Backtesting Hull Moving Average (HMA) Algo-Trading: NVDA Price vs Volume Buy/Sell Signals & Expected Returns

- The objective of this post is to effectively backtest two Nvidia (NASDAQ: NVDA) algo-trading strategies based on the Hull Moving Average (HMA) trading indicator.

- According to Zacks, NVDA is a top growth stock for the long-term. NVDA is a #2 (Buy) on the Zacks Rank, with a VGM Score of B. NVDA has a Growth Style Score of A, forecasting year-over-year earnings growth of 84.7% for the current fiscal year. With a solid Zacks Rank and top-tier Growth and VGM Style Scores, NVDA should be on investors’ short list.

- Our current goal is to compare expected returns generated by HMA NVDA historical price vs volume crossover signals, being referred to as Strategies A and B, respectively.

- While many traders focus solely on trading strategies that utilize price data only (Strategy A), we will delve into the importance of volume analysis and explore how Strategy B can provide insights into potential market trends and strength.

Price-Volume HMA Crossover Strategies

- Conventionally, the HMA crossover strategy involves using two different HMA timeframes, a shorter period and a longer period, to generate trading signals when they cross each other.

- The key idea is to generate buy and sell signals based on the interaction between the two HMA lines. As with other moving average indicators, when the price/volume crosses above the HMA line from below, it is considered a buy signal. Conversely, when the price/volume crosses below the HMA line from above, it is a sell signal.

- Generally, the HMA strategy reduces noise in the data and provides clearer buy or sell signals when used alongside other technical indicators like oscillators or trend lines.

- Unlike other moving averages that rely solely on closing prices, Strategy A takes into account high and low prices as well. This additional information helps smooth out volatility and provides a more comprehensive view of market dynamics.

- In the proposed technical analysis, Strategies A and B are combined specifically to support investors that incorporate price-volume relationships into their trading decisions.

Let’s explore nuts & bolts of the HMA algo-trading strategies, covering everything from their implementation in Python to backtesting NVDA HMA price vs volume entry/exit positions and expected cumulative returns of Strategies A and B.

Downloading Stock Data

- Importing libraries and reading the NVDA historical stock data 2022–2024

import datetime as dt

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

plt.style.use('fivethirtyeight')

plt.rcParams['figure.figsize'] = (20,10)

def download_stock_data(ticker,timestamp_start,timestamp_end):

url=f"https://query1.finance.yahoo.com/v7/finance/download/{ticker}?period1={timestamp_start}&period2={timestamp_end}&interval\

=1d&events=history&includeAdjustedClose=true"

df = pd.read_csv(url)

return df

datetime_start=dt.datetime(2022, 1, 1, 7, 35, 51)

datetime_end=dt.datetime.today()

# Convert to timestamp:

timestamp_start=int(datetime_start.timestamp())

timestamp_end=int(datetime_end.timestamp())

ticker='NVDA'

df = download_stock_data(ticker,timestamp_start,timestamp_end)

df = df.set_index('Date')

df.tail()

Open High Low Close Adj Close Volume

Date

2024-05-13 904.780029 909.979980 885.289978 903.989990 903.989990 28968000

2024-05-14 895.989990 916.510010 889.340027 913.559998 913.559998 29650700

2024-05-15 924.719971 948.619995 915.989990 946.299988 946.299988 41773500

2024-05-16 949.099976 958.190002 941.030029 943.590027 943.590027 32395200

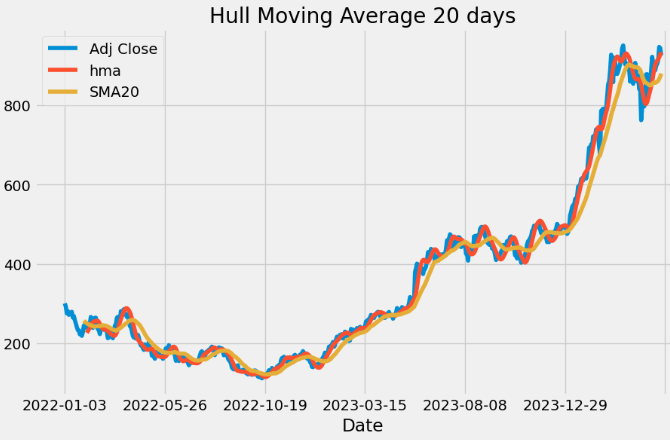

2024-05-17 943.690002 947.400024 918.059998 924.789978 924.789978 34651900Plotting SMA20 vs HMA20

- Calculating and plotting 20-day HMA vs SMA for Adj Close price

def hma(period):

wma_1 = df['Adj Close'].rolling(period//2).apply(lambda x: \

np.sum(x * np.arange(1, period//2+1)) / np.sum(np.arange(1, period//2+1)), raw=True)

wma_2 = df['Adj Close'].rolling(period).apply(lambda x: \

np.sum(x * np.arange(1, period+1)) / np.sum(np.arange(1, period+1)), raw=True)

diff = 2 * wma_1 - wma_2

hma = diff.rolling(int(np.sqrt(period))).mean()

return hma

period = 20

df['hma'] = hma(period)

df['SMA20'] = df['Adj Close'].rolling(period).mean()

figsize = (10,6)

df[['Adj Close','hma','SMA20']].plot(figsize=figsize)

plt.title('Hull Moving Average {0} days'.format(period))

plt.show()

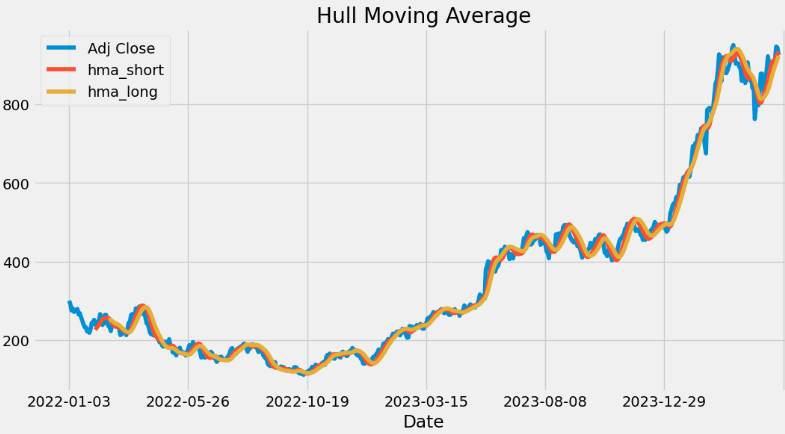

Plotting HMA Short/Long Lines

- Calculating and plotting short (20-day) and long (30-day) HMA lines

df['hma_short']=hma(20)

df['hma_long']=hma(30)

figsize = (12,6)

df[['Adj Close','hma_short','hma_long']].plot(figsize=figsize)

plt.title('Hull Moving Average')

plt.show()

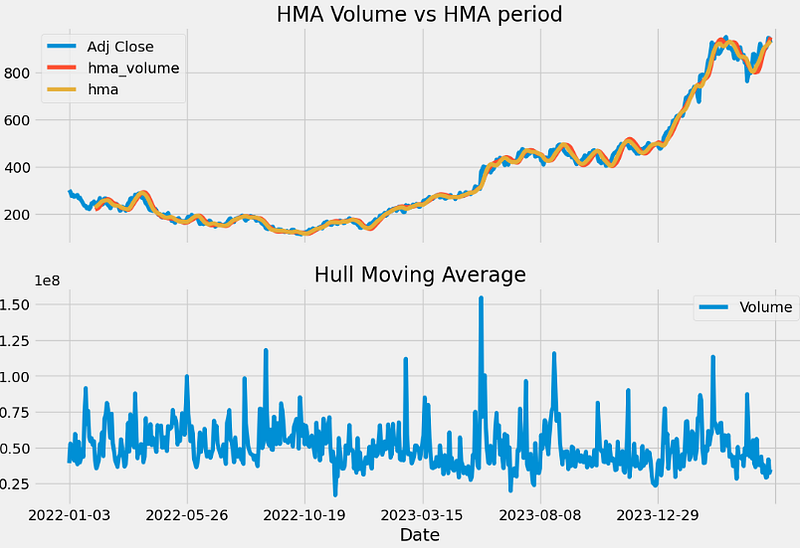

Comparing HMA Volume vs Period

- Invoking the volume to calculate the weighted average

def hma_volume(period):

wma_1 = df['nominal'].rolling(period//2).sum()/df['Volume'].rolling(period//2).sum()

wma_2 = df['nominal'].rolling(period).sum()/df['Volume'].rolling(period).sum()

diff = 2 * wma_1 - wma_2

hma = diff.rolling(int(np.sqrt(period))).mean()

return hma

df['nominal'] = df['Adj Close'] * df['Volume']

period = 20

df['hma_volume']=hma_volume(period)

figsize=(12,8)

fig, (ax0,ax1) = plt.subplots(nrows=2, sharex=True, subplot_kw=dict(frameon=True),figsize=figsize)

df[['Adj Close','hma_volume','hma']].plot(ax=ax0)

ax0.set_title('HMA Volume vs HMA period')

df[['Volume']].plot(ax=ax1)

ax1.set_title('Hull Moving Average')

plt.show()

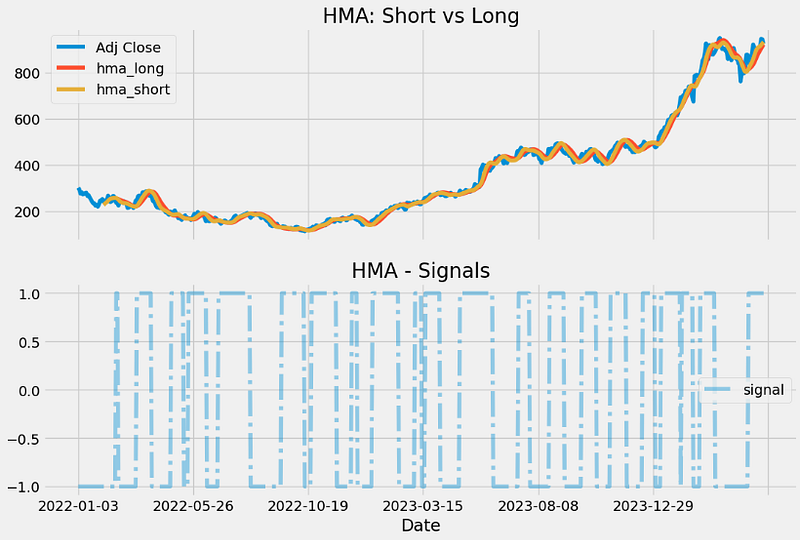

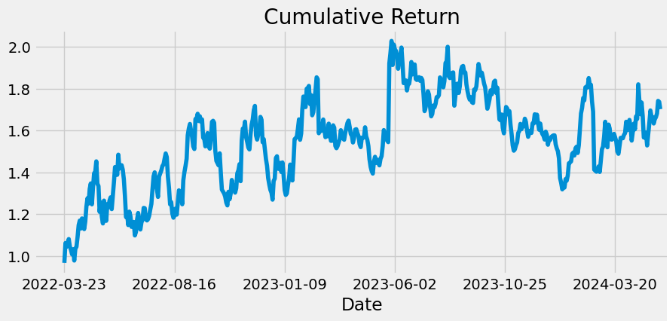

Backtesting Strategy A

- Calculating trading signals and cumulative returns (CR) of Strategy A

#SIGNAL

df['hma_short']=hma(20)

df['hma_long']=hma(30)

df['signal'] = np.where(df['hma_short'] > df['hma_long'],1,-1)

#RETURN

df['signal_shifted']=df['signal'].shift()

## Calculate the returns on the days we trigger a signal

df['returns'] = df['Adj Close'].pct_change()

## Calculate the strategy returns

df['strategy_returns'] = df['signal_shifted'] * df['returns']

## Calculate the cumulative returns

df1=df.dropna()

df1['cumulative_returns'] = (1 + df1['strategy_returns']).cumprod()

#PLOT

figsize=(12,8)

fig, (ax0,ax1) = plt.subplots(nrows=2, sharex=True, subplot_kw=dict(frameon=True),figsize=figsize)

df[['Adj Close','hma_long','hma_short']].plot(ax=ax0)

ax0.set_title("HMA: Short vs Long")

df[['signal']].plot(ax=ax1,style='-.',alpha=0.4)

ax1.legend()

ax1.set_title("HMA - Signals")

plt.show()

df1['cumulative_returns'].plot(figsize=(10,4))

plt.title("Cumulative Return")

plt.show()

- Printing the latest value of CR

df1['cumulative_returns'].tail()[-1]

1.7016343263088096Backtesting Strategy B

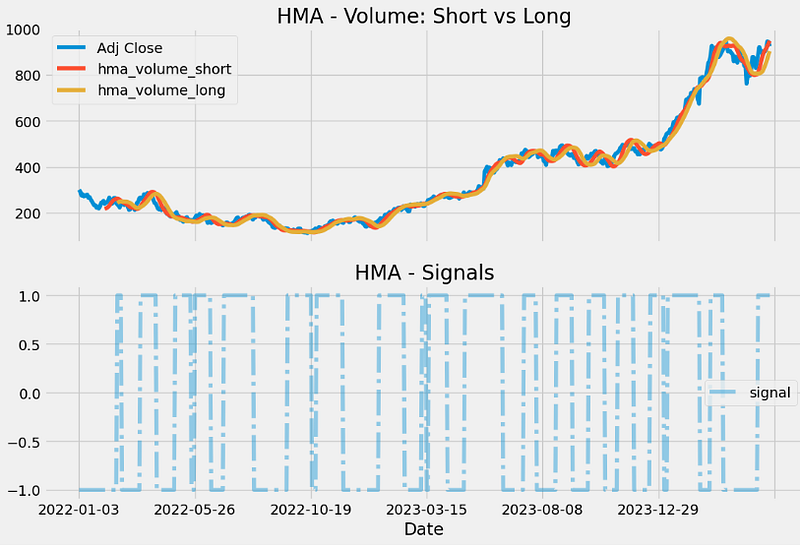

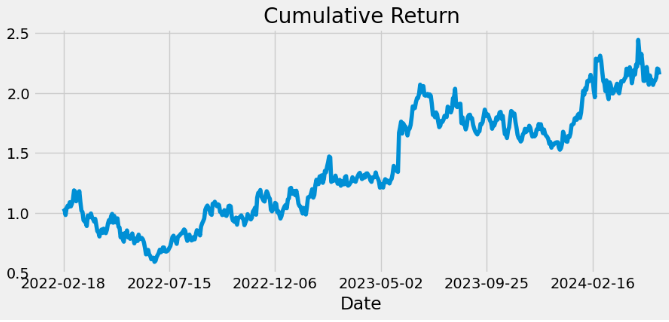

- Calculating trading signals and cumulative returns (CR) of Strategy B

#SIGNAL

df['hma_volume_short']=hma_volume(20)

df['hma_volume_long']=hma_volume(30)

df['signal'] = np.where(df['hma_volume_short'] > df['hma_volume_long'],1,-1)

#RETURN

df['returns'] = df['Adj Close'].pct_change()

## Calculate the strategy returns

df['strategy_returns'] = df['signal'].shift() * df['returns']

## Calculate the cumulative returns

df2=df.dropna()

df2['cumulative_returns_volume'] = (1 + df2['strategy_returns']).cumprod()

# PLOT

figsize=(12,8)

fig, (ax0,ax1) = plt.subplots(nrows=2, sharex=True, subplot_kw=dict(frameon=True),figsize=figsize)

df[['Adj Close','hma_volume_short','hma_volume_long']].plot(ax=ax0)

df[['signal']].plot(ax=ax1,style='-.',alpha=0.4)

ax0.set_title("HMA - Volume: Short vs Long")

ax1.legend()

plt.title("HMA - Signals")

plt.show()

figs = (10,4)

df2['cumulative_returns_volume'].plot(figsize = figs)

plt.title("Cumulative Return")

plt.show()

- Printing the latest value of CR

df2['cumulative_returns_volume'].tail()[-1]

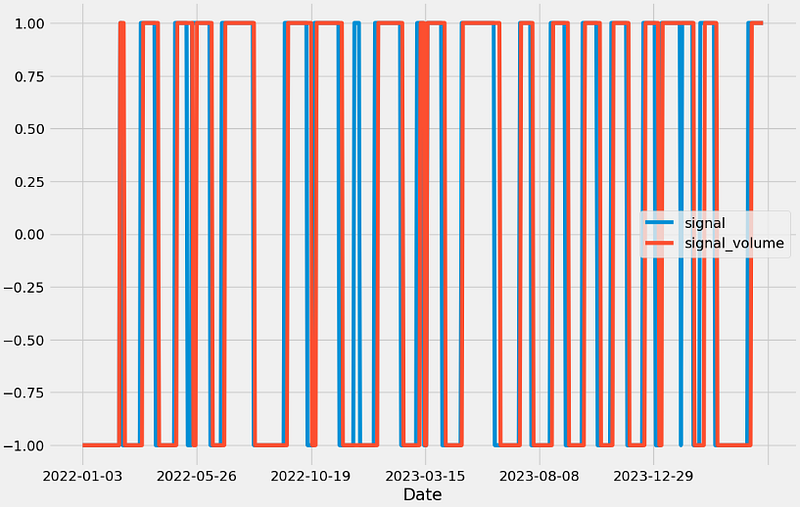

2.1535115868707386Trading Signals of Strategies A and B

- Comparing trading signals of Strategies A and B

df['signal'] = np.where(df['hma_short'] > df['hma_long'],1,-1)

df['signal_volume'] = np.where(df['hma_volume_short'] > df['hma_volume_long'],1,-1)

figsize=(12,8)

df[['signal','signal_volume']].plot(figsize=figsize)

plt.show()

Backtesting Buy & Hold Strategy

- Calculating expected returns of the NVDA Buy/Hold passive strategy

# Selecting libraries

import yfinance as yf

import pandas as pd

import numpy as np

benchmark='NVDA'

def get_benchmark(start_date, investment_value):

spy=yf.download(benchmark, start=start_date)['Adj Close']

benchmark1 = pd.DataFrame(np.diff(spy)).rename(columns = {0:'benchmark_returns'})

investment_value = investment_value

number_of_stocks = floor(investment_value/spy[0])

benchmark_investment_ret = []

for i in range(len(benchmark1['benchmark_returns'])):

returns = number_of_stocks*benchmark1['benchmark_returns'][i]

benchmark_investment_ret.append(returns)

benchmark_investment_ret_df = pd.DataFrame(benchmark_investment_ret).rename(columns = {0:'investment_returns'})

return benchmark_investment_ret_df

benchmark1 = get_benchmark('2022-01-01', 10000)

investment_value = 10000

total_benchmark_investment_ret = round(sum(benchmark1['investment_returns']), 2)

benchmark_profit_percentage = floor((total_benchmark_investment_ret/investment_value)*100)

print(cl('Buy/Hold Profit by investing $10k in NVDA: {}'.format(total_benchmark_investment_ret), attrs = ['bold']))

print(cl('Buy/Hold Profit percentage : {}%'.format(benchmark_profit_percentage), attrs = ['bold']))

Buy/Hold Profit by investing $10k in NVDA: 20592.3

Buy/Hold Profit percentage : 205%Backtesting S&P 500 Benchmark

- Calculating expected returns of the ^GSPC benchmark

benchmark='^GSPC'

def get_benchmark(start_date, investment_value):

spy=yf.download(benchmark, start=start_date)['Adj Close']

benchmark1 = pd.DataFrame(np.diff(spy)).rename(columns = {0:'benchmark_returns'})

investment_value = investment_value

number_of_stocks = floor(investment_value/spy[0])

benchmark_investment_ret = []

for i in range(len(benchmark1['benchmark_returns'])):

returns = number_of_stocks*benchmark1['benchmark_returns'][i]

benchmark_investment_ret.append(returns)

benchmark_investment_ret_df = pd.DataFrame(benchmark_investment_ret).rename(columns = {0:'investment_returns'})

return benchmark_investment_ret_df

benchmark1 = get_benchmark('2022-01-01', 10000)

investment_value = 10000

total_benchmark_investment_ret = round(sum(benchmark1['investment_returns']), 2)

benchmark_profit_percentage = floor((total_benchmark_investment_ret/investment_value)*100)

print(cl('Benchmark Profit by investing $10k in ^GSPC: {}'.format(total_benchmark_investment_ret), attrs = ['bold']))

print(cl('Benchmark Profit percentage : {}%'.format(benchmark_profit_percentage), attrs = ['bold']))

Benchmark Profit by investing $10k in ^GSPC: 1013.42

Benchmark Profit percentage : 10%Conclusions

- Our HMA backtesting results can be summarized in terms of 2Y NVDA ROI % on 2024–05–17 as follows:

- Strategy A: 170

- Strategy B: 215

- Buy/Hold: 205

- ^GSPC: 10

- We can see that Strategy B yields the highest win rate.

- All three strategies outperform the S&P 500 from 2022–01–01 to 2024–05–17.

Credits

References

- Hull Moving Average (HMA) Using Python

- Mean Reversion Trading Strategy Using Python

- Advanced Trading Techniques: Mastering the Hull Moving Average

- Nikhil-Adithyan/Algorithmic-Trading-with-Python

Explore More

- A Market-Neutral Strategy

- A Comprehensive Analysis of Best Trading Technical Indicators w/ TA-Lib — Tesla ‘23

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- NVIDIA Rolling Volatility: GARCH & XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Plotly Dash TA Stock Market App

- Data Visualization in Python — 1. Stock Technical Indicators