Backtesting Hybrid CI & MACD Trading Strategies for NVIDIA

Featured image template via Canva.

- In this post, we’ll take a closer look at backtesting NVIDIA (NASDAQ: NVDA) algo-trading strategies in Python that maximize the ROI/Risk ratio by combining Chopping Index (CHOP/CI) & MACD technical indicators, as explained here.

- The CI indicates whether a choppy market exists. A choppy market refers to a period of market volatility where a trend is generally absent.

- As a range-bound oscillator, the CI has values within the range [1,100]. The closer the value is to 100, the higher the sideways movement levels.

- A CI value above MAX0=61.8 indicates a trending market, while a value below MIN0=38.2 indicates a choppy market.

- In this study, we’ll set MIN=50 and MAX=MAX0 because the default value MIN0 leads to lower ROI for NVDA within the time frame of interest.

- The Moving Average Convergence/Divergence (MACD) indicator is designed to help investors identify price trends, measure trend momentum, and identify market entry points for buying or selling.

- MACD is best used with daily periods, where the traditional settings of 26/12/9 days is the default.

- Why CI + MACD: While the MACD is effective in trend confirmation, the CI can quickly respond to immediate price fluctuations if the market is trading sideways.

- Let’s get down to implementation details!

Reading Input Stock Data

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()- Importing basic libraries and reading the 2Y NVDA historical data

import pandas as pd

import requests

import matplotlib.pyplot as plt

import numpy as np

plt.style.use('fivethirtyeight')

plt.rcParams['figure.figsize'] = (20, 10)

def get_historical_data(symbol, start_date):

api_key = 'YOUR API KEY'

api_url = f'https://api.twelvedata.com/time_series?symbol={symbol}&interval=1day&outputsize=5000&apikey={api_key}'

raw_df = requests.get(api_url).json()

df = pd.DataFrame(raw_df['values']).iloc[::-1].set_index('datetime').astype(float)

df = df[df.index >= start_date]

df.index = pd.to_datetime(df.index)

return df

tsla = get_historical_data('NVDA', '2022-01-01')

tsla

open high low close volume

datetime

2022-01-03 298.14999 307.10999 297.85001 301.20999 39240296.0

2022-01-04 302.76999 304.67999 283.48999 292.89999 52715440.0

2022-01-05 289.48999 294.16000 275.32999 276.04001 49806388.0

2022-01-06 276.39999 284.37991 270.64999 281.78000 45418636.0

2022-01-07 281.41000 284.22000 270.57001 272.47000 40993852.0

... ... ... ... ... ...

2024-04-05 868.65997 884.81000 859.26001 880.08002 39885700.0

2024-04-08 887.00000 888.29999 867.32001 871.33002 28322000.0

2024-04-09 874.41998 876.34998 830.21997 853.53998 50354700.0

2024-04-10 839.26001 874.00000 837.09003 870.39001 43192900.0

2024-04-11 874.20001 907.39001 869.26001 906.15997 42969300.0

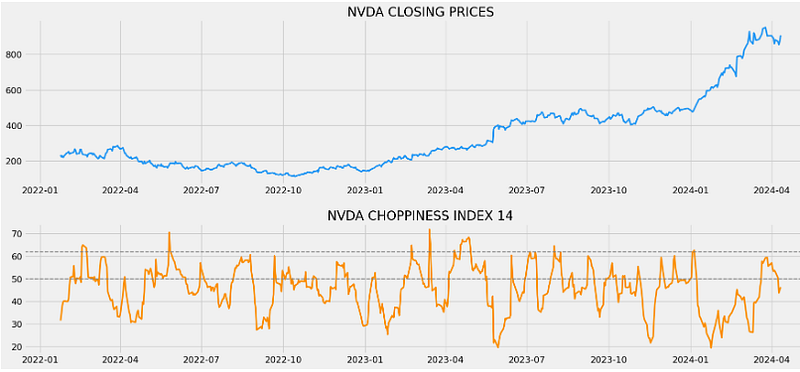

571 rows × 5 columnsCI Indicator

- Calculating and plotting the CI 14 indicator

def get_ci(high, low, close, lookback):

tr1 = pd.DataFrame(high - low).rename(columns = {0:'tr1'})

tr2 = pd.DataFrame(abs(high - close.shift(1))).rename(columns = {0:'tr2'})

tr3 = pd.DataFrame(abs(low - close.shift(1))).rename(columns = {0:'tr3'})

frames = [tr1, tr2, tr3]

tr = pd.concat(frames, axis = 1, join = 'inner').dropna().max(axis = 1)

atr = tr.rolling(1).mean()

highh = high.rolling(lookback).max()

lowl = low.rolling(lookback).min()

ci = 100 * np.log10((atr.rolling(lookback).sum()) / (highh - lowl)) / np.log10(lookback)

return ci

tsla['ci_14'] = get_ci(tsla['high'], tsla['low'], tsla['close'], 14)

tsla = tsla.dropna()

tsla

ax1 = plt.subplot2grid((11,1,), (0,0), rowspan = 5, colspan = 1)

ax2 = plt.subplot2grid((11,1,), (6,0), rowspan = 4, colspan = 1)

ax1.plot(tsla['close'], linewidth = 2.5, color = '#2196f3')

ax1.set_title('NVDA CLOSING PRICES')

ax2.plot(tsla['ci_14'], linewidth = 2.5, color = '#fb8c00')

ax2.axhline(50, linestyle = '--', linewidth = 1.5, color = 'grey')

ax2.axhline(61.8, linestyle = '--', linewidth = 1.5, color = 'grey')

ax2.set_title('NVDA CHOPPINESS INDEX 14')

plt.show()

MACD Indicator

- Calculating the MACD 26/12/9 indicator

def get_macd(price, slow, fast, smooth):

exp1 = price.ewm(span = fast, adjust = False).mean()

exp2 = price.ewm(span = slow, adjust = False).mean()

macd = pd.DataFrame(exp1 - exp2).rename(columns = {'close':'macd'})

signal = pd.DataFrame(macd.ewm(span = smooth, adjust = False).mean()).rename(columns = {'macd':'signal'})

hist = pd.DataFrame(macd['macd'] - signal['signal']).rename(columns = {0:'hist'})

frames = [macd, signal, hist]

df = pd.concat(frames, join = 'inner', axis = 1)

return df

tsla_macd = get_macd(tsla['close'], 26, 12, 9)

tsla_macd.tail()

macd signal hist

datetime

2024-04-05 24.096374 37.124507 -13.028134

2024-04-08 20.667086 33.833023 -13.165937

2024-04-09 16.325652 30.331549 -14.005897

2024-04-10 14.082358 27.081711 -12.999353

2024-04-11 15.017752 24.668919 -9.65116CI & MACD Trading Strategy

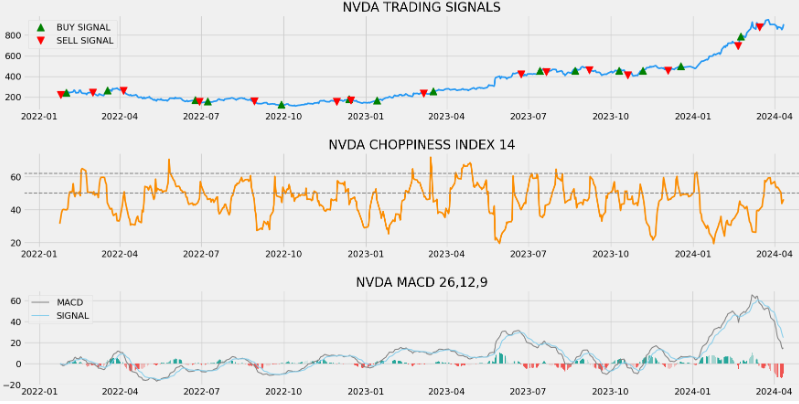

- Implementing the hybrid CI & MACD trading strategy and plotting the resulting NVDA trading signals

par=50

# Implementing the CI & MACD trading strategy

def implement_ci_macd_strategy(prices, data, ci):

buy_price = []

sell_price = []

ci_macd_signal = []

signal = 0

for i in range(len(prices)):

if data['macd'][i] > data['signal'][i] and ci[i] < par:

if signal != 1:

buy_price.append(prices[i])

sell_price.append(np.nan)

signal = 1

ci_macd_signal.append(signal)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

ci_macd_signal.append(0)

elif data['macd'][i] < data['signal'][i] and ci[i] < par:

if signal != -1:

buy_price.append(np.nan)

sell_price.append(prices[i])

signal = -1

ci_macd_signal.append(signal)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

ci_macd_signal.append(0)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

ci_macd_signal.append(0)

return buy_price, sell_price, ci_macd_signal

#Plotting CI & MACD trading signals

buy_price, sell_price, ci_macd_signal = implement_ci_macd_strategy(tsla['close'], tsla_macd, tsla['ci_14'])

ax1 = plt.subplot2grid((19,1,), (0,0), rowspan = 5, colspan = 1)

ax2 = plt.subplot2grid((19,1), (7,0), rowspan = 5, colspan = 1)

ax3 = plt.subplot2grid((19,1), (14,0), rowspan = 5, colspan = 1)

ax1.plot(tsla['close'], linewidth = 2.5, color = '#2196f3')

ax1.plot(tsla.index, buy_price, marker = '^', color = 'green', markersize = 12, label = 'BUY SIGNAL', linewidth = 0)

ax1.plot(tsla.index, sell_price, marker = 'v', color = 'r', markersize = 12, label = 'SELL SIGNAL', linewidth = 0)

ax1.legend()

ax1.set_title('NVDA TRADING SIGNALS')

ax2.plot(tsla['ci_14'], linewidth = 2.5, color = '#fb8c00')

ax2.axhline(50, linestyle = '--', linewidth = 1.5, color = 'grey')

ax2.axhline(61.8, linestyle = '--', linewidth = 1.5, color = 'grey')

ax2.set_title('NVDA CHOPPINESS INDEX 14')

ax3.plot(tsla_macd['macd'], color = 'grey', linewidth = 1.5, label = 'MACD')

ax3.plot(tsla_macd['signal'], color = 'skyblue', linewidth = 1.5, label = 'SIGNAL')

for i in range(len(tsla_macd)):

if str(tsla_macd['hist'][i])[0] == '-':

ax3.bar(tsla_macd.index[i], tsla_macd['hist'][i], color = '#ef5350')

else:

ax3.bar(tsla_macd.index[i], tsla_macd['hist'][i], color = '#26a69a')

ax3.legend()

ax3.set_title('NVDA MACD 26,12,9')

plt.show()

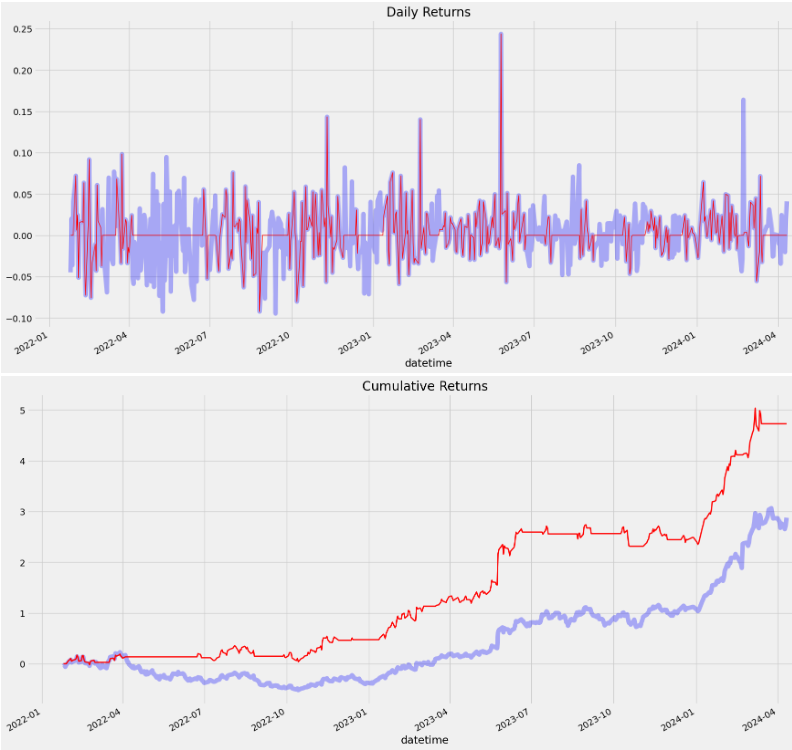

Daily & Cumulative Returns

- Formulating the NVDA stock trading position and calculating the daily/cumulative returns since 2022–01–01

osition = []

for i in range(len(ci_macd_signal)):

if ci_macd_signal[i] > 1:

position.append(0)

else:

position.append(1)

for i in range(len(tsla['close'])):

if ci_macd_signal[i] == 1:

position[i] = 1

elif ci_macd_signal[i] == -1:

position[i] = 0

else:

position[i] = position[i-1]

ci = tsla['ci_14']

close_price = tsla['close']

ci_macd_signal = pd.DataFrame(ci_macd_signal).rename(columns = {0:'ci_macd_signal'}).set_index(tsla.index)

position = pd.DataFrame(position).rename(columns = {0:'ci_macd_position'}).set_index(tsla.index)

frames = [close_price, ci, ci_macd_signal, position]

strategy = pd.concat(frames, join = 'inner', axis = 1)

strategy.head()

rets = tsla.close.pct_change()[1:]

strat_rets = strategy.ci_macd_position[1:] * rets

plt.title('Daily Returns')

rets.plot(color = 'blue', alpha = 0.3, linewidth = 7)

strat_rets.plot(color = 'r', linewidth = 1)

plt.show()

rets_cum = (1 + rets).cumprod() - 1

strat_cum = (1 + strat_rets).cumprod() - 1

plt.title('Cumulative Returns')

rets_cum.plot(color = 'blue', alpha = 0.3, linewidth = 7)

strat_cum.plot(color = 'r', linewidth = 2)

plt.show()

Backtesting ROI

- Calculating the profit gained from the CI-MACD strategy by investing $10k in NVDA

from termcolor import colored as cl

fb_ret = pd.DataFrame(np.diff(tsla['close'])).rename(columns = {0:'returns'})

cci_strategy_ret = []

for i in range(len(fb_ret)):

returns = fb_ret['returns'][i]*strategy['ci_macd_position'][i]

cci_strategy_ret.append(returns)

cci_strategy_ret_df = pd.DataFrame(cci_strategy_ret).rename(columns = {0:'ci_macd_returns'})

investment_value = 10000

number_of_stocks = np.floor(investment_value/tsla['close'][-1])

cci_investment_ret = []

for i in range(len(cci_strategy_ret_df['ci_macd_returns'])):

returns = number_of_stocks*cci_strategy_ret_df['ci_macd_returns'][i]

cci_investment_ret.append(returns)

cci_investment_ret_df = pd.DataFrame(cci_investment_ret).rename(columns = {0:'investment_returns'})

total_investment_ret = round(sum(cci_investment_ret_df['investment_returns']), 2)

profit_percentage = round((total_investment_ret/investment_value)*100, 2)

print(cl('Profit gained from the CI-MACD strategy by investing $10k in NVDA : {}'.format(total_investment_ret), attrs = ['bold']))

print(cl('Profit percentage of the CI-MACD strategy : {}%'.format(profit_percentage), attrs = ['bold']))

Profit gained from the CI-MACD strategy by investing $10k in NVDA : 4908.31

Profit percentage of the CI-MACD strategy : 49.08%SPY ETF Benchmark

- Considering the SPY ETF benchmark

# SPY ETF COMPARISON

def get_benchmark(start_date, investment_value):

spy = get_historical_data('SPY', start_date)['close']

benchmark = pd.DataFrame(np.diff(spy)).rename(columns = {0:'benchmark_returns'})

investment_value = investment_value

number_of_stocks = np.floor(investment_value/spy[0])

benchmark_investment_ret = []

for i in range(len(benchmark['benchmark_returns'])):

returns = number_of_stocks*benchmark['benchmark_returns'][i]

benchmark_investment_ret.append(returns)

benchmark_investment_ret_df = pd.DataFrame(benchmark_investment_ret).rename(columns = {0:'investment_returns'})

return benchmark_investment_ret_df

benchmark = get_benchmark('2022-01-01', 10000)

investment_value = 10000

total_benchmark_investment_ret = round(sum(benchmark['investment_returns']), 2)

benchmark_profit_percentage = np.floor((total_benchmark_investment_ret/investment_value)*100)

print(cl('Benchmark profit by investing $10k : {}'.format(total_benchmark_investment_ret), attrs = ['bold']))

print(cl('Benchmark Profit percentage : {}%'.format(benchmark_profit_percentage), attrs = ['bold']))

print(cl('CI-MACD Strategy profit is {}% higher than the Benchmark Profit'.format(profit_percentage - benchmark_profit_percentage), attrs = ['bold']))

Benchmark profit by investing $10k : 805.8

Benchmark Profit percentage : 8.0%

CI-MACD Strategy profit is 41.08% higher than the Benchmark ProfitConclusions

- We have shown that the hybrid CI & MACD algo-trading strategy is a valuable tool in analyzing market trends, sideways movements and making informed trading decisions. Specifically, CI helps distinguish sideways movements from trending market activity, while it’s also used to evaluate an asset’s volatility.

- This article describes the purpose, calculation, and application of this efficient strategy.

- 2Y backtesting results: ROI of the strategy is 49.08%.

- 2Y SPY ETF benchmark: the strategy ROI is 41.08% higher than the benchmark.

- Future work: predicting NVDA stock price using ML/AI and statistical modeling approaches.

Explore More

- A Market-Neutral Strategy

- Returns-Volatility Domain K-Means Clustering and LSTM Anomaly Detection of S&P 500 Stocks

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- NVIDIA Rolling Volatility: GARCH & XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

E-Training Guides

- Towards Max(ROI/Risk) Trading

- Algorithmic Testing Stock Portfolios to Optimize the Risk/Reward Ratio

- Basic Stock Price Analysis in Python

- Quant Trading using Monte Carlo Predictions and 62 AI-Assisted Trading Technical Indicators (TTI)

References

- Detecting Ranging and Trending Markets with Choppiness Index in Python

- What is CHOP indicator in Trading and Why it is Important?

- Risk-Return Tradeoff: How the Investment Principle Works

- What Is MACD?

- Choppiness Index (CHOP)

- Choppy Market: Overview and Examples of Trendless Trading

- Choppiness Index