The web content outlines a comprehensive analysis of portfolio optimization strategies for four major tech stocks—Apple (AAPL), Meta Platforms (META), Amazon (AMZN), and NVIDIA (NVDA)—using key financial models such as Markowitz's Efficient Frontier, Sharpe Ratio, Value at Risk (VaR), and the Capital Asset Pricing Model (CAPM) to maximize risk-adjusted returns.

Abstract

The article delves into the application of stochastic optimization techniques to construct investment portfolios for four leading technology companies: Apple, Meta Platforms, Amazon, and NVIDIA. It emphasizes the importance of the Return/Risk Ratio (RRR) and employs several financial models to achieve the maximum possible RRR. The Markowitz Efficient Frontier, Monte Carlo simulations,

Portfolio Optimization of 4 Major Techs: Markowitz, Sharpe, VaR & CAPM

This article outlines a stochastic approach to investment portfolio optimization using several key KPIs and underlying models for maximizing the ratio RRR, where RRR=Return/Risk.

Notably, Apple has achieved a remarkable feat by surpassing a $3 trillion market cap, making it the sole company in recorded history to reach this milestone. Read more here.

If you’re considering entering the eCommerce market, it’s important to note that AMZN currently commands 37.8% of the US eCommerce market share, demonstrating its significant dominance in the industry.

Recent revenue growth reports suggest that META is still a major player in the digital advertising market, and that it is well-positioned for future growth.

In 2023, NVDA saw a remarkable surge in its share price by 228%, reaching a market capitalization of a staggering $1.19 trillion. This impressive financial performance is reflective of the company’s strategic shift from a gaming-focused business to designing chips for self-driving and driver-assisting vehicle technologies, cloud computing, and data centers. In fact, the data segment has now become the largest revenue generator for the company. Read full story.

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

Basic Imports

import pandas as pd

import numpy as np

from functools import reduce

import yfinance as yfin

from pandas_datareader import data as pdr

import yfinance as yf

import datetime

import random

import scipy.optimize as sco

from scipy import stats

import matplotlib.pyplot as plt

import matplotlib as mpl

import seaborn as sns

%matplotlib inline

mpl.style.use('ggplot')

figsize = (15, 8)

yf.pdr_override()

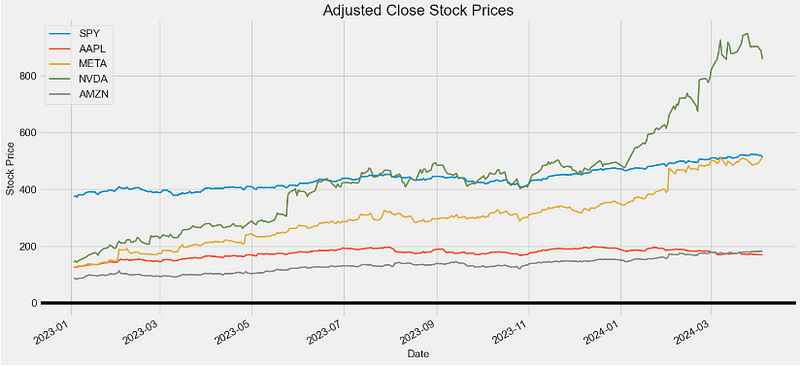

Input Stock Data Analysis

Downloading tech stock data and exporting as CSV

tickers = ("SPY", "AAPL", "META", "NVDA", "AMZN")

start = "2023-01-03"

end = '2024-04-05'

fin_data = yfin.download(tickers, start, end) #download yahoo finance data for specific dates

fin_data.to_csv('fin_data.csv') #convert data to csv#check the dimensions of the data

fin_data.shape

(315, 30)

#view the last 5 rows of the data

fin_data.tail()

Price Adj Close Close ... Open Volume

Ticker AAPL AMZN META NVDA SPY AAPL AMZN META NVDA SPY ... AAPL AMZN META NVDA SPY AAPL AMZN META NVDA SPY

Date

2024-03-28171.479996180.380005485.579987903.559998523.070007171.479996180.380005485.579987903.559998523.070007 ... 171.750000180.169998492.839996900.000000523.21002265672700380516001521280043521200962949002024-04-01 170.029999180.970001491.350006903.630005522.159973170.029999180.970001491.350006903.630005522.159973 ... 171.190002180.789993487.200012902.989990523.8300174624050029174500924700045244100624775002024-04-02 168.839996180.690002497.369995894.520020518.840027168.839996180.690002497.369995894.520020518.840027 ... 169.080002179.070007485.100006884.479980518.23999049329500326115001108100043306400742303002024-04-03 169.649994182.410004506.739990889.640015519.409973169.649994182.410004506.739990889.640015519.409973 ... 168.789993179.899994498.929993884.840027517.71997147602100309598001204710036845000590368002024-04-04 168.820007180.000000510.920013859.049988513.070007168.820007180.000000510.920013859.049988513.070007 ... 170.289993184.199997516.510010904.059998523.52002053289969414745452623481842761958962621415 rows × 30 columns

Check if there are missing values

fin_data.isnull().sum()

Descriptive statistics of Price = Adj Close

fin_data[['Adj Close']].describe().T

count mean std min25% 50% 75% max

Ticker

AAPL 315.0173.77133016.368597124.166641166.111610176.602585186.443153197.857529

AMZN 315.0130.95146025.71501083.120003105.065002130.220001147.029999182.410004

META 315.0299.96505898.044027124.607788226.894264299.352386336.288208512.190002

NVDA 315.0441.782295189.310871142.580032277.540955437.434967488.005554950.020020

SPY 315.0437.96826438.259185372.542725406.521133433.460419457.810654523.169983

Looking at the Maximum Closing Value for our stocks

defmax_close(stocks,df):

""" This calculates and returns the maximum closing value of a specific stock"""return df['Close'][stocks].max()

deftest_max():

""" This tests the max_close function"""for stocks in ["SPY", "AAPL", "META", "NVDA", "AMZN"]:

print("Maxiumum Closing Value for {} is {}".format(stocks, max_close(stocks,fin_data)))

test_max()

Maxiumum Closing Value for SPY is523.1699829101562

Maxiumum Closing Value for AAPL is198.11000061035156

Maxiumum Closing Value for META is512.1900024414062

Maxiumum Closing Value for NVDA is950.02001953125

Maxiumum Closing Value for AMZN is182.41000366210938

Examining the Mean Volume

defmean_vol(stocks,df):

""" This calculates and returns the minimum volume of a specific stock"""return df['Volume'][stocks].mean()

deftest_mean():

for stocks in ["SPY", "AAPL", "META", "NVDA", "AMZN"]:

print("Mean Volume for {} is {}".format(stocks, mean_vol(stocks,fin_data)))

test_mean()

Mean Volume for SPY is80445469.01904762

Mean Volume for AAPL is59626502.75873016

Mean Volume for META is22872390.215873014

Mean Volume for NVDA is48560584.62857143

Mean Volume for AMZN is55690328.07936508

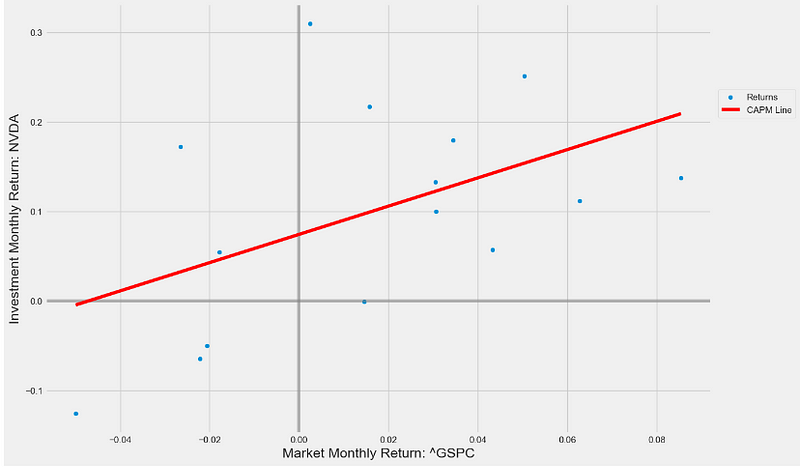

Examining the Market vs Investment Monthly Returns

stock_a =['NVDA']

stock_m = ['^GSPC']

CAPM(stock_a,stock_m,start, end)

========================================

Beta from formula: 1.5791

Beta from Linear Regression: 1.5791

Alpha: 0.074

========================================

CAPM Line for NVDA vs ^GSPC Monthly Returns

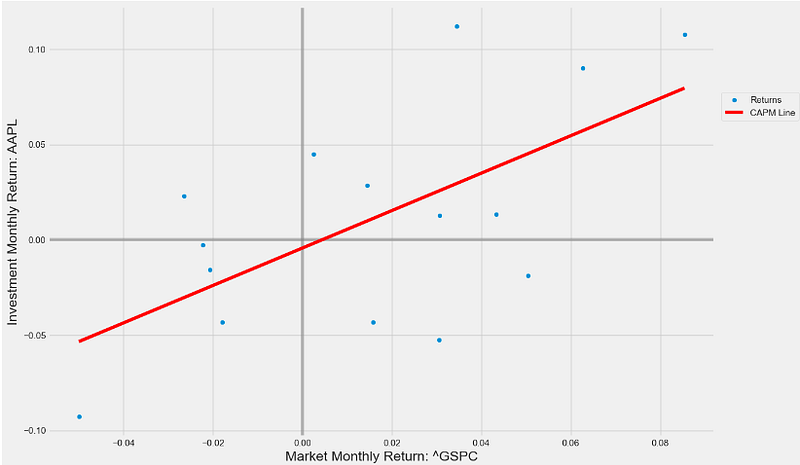

stock_a =['AAPL']

stock_m = ['^GSPC']

CAPM(stock_a,stock_m,start, end)

========================================

Beta from formula: 0.9823

Beta from Linear Regression: 0.9823

Alpha: -0.004

========================================

CAPM Line for AAPL vs ^GSPC Monthly Returns

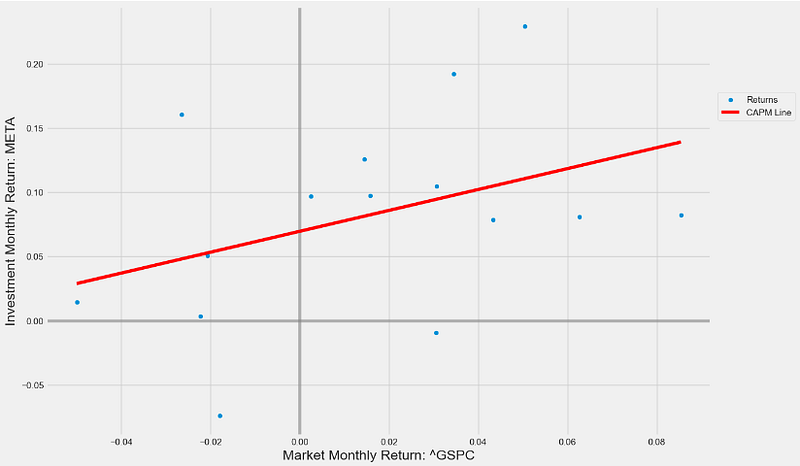

stock_a =['META']

stock_m = ['^GSPC']

CAPM(stock_a,stock_m,start, end)

========================================

Beta from formula: 0.8131

Beta from Linear Regression: 0.8131

Alpha: 0.07

========================================

CAPM Line for META vs ^GSPC Monthly Returns

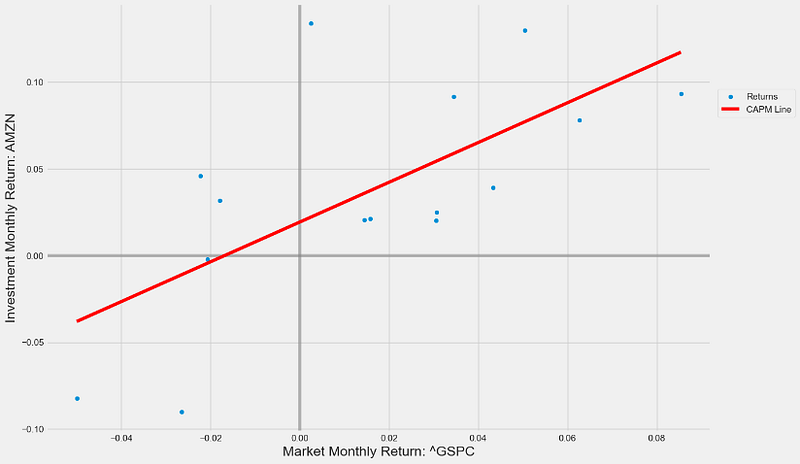

stock_a =['AMZN']

stock_m = ['^GSPC']

CAPM(stock_a,stock_m,start, end)

========================================

Beta from formula: 1.1471

Beta from Linear Regression: 1.1471

Alpha: 0.019

========================================

CAPM Line for AMZN vs ^GSPC Monthly Returns

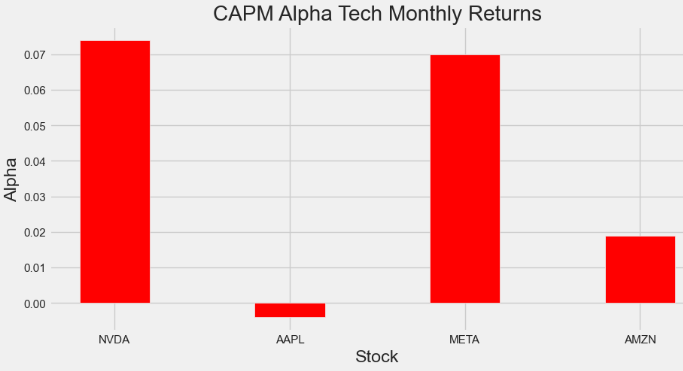

Creating a bar plot of the Estimated CAPM Alpha Tech Monthly Returns

# creating the dataset

data = {'NVDA':0.074, 'AAPL':-0.004, 'META':0.07,

'AMZN':0.019}

xvalues = list(data.keys())

yvalues = list(data.values())

fig = plt.figure(figsize = (10, 5))

# creating the bar plot

plt.bar(xvalues, yvalues, color ='red',

width = 0.4)

plt.xlabel("Stock")

plt.ylabel("Alpha")

plt.title("CAPM Alpha Tech Monthly Returns")

plt.show()

CAPM Alpha Tech Monthly Returns

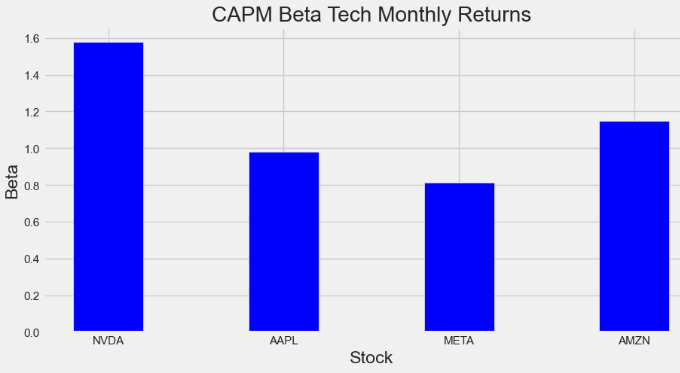

Creating a bar plot of the Estimated CAPM Beta Tech Monthly Returns

# creating the dataset

data = {'NVDA':1.5791, 'AAPL':0.9823, 'META':0.8131,

'AMZN':1.1471}

xvalues = list(data.keys())

yvalues = list(data.values())

fig = plt.figure(figsize = (10, 5))

# creating the bar plot

plt.bar(xvalues, yvalues, color ='blue',

width = 0.4)

plt.xlabel("Stock")

plt.ylabel("Beta")

plt.title("CAPM Beta Tech Monthly Returns")

plt.show()

CAPM Beta Tech Monthly Returns

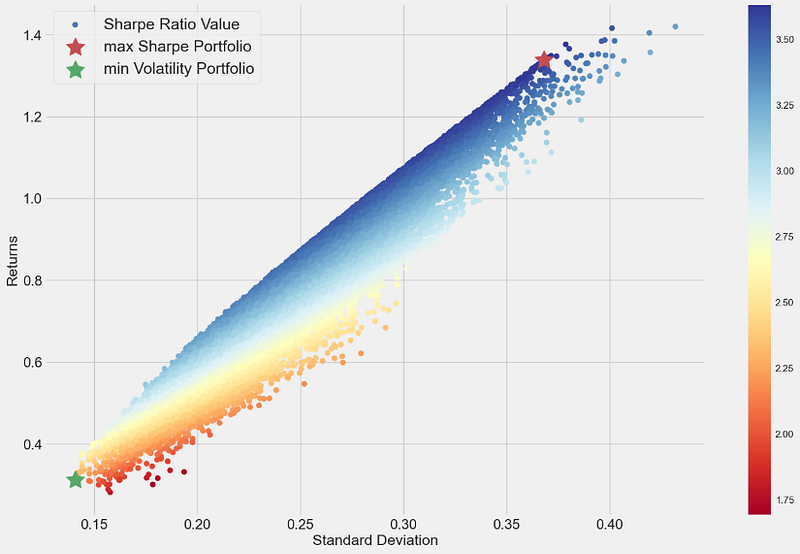

Max Sharpe Efficient Frontier

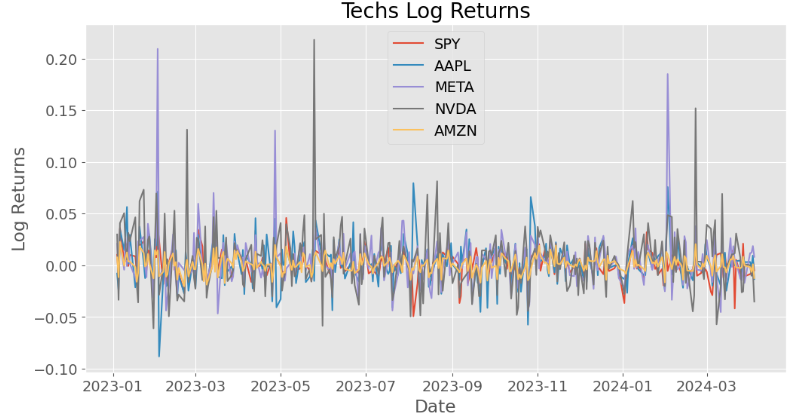

Let’s construct the Markowitz portfolio optimization model using the stochastic simulation algorithm. Our objective is to provide the highest Sharpe Ratio, which is a metric that compares the amount of return versus the amount of risk, based on historical data. Return is based on CAGR and risk is based on volatility. The portfolio is well suited for risk adverse investors with moderate growth expectations.

Creating max Sharpe and min Volatility Portfolios using simulated random portfolios

defcalc_portfolio_perf(weights, mean_returns, cov, rf):

portfolio_return = np.sum(mean_returns * weights) * 252

portfolio_std = np.sqrt(np.dot(weights.T, np.dot(cov, weights))) * np.sqrt(252)

sharpe_ratio = (portfolio_return - rf) / portfolio_std

return portfolio_return, portfolio_std, sharpe_ratio

defsimulate_random_portfolios(num_portfolios, mean_returns, cov, rf):

results_matrix = np.zeros((len(mean_returns)+3, num_portfolios))

for i inrange(num_portfolios):

weights = np.random.random(len(mean_returns))

weights /= np.sum(weights)

portfolio_return, portfolio_std, sharpe_ratio = calc_portfolio_perf(weights, mean_returns, cov, rf)

results_matrix[0,i] = portfolio_return

results_matrix[1,i] = portfolio_std

results_matrix[2,i] = sharpe_ratio

#iterate through the weight vector and add data to results arrayfor j inrange(len(weights)):

results_matrix[j+3,i] = weights[j]

results_df = pd.DataFrame(results_matrix.T,columns=['ret','stdev','sharpe'] + [ticker for ticker in tickers])

return results_df

mean_returns = df.pct_change().mean()

cov = df.pct_change().cov()

num_portfolios = 100000

rf = 0.0

results_frame = simulate_random_portfolios(num_portfolios, mean_returns, cov, rf)

#locate position of portfolio with highest Sharpe Ratio

max_sharpe_port = results_frame.iloc[results_frame['sharpe'].idxmax()]

#locate positon of portfolio with minimum standard deviation

min_vol_port = results_frame.iloc[results_frame['stdev'].idxmin()]

plt.rc('font', size=14)

#create scatter plot coloured by Sharpe Ratio

plt.subplots(figsize=(15,10))

plt.scatter(results_frame.stdev,results_frame.ret,c=results_frame.sharpe,cmap='RdYlBu')

plt.xlabel('Standard Deviation')

plt.ylabel('Returns')

plt.colorbar()

#plot red star to highlight position of portfolio with highest Sharpe Ratio

plt.scatter(max_sharpe_port[1],max_sharpe_port[0],marker=(5,1,0),color='r',s=500)

#plot green star to highlight position of minimum variance portfolio

plt.scatter(min_vol_port[1],min_vol_port[0],marker=(5,1,0),color='g',s=500)

plt.legend(["Sharpe Ratio Value","max Sharpe Portfolio" , "min Volatility Portfolio"],fontsize="18", loc ="upper left")

plt.yticks(fontsize=16)

plt.xticks(fontsize=16)

plt.show()

Simulated random portfolios, max Sharpe & min Volatility Portfolios

Comparing the 2 stock weighting tables that made up those two portfolios, along with the annualized return (ret), STDEV and Sharpe ratio, viz.

max_sharpe_port.to_frame().T

ret stdev sharpe SPY AAPL META NVDA AMZN

258251.3381560.368153.6348070.0059070.0280120.4704470.4800560.015578

min_vol_port.to_frame().T

ret stdev sharpe SPY AAPL META NVDA AMZN

575820.311990.1407412.2167720.7107720.2040890.0129640.0099550.06222

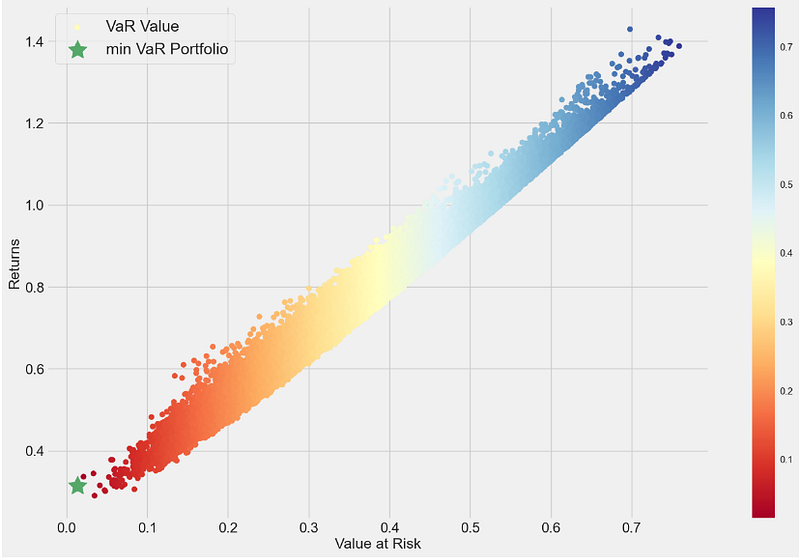

Min VaR Efficient Frontier

Identifying the portfolio weights that minimize the Value at Risk (VaR)

defcalc_portfolio_perf_VaR(weights, mean_returns, cov, alpha, days):

portfolio_return = np.sum(mean_returns * weights) * days

portfolio_std = np.sqrt(np.dot(weights.T, np.dot(cov, weights))) * np.sqrt(days)

portfolio_var = abs(portfolio_return - (portfolio_std * stats.norm.ppf(1 - alpha)))

return portfolio_return, portfolio_std, portfolio_var

defsimulate_random_portfolios_VaR(num_portfolios, mean_returns, cov, alpha, days):

results_matrix = np.zeros((len(mean_returns)+3, num_portfolios))

for i inrange(num_portfolios):

weights = np.random.random(len(mean_returns))

weights /= np.sum(weights)

portfolio_return, portfolio_std, portfolio_VaR = calc_portfolio_perf_VaR(weights, mean_returns, cov, alpha, days)

results_matrix[0,i] = portfolio_return

results_matrix[1,i] = portfolio_std

results_matrix[2,i] = portfolio_VaR

#iterate through the weight vector and add data to results arrayfor j inrange(len(weights)):

results_matrix[j+3,i] = weights[j]

results_df = pd.DataFrame(results_matrix.T,columns=['ret','stdev','VaR'] + [ticker for ticker in tickers])

return results_df

mean_returns = df.pct_change().mean()

cov = df.pct_change().cov()

num_portfolios = 100000

rf = 0.0

days = 252

alpha = 0.05

results_frame = simulate_random_portfolios_VaR(num_portfolios, mean_returns, cov, alpha, days)

#locate positon of portfolio with minimum VaR

min_VaR_port = results_frame.iloc[results_frame['VaR'].idxmin()]

#create scatter plot coloured by VaR

plt.subplots(figsize=(15,10))

plt.scatter(results_frame.VaR,results_frame.ret,c=results_frame.VaR,cmap='RdYlBu')

plt.xlabel('Value at Risk')

plt.ylabel('Returns')

plt.colorbar()

#plot red star to highlight position of minimum VaR portfolio

plt.scatter(min_VaR_port[2],min_VaR_port[0],marker=(5,1,0),color='g',s=500)

plt.legend(["VaR Value","min VaR Portfolio"] ,fontsize="18", loc ="upper left")

plt.yticks(fontsize=16)

plt.xticks(fontsize=16)

plt.show()

Simulated random portfolios & min VaR Portfolio

The stock weighting table that made up the above portfolio is given by

min_VaR_port.to_frame().T

ret stdev VaR SPY AAPL META NVDA AMZN

205370.3142270.1829320.013330.1596290.7791880.0172460.0168460.027091

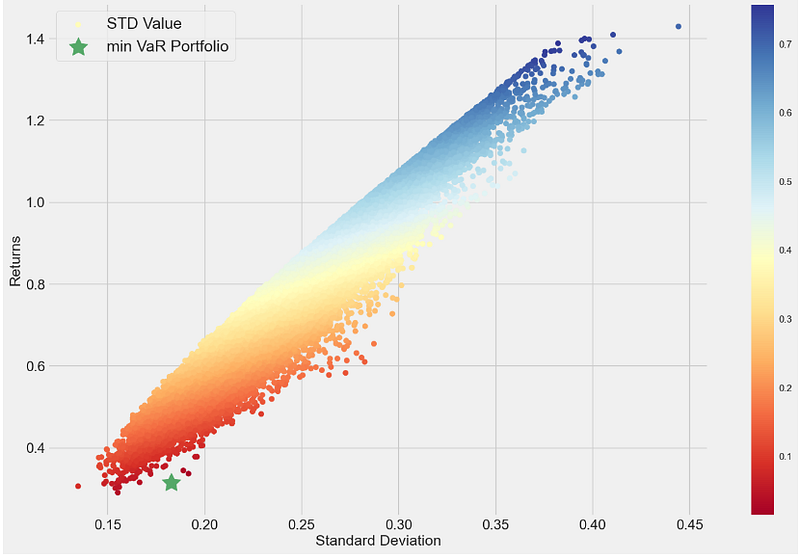

Finally, converting the horizontal axis from VaR to STDEV (cf. here)

#locate positon of portfolio with minimum VaR

min_VaR_port = results_frame.iloc[results_frame['VaR'].idxmin()]

#create scatter plot coloured by VaR

plt.subplots(figsize=(15,10))

plt.scatter(results_frame.stdev,results_frame.ret,c=results_frame.VaR,cmap='RdYlBu')

plt.xlabel('Standard Deviation')

plt.ylabel('Returns')

plt.colorbar()

#plot red star to highlight position of minimum VaR portfolio

plt.scatter(min_VaR_port[1],min_VaR_port[0],marker=(5,1,0),color='g',s=500)

plt.legend(["STD Value","min VaR Portfolio"] ,fontsize="18", loc ="upper left")

plt.yticks(fontsize=16)

plt.xticks(fontsize=16)

plt.show()

Simulated random portfolios & min VaR Portfolio in the Returns — STDEV plane

Conclusions

In this post, we have compared several popular stochastic portfolio optimization techniques that maximize returns while minimizing risk, excluding product costs and related fees.

It turns out that max Sharpe is the best tech portfolio in terms of the ret-to-stdev ratio

minVaR minVol maxSharpe

ret % 3131134

stdev % 181437

ratio 1.722.213.62

We have compared the CAPM Lines of Monthly Returns for our stocks against the benchmark (^GSPC).

According to the estimated CAPM Alpha (Beta), a positive value of 0.074 (0.81) is good for NVDA (META) as compared to other 3 tech stocks.

Results confirm that NVDA and META remain our tech growth stocks in focus today, indicating bullish sentiments.