:]) > 0:

return 1

else:

return 0

def find_consolidation(prices: np.array,

days_to_smooth: int = 50,

perc_change_days: int = 5,

perc_change_thresh: float = 0.015,

check_days: int = 5) -> np.array:

res = np.full(prices.shape, np.nan)

for idx in range(days_to_smooth, prices.shape[0]):

res[idx] = check_consolidation(

prices = prices[idx-days_to_smooth:idx],

perc_change_days = perc_change_days,

perc_change_thresh = perc_change_thresh,

check_days = check_days,

)

return res

if __name__ == '__main__':

df = yf.download(ticker)

df.loc[:, 'consolidating'] = find_consolidation(df['Close'].values)

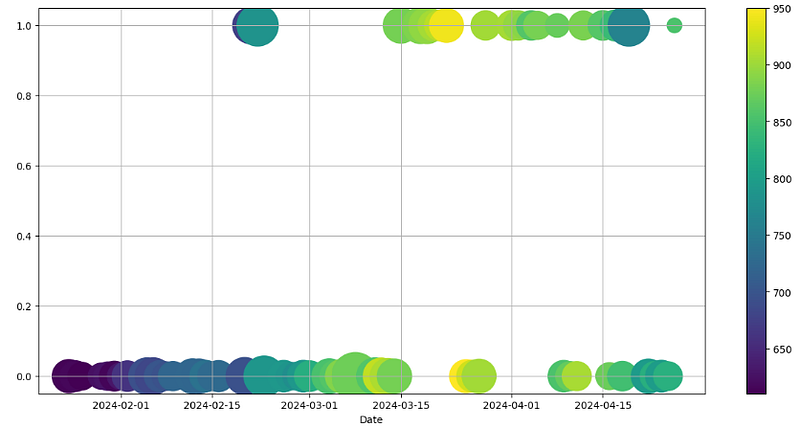

df.dropna()- Plotting the binary ‘consolidating’ if df[‘Close’] > 600 USD

dff=df[df['Close'] > 600]

fig = plt.figure(figsize=(15, 7))

scal=5e4

plt.scatter(dff.index,dff['consolidating'],s=dff["Volume"]/scal,c=dff["Close"],cmap='viridis')

plt.colorbar()

plt.xlabel('Date')

plt.grid()

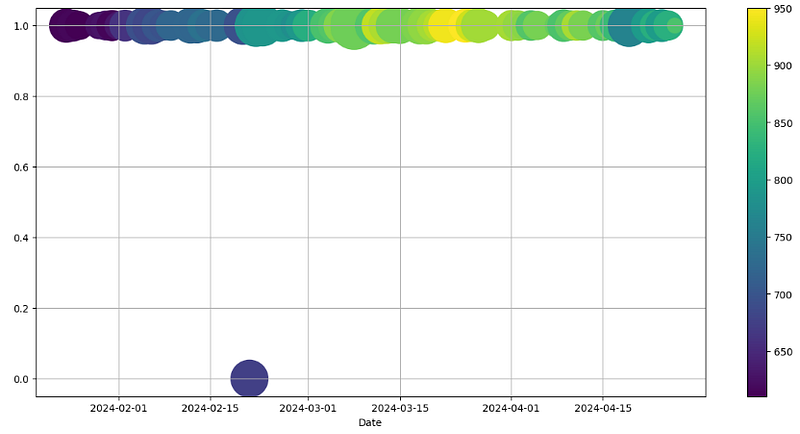

- Creating and plotting the ‘filtered’ binary column

df = yf.download('NVDA')

df.loc[:, 'consolidating'] = find_consolidation(df['Close'].values)

df.loc[:, 'trend_filter'] = trend_filter(df['Close'])

df.loc[:, 'filtered'] = np.where(

df['consolidating'] + df['trend_filter'] == 2,

True,

False,

)

dff1=df[df['Close'] > 600]

ig = plt.figure(figsize=(15, 7))

scal=5e4

plt.scatter(dff1.index,dff1['trend_filter'],s=dff["Volume"]/scal,c=dff["Close"],cmap='viridis')

plt.colorbar()

plt.xlabel('Date')

plt.grid()

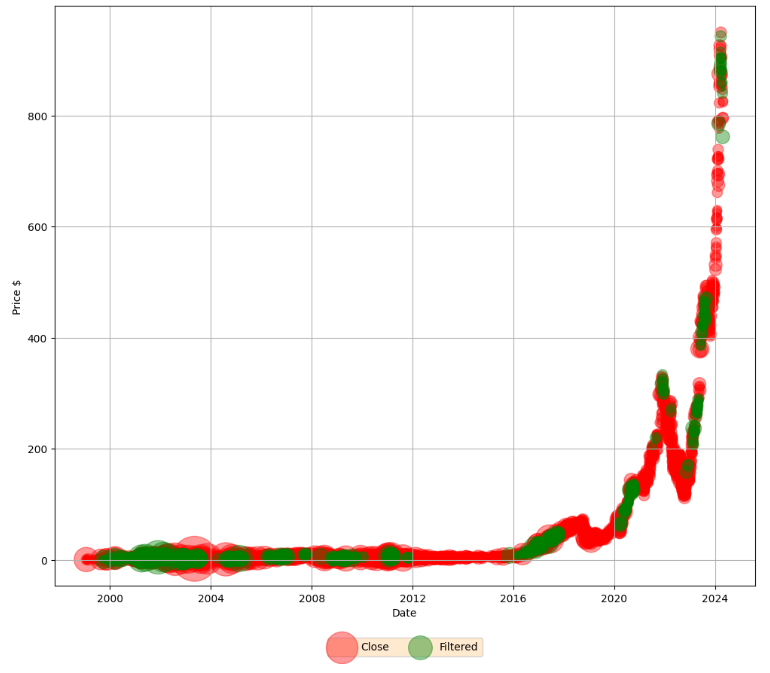

- Final visualization of the ‘filtered’ column based on the binary value — close price before/after filtering

df.index = pd.DatetimeIndex(data=df.index, tz='US/Eastern')

dft = pd.DataFrame({'DateTime': df.index})

# selecting rows based on condition

df1 = df[df['filtered'] > 0]

df0 = df[df['filtered'] < 1]

dft1 = pd.DataFrame({'DateTime': df1.index})

dft0 = pd.DataFrame({'DateTime': df0.index})

plt.figure(figsize=(12,10))

scal=5e5

plt.scatter(df0.index, df0["Close"],color='red',s=df0["Volume"]/scal,alpha=0.4)

plt.scatter(df1.index, df1["Close"],color='green',s=df1["Volume"]/scal,alpha=0.4)

plt.xlabel("Date")

plt.ylabel("Price $")

plt.legend(["Close" , "Filtered"], facecolor='bisque',

loc='upper center', bbox_to_anchor=(0.5, -0.08),

ncol=2)

plt.grid()

plt.show()

- Optionally checking DateTime Index and shape of our data

print(df0.index)

DatetimeIndex(['1999-01-22 00:00:00-05:00', '1999-01-25 00:00:00-05:00',

'1999-01-26 00:00:00-05:00', '1999-01-27 00:00:00-05:00',

'1999-01-28 00:00:00-05:00', '1999-01-29 00:00:00-05:00',

'1999-02-01 00:00:00-05:00', '1999-02-02 00:00:00-05:00',

'1999-02-03 00:00:00-05:00', '1999-02-04 00:00:00-05:00',

...

'2024-03-27 00:00:00-04:00', '2024-04-09 00:00:00-04:00',

'2024-04-10 00:00:00-04:00', '2024-04-11 00:00:00-04:00',

'2024-04-16 00:00:00-04:00', '2024-04-18 00:00:00-04:00',

'2024-04-22 00:00:00-04:00', '2024-04-23 00:00:00-04:00',

'2024-04-24 00:00:00-04:00', '2024-04-25 00:00:00-04:00'],

dtype='datetime64[ns, US/Eastern]', name='Date', length=5643, freq=None)

df0.shape

(5643, 9)

print(df1.index)

DatetimeIndex(['1999-09-09 00:00:00-04:00', '1999-09-10 00:00:00-04:00',

'1999-09-13 00:00:00-04:00', '1999-10-06 00:00:00-04:00',

'1999-10-08 00:00:00-04:00', '1999-12-01 00:00:00-05:00',

'1999-12-02 00:00:00-05:00', '1999-12-03 00:00:00-05:00',

'1999-12-06 00:00:00-05:00', '1999-12-07 00:00:00-05:00',

...

'2024-04-02 00:00:00-04:00', '2024-04-03 00:00:00-04:00',

'2024-04-04 00:00:00-04:00', '2024-04-05 00:00:00-04:00',

'2024-04-08 00:00:00-04:00', '2024-04-12 00:00:00-04:00',

'2024-04-15 00:00:00-04:00', '2024-04-17 00:00:00-04:00',

'2024-04-19 00:00:00-04:00', '2024-04-26 00:00:00-04:00'],

dtype='datetime64[ns, US/Eastern]', name='Date', length=714, freq=None

df1.shape

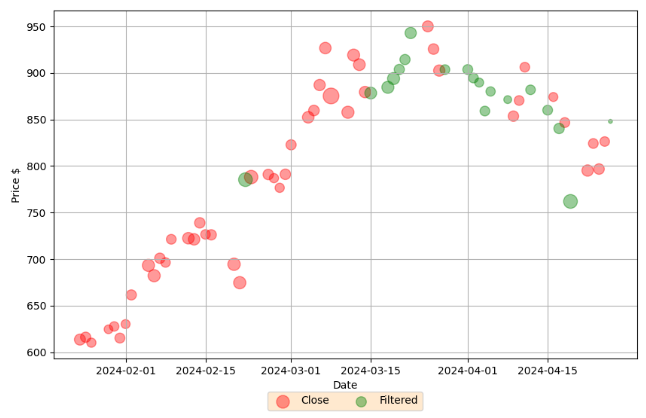

(714, 9)- Examining the zoomed version of the above plot if df[‘Close’] > 600 USD

rslt_df0 = df0.loc[df0['Close'] > 600]

rslt_df1 = df1.loc[df1['Close'] > 600]

plt.figure(figsize=(10,6))

scal=5e5

plt.scatter(rslt_df0.index, rslt_df0["Close"],color='red',s=rslt_df0["Volume"]/scal,alpha=0.4)

plt.scatter(rslt_df1.index, rslt_df1["Close"],color='green',s=rslt_df1["Volume"]/scal,alpha=0.4)

plt.xlabel("Date")

plt.ylabel("Price $")

plt.legend(["Close" , "Filtered"], facecolor='bisque',

loc='upper center', bbox_to_anchor=(0.5, -0.08),

ncol=2)

plt.grid()

plt.show()

- Breakouts are certainly key indicators of trend shifts, providing traders with chances for financial gain.

- It is therefore useful to compare these indicators to NVDA candlesticks with other trading indicators.

Conclusions

- Today we have talked about the swing breakout algo-trading algorithm in Python.

- To be a successful swing trader, we must minimize losses and maximize profits by holding a position either long or short for more than one trading session, but usually not longer than several weeks or a couple of months.

- Our current swing algo-trading strategy is based on the Qullamaggie methodology that combines technical analysis market indicators and risk management strategies.

- We have shown how to profit from short-term price movements in the NVDA price swings using this methodology.

Explore More

- Backtesting Algo-Trading Strategies, FinTech Analysis & Portfolio Optimization: NVDA, AMD, INTC, MSI vs S&P 500 Benchmark

- Backtesting the NVIDIA Scalping Strategy with SPY Benchmark & VaR Simulations

- Backtesting Hybrid CI & MACD Trading Strategies for NVIDIA

- NVIDIA Algo-Trading: VaR, Q-Q Plots & Stochastic Simulations

- A Deeper Look at NVIDIA KST Algo-Trading Signals & Backtesting

- NVIDIA 14–20 RSI-BB Algo-Trading

- Portfolio Optimization of 4 Major Techs: Markowitz, Sharpe, VaR & CAPM

- Algo-Trading NVIDIA with Donchian Channels

- Algo-Trading NVIDIA with ADX & RSI Indicators

- Deploying Streamlit Stock Fundamental Analysis App — NVIDIA Example

- An Algo-Trading Sneak Peek at Top AI-Powered Growth Stocks — 1. NVIDIA

- A Market-Neutral Strategy

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Returns-Volatility Domain K-Means Clustering and LSTM Anomaly Detection of S&P 500 Stocks

- NVIDIA Rolling Volatility: GARCH & XGBoost

- The Qullamaggie’s TSLA Breakouts for Swing Traders

- The Qullamaggie’s OXY Swing Breakouts

References

- A Simple Way to Scan for Breakout Candidates Using Python

- Scripting the Swing: To filter stocks based on setup

- Trading Breakout Strategies — the Dos and Don’ts

- Breakout Trading Strategy Used by Professional Traders

- What is Swing Trading?

- Swing Trading

- How to Swing Trade Tech Stocks (by Scott Redler / @RedDogT3)