BTC Price Prediction using FB Prophet

- In this article we are going to discuss the BTC price prediction using the FB Prophet algorithm in Python.

- Utilizing historical BTC-USD data, the project employs this statistical modeling library to predict future BTC prices, contributing to informed decision-making in cryptocurrency markets.

- Predicting the BTC price accurately is a difficult task due to its high volatility. One of the major problems with many price predictions about BTC is that they lack sufficient analytical support to back up their claims.

- Where Prophet shines: It appears that by combining automatic forecasting with analyst-in-the-loop forecasts for special cases, it is possible to cover a wide variety of business use-cases.

- At its core, the Prophet procedure is a regression model with four main components: a piecewise linear or logistic growth curve trend; a yearly seasonal component modeled using Fourier series; a weekly seasonal component using dummy variables; a user-provided list of important holidays.

- Let’s delve into details.

Basic Imports, Installations & Setups

- Installing and activating the slim Miniconda environment from cmd

conda activate my-conda-env

- To deactivate this environment on Windows, run

conda deactivate

- Launching the Jupyter Notebook

jupyter notebook

- Creating a new project in the Notebook and selecting Python-3.

- Setting a working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()- Importing and installing the following Python libraries

!pip install plotly, statsmodels, termcolor, math, requests, prophet, itertools

import pandas as pd

import plotly.express as px

import requests

import numpy as np

import matplotlib.pyplot as plt

from math import floor

from termcolor import colored as cl

from statsmodels.base.transform import BoxCox

from prophet import Prophet

plt.rcParams['figure.figsize'] = (20, 10)

plt.style.use('fivethirtyeight')Reading & Plotting Input Data

- Reading the Bitcoin USD (BTC-USD) stock data 2021/01–2023/09

def get_crypto_price(symbol, exchange, start_date = None):

api_key = 'YOUR_API_KEY'

api_url = f'https://www.alphavantage.co/query?function=DIGITAL_CURRENCY_DAILY&symbol={symbol}&market={exchange}&apikey={api_key}'

raw_df = requests.get(api_url).json()

df = pd.DataFrame(raw_df['Time Series (Digital Currency Daily)']).T

df = df.rename(columns = {'1a. open (USD)': 'Open', '2a. high (USD)': 'High', '3a. low (USD)': 'Low', '4a. close (USD)': 'Close', '5. volume': 'Volume'})

for i in df.columns:

df[i] = df[i].astype(float)

df.index = pd.to_datetime(df.index)

df = df.iloc[::-1].drop(['1b. open (USD)', '2b. high (USD)', '3b. low (USD)', '4b. close (USD)', '6. market cap (USD)'], axis = 1)

if start_date:

df = df[df.index >= start_date]

return df

df = get_crypto_price(symbol = 'BTC', exchange = 'USD', start_date = '2021-01-01')

df.tail()

Open High Low Close Volume

2023-09-09 25910.50 25945.09 25796.64 25901.61 10980.62277

2023-09-10 25901.60 26033.66 25570.57 25841.61 18738.26914

2023-09-11 25841.60 25900.69 24901.00 25162.52 41682.32000

2023-09-12 25162.53 26567.00 25131.48 25840.10 56434.38537

2023-09-13 25840.10 25921.30 25764.17 25906.28 1145.95202- Examining the basic statistics of the input dataset

print(df.info())

print(df.describe())

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 986 entries, 2021-01-01 to 2023-09-13

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Open 986 non-null float64

1 High 986 non-null float64

2 Low 986 non-null float64

3 Close 986 non-null float64

4 Volume 986 non-null float64

dtypes: float64(5)

memory usage: 46.2 KB

None

Open High Low Close Volume

count 986.000000 986.000000 986.000000 986.000000 986.000000

mean 34817.236826 35707.027231 33810.720132 34814.295193 113293.874440

std 13051.431676 13450.720416 12571.628634 13053.326751 112610.375448

min 15781.290000 16315.000000 15476.000000 15781.290000 1145.952020

25% 23471.322500 24033.087500 23020.265000 23471.225000 42121.412306

50% 31242.545000 32192.295000 30177.500000 31242.545000 66665.796138

75% 44565.617500 46163.590000 43160.757500 44565.620000 145398.000907

max 67525.820000 69000.000000 66222.400000 67525.830000 760705.362783- Resetting the index and renaming the time column

df.reset_index(inplace=True)

df.rename(columns={'index': 'Date'}, inplace=True)- Plotting the BTC-USD close price vs Date

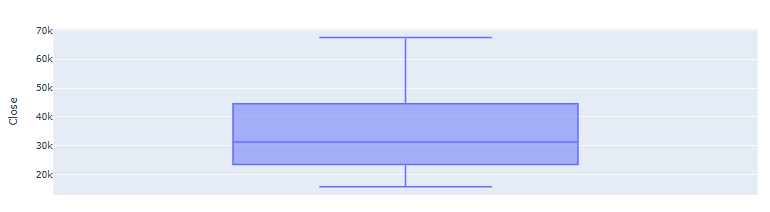

px.area(df, x='Date', y='Close')

px.box(df, y='Close')

Box Cox Data Transformation

- Applying the forward Box Cox transformation to the input data

bc= BoxCox()

df["Close"], lmbda =bc.transform_boxcox(df["Close"])- This is a statistical technique that transforms our target variable so that the transformed data closely resembles a normal distribution. In many statistical techniques, we assume that the errors are normally distributed. This assumption allows us to construct confidence intervals and conduct hypothesis tests implicit in Prophet.

Change of Variables

- The input to Prophet is always a dataframe with two columns:

dsandy. Therefore, we need to change the variables

data= df[["Date", "Close"]]

data.columns=["ds", "y"]- Here, the

ds(date stamp) column should be of a format expected by Pandas, ideally YYYY-MM-DD for a date or YYYY-MM-DD HH:MM:SS for a timestamp. Theycolumn must be numeric, and represents the measurement we wish to forecast (target).

Trend, Multi-Seasonal Decomposition & Forecast

- Creating the Prophet model parameters

## Creating model parameters

model_param ={

"daily_seasonality": False,

"weekly_seasonality":False,

"yearly_seasonality":True,

"seasonality_mode": "multiplicative",

"growth": "logistic"

}- Creating the model and setting a cap or upper limit for the forecast as we are using logistics growth

model = Prophet(**model_param)

data['cap']= data["y"].max() + data["y"].std() * 0.05

# Setting a cap or upper limit for the forecast as we are using logistics growth

# The cap will be maximum value of target variable plus 5% of std.- Fitting the model and making the 1Y forecast in the (ds-y) domain

model.fit(data)

future= model.make_future_dataframe(periods=365)

future['cap'] = data['cap'].max()

forecast= model.predict(future)- Plotting the trend, yearly seasonality, and forecast

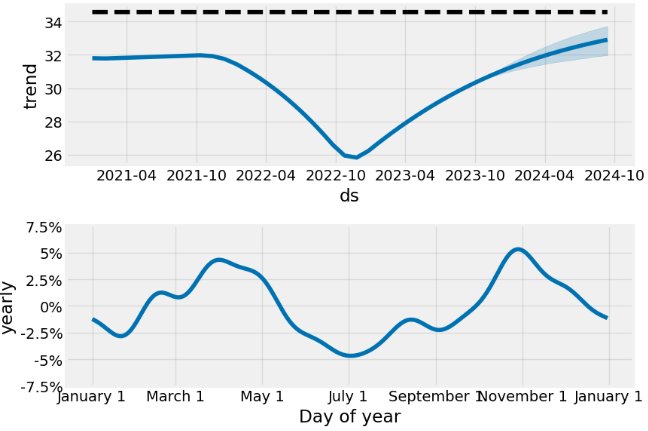

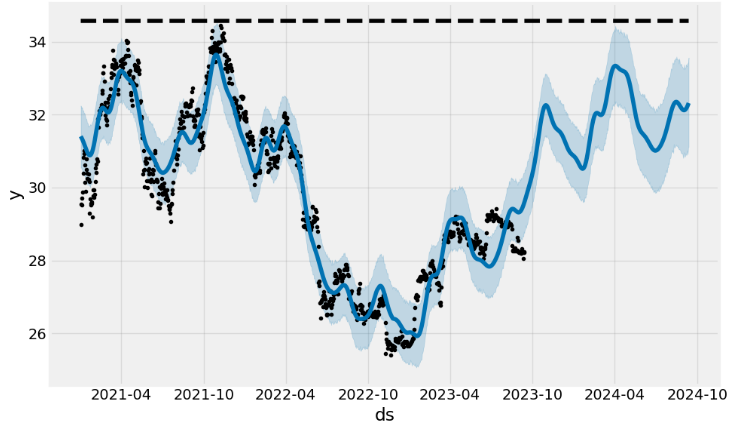

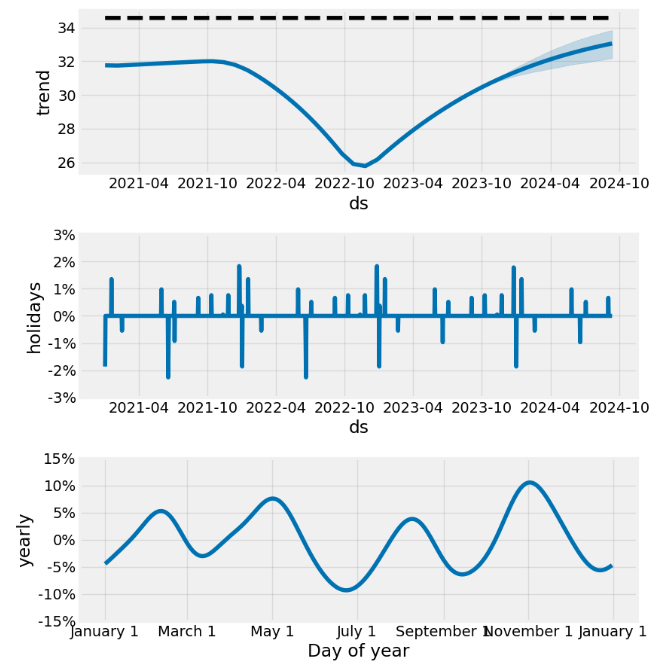

model.plot_components(forecast);

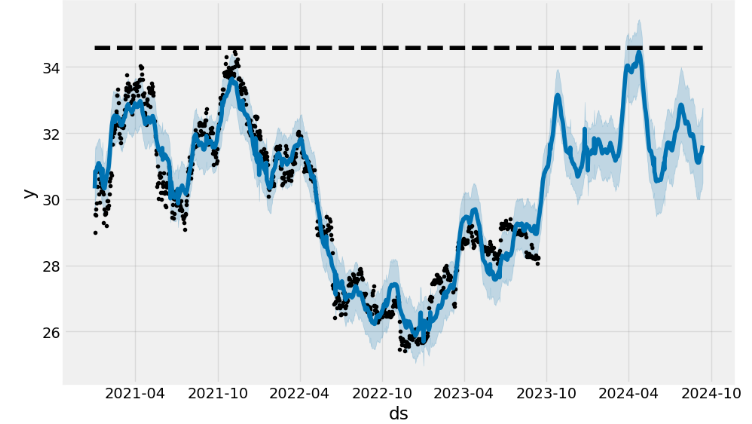

model.plot(forecast);# block dots are actual values and blue dots are forecast

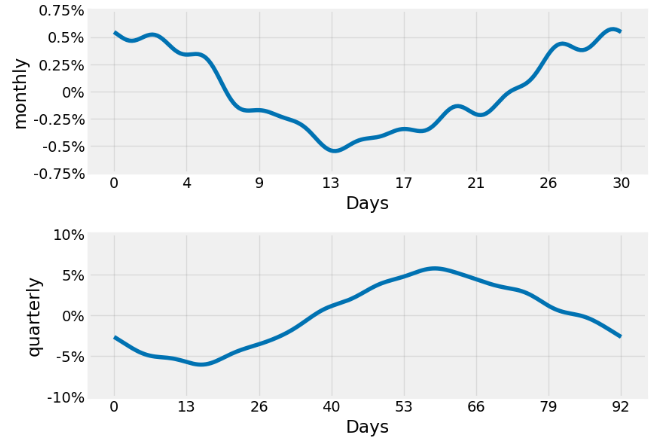

- Adding monthly/quarterly seasonality and US events

model = Prophet(**model_param)

model= model.add_seasonality(name="monthly", period=30, fourier_order=10)

model= model.add_seasonality(name="quarterly", period=92.25, fourier_order=10)

model.add_country_holidays("US")

model.fit(data)

# Create future dataframe

future= model.make_future_dataframe(periods=365)

future['cap'] = data['cap'].max()

forecast= model.predict(future)

model.plot_components(forecast);

model.plot(forecast);

- An interactive figure of the forecast and components can be created with plotly.

- To get uncertainty in seasonality, we must do full Bayesian sampling.

Hyper-Parameter Tuning

- Implementing the hyper-parameter model tuning

## Hyper parameter Tuning

import itertools

import numpy as np

from prophet.diagnostics import cross_validation, performance_metrics

param_grid={

"daily_seasonality": [False],

"weekly_seasonality":[False],

"yearly_seasonality":[True],

"growth": ["logistic"],

'changepoint_prior_scale': [0.001, 0.01, 0.1, 0.5], # to give higher value to prior trend

'seasonality_prior_scale': [0.01, 0.1, 1.0, 10.0] # to control the flexibility of seasonality components

}

# Generate all combination of parameters

all_params= [

dict(zip(param_grid.keys(), v))

for v in itertools.product(*param_grid.values())

]

print(all_params)

[{'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 0.01}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 0.1}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 1.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 10.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.01, 'seasonality_prior_scale': 0.01}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.01, 'seasonality_prior_scale': 0.1}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.01, 'seasonality_prior_scale': 1.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.01, 'seasonality_prior_scale': 10.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.1, 'seasonality_prior_scale': 0.01}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.1, 'seasonality_prior_scale': 0.1}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.1, 'seasonality_prior_scale': 1.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.1, 'seasonality_prior_scale': 10.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.5, 'seasonality_prior_scale': 0.01}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.5, 'seasonality_prior_scale': 0.1}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.5, 'seasonality_prior_scale': 1.0}, {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.5, 'seasonality_prior_scale': 10.0}]- Adding seasonality, US events and finding the best hyper-parameters

rmses= list ()

# go through each combinations

for params in all_params:

m= Prophet(**params)

m= m.add_seasonality(name= 'monthly', period=15, fourier_order=5)

m= m.add_seasonality(name= "quarterly", period= 30, fourier_order= 10)

m.add_country_holidays(country_name="US")

m.fit(data)

df_cv= cross_validation(m, initial="365 days", period="30 days", horizon="365 days")

df_p= performance_metrics(df_cv, rolling_window=1)

rmses.append(df_p['rmse'].values[0])

# find teh best parameters

best_params = all_params[np.argmin(rmses)]

print("\n The best parameters are:", best_params)

The best parameters are: {'daily_seasonality': False, 'weekly_seasonality': False, 'yearly_seasonality': True, 'growth': 'logistic', 'changepoint_prior_scale': 0.001, 'seasonality_prior_scale': 0.1}

forecast.head()

ds trend cap yhat_lower yhat_upper trend_lower trend_upper Christmas Day Christmas Day_lower Christmas Day_upper ... quarterly quarterly_lower quarterly_upper yearly yearly_lower yearly_upper additive_terms additive_terms_lower additive_terms_upper yhat

0 2021-02-04 27.956658 29.941582 27.135661 28.463372 27.956658 27.956658 0.0 0.0 0.0 ... -0.013422 -0.013422 -0.013422 0.008683 0.008683 0.008683 0.0 0.0 0.0 27.830485

1 2021-02-05 27.956395 29.941582 27.249080 28.605843 27.956395 27.956395 0.0 0.0 0.0 ... -0.012904 -0.012904 -0.012904 0.010045 0.010045 0.010045 0.0 0.0 0.0 27.921307

2 2021-02-06 27.956132 29.941582 27.357438 28.666751 27.956132 27.956132 0.0 0.0 0.0 ... -0.012104 -0.012104 -0.012104 0.011362 0.011362 0.011362 0.0 0.0 0.0 27.980221

3 2021-02-07 27.955869 29.941582 27.260377 28.679535 27.955869 27.955869 0.0 0.0 0.0 ... -0.011221 -0.011221 -0.011221 0.012609 0.012609 0.012609 0.0 0.0 0.0 28.036166

4 2021-02-08 27.955606 29.941582 27.461987 28.820484 27.955606 27.955606 0.0 0.0 0.0 ... -0.010445 -0.010445 -0.010445 0.013763 0.013763 0.013763 0.0 0.0 0.0 28.129553

5 rows × 74 columnsInverse Box Cox Transformation

- Applying the inverse Box Cox transformation to the forecast in the (ds-y) domain

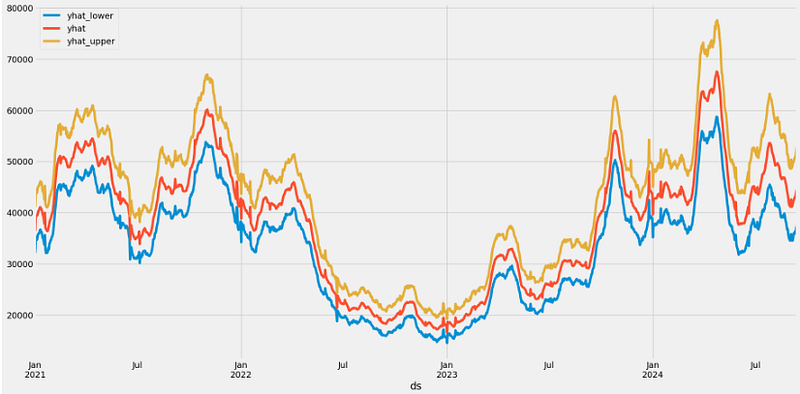

forecast["yhat"]=bc.untransform_boxcox(x=forecast["yhat"], lmbda=lmbda)

forecast["yhat_lower"]=bc.untransform_boxcox(x=forecast["yhat_lower"], lmbda=lmbda)

forecast["yhat_upper"]=bc.untransform_boxcox(x=forecast["yhat_upper"], lmbda=lmbda)

forecast.plot(x="ds", y=["yhat_lower", "yhat", "yhat_upper"])

- By default Prophet returns uncertainty intervals for the forecast

yhat. The biggest source of uncertainty in the forecast is the potential for future trend changes. Here, we assume that the future will see similar trend changes as the history.

Conclusions

- Recently, BTC has gained popularity among investors interested in the possibility of fast returns because it can be exchanged for and used in place of fiat currency.

- In this post, we have addressed the very difficult task of predicting the highly volatile BTC price by invoking the state-of-the-art FB Prophet algorithm. The ultimate goal is to create algo-trading bots that learn to make money trading BTC.

- One of the key advantages of Prophet over other models is its interpretability. Indeed, Prophet has been a key piece to improving Facebook’s ability to create a large number of trustworthy forecasts used for decision-making.

- Generally, our results demonstrate the model’s effectiveness in capturing key trends and multi-seasonal fluctuations of BTC prices while accepting the uncertainties posed by the inherent volatility of the cryptocurrency market.

- Note of caution: (1) if our dataset is noisy and does not follow business cycles, fine-tuning the model’s performance can be problematic; (2) Prophet provides an interpretable model with good performance in a short time; (3) although the model’s decisions are easy to interpret, it’s not precise enough to be used to measure the impact of an external event.

- This Note does support the earlier QC studies.

Explore More

- Stock Forecasting with FBProphet

- S&P 500 Algorithmic Trading with FBProphet

- BTC-USD Freefall vs FB/Meta Prophet 2022–23 Predictions

- BTC-USD Price Prediction with LSTM

- Retail Sales, Store Item Demand Time-Series Analysis/Forecasting: AutoEDA, FB Prophet, SARIMAX & Model Tuning

- Sales Forecasting: tslearn, Random Walk, Holt-Winters, SARIMAX, GARCH, Prophet, and LSTM

- A Balanced Mix-and-Match Time Series Forecasting: ThymeBoost, Prophet, and AutoARIMA

- Time Series Forecasting of Hourly U.S.A. Energy Consumption — PJM East Electricity Grid

- EUR/USD Forecast: Prophet vs JPM

- Joint Analysis of Bitcoin, Gold and Crude Oil Prices

- DOGE-INR Price Prediction Backtesting

- USDTUSD | Tether USD Analysis

References

- Stock Price Prediction Using Facebook Prophet

- Facebook Prophet Documentation & Quick Start

- Box-Cox Transformation and Target Variable: Explained

- Bitcoin-Price-Prediction-using-Facebook-Prophet

- Bitcoin Price Prediction using Facebook Prophet

- Time Series Forecasting Of Bitcoin Prices with Facebook Prophet | Machine Learning

- Forecasting Bitcoin prices using artificial intelligence: Combination of ML, SARIMA, and Facebook Prophet models

- Bitcoin Price Forecasting using FB PROPHET

- Bitcoin Predictive Price Modeling with Facebook’s Prophet