NVDA vs BTC Algorithmic Trading: Backtest BB, MACD & AO Trading Strategies

Comparing NVIDIA vs BTC-USD Historical Returns (Backtesting) using Bollinger Bands (BB), MACD & Awesome Oscillator (AO) Trading Strategies — it It About to Flip?

“Never depend on a single income. Make an investment to create a second source.” — Warren Buffett

- Crypto News July 31, 2024: Since late 2022, NVDA’s stock has become a key indicator for both equity and crypto markets. The correlation between NVDA’s stock and BTC is strong; according to a source, the 3-month correlation between BTC and Nvidia is 0.71. Surprisingly, both hit bottom in late 2022 and have shown similar trends.

- In this post, we will backtest NVDIA and BTC trading strategies: starting from fetching stock data, computing technical indicators, generating trading signals and finally comparing expected returns.

- Firstly, we will compute the Bollinger Bands (BB) [1, 2] to identify the over-sold and over-bought signals of the NVDIA stock since 2022. While every strategy has its drawbacks, BB are among the most useful and commonly used tools in spotlighting extreme short-term security prices. Read more here.

- Secondly, we will download the BTC-USD prices from Kraken’s API and build trading strategies based on the Moving Average Convergence/Divergence (MACD) and the Awesome Oscillator (AO) [3].

- One of the biggest advantages of the MACD is that it’s both a trend and momentum indicator. It is designed to help investors identify price trends, measure trend momentum, and identify acceleration points to fine-tune market entry timing.

- One of the key benefits of using the AO is its simplicity. The AO indicator provides traders with a clear and straightforward way to analyze market trends, as positive values indicate an uptrend and negative values indicate a downtrend.

Business Goals:

- NVDA or BTC — What’s a better investment?

- Given MicroStrategy’s success, what if NVDA were to adopt a similar BTC strategy?

Basic Imports & Settings

- Importing and installing the necessary Python libraries

!pip install requests_html, yfinance, ccxt,ta, quantstats

import pandas as pd

import numpy as np

import yfinance as yf

import yahoo_fin.stock_info as si

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

import ccxt

import ta

import quantstats as qs- V.i. more imports and settings on a as-needed basis.

Reading NVDA Close Price

- Using Yahoo Finance to download the NVDA historical stock data

def load_data(tickers):

data = pd.DataFrame(columns = tickers)

for ticker in tickers:

data[ticker] = yf.download(ticker, start_date)['Close']

return data

tickers = ['NVDA']

start_date = '2020-01-01'

df = load_data(tickers)

df.tail()

NVDA

Date

2024-08-13 116.139999

2024-08-14 118.080002

2024-08-15 122.860001

2024-08-16 124.580002

2024-08-19 130.000000- Plotting the NVDA Close price

fig, ax = plt.subplots(figsize=(12,6))

plt.title(f'Close Price - {tickers[0]}')

plt.ylabel('Price in USD')

plt.xlabel('Dates')

ax.plot(df['NVDA'], label = 'Close Price', alpha = 1., color = 'r')

plt.grid()

Bollinger Bands (BB)

- Introducing the FinTa-style moving average functions EMA and DEMA

def EMA(ohlc,period = 9,column = "NVDA", adjust = True):

"""

Exponential Weighted Moving Average - Like all moving average indicators, they are much better suited for trending markets.

When the market is in a strong and sustained uptrend, the EMA indicator line will also show an uptrend and vice-versa for a down trend.

EMAs are commonly used in conjunction with other indicators to confirm significant market moves and to gauge their validity.

"""

return pd.Series(

ohlc[column].ewm(span=period, adjust=adjust).mean(),

name="{0} period EMA".format(period),

)

def DEMA(ohlc,period = 9,column = "NVDA",adjust = True):

"""

Double Exponential Moving Average - attempts to remove the inherent lag associated to Moving Averages

by placing more weight on recent values. The name suggests this is achieved by applying a double exponential

smoothing which is not the case. The name double comes from the fact that the value of an EMA (Exponential Moving Average) is doubled.

To keep it in line with the actual data and to remove the lag the value 'EMA of EMA' is subtracted from the previously doubled EMA.

Because EMA(EMA) is used in the calculation, DEMA needs 2 * period -1 samples to start producing values in contrast to the period

samples needed by a regular EMA

"""

DEMA = (

2 * EMA(ohlc, period)

- EMA(ohlc, period).ewm(span=period, adjust=adjust).mean()

)

return pd.Series(DEMA, name="{0} period DEMA".format(period))- Computing the Bollinger Bands (BB) [1, 2] in terms of the above two functions

sma=DEMA(df, period=30, column="NVDA",adjust=True).dropna()

rstd = df.rolling(window=30).std().dropna()

upper_band = sma + 2 * rstd['NVDA']

lower_band = sma - 2 * rstd['NVDA']

column_names=["upper"]

upper_band1=pd.DataFrame(upper_band, columns=column_names)

column_names=["lower"]

lower_band1=pd.DataFrame(lower_band, columns=column_names)

df_bollinger_band = df.join(upper_band1).join(lower_band1)

df_bollinger_band = df_bollinger_band.dropna()

df_bollinger_band.tail()

NVDA upper lower

Date

2024-08-13 116.139999 130.763241 90.159861

2024-08-14 118.080002 131.440269 91.046983

2024-08-15 122.860001 132.424561 92.682191

2024-08-16 124.580002 133.754831 94.159677

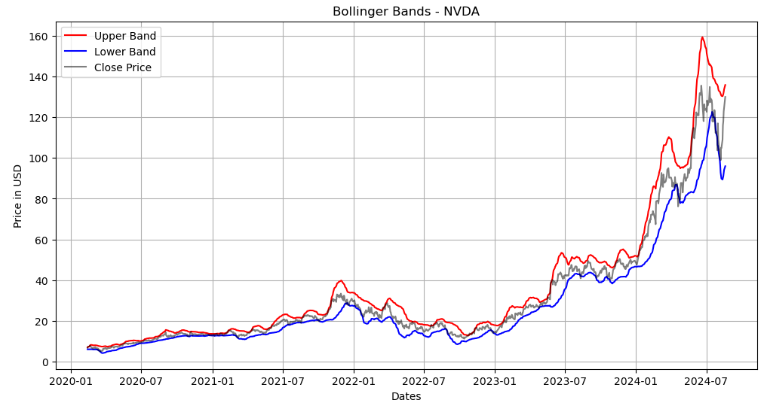

2024-08-19 130.000000 135.858740 95.954941- Plotting the NVDA Close price & upper/lower BB

fig, ax = plt.subplots(figsize=(12,6))

ax.plot(df_bollinger_band['upper'], label = 'Upper Band', alpha = 1,

color = 'red')

ax.plot(df_bollinger_band['lower'], label = 'Lower Band', alpha = 1,

color = 'blue')

plt.title(f'Bollinger Bands - {tickers[0]}')

plt.ylabel('Price in USD')

plt.xlabel('Dates')

ax.plot(df_bollinger_band['NVDA'], label = 'Close Price', alpha = 0.5, color = 'black')

plt.legend(loc='upper left')

plt.grid()

BB Trading Signals

- Implementing the BB trading strategy as follows [1, 2]

buyers = df_bollinger_band[df_bollinger_band['NVDA'] <= df_bollinger_band['lower']]

sellers = df_bollinger_band[df_bollinger_band['NVDA'] >= df_bollinger_band['upper']]

def implement_bb_strategy(data,price='NVDA',upper='upper',lower='lower'):

buy_price = []

sell_price = []

sma_signal = []

signal = 0

for i in range(len(data)):

if data[price].iloc[i] > data[lower].iloc[i]:

if signal != 1:

buy_price.append(data[price].iloc[i])

sell_price.append(np.nan)

signal = 1

sma_signal.append(signal)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

sma_signal.append(0)

elif data[price].iloc[i] < data[upper].iloc[i]:

if signal != -1:

buy_price.append(np.nan)

sell_price.append(data[price].iloc[i])

signal = -1

sma_signal.append(-1)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

sma_signal.append(0)

else:

buy_price.append(np.nan)

sell_price.append(np.nan)

sma_signal.append(0)

return buy_price, sell_price, sma_signal

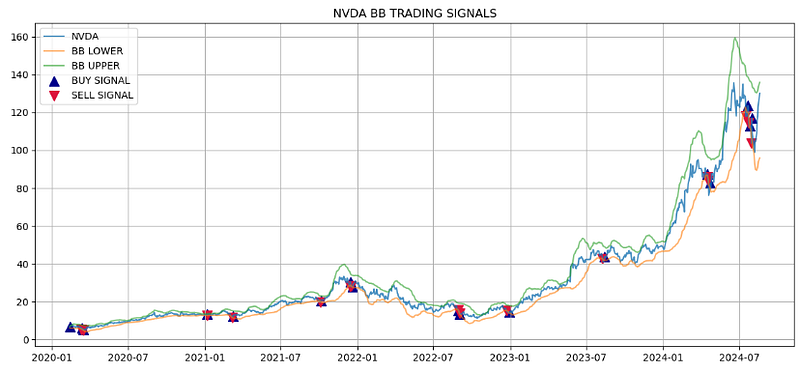

- Plotting the BB strategy output

buy_price, sell_price, signal = implement_bb_strategy(df_bollinger_band)

plt.figure(figsize=(14,6))

plt.plot(df_bollinger_band['NVDA'], alpha = 0.8, label = 'NVDA')

plt.plot(df_bollinger_band['lower'], alpha = 0.6, label = 'BB LOWER')

plt.plot(df_bollinger_band['upper'], alpha = 0.6, label = 'BB UPPER')

plt.scatter(df_bollinger_band.index, buy_price, marker = '^', s = 100, color = 'darkblue', label = 'BUY SIGNAL')

plt.scatter(df_bollinger_band.index, sell_price, marker = 'v', s = 100, color = 'crimson', label = 'SELL SIGNAL')

plt.legend(loc = 'upper left')

plt.grid()

plt.title('NVDA BB TRADING SIGNALS')

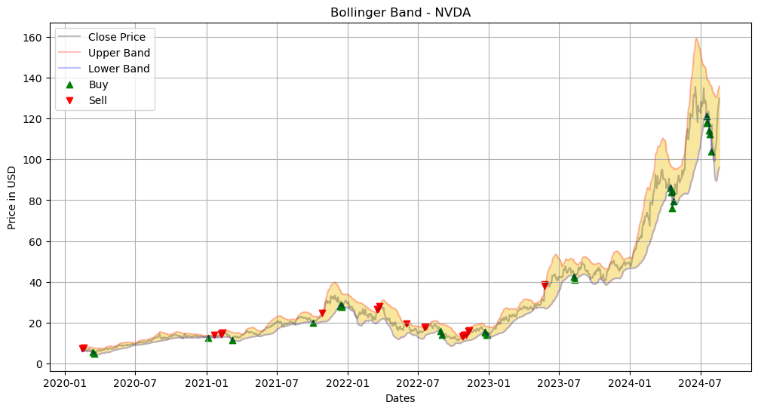

- Plotting the BB buyers & sellers

# Visualizing the Bolling Bands

fig, ax = plt.subplots(figsize=(12,6))

plt.title(f'Bollinger Band - {tickers[0]}')

plt.ylabel('Price in USD')

plt.xlabel('Dates')

ax.plot(df_bollinger_band['NVDA'], label = 'Close Price', alpha = 0.25, color = 'black')

ax.plot(df_bollinger_band['upper'], label = 'Upper Band', alpha = 0.25, color = 'red')

ax.plot(df_bollinger_band['lower'], label = 'Lower Band', alpha = 0.25, color = 'blue')

ax.fill_between(df_bollinger_band.index, df_bollinger_band['upper'], df_bollinger_band['lower'], color = '#F9E79F')

ax.scatter(buyers.index, buyers['NVDA'], label = 'Buy', alpha = 1, marker = '^', color = 'green')

ax.scatter(sellers.index, sellers['NVDA'], label = 'Sell', alpha = 1, marker = 'v', color = 'red')

plt.legend()

plt.grid()

plt.show()

BB Strategy Returns

- Creating the stock position

position = []

for i in range(len(signal)):

if signal[i] > 1:

position.append(0)

else:

position.append(1)

for i in range(len(df_bollinger_band['NVDA'])):

if signal[i] == 1:

position[i] = 1

elif signal[i] == -1:

position[i] = 0

else:

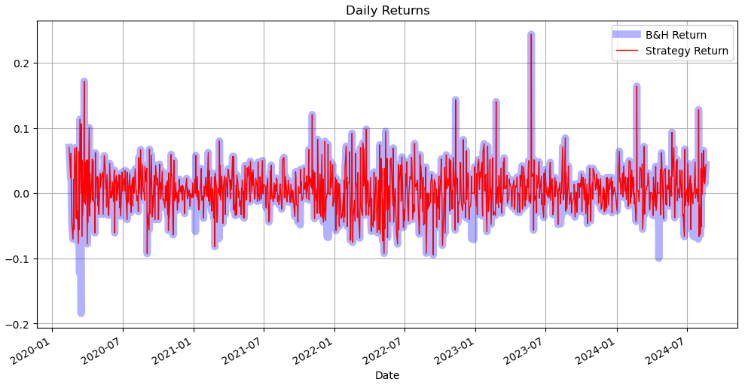

position[i] = position[i-1]- Plotting the NVDA daily returns: BB strategy vs Buy & Hold (B&H)

plt.figure(figsize=(12,6))

rets = df_bollinger_band['NVDA'].pct_change().dropna()

strat_rets = position[1:]*rets

plt.title('Daily Returns')

rets.plot(color = 'blue', alpha = 0.3, linewidth = 7,label='B&H Return')

strat_rets.plot(color = 'r', linewidth = 1,label='Strategy Return')

plt.legend()

plt.grid()

plt.show()

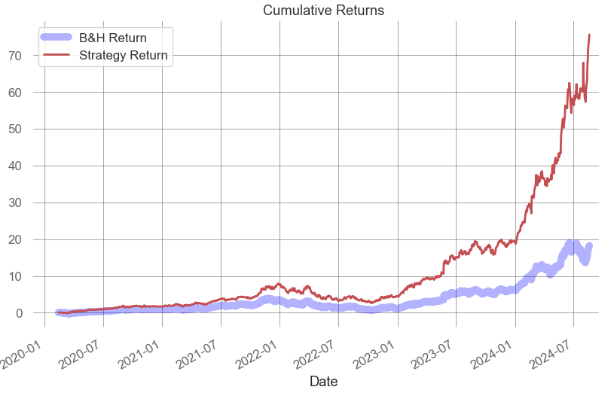

- Plotting the NVDA cumulative returns: BB strategy vs B&H

rets_cum = (1 + rets).cumprod() - 1

strat_cum = (1 + strat_rets).cumprod() - 1

plt.title('Cumulative Returns')

rets_cum.plot(color = 'blue', alpha = 0.3, linewidth = 7,label='B&H Return')

strat_cum.plot(color = 'r', linewidth = 2,label='Strategy Return')

plt.legend()

plt.grid(color='grey')

plt.show()

Reading BTC-USD Close Price

- Using the Kraken API to read the BTC-USD stock historical data [3]

# Kraken API

exchange = ccxt.kraken()

# We define the symbol and timeframe

symbol = 'BTC/USD'

timeframe = '1d'

# We fetch OHLCV data

ohlcv = exchange.fetch_ohlcv(symbol, timeframe)

# We first convert to DataFrame then to Timestamp for a more readable format

df = pd.DataFrame(ohlcv, columns=['Timestamp', 'Open', 'High', 'Low', 'Close', 'Volume'])

df['Timestamp'] = pd.to_datetime(df['Timestamp'], unit='ms')

df.set_index('Timestamp', inplace=True)

# We now have our DataFrame

df

Open High Low Close Volume

Timestamp

2022-09-01 20049.4 20195.0 19560.0 20127.8 2829.586687

2022-09-02 20127.8 20434.9 19764.3 19954.6 3594.858626

2022-09-03 19954.0 20047.4 19655.6 19834.9 1409.931849

2022-09-04 19833.3 20010.0 19601.0 19995.8 1308.952671

2022-09-05 20000.0 20045.0 19642.9 19790.5 2418.522014

... ... ... ... ... ...

2024-08-16 57555.0 59800.0 57100.9 58898.4 1659.798395

2024-08-17 58895.6 59682.2 58812.4 59473.3 456.341715

2024-08-18 59473.4 60234.4 58451.6 58466.5 812.959316

2024-08-19 58466.5 59593.0 57860.8 59493.7 1313.020804

2024-08-20 59493.7 61391.9 59402.0 60682.2 952.381669

720 rows × 5 columnsMACD & AO Indicators

- Calculating the MACD Line, Signal Line and Histogram [3]

# Calculate MACD Line, Signal Line and MACD Histogram

macd = ta.trend.MACD(df['Close'])

df['macd_line'] = macd.macd() # MACD Line

df['macd_signal'] = macd.macd_signal() # Signal Line

df['macd_hist'] = macd.macd_diff() # MACD Histogram (MACD Line - Signal Line)- Calculating the Awesome Oscillator (AO)

# Calculate MACD Line, Signal Line and MACD Histogram

macd = ta.trend.MACD(df['Close'])

df['macd_line'] = macd.macd() # MACD Line

df['macd_signal'] = macd.macd_signal() # Signal Line

df['macd_hist'] = macd.macd_diff() # MACD Histogram (MACD Line - Signal Line)

# Calculate Awesome Oscillator

ao = ta.momentum.AwesomeOscillatorIndicator(df['High'], df['Low'])

df['ao'] = ao.awesome_oscillator() # Awesome Oscillator

df

Open High Low Close Volume macd_line macd_signal macd_hist ao

Timestamp

2022-09-01 20049.4 20195.0 19560.0 20127.8 2829.586687 NaN NaN NaN NaN

2022-09-02 20127.8 20434.9 19764.3 19954.6 3594.858626 NaN NaN NaN NaN

2022-09-03 19954.0 20047.4 19655.6 19834.9 1409.931849 NaN NaN NaN NaN

2022-09-04 19833.3 20010.0 19601.0 19995.8 1308.952671 NaN NaN NaN NaN

2022-09-05 20000.0 20045.0 19642.9 19790.5 2418.522014 NaN NaN NaN NaN

... ... ... ... ... ... ... ... ... ...

2024-08-16 57555.0 59800.0 57100.9 58898.4 1659.798395 -1269.449533 -1161.663033 -107.786500 -3568.995588

2024-08-17 58895.6 59682.2 58812.4 59473.3 456.341715 -1177.388338 -1164.808094 -12.580244 -3523.468235

2024-08-18 59473.4 60234.4 58451.6 58466.5 812.959316 -1172.157619 -1166.277999 -5.879620 -3552.745588

2024-08-19 58466.5 59593.0 57860.8 59493.7 1313.020804 -1072.759676 -1147.574334 74.814659 -3681.345294

2024-08-20 59493.7 61391.9 59402.0 60682.2 952.381669 -887.849496 -1095.629367 207.779871 -3067.566765

720 rows × 9 columns- Dropping the NaN values

# Drop NaN values

df.dropna(inplace=True)

df.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 687 entries, 2022-10-04 to 2024-08-20

Data columns (total 9 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Open 687 non-null float64

1 High 687 non-null float64

2 Low 687 non-null float64

3 Close 687 non-null float64

4 Volume 687 non-null float64

5 macd_line 687 non-null float64

6 macd_signal 687 non-null float64

7 macd_hist 687 non-null float64

8 ao 687 non-null float64

dtypes: float64(9)

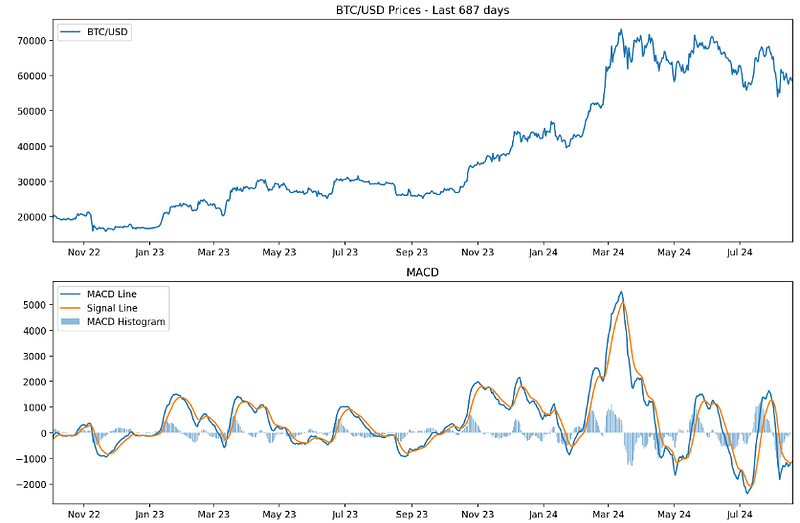

memory usage: 53.7 KB- Plotting the BTC-USD Close price, the MACD and AO indicators

fig, ax = plt.subplots(3, figsize=(12,12), dpi=200)

# Plot BTC prices

ax[0].plot(df.index, df['Close'], label='BTC/USD')

ax[0].set_title('BTC/USD Prices - Last 687 days')

ax[0].legend(loc='upper left')

ax[0].set_xlim([df.index.min(), df.index.max()])

#ax[0].grid()

# Plot MACD Line, Signal Line and Histogram

ax[1].plot(df.index, df['macd_line'], label='MACD Line') # Plot MACD Line and Signal Line

ax[1].plot(df.index, df['macd_signal'], label='Signal Line') # Plot MACD Line and Signal Line

ax[1].bar(df.index, df['macd_hist'], alpha=0.5, label='MACD Histogram') # Plot MACD Histogram as bar plot

ax[1].set_title('MACD')

ax[1].legend(loc='upper left')

ax[1].set_xlim([df.index.min(), df.index.max()])

#ax[1].grid()

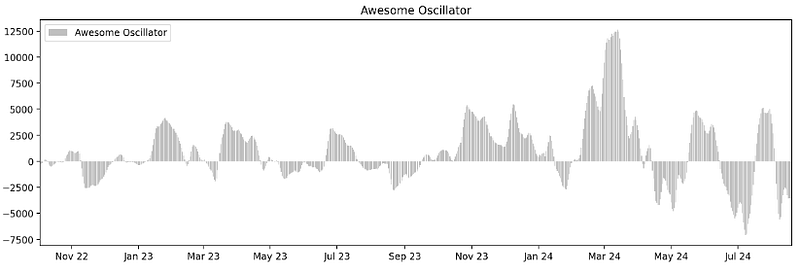

# Plot Awesome Oscillator

ax[2].bar(df.index, df['ao'], alpha=0.5, label='Awesome Oscillator', color='gray')

ax[2].set_title('Awesome Oscillator')

ax[2].legend(loc='upper left')

ax[2].set_xlim([df.index.min(), df.index.max()])

#ax[2].grid()

# Set date format

date_format = mdates.DateFormatter('%b %y')

ax[0].xaxis.set_major_formatter(date_format)

ax[1].xaxis.set_major_formatter(date_format)

ax[2].xaxis.set_major_formatter(date_format)

# Show the plot

plt.tight_layout()

plt.show()

MACD/AO Trading Signals

- Generating the buy/sell trading signals [3]

# Strategy 1

# Generating the buy "signal1"

df['signal1'] = np.where((df['macd_line'] > df['macd_signal']) & (df['ao'] > 0), 1, 0)

# Generating the "sell_signal1"

df['sell_signal1'] = np.where((df['macd_line'] < df['macd_signal']) & (df['ao'] < 0), 1, 0)

# Strategy 2

# Generating the buy "signal2"

df['signal2'] = np.where((df['macd_line'] > df['macd_signal']) & (df['macd_line'].shift() < df['macd_signal'].shift()) & (df['ao'] > 0) & (df['ao'].shift() < 0), 1, 0)

# Generating the "sell_signal2"

df['sell_signal2'] = np.where((df['macd_line'] < df['macd_signal']) & (df['macd_line'].shift() > df['macd_signal'].shift()) & (df['ao'] < 0) & (df['ao'].shift() > 0), 1, 0)

# Counting the buy/sell signals

num_signals1 = df['signal1'].sum()

num_sells1 = df['sell_signal1'].sum()

num_signals2 = df['signal2'].sum()

num_sells2 = df['sell_signal2'].sum()

print(f"Number of buy signals in Strategy 1: {num_signals1}")

print(f"Number of sell signals in Strategy 1: {num_sells1}")

print(f"Number of buy signals in Strategy 2: {num_signals2}")

print(f"Number of sell signals in Strategy 2: {num_sells2}")

Number of buy signals in Strategy 1: 225

Number of sell signals in Strategy 1: 198

Number of buy signals in Strategy 2: 1

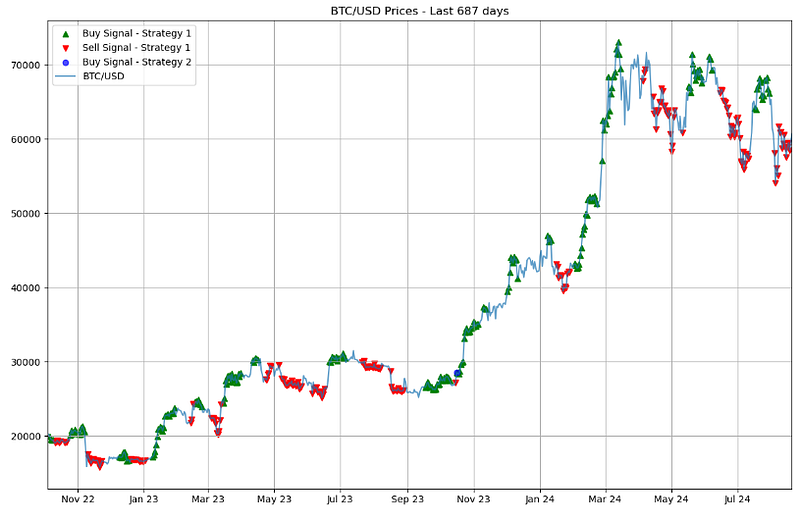

Number of sell signals in Strategy 2: 0- Plotting the buy/sell trading signals of Strategy 1 and a single buy signal of Strategy 2 to be neglected

fig, ax = plt.subplots(4, figsize=(12, 30))

# Plot ETH prices

ax[0].scatter(df[df['signal1'] == 1].index, df[df['signal1'] == 1]['Close'], color='g', marker='^', label='Buy Signal - Strategy 1')

ax[0].scatter(df[df['sell_signal1'] == 1].index, df[df['sell_signal1'] == 1]['Close'], color='r', marker='v', label='Sell Signal - Strategy 1')

ax[0].scatter(df[df['signal2'] == 1].index, df[df['signal2'] == 1]['Close'], color='b', marker='o', label='Buy Signal - Strategy 2', alpha=0.7)

#ax[0].scatter(df[df['sell_signal2'] == 1].index, df[df['sell_signal2'] == 1]['Close'], s=100,color='orange', marker='x', label='Sell Signal - Strategy 2', alpha=0.7)

ax[0].plot(df.index, df['Close'], label='BTC/USD',alpha=0.7)

ax[0].set_title('BTC/USD Prices - Last 687 days')

ax[0].legend()

ax[0].set_xlim([df.index.min(), df.index.max()])

ax[0].grid()

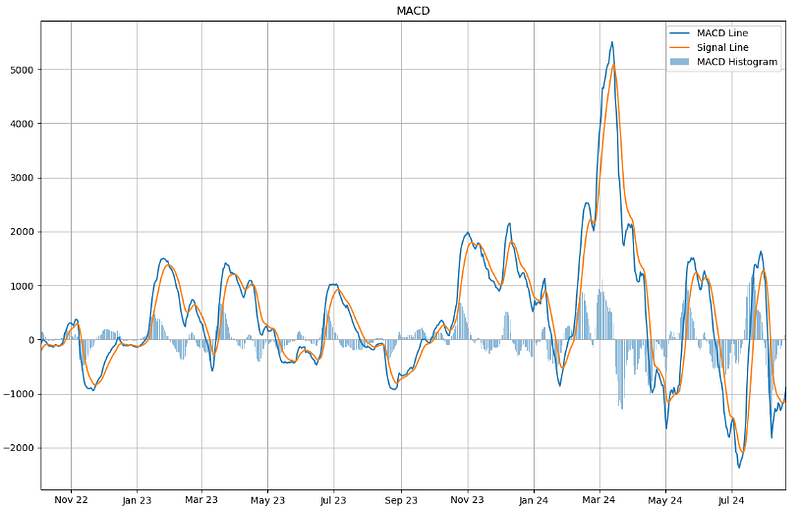

# Plot MACD Line, Signal Line and Histogram

ax[1].plot(df.index, df['macd_line'], label='MACD Line')

ax[1].plot(df.index, df['macd_signal'], label='Signal Line')

ax[1].bar(df.index, df['macd_hist'], alpha=0.5, label='MACD Histogram')

ax[1].set_title('MACD')

ax[1].legend()

ax[1].set_xlim([df.index.min(), df.index.max()])

ax[1].grid()

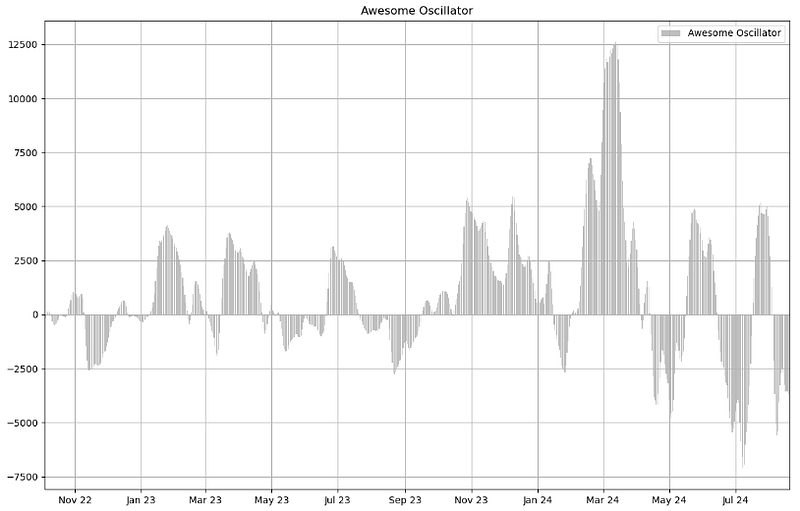

# Plot Awesome Oscillator

ax[2].bar(df.index, df['ao'], alpha=0.5, label='Awesome Oscillator', color='gray')

ax[2].set_title('Awesome Oscillator')

ax[2].legend()

ax[2].set_xlim([df.index.min(), df.index.max()])

ax[2].grid()

# Let's also set the appropriate date format

date_format = mdates.DateFormatter('%b %y')

for a in ax:

a.xaxis.set_major_formatter(date_format)

# Plot

plt.tight_layout()

plt.show()

- Plotting the MACD and AO indicators for the sake of comparison

MACD/AO Strategy Backtesting

- Using quantstats to backtest Strategy 1 [3]

# We calculate the daily returns

df['returns'] = df['Close'].pct_change()

# Strategy 1 returns

df['strategy1_returns'] = df['returns'] * df['signal1'].shift()

df['strategy1_cum_returns'] = (1 + df['strategy1_returns']).cumprod()

# Drop the NaN values

df.dropna(inplace=True)

# Let's print the report for Strategy 1

print("Strategy 1:")

qs.reports.full(df['strategy1_returns'])

Strategy 1:

Performance Metrics

Strategy

------------------------- ----------

Start Period 2022-10-04

End Period 2024-08-19

Risk-Free Rate 0.0%

Time in Market 33.0%

Cumulative Return 89.3%

CAGR﹪ 26.46%

Sharpe 1.12

Prob. Sharpe Ratio 97.23%

Smart Sharpe 1.09

Sortino 1.92

Smart Sortino 1.87

Sortino/√2 1.36

Smart Sortino/√2 1.32

Omega 1.44

Max Drawdown -16.44%

Longest DD Days 159

Volatility (ann.) 23.42%

Calmar 1.61

Skew 1.38

Kurtosis 17.17

Expected Daily % 0.09%

Expected Monthly % 2.81%

Expected Yearly % 23.7%

Kelly Criterion 14.96%

Risk of Ruin 0.0%

Daily Value-at-Risk -2.32%

Expected Shortfall (cVaR) -2.32%

Max Consecutive Wins 8

Max Consecutive Losses 4

Gain/Pain Ratio 0.44

Gain/Pain (1M) 1.87

Payoff Ratio 1.51

Profit Factor 1.44

Common Sense Ratio 2.01

CPC Index 1.06

Tail Ratio 1.4

Outlier Win Ratio 12.87

Outlier Loss Ratio 2.31

MTD 0.0%

3M 0.36%

6M 11.42%

YTD 22.56%

1Y 56.6%

3Y (ann.) 26.46%

5Y (ann.) 26.46%

10Y (ann.) 26.46%

All-time (ann.) 26.46%

Best Day 10.33%

Worst Day -9.97%

Best Month 32.9%

Worst Month -9.54%

Best Year 81.81%

Worst Year -15.05%

Avg. Drawdown -3.72%

Avg. Drawdown Days 22

Recovery Factor 4.33

Ulcer Index 0.08

Serenity Index 0.94

Avg. Up Month 11.44%

Avg. Down Month -4.27%

Win Days % 48.89%

Win Month % 52.63%

Win Quarter % 50.0%

Win Year % 66.67%

None

Worst 5 Drawdowns

Start Valley End Days Max Drawdown 99% Max Drawdown

1 2022-11-06 2022-12-19 2023-01-13 69 -16.444587 -15.474868

2 2023-12-09 2024-02-04 2024-02-13 67 -15.678754 -15.562739

3 2024-03-14 2024-05-19 2024-08-19 159 -11.757961 -11.278155

4 2023-01-30 2023-02-24 2023-03-16 46 -9.249899 -6.713859

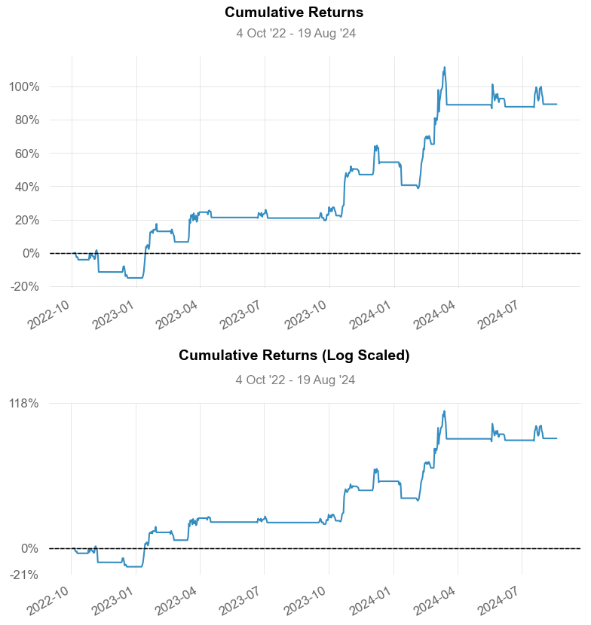

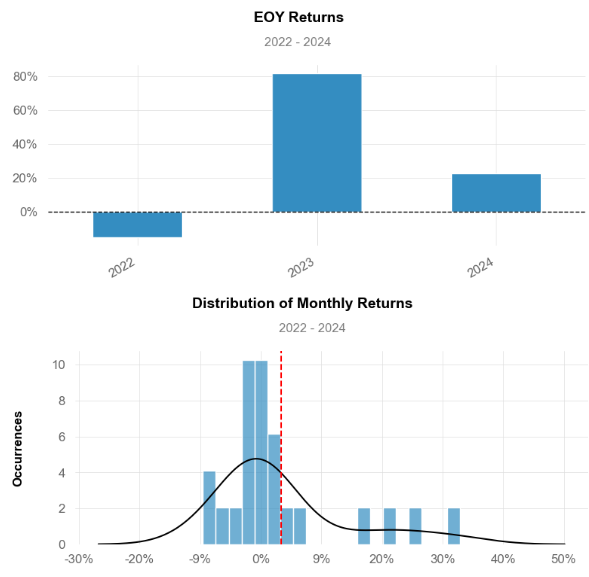

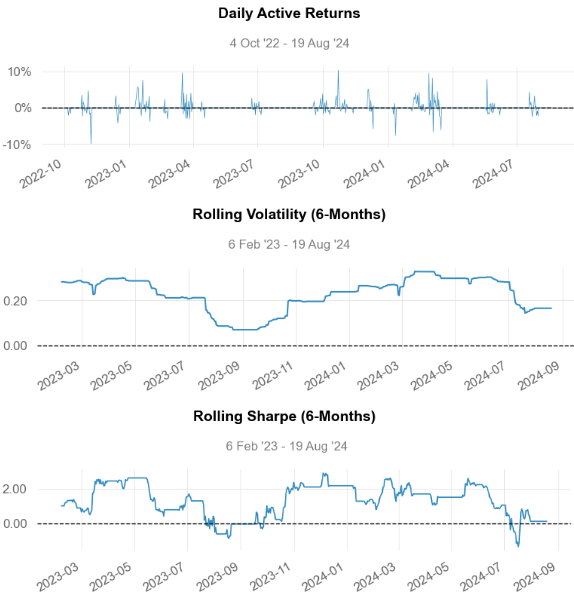

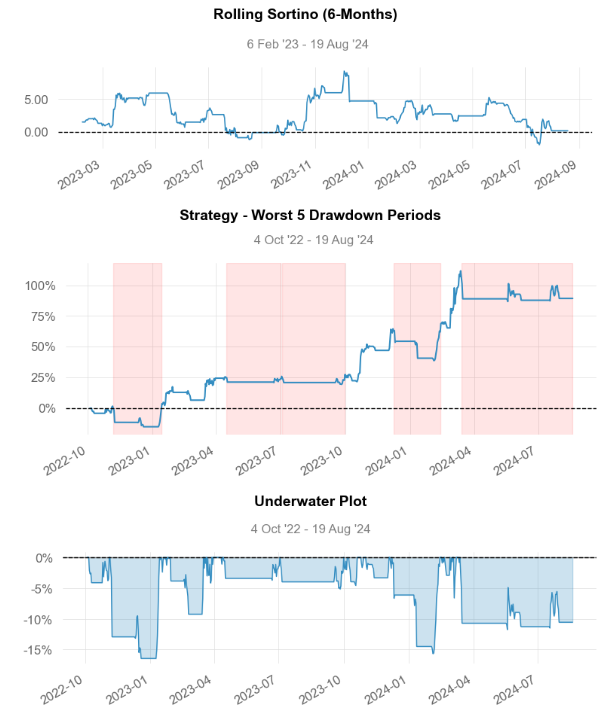

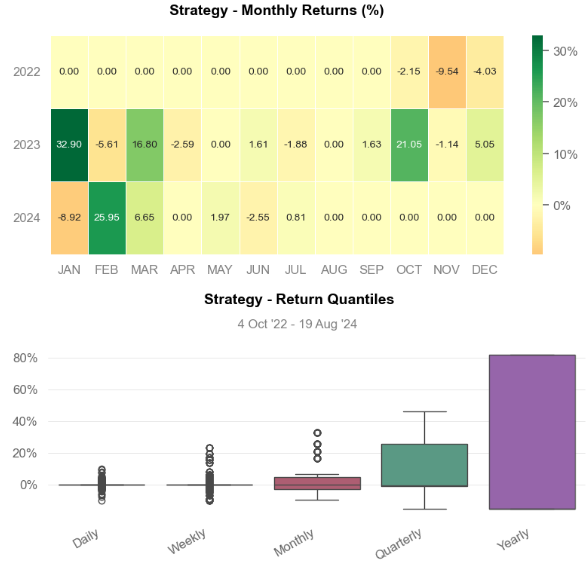

5 2024-03-05 2024-03-05 2024-03-07 3 -6.616796 -3.255414- Strategy 1 Visualization

Conclusions

- NVDA 4Y BB Strategy [1, 2] Cumulative Return is ~ 75% as compared to B&H Return of 20%.

- BTC-USD 2Y MACD-based Strategy [3] Cumulative Return is ~ 89%, CAGR ~ 26%, Volatility (ann.) is 23.42%, the Kelly Criterion is 14.96%, CVaR is -2.32%, Sortino is 1.92 and Sharpe is 1.12.

- Results indicate that NVDA will have no choice but to adopt BTC and integrate “digital gold” into its business processes as a valuable hedge against inflation.

- Bottom Line: Holding NVDA stock and BTC together in a portfolio can reduce certain risks compared to keeping just one of them.

References

- How To Build Basic Trading Strategy Using Python

- Financial Analysis/Bollinger_Bands.py

- The A-Z of Coding a Trading Strategy. A Python Series

Explore More

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- Joint Analysis of Bitcoin, Gold and Crude Oil Prices

- Real-Time Stock Sentiment Analysis w/ NLP Web Scraping

- A Market-Neutral Strategy

- NVIDIA Rolling Volatility: GARCH & XGBoost

- Dividend-NG-BTC Diversify Big Tech

- NVIDIA Short-Term Stock Price Forecasting: SHAP Explainer, Lags, Optimized ML Regressors, Auto-ARIMA, Multi-Seasonal FB Prophet Tuning & LSTM

- BTC-USD Price Prediction using FB Prophet with Hyperparameter Optimization, Cross-Validation QC & Modified Algo-Trading Strategies

- NVDA Technical Analysis using 75 Simplified FinTA Indicators

- Semi-Automated Detection of BTC-USD Price Support & Resistance Levels: Comparing 15 Essential Methods

- Resolving Bias-Variance Tradeoff in BTC-USD Price Prediction: Incorporating Technical Indicators into XGBoost Regression with Optuna Hyperparameter Optimization

- Max Sharpe Portfolio of Top 10 Cryptos with Risk-Adjusted Weights

- Backtesting Hull Moving Average (HMA) Algo-Trading: NVDA Price vs Volume Buy/Sell Signals & Expected Returns

- 2Y Big Techs Portfolio Diversification, Risk-Return Tradeoff and LSTM Price Prediction: AAPL, NVDA, META & AMZN

- Risk-Adjusted BTC-Gold-Oil- EURUSD Portfolio Optimization for Quant Traders: AutoEDA, Scipy SLSQP, Markowitz, Sharpe & VAR

Contacts

Disclaimer

- The following disclaimer clarifies that the information provided in this article is for educational use only and should not be considered financial or investment advice.

- The information provided does not take into account your individual financial situation, objectives, or risk tolerance.

- Any investment decisions or actions you undertake are solely your responsibility.

- You should independently evaluate the suitability of any investment based on your financial objectives, risk tolerance, and investment timeframe.

- It is recommended to seek advice from a certified financial professional who can provide personalized guidance tailored to your specific needs.

- The tools, data, content, and information offered are impersonal and not customized to meet the investment needs of any individual. As such, the tools, data, content, and information are provided solely for informational and educational purposes only.