Markowitz portfolio:

What is markowitz portfolio?

“The Markowitz Portfolio Theory, developed by Harry Markowitz in the 1950s, is a mathematical framework for constructing investment portfolios that seek to balance risk and return. It’s based on the idea that investors can achieve a more efficient portfolio by diversifying their investments across assets with different risk and return profiles.”

● Key concepts of the Markowitz Portfolio Theory include:

- Risk and Return: It quantifies the risk and return of individual assets and considers how they interact when combined in a portfolio.

2. Efficient Frontier: The theory aims to find the set of portfolios that offer the highest expected return for a given level of risk or the lowest risk for a given level of expected return. This set of portfolios is known as the efficient frontier.

3. Diversification: Markowitz emphasized the importance of diversifying investments to reduce overall portfolio risk. By spreading investments across different assets, the theory seeks to achieve a more favorable risk-return trade-off.

Correlation: The theory considers the correlation between assets, as negatively correlated assets can help reduce portfolio risk more effectively.

4. Risk-averse Investors: It assumes that investors are risk-averse, meaning they prefer portfolios that offer higher returns for a given level of risk or lower risk for a given level of return.

In practice, portfolio managers and investors use the Markowitz Portfolio Theory to select a combination of assets that align with their risk tolerance and return objectives. Modern portfolio management techniques, such as the Capital Asset Pricing Model (CAPM) and the Sharpe Ratio, build upon Markowitz's work to help investors make informed investment decisions.

➡️ Example of markowitz portfolio:

Certainly, let's walk through a simplified example of a Markowitz portfolio:

Suppose you are an investor looking to create a portfolio from two assets: Stock A and Stock B. You want to find the optimal allocation of these assets to maximize your expected return while managing risk.

Here are some hypothetical details:

Stock A:

Expected Annual Return: 10%

Standard Deviation (a measure of risk): 15%

Stock B:

Expected Annual Return: 8%

Standard Deviation: 10%

Now, the correlation between these two stocks is an important factor. Let's assume that the correlation between Stock A and Stock B is 0.4. A positive correlation means that they tend to move in the same direction, but not perfectly.

To construct a Markowitz portfolio:

- Calculate the expected return and risk (standard deviation) of various portfolio combinations.

2. Vary the allocation between Stock A and Stock B, for example, you can allocate 30% to Stock A and 70% to Stock B.

3. Calculate the expected portfolio return and risk for each allocation using the correlation between the two stocks.

4. Repeat this process for different allocations, and you will create a set of portfolios with varying risk-return profiles. Some portfolios will have higher expected returns but also higher risk, while others will have lower returns but lower risk.

The efficient frontier represents the combinations of these assets that provide the best risk-return trade-offs. You can then choose a portfolio along the efficient frontier that aligns with your risk tolerance and return objectives.

In practice, financial software and tools are often used to perform these calculations, as they involve complex mathematical optimizations. The goal is to find the portfolio allocation that suits your investment preferences while considering the trade-off between risk and return.

➡️ Benefits of markowitz portfolio in finance:

The Markowitz Portfolio Theory offers several benefits in the field of finance:

a) Risk Management: Markowitz’s theory is fundamentally about managing risk. By diversifying a portfolio across assets with different risk profiles and correlations, investors can reduce overall portfolio risk. This is crucial for protecting investments during market downturns.

b) Optimal Risk-Return Trade-off: It helps investors find the optimal balance between risk and return. The theory identifies portfolios on the efficient frontier that offer the highest expected return for a given level of risk or the lowest risk for a given level of expected return. This aids in making informed investment decisions aligned with an investor’s risk tolerance.

c) Diversification: Markowitz highlights the importance of diversification. A diversified portfolio can lower the impact of a poor-performing asset on the entire portfolio. It’s a way to "not put all your eggs in one basket," reducing the potential for catastrophic losses.

d) Quantitative Approach: The theory provides a quantitative framework for portfolio construction. It allows investors and portfolio managers to use mathematical models to assess and optimize their investment strategies, which can lead to more objective decision-making.

e) Foundation for Modern Portfolio Theory: Markowitz’s work laid the foundation for subsequent advancements in finance, such as the Capital Asset Pricing Model (CAPM) and the Arbitrage Pricing Theory (APT). These models are widely used in pricing and evaluating assets.

f) Performance Evaluation: Portfolio managers can use Markowitz Portfolio Theory to evaluate the performance of their portfolios. By comparing the actual performance of a portfolio to the expected performance based on the theory, they can assess whether their investment decisions are adding value.

g) Asset Allocation: The theory is instrumental in determining the allocation of assets within a portfolio. It helps investors decide how much to allocate to different asset classes (e.g., stocks, bonds, real estate) to achieve their financial goals.

h) Risk Assessment: It encourages a more sophisticated assessment of risk. Instead of merely looking at the historical performance of assets, investors consider how assets interact with each other, accounting for correlations and variances, leading to a more comprehensive risk assessment.

i) Long-Term Perspective: Markowitz Portfolio Theory encourages investors to take a long-term perspective. By focusing on the risk-return trade-off over time, it can help investors avoid making impulsive decisions based on short-term market fluctuations.

j) Widespread Use: It’s widely taught in finance and used by professionals in asset management, wealth management, and investment banking, making it a common language and framework in the financial industry.

While Markowitz Portfolio Theory has been criticized for its simplifications and assumptions, it remains a valuable tool for understanding and managing investment portfolios. Many of its principles are still relevant in today’s complex financial markets.

➡️ Uses of markowitz in finance :

The Markowitz Portfolio Theory has several practical uses in finance:

Portfolio Construction: Markowitz Portfolio Theory is primarily used to construct portfolios that optimize the trade-off between risk and return. Investors and portfolio managers use this theory to select the right mix of assets that align with their investment objectives and risk tolerance.

Risk Management: It plays a crucial role in risk management. By diversifying investments across assets with low or negative correlations, investors can reduce the overall risk of their portfolio. This diversification strategy helps protect investments during market downturns.

Asset Allocation: Markowitz's theory is integral to the process of asset allocation. It guides investors in deciding how much to allocate to different asset classes, such as stocks, bonds, real estate, and more, to achieve their financial goals while managing risk.

Performance Evaluation: Portfolio managers and investors can use Markowitz Portfolio Theory to evaluate the performance of their portfolios. They can compare the actual performance of their portfolio to the expected performance based on the theory's predictions.

Risk Assessment: The theory provides a comprehensive approach to assessing risk. Instead of relying solely on historical performance data, it considers how different assets interact with each other in terms of risk and return, providing a more nuanced understanding of portfolio risk.

Investment Decision-Making: It aids in making informed investment decisions. Investors can use the theory to analyze the potential impact of adding or removing specific assets from their portfolios, helping them make decisions that align with their investment goals.

Hedging Strategies: In the context of derivatives and hedging, Markowitz Portfolio Theory can be used to construct hedging strategies that balance risk exposure in a portfolio. This is especially important for institutions and investors with complex financial positions.

Benchmarking: Portfolio managers often use the efficient frontier as a benchmark for their portfolios. They aim to outperform this frontier to demonstrate that their portfolio's risk-return profile is superior to a diversified mix of assets.

Long-Term Investment Planning: Markowitz's approach encourages investors to take a long-term perspective by focusing on the risk-return trade-off over time. This is particularly useful for retirement planning and long-term financial goals.

Academic Research: The theory continues to be a subject of academic research in finance. Researchers use it as a foundation to develop more sophisticated models and explore various aspects of portfolio management and asset pricing.

Risk-Adjusted Performance Metrics: Risk-adjusted performance metrics like the Sharpe Ratio and Treynor Ratio, which are based on Markowitz's work, are widely used to assess the performance of investment portfolios and individual assets.

Overall, Markowitz Portfolio Theory is a fundamental framework that helps investors and financial professionals make rational and informed decisions in the complex world of finance by considering the trade-off between risk and return.

How markowitz influence finance management ?

Harry Markowitz's work on Portfolio Theory has had a profound influence on the field of finance and investment management in several ways:

Diversification: Markowitz's insight into the benefits of diversification has greatly influenced the way investors manage their portfolios. Diversifying across different assets or asset classes is now a standard practice to spread risk and enhance long-term returns.

Risk-Return Trade-off: Markowitz's theory introduced the concept of optimizing the risk-return trade-off. This concept is central to modern finance management, where investors and portfolio managers aim to balance the potential for higher returns with the associated risk.

Asset Allocation: The theory is a cornerstone of asset allocation strategies. Investment professionals use it to determine how much of a portfolio should be allocated to various asset classes like stocks, bonds, and alternative investments.

Efficient Frontier: The efficient frontier, a key concept from Markowitz's work, guides investors in constructing portfolios that offer the best possible returns for a given level of risk or the lowest risk for a given level of return. This helps in designing portfolios tailored to investors' goals and risk tolerance.

Risk Management: Markowitz's approach is foundational for risk management in finance. Portfolio managers use his principles to manage and mitigate risks associated with investments.

Modern Portfolio Management Tools: The Markowitz Portfolio Theory laid the groundwork for various modern portfolio management tools and techniques, including the Capital Asset Pricing Model (CAPM), Arbitrage Pricing Theory (APT), and the development of risk-adjusted performance measures like the Sharpe Ratio and Treynor Ratio.

Quantitative Analysis: It introduced quantitative methods into investment decision-making. Financial professionals use mathematical models and computer algorithms to optimize portfolios, taking into account asset correlations and return expectations.

Academic Research: Markowitz's work has spurred extensive academic research in finance. Researchers have built upon his theory to develop more sophisticated models, test hypotheses, and expand the understanding of portfolio management and asset pricing.

Investment Industry Standards: Markowitz's theories have influenced industry standards and regulations. For example, pension funds, endowments, and other institutional investors often follow principles derived from his work when managing their portfolios.

Education: Portfolio Theory is a fundamental topic in finance education. Students and professionals learn about the theory to gain a solid understanding of portfolio construction and management.

In summary, Harry Markowitz's Portfolio Theory has significantly shaped the practice of finance management. It has provided a systematic and mathematical approach to portfolio construction, risk management, and asset allocation, helping investors and financial professionals make more informed decisions in the world of finance.

Result of markowitz portfolio :

The result of a Markowitz portfolio analysis is typically a set of portfolios that represent different combinations of assets or asset classes. These portfolios are designed to achieve specific risk and return objectives. Here are some key results you can expect from a Markowitz portfolio analysis:

Efficient Frontier: The primary result is the efficient frontier, which is a graphical representation of portfolios that offer the maximum expected return for a given level of risk or the minimum risk for a given level of expected return. The efficient frontier is a key outcome of the analysis and is central to portfolio optimization.

Optimal Portfolio: Within the efficient frontier, there is one portfolio that represents the optimal trade-off between risk and return based on the investor's preferences. This portfolio is often referred to as the "tangency portfolio" or the "optimal portfolio" and is typically the recommended allocation for the investor.

Portfolio Allocations: The analysis provides specific allocations or weightings for each asset or asset class within the optimal portfolio. For example, it might recommend allocating a certain percentage to stocks, bonds, real estate, and other assets to achieve the desired risk-return profile.

Risk and Return Metrics: The analysis provides quantitative measures of risk and return for the recommended portfolio and other portfolios along the efficient frontier. This includes expected return, standard deviation (a measure of risk), and other risk-adjusted performance metrics like the Sharpe Ratio.

Comparison with Current Portfolio: Investors can compare the characteristics of their current portfolio to the results of the Markowitz analysis. This helps in evaluating whether their existing portfolio aligns with their risk and return objectives or if adjustments are needed.

Sensitivity Analysis: Some portfolio analysis tools allow for sensitivity analysis, where investors can explore how changes in expected returns or correlations among assets impact portfolio outcomes. This helps investors understand the robustness of their portfolio choices.

Risk-Return Trade-off Insights: The analysis provides insights into the trade-off between risk and return. Investors can see how adjusting their portfolio allocation affects the level of risk they are exposed to and the potential return they can expect.

Visual Representation: Efficient frontier plots and risk-return scatterplots are often used to visually represent the results. These visuals help investors and advisors better understand the relationship between risk and return.

Portfolio Recommendations: Based on the analysis, investors may receive specific portfolio recommendations tailored to their financial goals, risk tolerance, and time horizon.

The ultimate goal of a Markowitz portfolio analysis is to help investors make informed decisions about how to allocate their investments in a way that aligns with their financial objectives and risk preferences while achieving an optimal risk-return balance.

Mathematical model of markowitz portfolio:

The mathematical model for Markowitz Portfolio Theory involves several equations and calculations to optimize portfolio construction. Here are the key components of the mathematical model:

1)Expected Return (μ):

The expected return of a portfolio is calculated as the weighted average of the expected returns of its individual assets. If you have n assets in the portfolio, the expected return (μ) is given by:

μ = w₁ * μ₁ + w₂ * μ₂ + ... + wₙ * μₙ

where:

μ₁, μ₂, ..., μₙ are the expected returns of the individual assets.

w₁, w₂, ..., wₙ are the weights (allocations) of each asset in the portfolio.

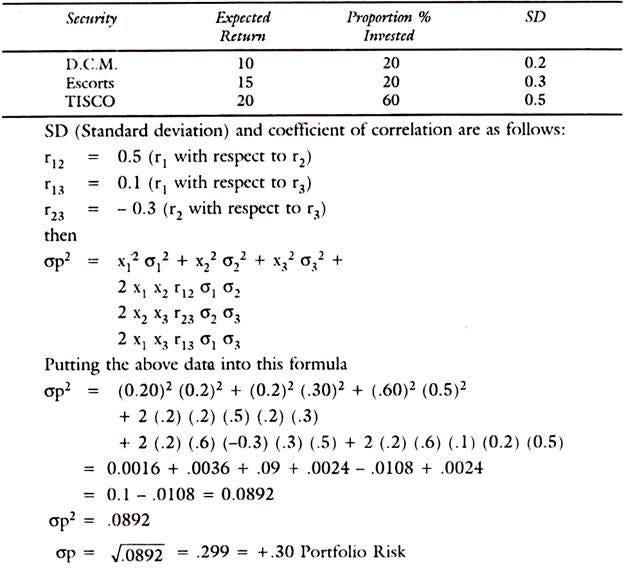

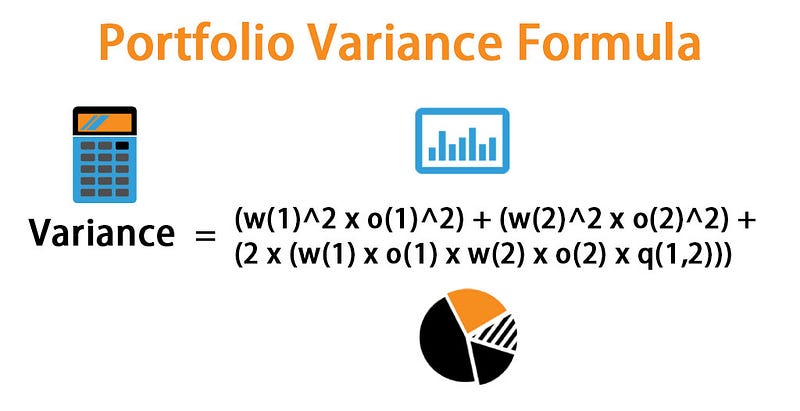

2)Portfolio Variance (σ²):

The portfolio variance represents the risk of the portfolio. It's calculated as the sum of all possible pairs of assets' covariances, weighted by their respective portfolio weights. If you have n assets, the portfolio variance (σ²) is given by:

σ² = w₁² * σ₁² + w₂² * σ₂² + ... + wₙ² * σₙ² + 2 * w₁ * w₂ * σ₁₂ + 2 * w₁ * w₃ * σ₁₃ + ... + 2 * wₙ₋₁ * wₙ * σₙ₋₁ₙ

where:

σ₁², σ₂², ..., σₙ² are the variances of the individual assets.

σ₁₂, σ₁₃, ..., σₙ₋₁ₙ are the covariances between pairs of assets.

Portfolio Standard Deviation (σ): The standard deviation of the portfolio is the square root of the portfolio variance. It represents the volatility or risk of the portfolio.

σ = √(σ²)

3)Risk-Free Rate (Rf): If you are considering a risk-free asset like Treasury bills, you incorporate the risk-free rate into the model. The risk-free rate represents the return an investor can earn with no risk. It’s typically used as a baseline for comparing the performance of a portfolio.

4) Optimization: The goal is to find the portfolio weights (w₁, w₂, ..., wₙ) that maximize the expected return for a given level of risk (standard deviation) or minimize the risk for a given level of expected return. This is typically done using mathematical optimization techniques such as the quadratic programming or the Sharpe ratio maximization.

Constraints can also be added, such as budget constraints (the sum of weights equals 1), minimum and maximum allocation limits, and so on.

5) Efficient Frontier: The efficient frontier is generated by running the optimization for various target levels of return or risk. This results in a curve or line representing the portfolios that achieve the best risk-return trade-offs.

6) Tangency Portfolio: The point where the efficient frontier is tangent to the Capital Market Line (CML) represents the optimal portfolio—the portfolio that offers the best risk-return trade-off. This is often referred to as the "tangency portfolio."

7)Sharpe Ratio: The Sharpe Ratio is a key performance measure derived from the model. It calculates the excess return of a portfolio per unit of risk (standard deviation) and is used to evaluate and compare portfolio performance.

This mathematical model forms the basis for constructing portfolios that aim to optimize the risk-return trade-off, taking into account the expected returns and covariances of assets. In practice, financial software and tools are commonly used to perform these calculations efficiently.