NVIDIA Short-Term Stock Price Forecasting: SHAP Explainer, Lags, Optimized ML Regressors, Auto-ARIMA, Multi-Seasonal FB Prophet Tuning & LSTM

- “Most forecasts don’t allow for alternative outcomes.” Howard Marks.

- The key question is whether the integrated Explainable AI, Statistical Modeling, Supervised ML algorithms and model tuning can predict the future of NVIDIA’s AI with alternative outcomes.

- This article is about NVIDIA (NASDAQ: NVDA) Short-Term Stock Price Forecasting [3] using SHAP 60+ Feature Engineering (FE) [1], Basic Linear Regression with Time Lags [2], 8 Supervised ML Regressors (Scikit-Learn) with Hyperparameter Optimization (HPO) [1,4], Auto-ARIMA time series fitting [1,5], Multi-Seasonal FB Prophet Forecasting HPO with anomalous dates [1], and end-to-end LSTM with Validation QC.

Motivation

- NVIDIA is one of the ‘Magnificent Seven’ group of influential US mega stocks (along with Apple, Microsoft, Alphabet, Amazon, Tesla and Meta Platforms) [3].

- The business has enjoyed meteoric success in recent years and, on 18 June 2024, leap-frogged both Microsoft and Apple to briefly become the world’s most valuable company.

- Charlie Huggins, manager of the Wealth Club Quality Shares Portfolio, says: “The NVIDIA stock split doesn’t change the fundamentals, or value, of the business. But it could make the shares even more attractive to retail investors.”

- Thanks to the boom in AI, NVIDIA is enjoying a purple patch. According to Victoria Scholar, head of investment at interactive investor, an online share trading service, the “AI stock market darling” was the most bought stock among the platform’s UK investors for the second month running in May 2024.

Challenge

- It’s impossible to predict with certainty how a company’s share price will perform [3].

- A stock’s behavior depends partly on the business’s internal performance, combined with wider macro-economic events affecting the markets in which it operates.

Objectives

- Predict short-term NVDA stock price through analyzing the relationship between the stock price and various features.

- Ultimately, the primary goal is to enhance the accuracy of NVDA price predictions, enabling investors to anticipate market movements and potentially maximize profits.

- Including making informed investment decisions, averting losses, optimizing stockholder investments, and improving decision-making strategies.

Tools

The Machine Learning library SciKit-learn in Python comes with a load of features to simplify ML:

- Supervised ML: Generalized linear models such as Linear regression, Decision Trees, SVM, Random Forest, Bayesian methods, etc.

- Unsupervised ML: factoring, clustering, PCA, and unsupervised NN.

- Cross-validation: The accuracy and validity of supervised models on unseen data can be checked with the help of SciKit-learn.

- FB Prophet

Developed by Facebook (FB) and made an open-source contribution to the data science community, Prophet is a powerful forecasting tool available in both R and Python. It is fast, accurate, automated, and feature-rich.

For the time series forecasting shown below, we will be using FB Prophet. More information can be found here: https://facebook.github.io/prophet/

Pros: The model provides an interpretable decomposition of the data that is observed or forecasted into seasonal, trend, and holiday components. This is useful if you want to understand why you are seeing certain patterns on certain day.

Cons: Seasonality not explicitly modeled; lagged effect when forecasting; lacks support for multiple inputs.

ARIMA perform well, if data is not stationary then we can use differencing to make it stationary. If data exhibits clear trends and regular seasonality, ARIMA can be a good choice. ARIMA’s forecasting accuracy tends to reduce as the forecast horizon increases. So it is not good for long-term forecasts.

Read more here.

Using Keras and Tensorflow (TF) makes building NN much easier to build from scratch.

Scikit-Learn is primarily used for traditional ML tasks and algorithms.

TF is mainly utilized for deep learning problems, particularly in AI.

SHAP (SHapley Additive exPlanations) values are a way to explain the output of any machine learning model. It uses a game theoretic approach that measures each player’s contribution to the final outcome. In ML, each feature is assigned an importance value representing its contribution to the model’s output.

SHAP values show how each feature affects each final prediction, the significance of each feature compared to others, and the model’s reliance on the interaction between features.

8 Supervised ML Algorithms

name model

0 Linear Regression LinearRegression()

1 KNeighbors Regressor KNeighborsRegressor()

2 Support Vector Machines SVR()

3 Linear SVR LinearSVR()

4 Random Forest Regressor RandomForestRegressor()

5 Bagging Regressor BaggingRegressor()

6 XGB Regressor XGBRegressor()

7 MLP Regressor MLPRegressor() Key ML Error Metrics

- R2 score, RMSE, MAE, Explained Variance Score, and MAPE.

Milestones

- Exploratory Data Analysis (EDA) of Input Stock Data

- Basic Linear Regression with Time-Step & Lag Features

- TSFRESH Feature Engineering [1]

- Multi-Seasonal FB Prophet Prediction & HPO

- Auto-ARIMA Model Fitting & SARIMAX QC Summary

- SciKit-Learn Supervised ML Regression & HPO

- SHAP Feature Dominance Analysis

- TF LSTM Keras Prediction & Validation QC

Let’s get into the specifics of the proposed methodology with a final source code line-by-line explained.

Python Imports, Installations & Settings

- Installing/importing necessary Python libraries and setting parameters

!pip install seaborn, yfinance, sklearn, tsfresh, prophet, lightgbm, xgboost, pmdarima, shap, statsmodels, plotly, xgboost

import random

import os

import numpy as np

import pandas as pd

import requests

#import pandas_datareader as web

import yfinance as yf

# Date

import datetime as dt

from datetime import date, timedelta, datetime

# EDA

import seaborn as sns

import matplotlib.pyplot as plt

from matplotlib.pylab import rcParams

import plotly.express as px

import plotly.graph_objects as go

from plotly.offline import init_notebook_mode

init_notebook_mode(connected=True)

# FE

from tsfresh import extract_features, select_features, extract_relevant_features

from tsfresh.utilities.dataframe_functions import impute

from sklearn.inspection import permutation_importance

import shap

# Time Series Modelling

import statsmodels.api as sm

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

from statsmodels.tsa.stattools import adfuller

from statsmodels.tsa.seasonal import seasonal_decompose

from statsmodels.tsa.arima_model import ARIMA

# Metrics

from sklearn.metrics import r2_score

from sklearn.metrics import mean_squared_error, mean_absolute_percentage_error

# Modeling and preprocessing

from sklearn.preprocessing import StandardScaler, MinMaxScaler

from sklearn.model_selection import train_test_split, GridSearchCV

from sklearn.linear_model import LinearRegression

from sklearn.svm import SVR, LinearSVR

from sklearn.neighbors import KNeighborsRegressor

from sklearn.ensemble import RandomForestRegressor

from sklearn.ensemble import BaggingRegressor, AdaBoostRegressor

from sklearn.neural_network import MLPRegressor

from prophet import Prophet

import xgboost as xgb

from xgboost import XGBRegressor

import lightgbm as lgb

from lightgbm import LGBMRegressor

import pmdarima as pm

import warnings

warnings.filterwarnings("ignore")

# Set random state

def fix_all_seeds(seed):

np.random.seed(seed)

random.seed(seed)

os.environ['PYTHONHASHSEED'] = str(seed)

random_state = 42

fix_all_seeds(random_state)

# Set main parameters

cryptocurrency = 'NVDA' #define any stock

target = 'Close'

forecasting_days = 10

# Set time interval of data for given cryptocurrency - the period of coronavirus in 2020-2021

date_start = dt.datetime(2020, 4, 1)

# date_end = dt.datetime.now()

date_end = dt.datetime(2024, 7, 13) Reading & Analyzing Input Stock Data

- Using Yahoo Finance to fetch the daily NVIDIA historical data from 2020–04–01 to 2024–07–12

def get_data(cryptocurrency, date_start, date_end=None):

# Get data for a given stock

# date_end = None means that the date_end is the current day

if date_end is None:

date_end = dt.datetime.now()

df =yf.download(cryptocurrency, date_start, date_end)

return df

# Download data of the cryptocurrency via API

df = get_data(cryptocurrency, date_start, date_end)- Let’s drop ‘Adj Close’ and take a look at the general structure, descriptive statistics of the dataset and missing values if any

df = df.drop(columns = ["Adj Close"])

df.tail()

Open High Low Close Volume

Date

2024-07-08 127.489998 130.770004 127.040001 128.199997 237677300

2024-07-09 130.350006 133.820007 128.649994 131.380005 285366600

2024-07-10 134.029999 135.100006 132.419998 134.910004 248978600

2024-07-11 135.750000 136.149994 127.050003 127.400002 374782700

2024-07-12 128.259995 131.919998 127.220001 129.240005 252103100

df.shape

(1077, 5)

df.info()

<class 'pandas.core.frame.DataFrame'>

DatetimeIndex: 1077 entries, 2020-04-01 to 2024-07-12

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Open 1077 non-null float64

1 High 1077 non-null float64

2 Low 1077 non-null float64

3 Close 1077 non-null float64

4 Volume 1077 non-null int64

dtypes: float64(4), int64(1)

memory usage: 50.5 KB

df_nan_count = df.isna().sum()

print(df_nan_count)

Open 0

High 0

Low 0

Close 0

Volume 0

dtype: int64- Creating the column ‘Time’ as follows

df['Time'] = np.arange(len(df.index))

Date

2020-01-02 0

2020-01-03 1

2020-01-06 2

2020-01-07 3

2020-01-08 4

...

2024-07-08 1134

2024-07-09 1135

2024-07-10 1136

2024-07-11 1137

2024-07-12 1138

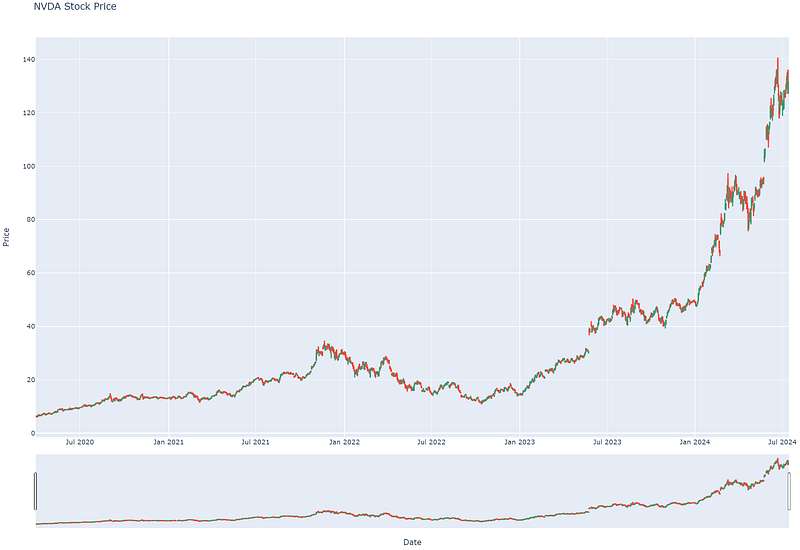

Name: Time, Length: 1139, dtype: int32- Using Plotly to plot the interactive stock candlesticks

import pandas as pd

import plotly.io as pio

import plotly.graph_objects as go

pio.renderers.default='browser'

def get_candlestick_chart(df: pd.DataFrame):

layout = go.Layout(

title = 'NVDA Stock Price',

xaxis = {'title': 'Date'},

yaxis = {'title': 'Price'},

)

fig = go.Figure(

layout=layout,

data=[

go.Candlestick(

x = df['Date'],

open = df['Open'],

high = df['High'],

low = df['Low'],

close = df['Close'],

name = 'Candlestick chart'

),

]

)

fig.update_xaxes(rangebreaks = [{'bounds': ['sat', 'mon']}])

return fig

if __name__ == '__main__':

fig = get_candlestick_chart(df)

fig.show()

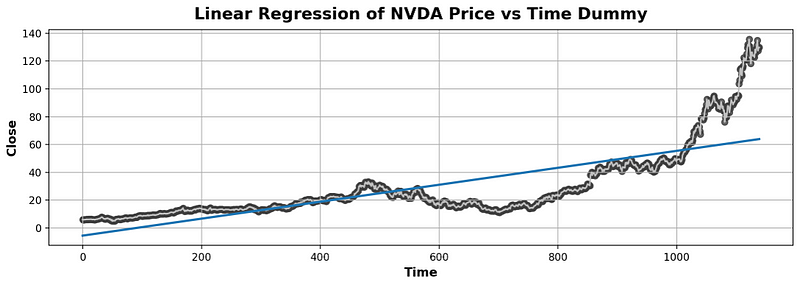

Linear Regression with Time-Step & Lag Features

- Let’s begin with Linear Regression (LR) using the most basic time-step feature ‘Time’ v.s. (aka time dummy)

#import matplotlib.pyplot as plt

#import seaborn as sns

plt.rc(

"figure",

autolayout=True,

figsize=(11, 4),

titlesize=18,

titleweight='bold',

)

plt.rc(

"axes",

labelweight="bold",

labelsize="large",

titleweight="bold",

titlesize=16,

titlepad=10,

)

%config InlineBackend.figure_format = 'retina'

fig, ax = plt.subplots()

ax.plot('Time', 'Close', data=df, color='0.75')

ax = sns.regplot(x='Time', y='Close', data=df, ci=None, scatter_kws=dict(color='0.25'))

ax.set_title('Linear Regression of NVDA Price vs Time Dummy');

plt.grid()

- Clearly, LR does not fit the Close price well as Time>1000.

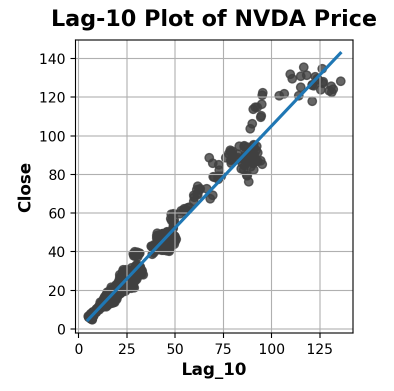

- Let’s try LR with lag features [2].

- Firstly, we compute Lag_10 for the 10-day forecast

df['Lag_10'] = df['Close'].shift(10)

df = df.reindex(columns=['Close', 'Lag_10'])

#df.head()

fig, ax = plt.subplots()

ax = sns.regplot(x='Lag_10', y='Close', data=df, ci=None, scatter_kws=dict(color='0.25'))

ax.set_aspect('equal')

ax.set_title('Lag-10 X-Plot of NVDA Price');

plt.grid()

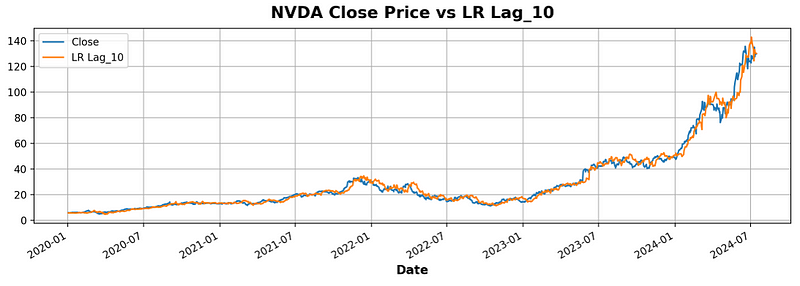

- Training the LR model with the above feature and making predictions

from sklearn.linear_model import LinearRegression

# Training data

X = df.loc[:, ['Lag_10']].fillna(method='bfill') # features

y = df.loc[:, 'Close'] # target

# Train the model

model = LinearRegression()

model.fit(X, y)

# Store the fitted values as a time series with the same time index as

# the training data

y_pred = pd.Series(model.predict(X), index=X.index)

y.plot(label='Close')

y_pred.plot(label='LR Lag_10')

plt.legend()

plt.title('NVDA Close Price vs LR Lag_10')

plt.grid()

- Quantifying the quality of LR predictions

from sklearn.metrics import r2_score

r2_score(y, y_pred)

0.9806962531842807

from sklearn.metrics import root_mean_squared_error

root_mean_squared_error(y, y_pred)

3.62088252156672

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y, y_pred)

2.2952125909109022

from sklearn.metrics import explained_variance_score

explained_variance_score(y, y_pred)

0.9806962531842807TSFRESH Feature Engineering

- Performing Feature Engineering with TSFRESH [1]

def get_tsfresh_features(data):

# Get statistic features using library TSFRESH

# Thanks to https://www.kaggle.com/code/vbmokin/btc-growth-forecasting-with-advanced-fe-for-ohlc

data = data.reset_index(drop=False).reset_index(drop=False)

# Extract features

extracted_features = extract_features(data, column_id="Date", column_sort="Date")

# Drop features with NaN

extracted_features_clean = extracted_features.dropna(axis=1, how='all').reset_index(drop=True)

# Drop features with constants

cols_std_zero = []

for col in extracted_features_clean.columns:

if extracted_features_clean[col].std()==0:

cols_std_zero.append(col)

extracted_features_clean = extracted_features_clean.drop(columns = cols_std_zero)

extracted_features_clean['Date'] = data['Date'] # For the merging

return extracted_features_clean

extracted_features_clean = get_tsfresh_features(df[['Close']])

#extracted_features_clean

extracted_features_clean.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1077 entries, 0 to 1076

Data columns (total 51 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 index__sum_values 1077 non-null float64

1 index__abs_energy 1077 non-null float64

2 index__median 1077 non-null float64

3 index__mean 1077 non-null float64

4 index__root_mean_square 1077 non-null float64

5 index__maximum 1077 non-null float64

6 index__absolute_maximum 1077 non-null float64

7 index__minimum 1077 non-null float64

8 index__benford_correlation 1076 non-null float64

9 index__quantile__q_0.1 1077 non-null float64

10 index__quantile__q_0.2 1077 non-null float64

11 index__quantile__q_0.3 1077 non-null float64

12 index__quantile__q_0.4 1077 non-null float64

13 index__quantile__q_0.6 1077 non-null float64

14 index__quantile__q_0.7 1077 non-null float64

15 index__quantile__q_0.8 1077 non-null float64

16 index__quantile__q_0.9 1077 non-null float64

17 index__cwt_coefficients__coeff_0__w_2__widths_(2, 5, 10, 20) 1077 non-null float64

18 index__cwt_coefficients__coeff_0__w_5__widths_(2, 5, 10, 20) 1077 non-null float64

19 index__cwt_coefficients__coeff_0__w_10__widths_(2, 5, 10, 20) 1077 non-null float64

20 index__cwt_coefficients__coeff_0__w_20__widths_(2, 5, 10, 20) 1077 non-null float64

21 index__fft_coefficient__attr_"real"__coeff_0 1077 non-null float64

22 index__fft_coefficient__attr_"abs"__coeff_0 1077 non-null float64

23 index__value_count__value_0 1077 non-null float64

24 index__value_count__value_1 1077 non-null float64

25 index__range_count__max_1__min_-1 1077 non-null float64

26 index__count_below__t_0 1077 non-null float64

27 Close__sum_values 1077 non-null float64

28 Close__abs_energy 1077 non-null float64

29 Close__median 1077 non-null float64

30 Close__mean 1077 non-null float64

31 Close__root_mean_square 1077 non-null float64

32 Close__maximum 1077 non-null float64

33 Close__absolute_maximum 1077 non-null float64

34 Close__minimum 1077 non-null float64

35 Close__benford_correlation 1077 non-null float64

36 Close__quantile__q_0.1 1077 non-null float64

37 Close__quantile__q_0.2 1077 non-null float64

38 Close__quantile__q_0.3 1077 non-null float64

39 Close__quantile__q_0.4 1077 non-null float64

40 Close__quantile__q_0.6 1077 non-null float64

41 Close__quantile__q_0.7 1077 non-null float64

42 Close__quantile__q_0.8 1077 non-null float64

43 Close__quantile__q_0.9 1077 non-null float64

44 Close__cwt_coefficients__coeff_0__w_2__widths_(2, 5, 10, 20) 1077 non-null float64

45 Close__cwt_coefficients__coeff_0__w_5__widths_(2, 5, 10, 20) 1077 non-null float64

46 Close__cwt_coefficients__coeff_0__w_10__widths_(2, 5, 10, 20) 1077 non-null float64

47 Close__cwt_coefficients__coeff_0__w_20__widths_(2, 5, 10, 20) 1077 non-null float64

48 Close__fft_coefficient__attr_"real"__coeff_0 1077 non-null float64

49 Close__fft_coefficient__attr_"abs"__coeff_0 1077 non-null float64

50 Date 1077 non-null datetime64[ns]

dtypes: datetime64[ns](1), float64(50)

memory usage: 429.2 KB- Merging all features

df = pd.merge(df, extracted_features_clean, how='left', on='Date')

df.shape

(1077, 56)- Adding more features

def get_add_features(df_feat):

# FE for data as row of DataFrame

# Thanks to https://www.kaggle.com/code/vbmokin/g-research-crypto-forecasting-baseline-fe

# Two new features from the competition tutorial

df_feat['Upper_Shadow'] = df_feat['High'] - np.maximum(df_feat['Close'], df_feat['Open'])

df_feat['Lower_Shadow'] = np.minimum(df_feat['Close'], df_feat['Open']) - df_feat['Low']

# Thanks to https://www.kaggle.com/code1110/gresearch-simple-lgb-starter

df_feat['lower_shadow'] = np.minimum(df_feat['Close'], df_feat['Open']) - df_feat['Low']

df_feat['high2low'] = (df_feat['High'] / df_feat['Low']).replace([np.inf, -np.inf, np.nan], 0.)

return df_feat

df = get_add_features(df)

df.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1077 entries, 0 to 1076

Data columns (total 60 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Date 1077 non-null datetime64[ns]

1 Open 1077 non-null float64

2 High 1077 non-null float64

3 Low 1077 non-null float64

4 Close 1077 non-null float64

5 Volume 1077 non-null int64

6 index__sum_values 1077 non-null float64

7 index__abs_energy 1077 non-null float64

8 index__median 1077 non-null float64

9 index__mean 1077 non-null float64

10 index__root_mean_square 1077 non-null float64

11 index__maximum 1077 non-null float64

12 index__absolute_maximum 1077 non-null float64

13 index__minimum 1077 non-null float64

14 index__benford_correlation 1076 non-null float64

15 index__quantile__q_0.1 1077 non-null float64

16 index__quantile__q_0.2 1077 non-null float64

17 index__quantile__q_0.3 1077 non-null float64

18 index__quantile__q_0.4 1077 non-null float64

19 index__quantile__q_0.6 1077 non-null float64

20 index__quantile__q_0.7 1077 non-null float64

21 index__quantile__q_0.8 1077 non-null float64

22 index__quantile__q_0.9 1077 non-null float64

23 index__cwt_coefficients__coeff_0__w_2__widths_(2, 5, 10, 20) 1077 non-null float64

24 index__cwt_coefficients__coeff_0__w_5__widths_(2, 5, 10, 20) 1077 non-null float64

25 index__cwt_coefficients__coeff_0__w_10__widths_(2, 5, 10, 20) 1077 non-null float64

26 index__cwt_coefficients__coeff_0__w_20__widths_(2, 5, 10, 20) 1077 non-null float64

27 index__fft_coefficient__attr_"real"__coeff_0 1077 non-null float64

28 index__fft_coefficient__attr_"abs"__coeff_0 1077 non-null float64

29 index__value_count__value_0 1077 non-null float64

30 index__value_count__value_1 1077 non-null float64

31 index__range_count__max_1__min_-1 1077 non-null float64

32 index__count_below__t_0 1077 non-null float64

33 Close__sum_values 1077 non-null float64

34 Close__abs_energy 1077 non-null float64

35 Close__median 1077 non-null float64

36 Close__mean 1077 non-null float64

37 Close__root_mean_square 1077 non-null float64

38 Close__maximum 1077 non-null float64

39 Close__absolute_maximum 1077 non-null float64

40 Close__minimum 1077 non-null float64

41 Close__benford_correlation 1077 non-null float64

42 Close__quantile__q_0.1 1077 non-null float64

43 Close__quantile__q_0.2 1077 non-null float64

44 Close__quantile__q_0.3 1077 non-null float64

45 Close__quantile__q_0.4 1077 non-null float64

46 Close__quantile__q_0.6 1077 non-null float64

47 Close__quantile__q_0.7 1077 non-null float64

48 Close__quantile__q_0.8 1077 non-null float64

49 Close__quantile__q_0.9 1077 non-null float64

50 Close__cwt_coefficients__coeff_0__w_2__widths_(2, 5, 10, 20) 1077 non-null float64

51 Close__cwt_coefficients__coeff_0__w_5__widths_(2, 5, 10, 20) 1077 non-null float64

52 Close__cwt_coefficients__coeff_0__w_10__widths_(2, 5, 10, 20) 1077 non-null float64

53 Close__cwt_coefficients__coeff_0__w_20__widths_(2, 5, 10, 20) 1077 non-null float64

54 Close__fft_coefficient__attr_"real"__coeff_0 1077 non-null float64

55 Close__fft_coefficient__attr_"abs"__coeff_0 1077 non-null float64

56 Upper_Shadow 1077 non-null float64

57 Lower_Shadow 1077 non-null float64

58 lower_shadow 1077 non-null float64

59 high2low 1077 non-null float64

dtypes: datetime64[ns](1), float64(58), int64(1)

memory usage: 505.0 KB

FB Prophet Prediction

- Preparing the DF for FB Prophet forecasting [1]

# Create a new dataframe with anomalous dates for Facebook Prophet

if is_anomalies:

anomalous_dates = ['2020-09-03', '2021-02-12', '2021-04-13', '2021-12-02',

'2022-04-01', '2023-08-29', '2024-03-26', '2024-06-18']

holidays_df = pd.DataFrame(columns = ['ds', 'lower_window', 'upper_window', 'prior_scale'])

holidays_df['ds'] = anomalous_dates

holidays_df['holiday'] = 'anomalous_dates'

holidays_df['lower_window'] = 0

holidays_df['upper_window'] = 0

holidays_df['prior_scale'] = 10

display(holidays_df)

ds lower_window upper_window prior_scale holiday

0 2020-09-03 0 0 10 anomalous_dates

1 2021-02-12 0 0 10 anomalous_dates

2 2021-04-13 0 0 10 anomalous_dates

3 2021-12-02 0 0 10 anomalous_dates

4 2022-04-01 0 0 10 anomalous_dates

5 2023-08-29 0 0 10 anomalous_dates

6 2024-03-26 0 0 10 anomalous_dates

7 2024-06-18 0 0 10 anomalous_dates

# Add a few more anomalous dates

if is_anomalies:

anomalous_dates_diff = anomalous_dates.copy()

anomalous_dates_diff.append('2022-08-08')

anomalous_dates_diff.append('2022-12-01')

anomalous_dates_diff.append('2023-11-21')

print(anomalous_dates_diff)

['2020-09-03', '2021-02-12', '2021-04-13', '2021-12-02', '2022-04-01', '2023-08-29', '2024-03-26', '2024-06-18', '2022-08-08', '2022-12-01', '2023-11-21']

# Create a new feature in df for anomalous_dates_diff

if is_anomalies:

df['Close_diff_anomalous'] = df['Date'].isin(anomalous_dates_diff).astype('int')

display(df)

# Number of anomalous dates

print(f"Number of anomalous dates - {df['Close_diff_anomalous'].sum()}")

Number of anomalous dates - 11

# Illustration of number transformations in the columns:

# "Close" -> "Close_diff" -> "Target" -> "Close_diff_pred" -> "Close_pred"

# Get target and the result of the forecasting

forecasting_days_example = 3

df_example = pd.DataFrame({'Close':[1, 2, 4, 8, 15, 25], 'Day': [0, 1, 2, 3, 4, 5]})

df_example['Close_diff'] = df_example['Close'].diff()

df_example['target'] = df_example['Close_diff'].shift(-forecasting_days_example)

df_example['target_pred'] = df_example['target'].copy() # Ideal forecasting result

print(f'Simulation of the result of ideal forecasting the "target_pred" for {forecasting_days_example} days')

display(df_example[['Day', 'Close', 'Close_diff', 'target', 'target_pred']])

# Get inverse target

print('\nSimulation of the recovering predicted values "Close_pred" from the "target_pred"')

df_example['Close_diff_pred_shifted'] = df_example['target_pred'].shift(forecasting_days_example)

# Let's create an intermediate feature to make it easier to explain the transformation

temp_column_name = f'Close_diff_pred_shifted_with_Close' # Intermediate feature for transformations

df_example[temp_column_name] = df_example['Close_diff_pred_shifted'].copy()

df_example.loc[forecasting_days_example, temp_column_name] = df_example.loc[forecasting_days_example,'Close']

df_example['Close_pred'] = np.concatenate((df_example['Close'].tolist()[:forecasting_days_example],

np.cumsum(df_example[temp_column_name].values[forecasting_days_example:], dtype=float)))

df_example['Close_pred'] = df_example['Close_pred'].astype('int')

display(df_example[['Day', 'Close', 'Close_diff', 'target', 'target_pred', 'Close_diff_pred_shifted', temp_column_name, 'Close_pred']])

Simulation of the result of ideal forecasting the "target_pred" for 3 days

Day Close Close_diff target target_pred

0 0 1 NaN 4.0 4.0

1 1 2 1.0 7.0 7.0

2 2 4 2.0 10.0 10.0

3 3 8 4.0 NaN NaN

4 4 15 7.0 NaN NaN

5 5 25 10.0 NaN NaN

Simulation of the recovering predicted values "Close_pred" from the "target_pred"

Day Close Close_diff target target_pred Close_diff_pred_shifted Close_diff_pred_shifted_with_Close Close_pred

0 0 1 NaN 4.0 4.0 NaN NaN 1

1 1 2 1.0 7.0 7.0 NaN NaN 2

2 2 4 2.0 10.0 10.0 NaN NaN 4

3 3 8 4.0 NaN NaN 4.0 8.0 8

4 4 15 7.0 NaN NaN 7.0 7.0 15

5 5 25 10.0 NaN NaN 10.0 10.0 25

def cut_data(df, y, num_start, num_end):

# Cutting dataframe df and array or list for [num_start, num_end-1]

df2 = df[num_start:(num_end+1)]

y2 = y[num_start:(num_end+1)] if y is not None else None

return df2, y2

def get_train_valid_test_ts(df, forecasting_days, target='Close'):

# Get training, validation and test datasets with target for Time Series models

# Data prepairing

df = df.dropna(how="any").reset_index(drop=True)

df = df[['Date', 'Close']]

df.columns = ['ds', 'y']

y = None

N = len(df)

train, _ = cut_data(df, y, 0, N-2*forecasting_days-1)

valid, _ = cut_data(df, y, N-2*forecasting_days, N-forecasting_days-1)

test, _ = cut_data(df, y, N-forecasting_days, N)

# Train+valid - for optimal model training

train_valid = pd.concat([train, valid])

print(f'Origin dataset has {len(df)} rows and {len(df.columns)} features')

print(f'Get training dataset with {len(train)} rows')

print(f'Get validation dataset with {len(valid)} rows')

print(f'Get test dataset with {len(test)} rows')

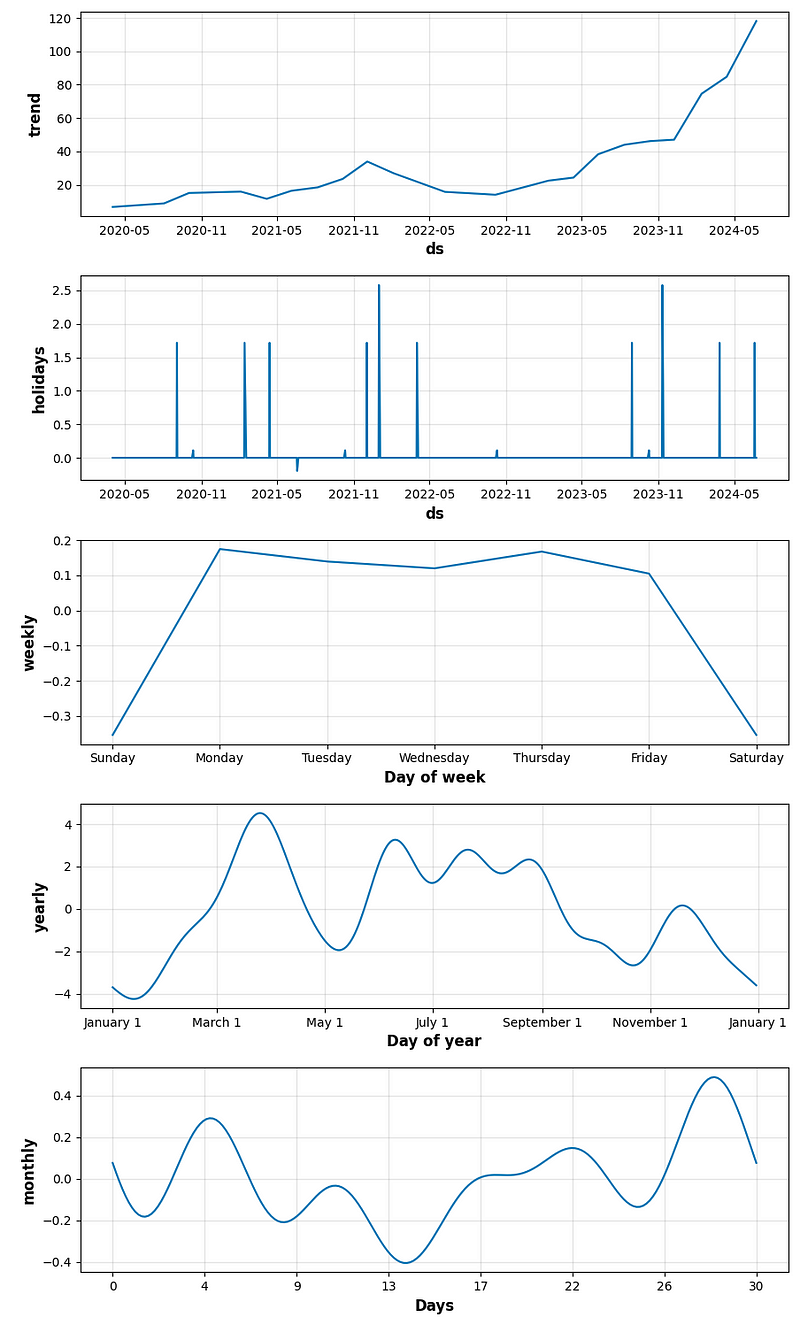

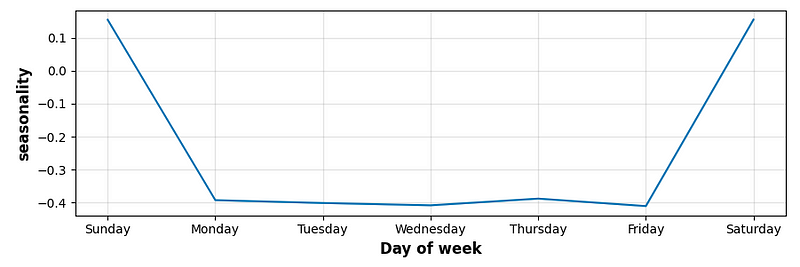

return train, valid, test, train_valid- FB Prophet model training, tuning and forecasting with multiple trends [1], seasonality, the above anomalous dates and in-built US holidays

def get_train_valid_test_mf(df, forecasting_days, target='target'):

# Get training, validation and test datasets with target for multi-features ML models

df = df.drop(columns = ['Date']).dropna(how="any").reset_index(drop=True)

# Save and drop target

y = df.pop(target)

# Get starting points for the recovering "Close" from "Close_diff_shigted"

N = len(df)

#print(f"Total - {N}, Valid start index = {N-forecasting_days-1}, Test start index = {N-1}")

start_points = {'valid_start_point' : df.loc[N-forecasting_days-1, 'Close'],

'test_start_point' : df.loc[N-1, 'Close']}

# Standartization data

scaler = StandardScaler()

df = pd.DataFrame(scaler.fit_transform(df), columns = df.columns)

train, ytrain = cut_data(df.copy(), y, 0, N-2*forecasting_days-1)

valid, yvalid = cut_data(df.copy(), y, N-2*forecasting_days, N-forecasting_days-1)

test, ytest = cut_data(df.copy(), y, N-forecasting_days, N)

# Train+valid - for optimal model training

train_valid = pd.concat([train, valid])

y_train_valid = pd.concat([ytrain, yvalid])

print(f'Origin dataset has {len(df)} rows and {len(df.columns)} features')

print(f'Get training dataset with {len(train)} rows')

print(f'Get validation dataset with {len(valid)} rows')

print(f'Get test dataset with {len(test)} rows')

return train, ytrain, valid, yvalid, test, ytest, train_valid, y_train_valid, start_points

#Model training and forecasting

def calc_metrics(type_score, list_true, list_pred):

# Calculation score with type=type_score for list_true and list_pred

if type_score=='r2_score':

score = r2_score(list_true, list_pred)

elif type_score=='rmse':

score = mean_squared_error(list_true, list_pred, squared=False)

elif type_score=='mape':

score = mean_absolute_percentage_error(list_true, list_pred)

return score

def result_add_metrics(result, n, y_true, y_pred):

# Calculate and add metrics to dataframe result[n,:]

result.loc[n,'r2_score'] = calc_metrics('r2_score', y_true, y_pred)

result.loc[n,'rmse'] = calc_metrics('rmse', y_true, y_pred) # in coins

result.loc[n,'mape'] = 100*calc_metrics('mape', y_true, y_pred) # in %

return result

# Results of all models

result = pd.DataFrame(columns = ['name_model', 'type_data', 'r2_score', 'rmse', 'mape', 'params', 'ypred'])

if is_Prophet:

df2=df.copy()

display(df2)

# Get datasets

if is_Prophet:

train_ts, valid_ts, test_ts, train_valid_ts = get_train_valid_test_ts(df2.copy(), forecasting_days, target='Close')

if not is_anomalies:

holidays_df = None

from prophet.plot import add_changepoints_to_plot

def prophet_modeling(result,

cryptocurrency,

train,

test,

holidays_df,

period_days,

fourier_order_seasonality,

forecasting_period,

name_model,

type_data):

# Performs FB Prophet model training for given train dataset, holidays_df and seasonality_mode

# Performs forecasting with period by this model, visualization and error estimation

# df - dataframe with real data in the forecasting_period

# can be such combinations of parameters: train=train, test=valid or train=train_valid, test=test

# Save results into dataframe result

# Build Prophet model with parameters and structure

model = Prophet(daily_seasonality=False,

weekly_seasonality=True,

yearly_seasonality=True,

changepoint_range=1,

changepoint_prior_scale = 0.5,

holidays=holidays_df,

seasonality_mode = 'additive'

)

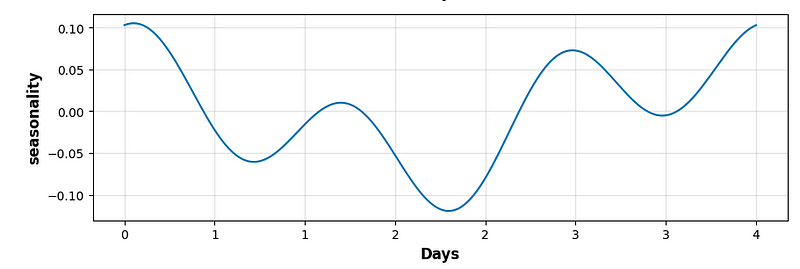

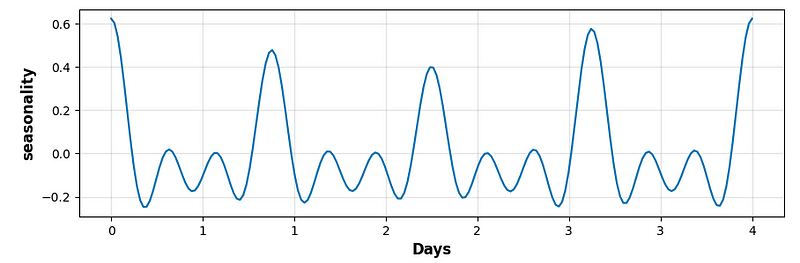

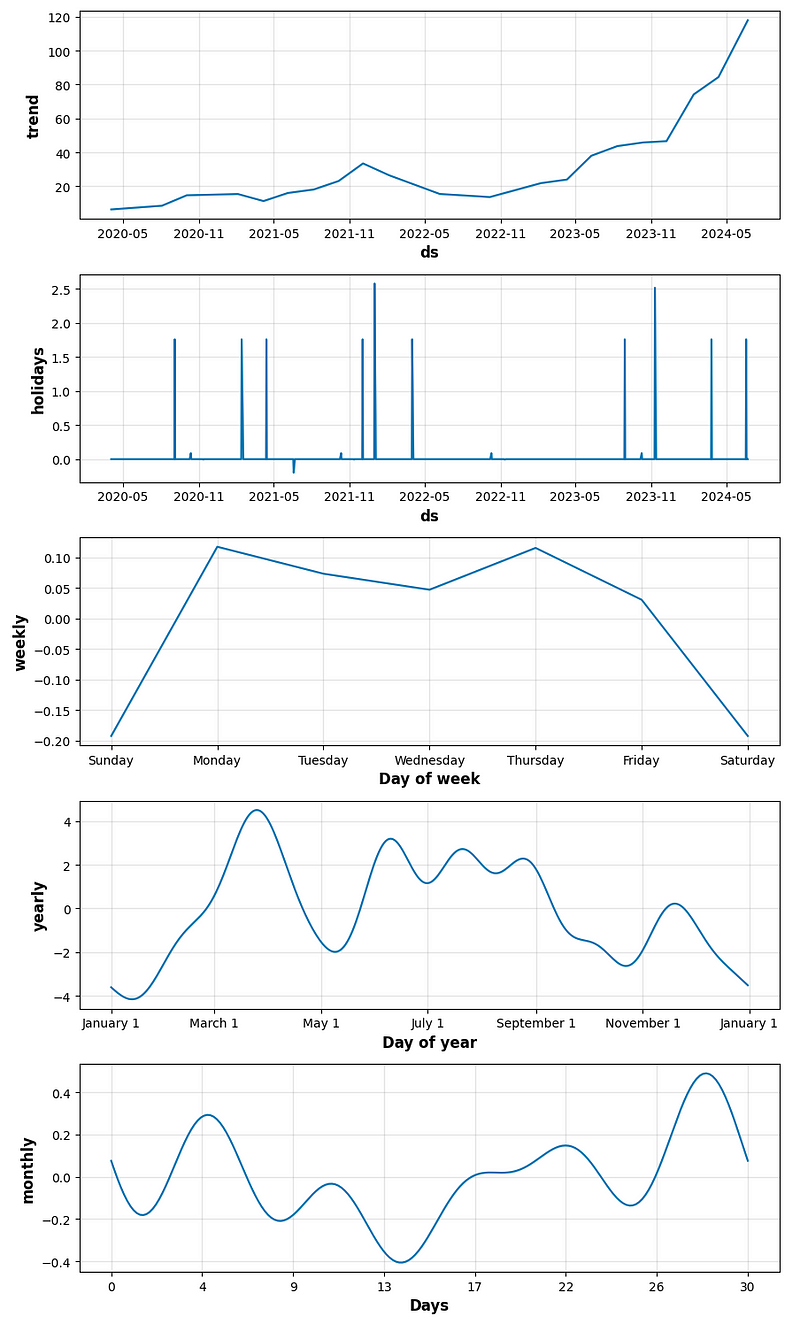

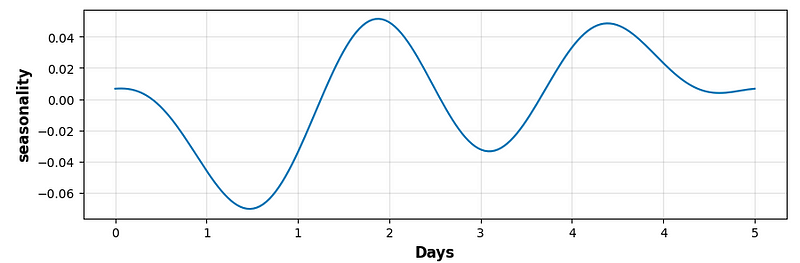

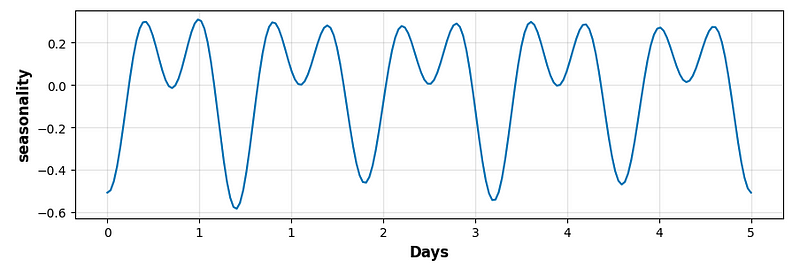

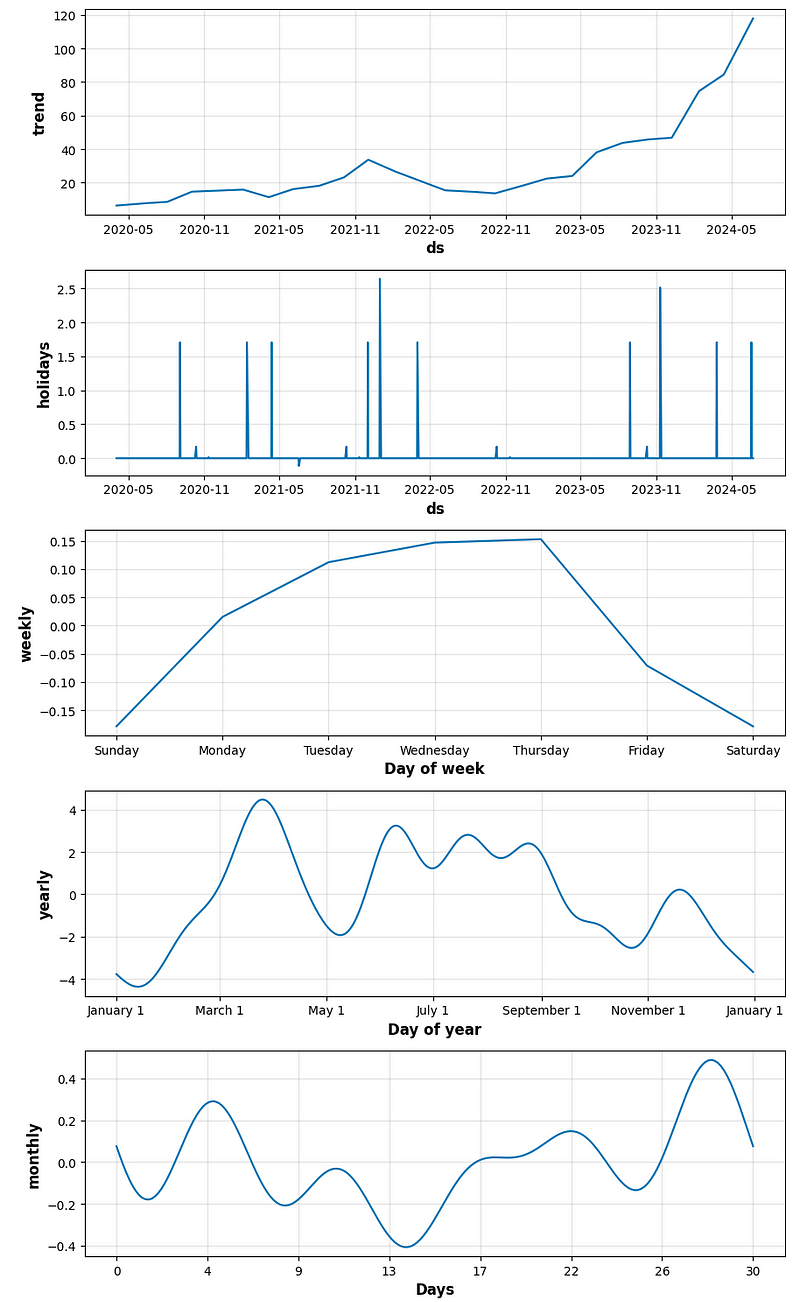

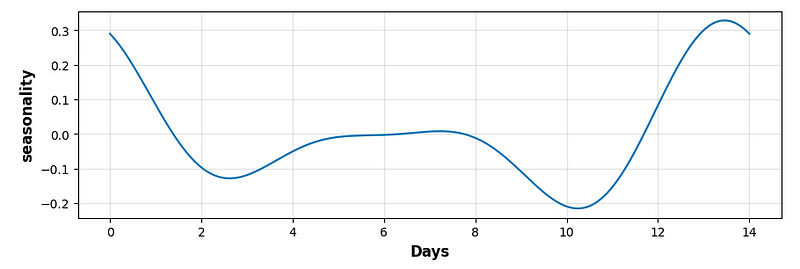

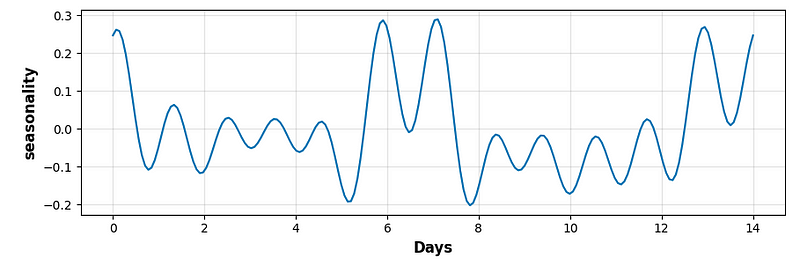

model.add_seasonality(name='seasonality', period=period_days,

fourier_order=fourier_order_seasonality,

mode = 'additive', prior_scale = 0.5)

model.add_seasonality(name='monthly', period=30.5, fourier_order=5)

model.add_country_holidays(country_name='US')

# Training model for df

model.fit(train)

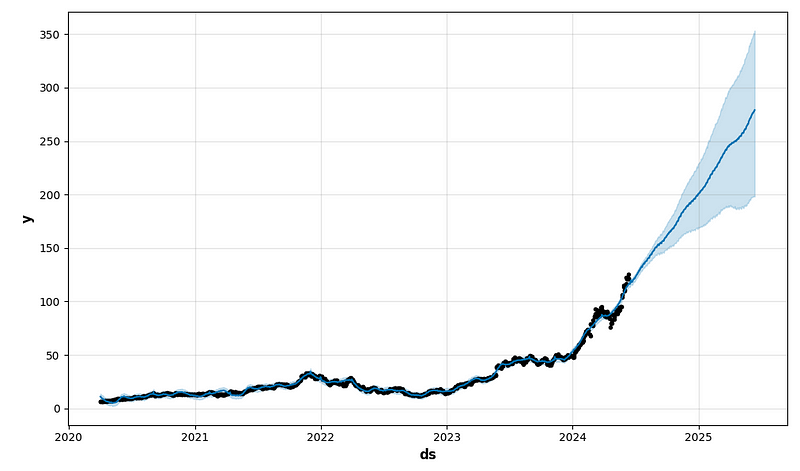

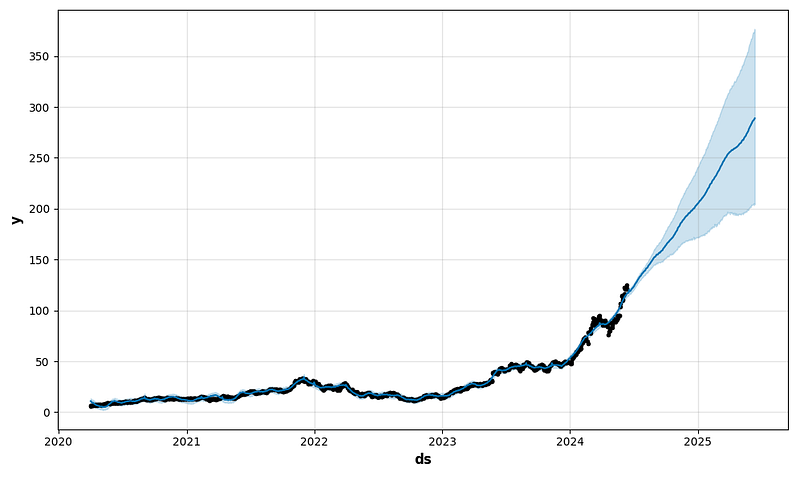

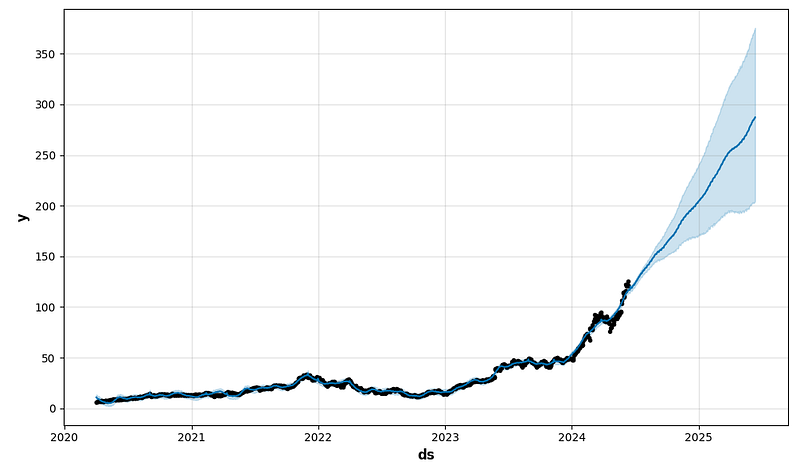

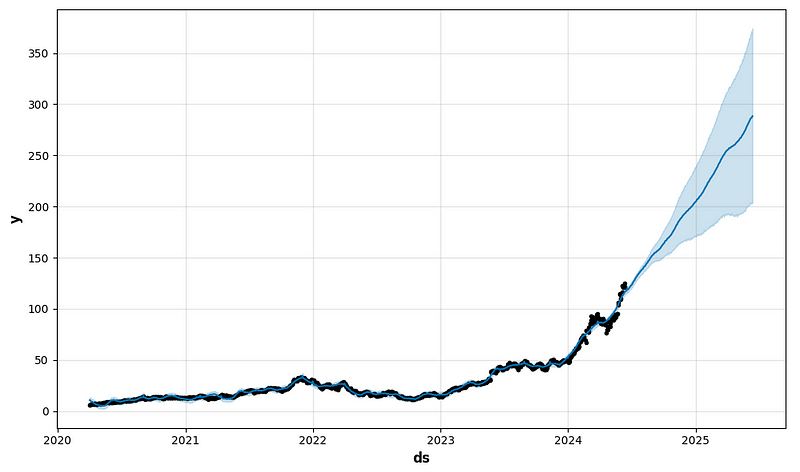

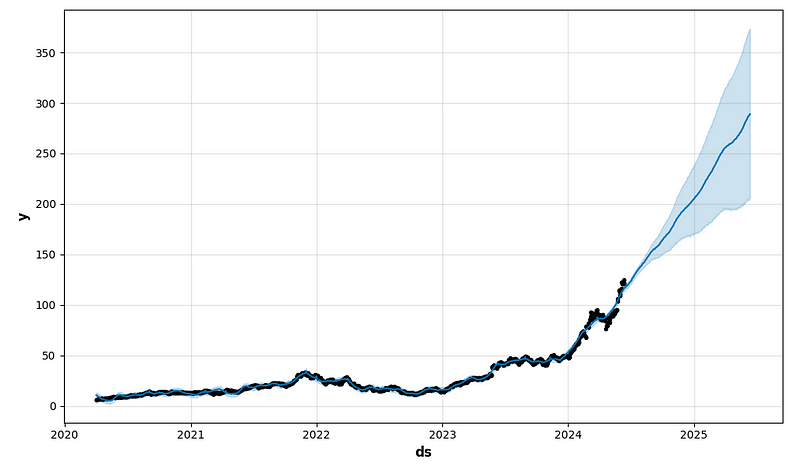

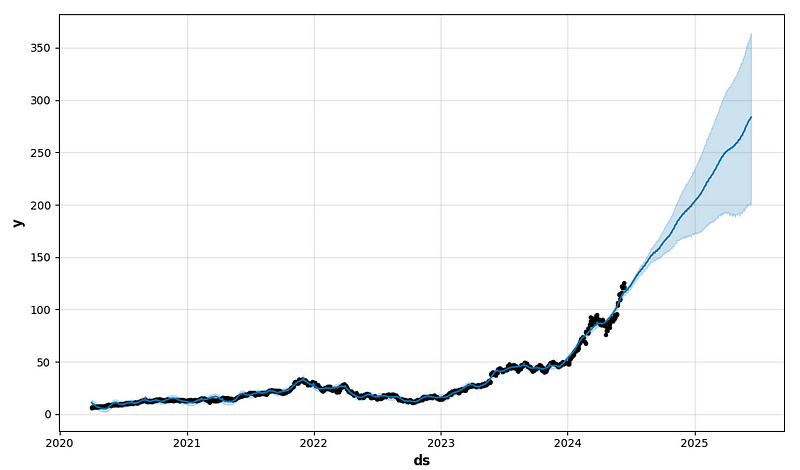

# Make a forecast

future = model.make_future_dataframe(periods = forecasting_period)

forecast = model.predict(future)

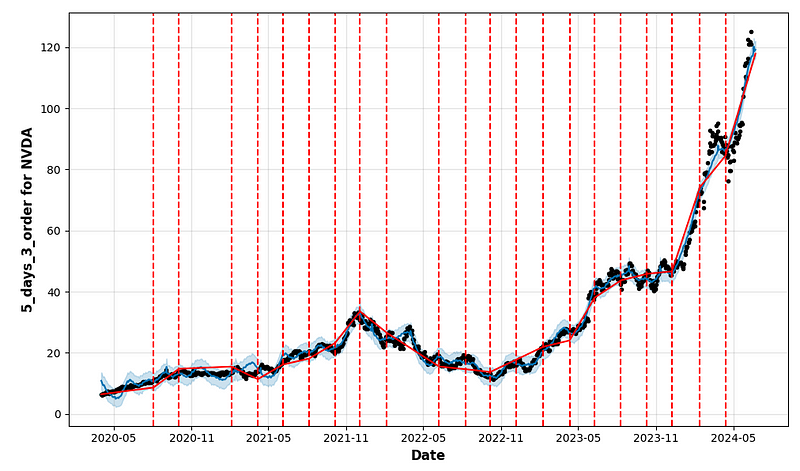

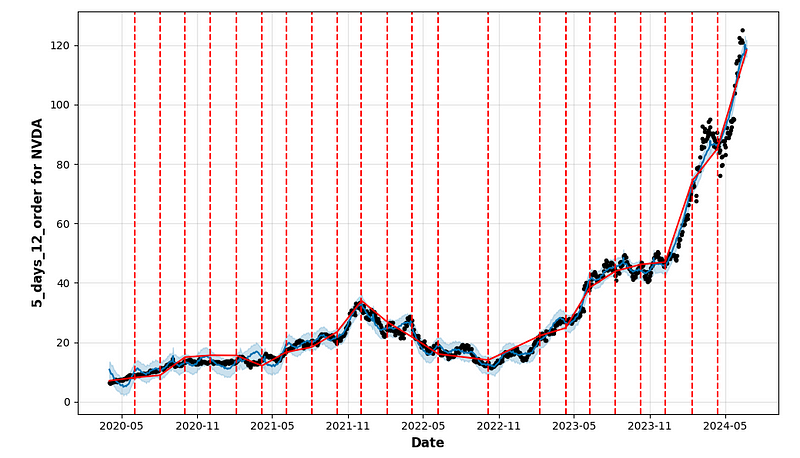

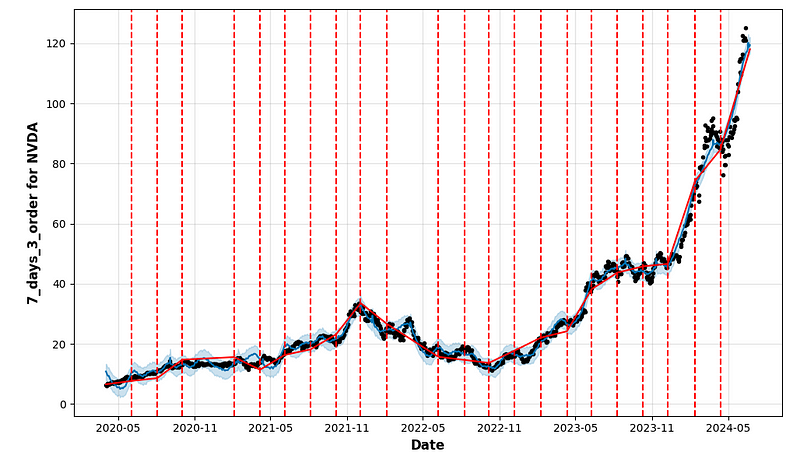

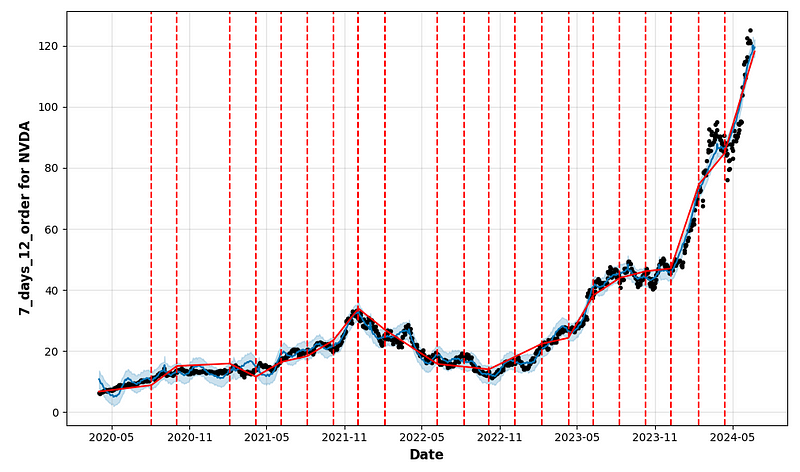

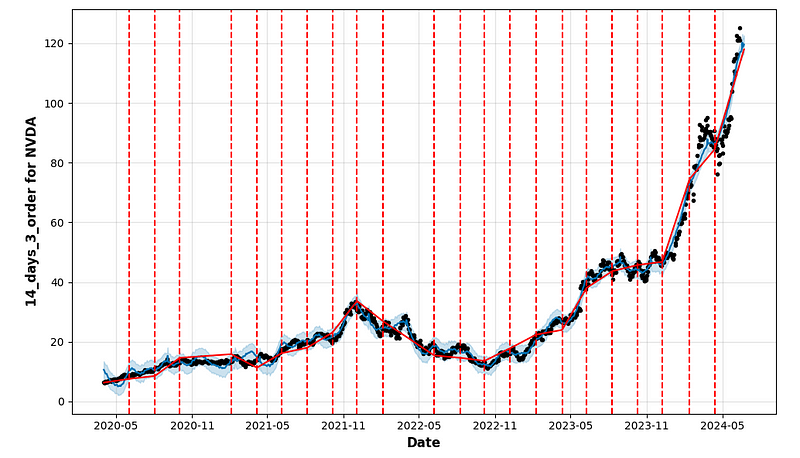

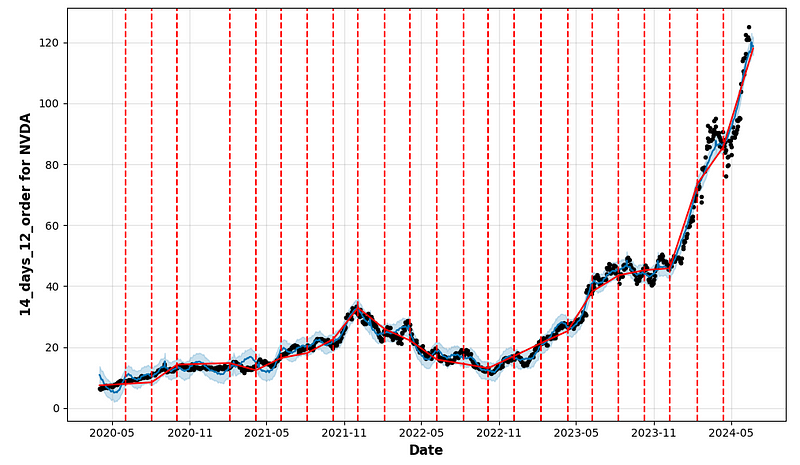

# Draw plot of the values with forecasting data

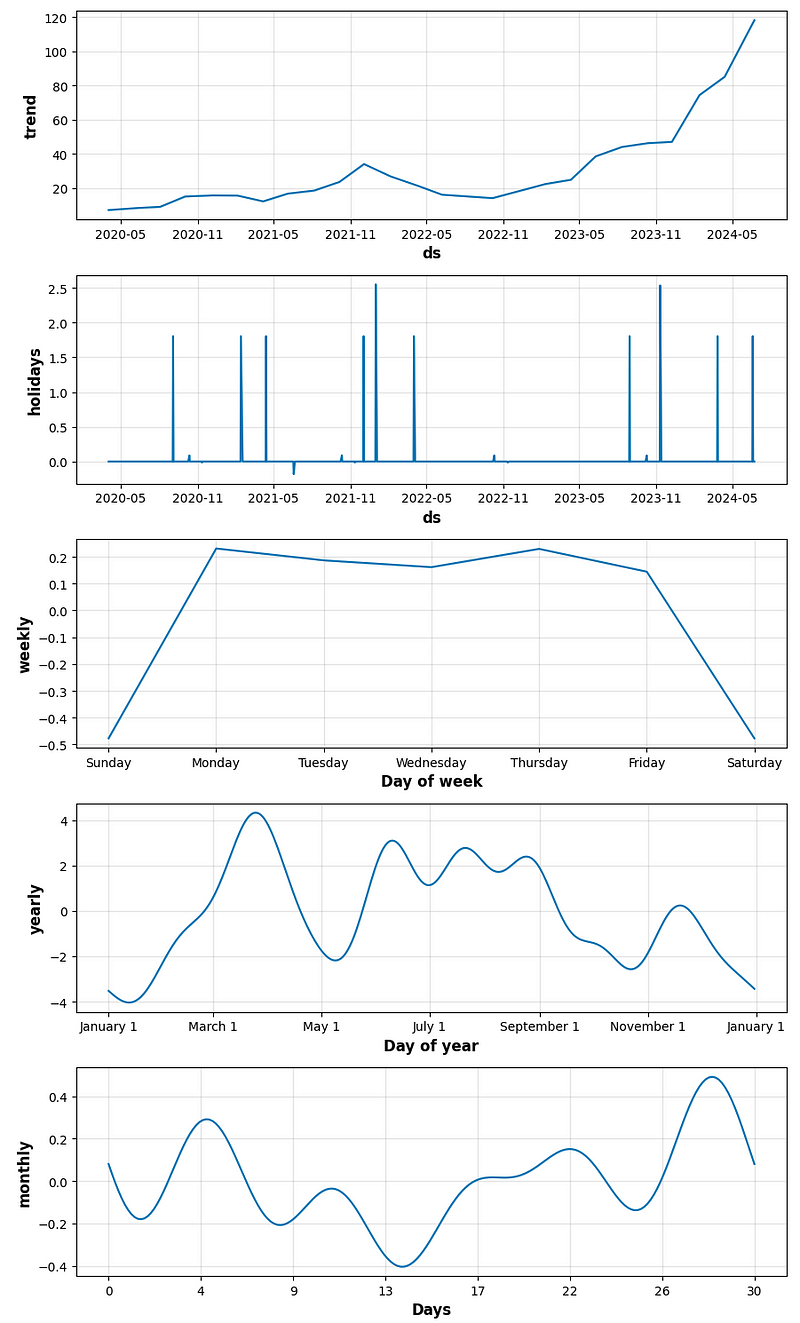

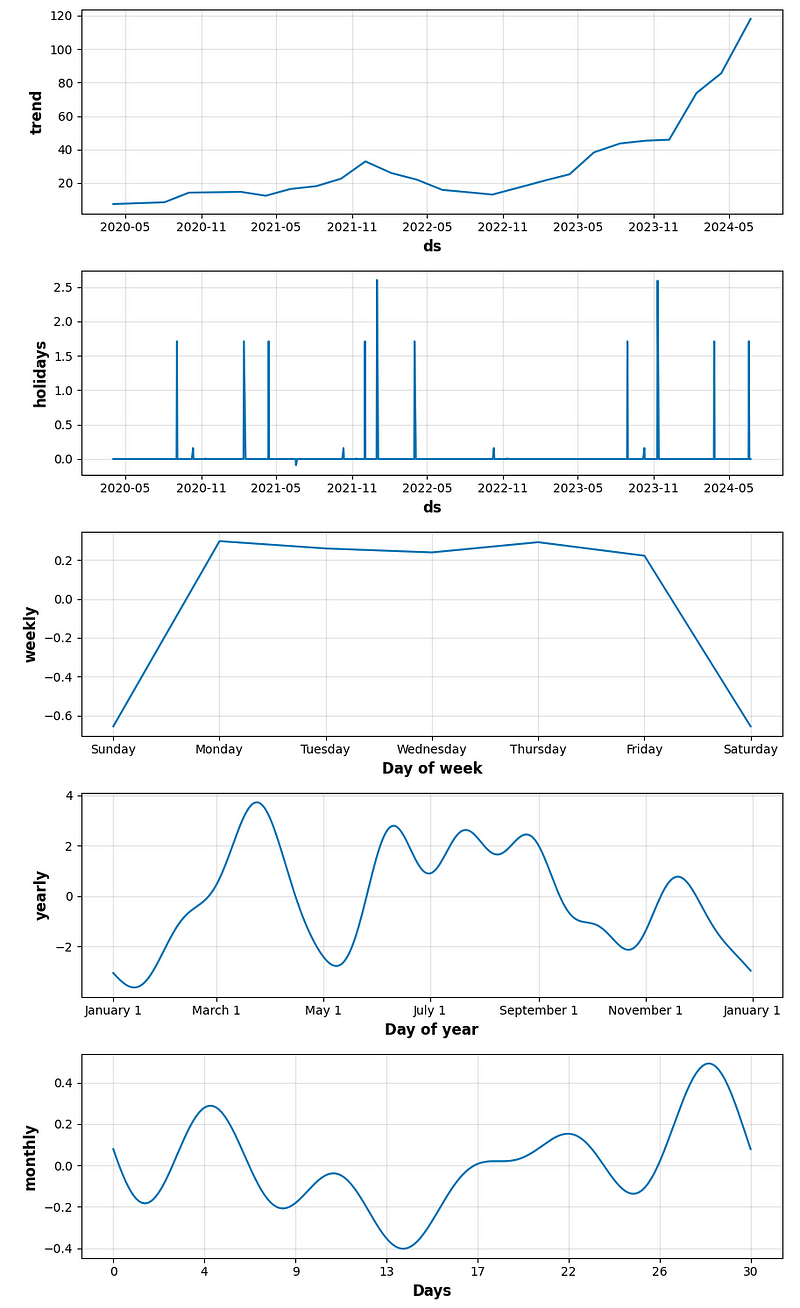

figure = model.plot(forecast, xlabel = 'Date', ylabel = f"{name_model} for {cryptocurrency}")

a = add_changepoints_to_plot(figure.gca(), model, forecast)

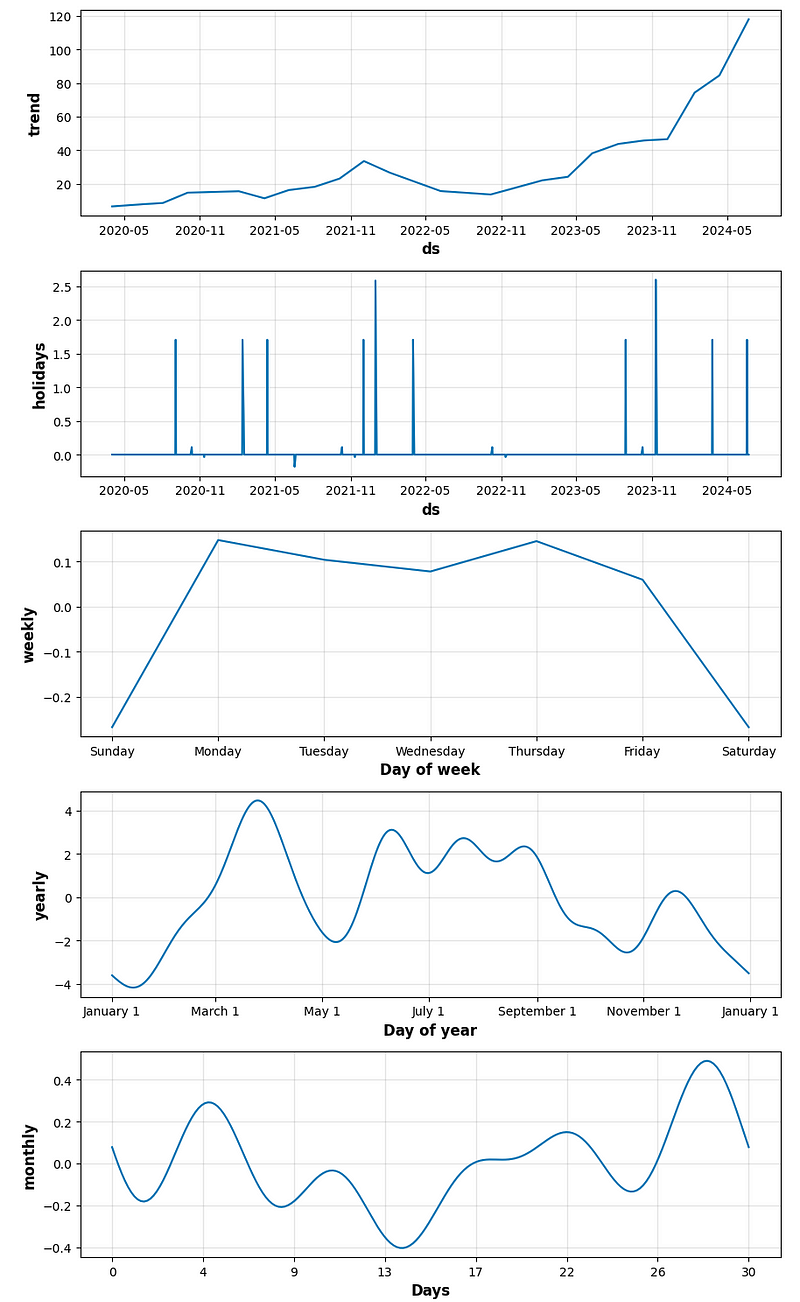

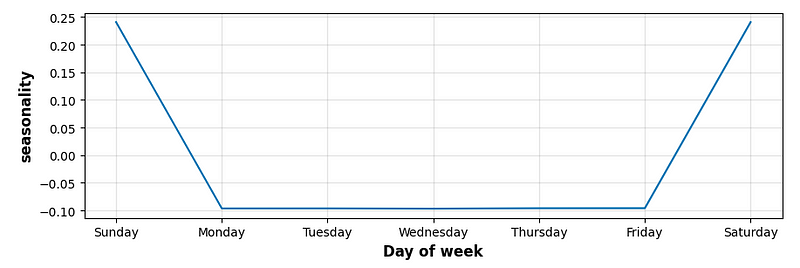

# Draw plot with the components (trend and seasonalities) of the forecasts

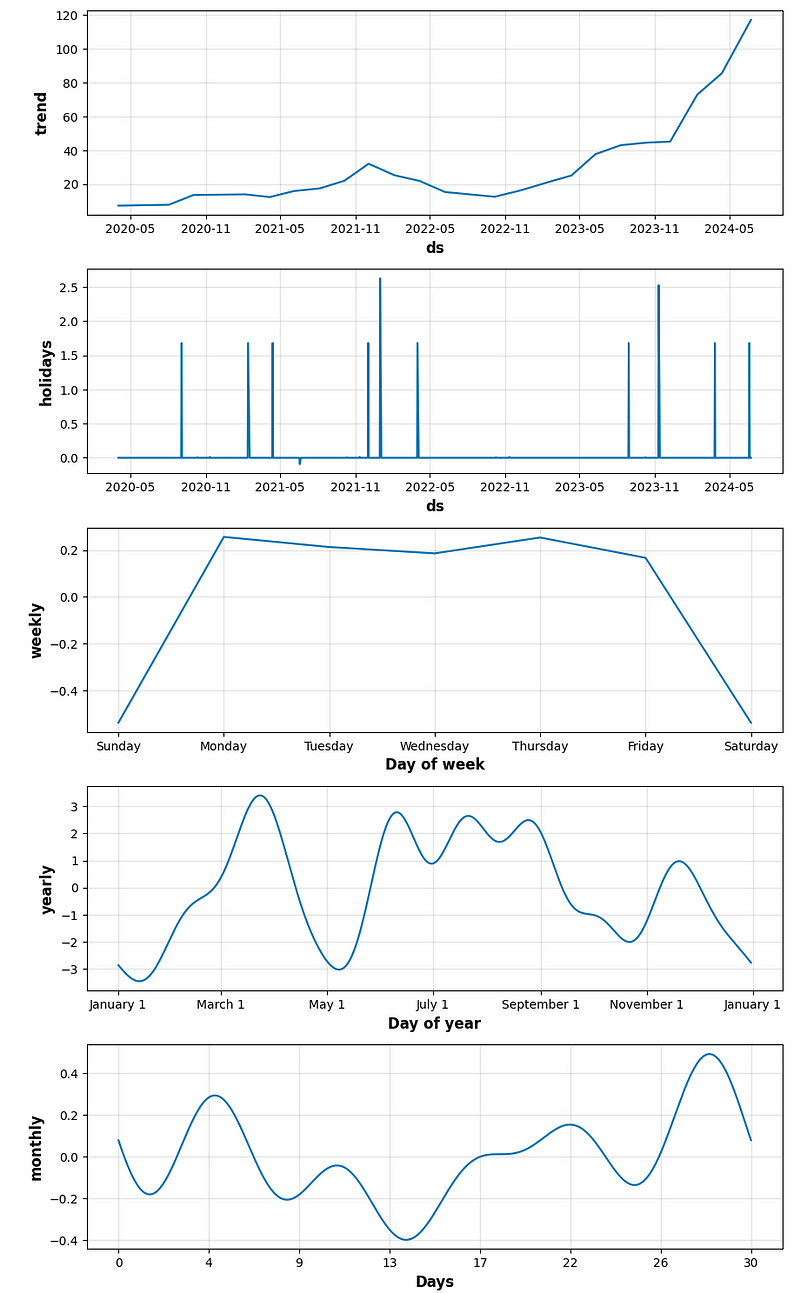

figure_component = model.plot_components(forecast)

# Ouput the prediction for the next time on forecasted_days

#forecast[['yhat_lower', 'yhat', 'yhat_upper']] = forecast[['yhat_lower', 'yhat', 'yhat_upper']].round(1)

#forecast[['ds', 'yhat_lower', 'yhat', 'yhat_upper']].tail(forecasting_period)

# Forecasting data by the model

ypred = forecast['yhat'][-forecasting_period:]

#print(ypred)

# Save results

n = len(result)

result.loc[n,'name_model'] = f"Prophet_{name_model}"

result.loc[n,'type_data'] = type_data

result.at[n,'params'] = [period_days]+[fourier_order_seasonality]

result.at[n,'ypred'] = ypred

#result = result_add_metrics(result, n, test['y'], y_pred)

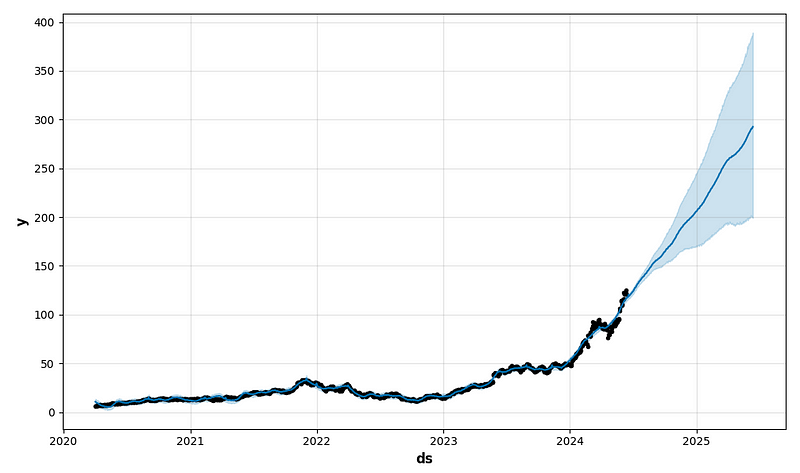

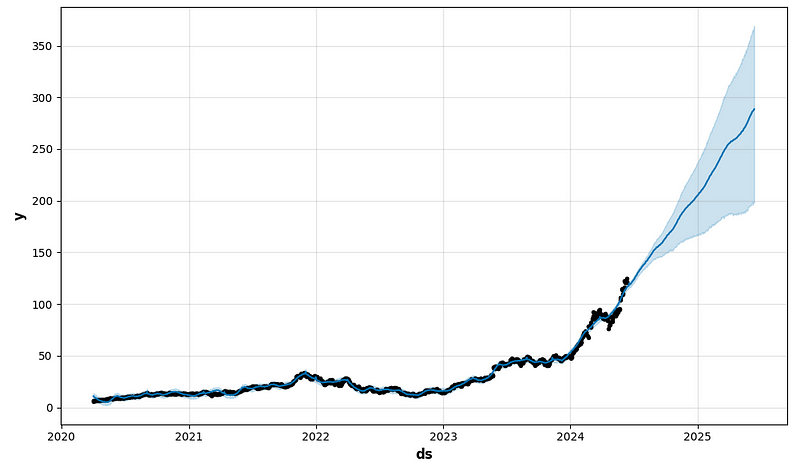

future1 = model.make_future_dataframe(periods=365)

forecast1 = model.predict(future1)

fig1 = model.plot(forecast1)

return result, ypred

# Models tuning

if is_Prophet:

for period_days in [4, 5, 7, 14]:

for fourier_order_seasonality in [3, 12]:

result, _ = prophet_modeling(result,

cryptocurrency,

train_ts,

valid_ts,

holidays_df,

period_days,

fourier_order_seasonality,

forecasting_days,

f'{period_days}_days_{fourier_order_seasonality}_order',

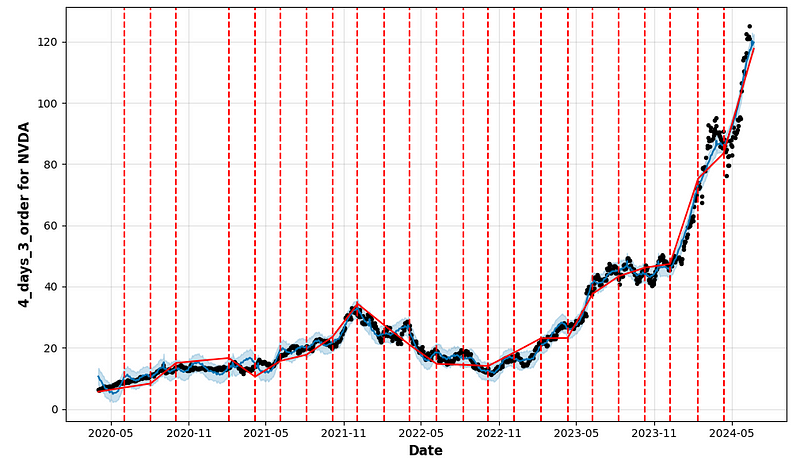

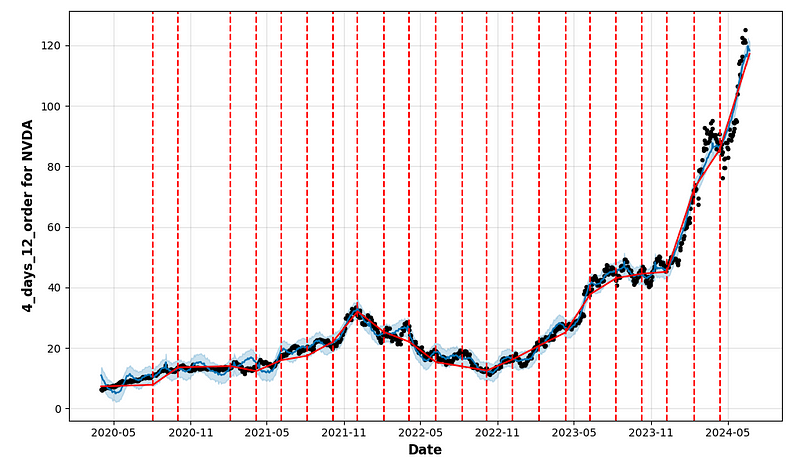

'valid')- Plotting the complete output of FB Prophet forecasting HPO

- period_days=4 & fourier_order_seasonality=3

- period_days=4 & fourier_order_seasonality=12

- period_days=5 & fourier_order_seasonality=3

- period_days=5 & fourier_order_seasonality=12

- period_days=7 & fourier_order_seasonality=3

- period_days=7 & fourier_order_seasonality=12

- period_days=14 & fourier_order_seasonality=3

- period_days=14 & fourier_order_seasonality=12

- Performing cross-validation QC

res1=result['ypred']

print(res1[1])

1056 116.936342

1057 116.850275

1058 116.233301

1059 116.709060

1060 117.953234

1061 119.812505

1062 118.262082

1063 118.641367

1064 118.779563

1065 118.254753

Name: yhat, dtype: float64

print(valid_ts)

ds y

1056 2024-06-13 129.610001

1057 2024-06-14 131.880005

1058 2024-06-17 130.979996

1059 2024-06-18 135.580002

1060 2024-06-20 130.779999

1061 2024-06-21 126.570000

1062 2024-06-24 118.110001

1063 2024-06-25 126.089996

1064 2024-06-26 126.400002

1065 2024-06-27 123.989998

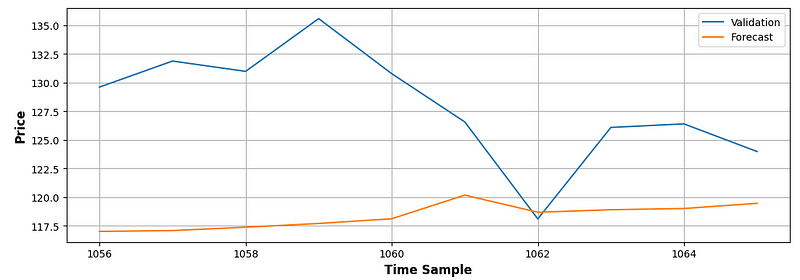

n=5

valid_ts['y'].plot(label='Validation')

res1[n].plot(label='Forecast')

plt.legend()

plt.xlabel('Time Sample')

plt.ylabel('Price')

plt.grid()

y_true=valid_ts['y']

y_pred=res1[5]

resr2 = calc_metrics('r2_score', y_true, y_pred)

resrmse = calc_metrics('rmse', y_true, y_pred) # in coins

resmape = 100*calc_metrics('mape', y_true, y_pred) # in %

print(resr2)

print(resrmse)

print(resmape)

-4.654220698172283

10.99633729407076

7.488504106783908

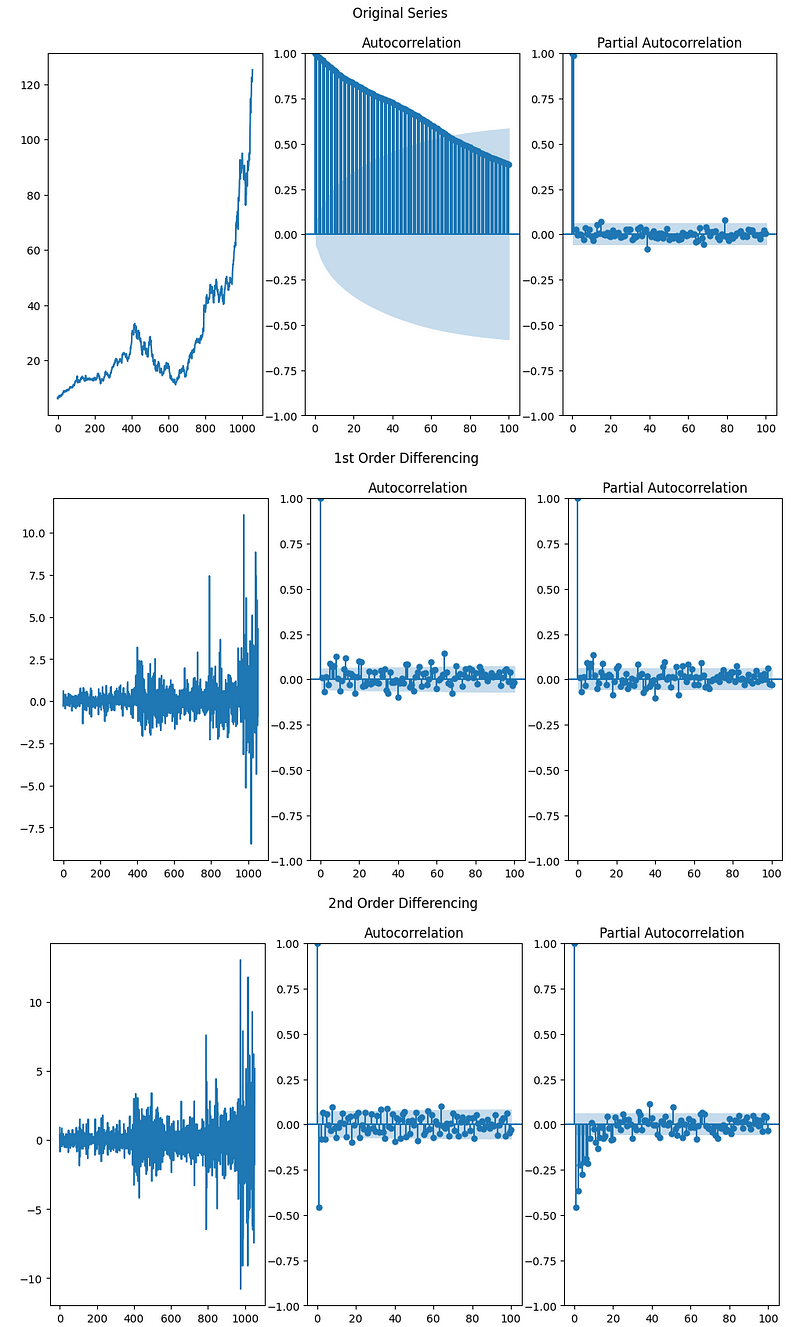

Auto-ARIMA Model Fitting

- This section is a demonstration on how to leverage Auto ARIMA functionality [1,5] using the pmdarima package to forecast the future NVDA stock price. The auto-ARIMA process seeks to identify the most optimal parameters for an ARIMA model, settling on a single fitted ARIMA model.

- Fetching and splitting the dataset

#ARIMA

# Get datasets

if is_ARIMA:

train_ts, valid_ts, test_ts, train_valid_ts = get_train_valid_test_ts(df2.copy(), forecasting_days, target='Close')

Origin dataset has 1076 rows and 2 features

Get training dataset with 1056 rows

Get validation dataset with 10 rows

Get test dataset with 10 rows- Calculating and plotting ACF/PACF for the original time series and first-, second-order time differences

if is_ARIMA:

# ACF and PACF

lag_num = 100

acf_pacf_draw(train_ts['y'], lag_num, True, True, 'Original Series')

acf_pacf_draw(train_ts['y'].diff().dropna(), lag_num, True, True, '1st Order Differencing')

acf_pacf_draw(train_ts['y'].diff().diff().dropna(), lag_num, True, True, '2nd Order Differencing')

- Implementing ARIMA model fitting and Auto-ARIMA HPO

def arima_fit(df, col, order=(1,1,1)):

# ARIMA model fitting for series df[col]

model = sm.tsa.arima.ARIMA(df[col].values.squeeze(), order=order)

model = model.fit()

return model

def get_residual_errors(model):

# Calculation and drawing the plot residual errors for ARIMA model

residuals = pd.DataFrame(model.resid)

fig, ax = plt.subplots(1,2, figsize=(12,6))

residuals.plot(title="Residuals", ax=ax[0])

residuals.plot(kind='kde', title='Density', ax=ax[1])

plt.show()

def arima_forecasting(result, model, params, name_model, df, type_data):

# Data df (validation or test) forecasting on the num days by the model

# with params and save metrics to result

ypred = model.forecast(steps=len(df))

n = len(result)

result.loc[n,'name_model'] = name_model

result.loc[n,'type_data'] = type_data

result.at[n,'params'] = params

result.at[n,'ypred'] = ypred

#result = result_add_metrics(result, n, df['y'], y_pred)

return result

if is_ARIMA:

# Automatic tuning of the ARIMA model

model_auto = pm.auto_arima(train_ts['y'].values,

start_p=4, # start p

start_q=4, # start q

test='adf', # use adftest to find optimal 'd'

max_p=5, max_q=5, # maximum p and q

m=1, # frequency of series (1 - No Seasonality)

d=None, # let model determine 'd'

seasonal=False, # No Seasonality

start_P=0,

D=0,

start_Q=0,

trace=True,

error_action='ignore',

suppress_warnings=False,

stepwise=True # use the stepwise algorithm outlined in Hyndman and Khandakar (2008)

# to identify the optimal model parameters.

# The stepwise algorithm can be significantly faster than fitting all

# hyper-parameter combinations and is less likely to over-fit the model

)

print(model_auto.summary())

Performing stepwise search to minimize aic

ARIMA(4,1,4)(0,0,0)[0] intercept : AIC=inf, Time=1.19 sec

ARIMA(0,1,0)(0,0,0)[0] intercept : AIC=3278.225, Time=0.01 sec

ARIMA(1,1,0)(0,0,0)[0] intercept : AIC=3280.157, Time=0.04 sec

ARIMA(0,1,1)(0,0,0)[0] intercept : AIC=3280.146, Time=0.04 sec

ARIMA(0,1,0)(0,0,0)[0] : AIC=3286.435, Time=0.01 sec

ARIMA(1,1,1)(0,0,0)[0] intercept : AIC=3274.481, Time=0.25 sec

ARIMA(2,1,1)(0,0,0)[0] intercept : AIC=3276.898, Time=0.17 sec

ARIMA(1,1,2)(0,0,0)[0] intercept : AIC=3276.272, Time=0.30 sec

ARIMA(0,1,2)(0,0,0)[0] intercept : AIC=3276.936, Time=0.06 sec

ARIMA(2,1,0)(0,0,0)[0] intercept : AIC=3277.302, Time=0.05 sec

ARIMA(2,1,2)(0,0,0)[0] intercept : AIC=3277.648, Time=0.34 sec

ARIMA(1,1,1)(0,0,0)[0] : AIC=3282.470, Time=0.14 sec

Best model: ARIMA(1,1,1)(0,0,0)[0] intercept

Total fit time: 2.629 seconds

SARIMAX Results

==============================================================================

Dep. Variable: y No. Observations: 1056

Model: SARIMAX(1, 1, 1) Log Likelihood -1633.240

Date: Wed, 17 Jul 2024 AIC 3274.481

Time: 14:06:03 BIC 3294.326

Sample: 0 HQIC 3282.003

- 1056

Covariance Type: opg

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

intercept 0.2192 0.076 2.876 0.004 0.070 0.369

ar.L1 -0.9472 0.020 -46.224 0.000 -0.987 -0.907

ma.L1 0.9748 0.016 59.838 0.000 0.943 1.007

sigma2 1.2946 0.020 64.815 0.000 1.255 1.334

===================================================================================

Ljung-Box (L1) (Q): 0.16 Jarque-Bera (JB): 16930.67

Prob(Q): 0.69 Prob(JB): 0.00

Heteroskedasticity (H): 23.15 Skew: 1.79

Prob(H) (two-sided): 0.00 Kurtosis: 22.30

===================================================================================- Getting orders of the best ARIMA model

if is_ARIMA:

# Get orders of the best model from AutoARIMA

arima_orders_best = list(model_auto.get_params().get('order'))

print(f"Optimal parameters are {arima_orders_best}")

model_auto = arima_fit(train_ts, 'y', order=(arima_orders_best[0],arima_orders_best[1],arima_orders_best[2]))

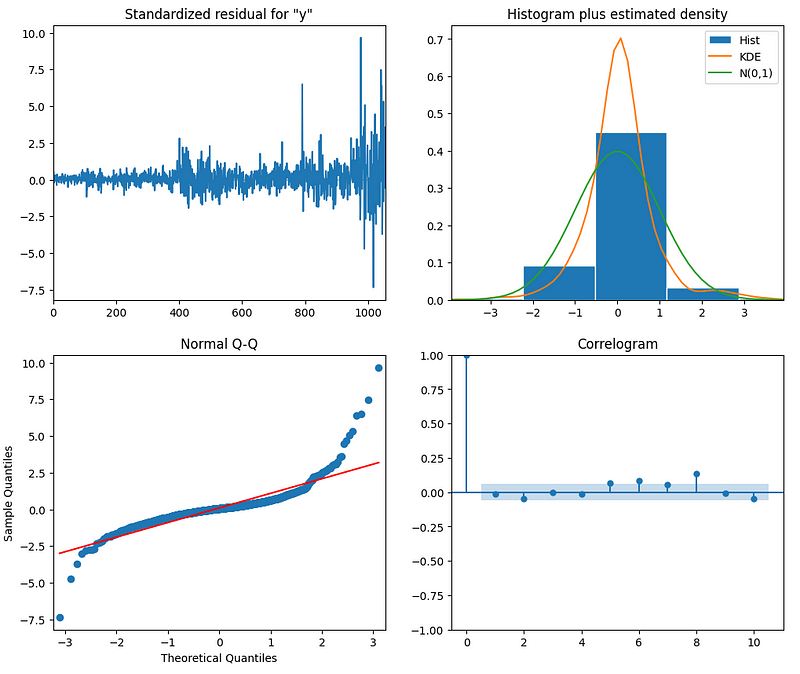

Optimal parameters are [1, 1, 1]- Plotting the Auto-ARIMA diagnostics summary

if is_ARIMA:

# Best model from AutoARIMA

fig = model_auto.plot_diagnostics(figsize=(12,10))

plt.show()

- Printing the final validation result

if is_ARIMA:

# Valid forecasting and save result

result = arima_forecasting(result, model_auto, arima_orders_best, 'ARIMA_auto', valid_ts, 'valid')

y_true=valid_ts['y']

y_pred=res1[0]

resr2 = calc_metrics('r2_score', y_true, y_pred)

resrmse = calc_metrics('rmse', y_true, y_pred) # in coins

resmape = 100*calc_metrics('mape', y_true, y_pred) # in %

print(resr2)

print(resrmse)

print(resmape)

-0.3756885596041244

5.424025684842693

3.472035737786662SciKit-Learn Supervised ML Regression & HPO

- Let’s train/test the popular supervised ML regression models and optimize their hyperparameters available in SciKit-Learn [1,4].

- Hyperparameters are parameters that are not directly learnt within estimators. In Scikit-Learn they are passed as arguments to the constructor of the estimator classes [4].

- Fetching and splitting the input dataset

if is_other_ML:

df2 = get_target_mf(df2, forecasting_days, col='Close')

train_mf, ytrain_mf, valid_mf, yvalid_mf, test_mf, ytest_mf, train_valid_mf, y_train_valid_mf, starting_point = \

get_train_valid_test_mf(df2.copy(), forecasting_days, target='target')

Origin dataset has 242 rows and 60 features

Get training dataset with 222 rows

Get validation dataset with 10 rows

Get test dataset with 10 rows- Defining the 8 supervised ML models with search hyperparameters

if is_other_ML:

# Set parameters of models

models = pd.DataFrame(columns = ['name', 'model', 'param_grid'])

# Linear Regression

n = len(models)

models.loc[n, 'name'] = 'Linear Regression'

models.at[n, 'model'] = LinearRegression()

models.at[n, 'param_grid'] = {'fit_intercept' : [True, False]}

# KNeighbors Regressor

n = len(models)

models.loc[n, 'name'] = 'KNeighbors Regressor'

models.at[n, 'model'] = KNeighborsRegressor()

models.at[n, 'param_grid'] = {'n_neighbors': [3, 5, 10, 20, 30],

'leaf_size': [10, 20, 30]

}

# Support Vector Machines

n = len(models)

models.loc[n, 'name'] = 'Support Vector Machines'

models.at[n, 'model'] = SVR()

models.at[n, 'param_grid'] = {'kernel': ['linear', 'poly', 'rbf', 'sigmoid'],

'C': np.linspace(1, 15, 15),

'tol': [1e-3, 1e-4]

}

# Linear SVC

n = len(models)

models.loc[n, 'name'] = 'Linear SVR'

models.at[n, 'model'] = LinearSVR()

models.at[n, 'param_grid'] = {'C': np.linspace(1, 15, 15)}

# Random Forest Classifier

n = len(models)

models.loc[n, 'name'] = 'Random Forest Regressor'

models.at[n, 'model'] = RandomForestRegressor()

models.at[n, 'param_grid'] = {'n_estimators': [40, 50, 60, 80],

'min_samples_split': [30, 40, 50, 60],

'min_samples_leaf': [10, 12, 15, 20, 50],

'max_features': [100],

'max_depth': [3, 4, 5, 6]

}

# Bagging Classifier

n = len(models)

models.loc[n, 'name'] = 'Bagging Regressor'

models.at[n, 'model'] = BaggingRegressor()

models.at[n, 'param_grid'] = {'max_features': np.linspace(0.05, 0.8, 1),

'n_estimators': [3, 4, 5, 6],

'warm_start' : [False]

}

# XGB Classifier

n = len(models)

models.loc[n, 'name'] = 'XGB Regressor'

models.at[n, 'model'] = xgb.XGBRegressor()

models.at[n, 'param_grid'] = {'n_estimators': [50, 70, 90],

'learning_rate': [0.01, 0.05, 0.1, 0.2],

'max_depth': [3, 4, 5]

}

# MLP Classifier

n = len(models)

models.loc[n, 'name'] = 'MLP Regressor'

models.at[n, 'model'] = MLPRegressor()

models.at[n, 'param_grid'] = {'hidden_layer_sizes': [i for i in range(2,5)],

'solver': ['lbfgs', 'sgd'],

'learning_rate': ['adaptive'],

'learning_rate_init': [0.001, 0.01],

'max_iter': [1000]

}

models

- Tuning the above ML models

def model_prediction(result, models, train_features, valid_features, train_labels, valid_labels):

# Models training and data prediction for all models from DataFrame models

# Saving results for validation dataset into dataframe result

def calc_add_score(res, n, type_score, list_true, list_pred, feature_end):

# Calculation score with type=type_score for list_true and list_pred

# Adding score into res.loc[n,...]

res.loc[i, type_score + feature_end] = calc_metrics(type_score, list_true, list_pred)

return res

# Results

model_all = []

for i in range(len(models)):

# Training

print(f"Tuning model '{models.loc[i, 'name']}'")

model = GridSearchCV(models.at[i, 'model'], models.at[i, 'param_grid'])

model.fit(train_features, train_labels)

model_all.append(model)

print(f"Best parameters: {model.best_params_}\n")

# Prediction

ypred = model.predict(valid_features)

# Scoring and saving results into the main dataframe result

n = len(result)

result.loc[n,'name_model'] = f"{models.loc[i, 'name']}"

result.loc[n,'type_data'] = "valid"

result.at[n,'params'] = model.best_params_

result.at[n,'ypred'] = ypred

#result = result_add_metrics(result, n, valid_labels, valid_pred)

return result, model_all

if is_other_ML:

# Models tuning and the forecasting

result, model_all = model_prediction(result, models, train_mf, valid_mf, ytrain_mf, yvalid_mf)

Tuning model 'Linear Regression'

Best parameters: {'fit_intercept': False}

Tuning model 'KNeighbors Regressor'

Best parameters: {'leaf_size': 10, 'n_neighbors': 30}

Tuning model 'Support Vector Machines'

Best parameters: {'C': 1.0, 'kernel': 'rbf', 'tol': 0.0001}

Tuning model 'Linear SVR'

Best parameters: {'C': 3.0}

Tuning model 'Random Forest Regressor'

Best parameters: {'max_depth': 6, 'max_features': 100, 'min_samples_leaf': 15, 'min_samples_split': 40, 'n_estimators': 40}

Tuning model 'Bagging Regressor'

Best parameters: {'max_features': 0.05, 'n_estimators': 6, 'warm_start': False}

Tuning model 'XGB Regressor'

Best parameters: {'learning_rate': 0.1, 'max_depth': 5, 'n_estimators': 70}

Tuning model 'MLP Regressor'

Best parameters: {'hidden_layer_sizes': 4, 'learning_rate': 'adaptive', 'learning_rate_init': 0.01, 'max_iter': 1000, 'solver': 's- Validating the optimized ML models and computing their r2_score, rmse, and mape [1]

def recovery_prediction(y, starting_point):

# Recovering prediction of multi-factors model for shifted col_diff to col in the dataframe df

# y has type np.array

# starting_point is dictionary with start values for the recovering data

# Returns y (np.array) with recovering data

return np.insert(y, 0, starting_point).cumsum()[1:]

def result_recover_and_metrics(result, df_ts, type_data, start_points):

# Recovering prediction: from shifted_Close_diff to Close

# Calculation metrics for recovering ypred forecasting for all models in result

# ypred real is from df_ts['y']

# start points value for the recovering is from dictionary start_points

# type_data = 'valid' or 'test'

for i in range(len(result)):

if (result.loc[i, 'type_data']==type_data) and (result.loc[i, 'mape'] is np.nan):

ypred = result.loc[i, 'ypred']

# Recovering ypred for multi-factors models

if not (str(result.loc[i, 'type_model']) in ['Prophet', 'ARIMA']):

# Multi-factors model

# Get start points value for the recovering

start_point_value = start_points['valid_start_point'] if type_data=='valid' else start_points['test_start_point']

# Recovering prediction

ypred = recovery_prediction(ypred, start_point_value)

# Calculation metrics

result = result_add_metrics(result, i, df_ts['y'], ypred)

return result

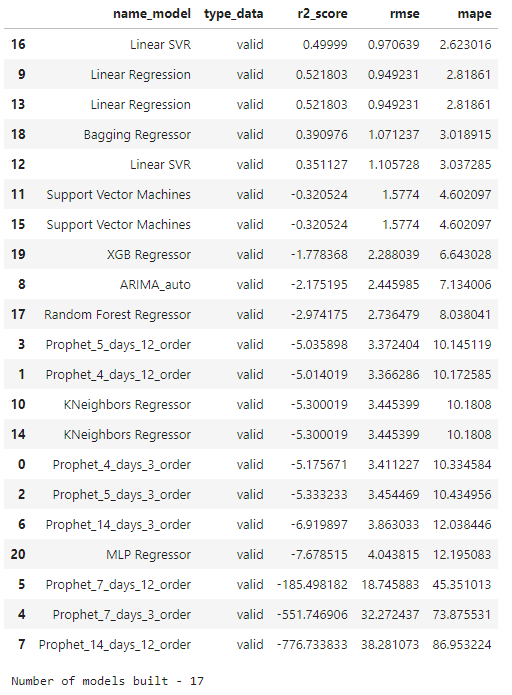

# Dispay and save all results for validation dataset

if len(result) > 0:

# Get type of each model

result['type_model'] = result['name_model'].str.split('_').str[0]

# Calculation metrics for recovering prediction ypred for validation dataset by all models

result = result_recover_and_metrics(result, valid_ts, 'valid', starting_point)

display(result[['name_model', 'type_data', 'r2_score', 'rmse', 'mape']].sort_values(by=['type_data', 'mape', 'rmse'], ascending=True))

# Save results

num_models = len(result[result['type_data']=='valid']['name_model'].unique().tolist())

print(f"Number of models built - {num_models}")

result.to_csv(f'result_of_{num_models}_models_for_forecasting_days_{forecasting_days}.csv')

else:

print('There are no tuned models!')

- Optimized ML model training and forecasting [1]

def get_model_opt(name_model, params):

# Model tuning for the name_model

print(name_model)

if name_model=='Linear Regression':

model = LinearRegression(**params)

elif name_model=='KNeighbors Regressor':

model = KNeighborsRegressor(**params)

elif name_model=='Support Vector Machines':

model = SVR(**params)

elif name_model=='Linear SVR':

model = LinearSVR(**params)

elif name_model=='Random Forest Regressor':

model = RandomForestRegressor(**params)

elif name_model=='Bagging Regressor':

model = BaggingRegressor(**params)

elif name_model=='MLP Regressor':

model = MLPRegressor(**params)

elif name_model=='XGB Regressor':

model = xgb.XGBRegressor(**params)

else: model = None

return model

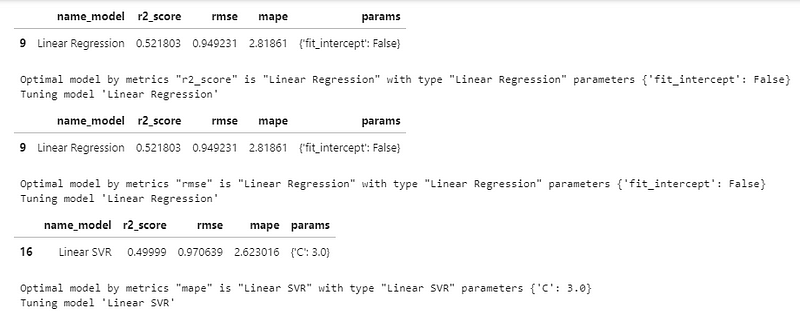

def get_params_optimal_model(result, main_metrics):

# Get parameters of the optimal model from dataframe result by main_metrics

# Set the data type to float (just in case)

result[main_metrics] = result[main_metrics].astype('float')

# Choose the optimal model

opt_result = result[result['type_data']=='valid'].reset_index(drop=True)

if main_metrics=='r2_score':

opt_model = opt_result.nlargest(1, main_metrics)

else:

# 'mape' or 'rmse'

opt_model = opt_result.nsmallest(1, main_metrics)

display(opt_model[['name_model', 'r2_score', 'rmse', 'mape', 'params']])

# Get parameters of the optimal model

opt_name_model = opt_model['name_model'].tolist()[0]

opt_type_model = opt_model['type_model'].tolist()[0]

opt_params_model = opt_model['params'].tolist()[0]

print(f'Optimal model by metrics "{main_metrics}" is "{opt_name_model}" with type "{opt_type_model}" parameters {opt_params_model}')

return opt_name_model, opt_type_model, opt_params_model

def model_training_forecasting(result, df, y, test, ytest,

name_model, type_model, params, type_test='1'):

# Model training for df and y

# Forecasting ypred

# type_model = 'Prophet' or "ARIMA" or 'Other ML'

# type_test = '1' (with find optimal parameters by GridSearchCV)

# type_test = '2' (with optimal parameters - without GridSearchCV)

# return params and metrics in the dataframe result

if type_model=='Prophet':

season_days_optimal = params[0]

fourier_order_seasonality_optimal = params[1]

model_opt = None

_, ypred = prophet_modeling(result,

cryptocurrency,

df,

test,

holidays_df,

season_days_optimal,

fourier_order_seasonality_optimal,

forecasting_days,

f'{type_model}_optimal',

'test')

elif type_model=='ARIMA':

season_days_optimal = params[0]

fourier_order_seasonality_optimal = params[1]

model_opt = None

# Training ARIMA optimal model for training+valid dataset

df['y'] = y

model_opt = arima_fit(df, 'y', order=(params[0],params[1],params[2]))

# Model diagnostics

fig = model_opt.plot_diagnostics(figsize=(12,10))

plt.show()

# Plot residual errors

get_residual_errors(model_opt)

# Test forecasting and save result

ypred = model_opt.forecast(steps=len(test))

else:

# Other ML model

# Training ML optimal model for training+valid dataset

print(f"Tuning model '{name_model}'")

models_opt_number = models[models['name']==name_model].index.tolist()[0]

#print(f"Model - {models.at[models_opt_number,'model']} with parameters {params}")

if type_test=='1':

model_opt = GridSearchCV(models.at[models_opt_number,'model'], models.at[models_opt_number,'param_grid'])

else:

# type_test=='2'

model_opt = get_model_opt(models.at[models_opt_number,'name'], params)

model_opt.fit(df, y)

# Forecasting

ypred = model_opt.predict(test)

# Scoring and saving results into the dataframe result

n = len(result)-1

result.loc[n,'name_model'] = f"{type_model}_optimal"

result.loc[n,'type_data'] = "test"

result.loc[n,'type_model'] = type_model

result.at[n,'params'] = params

result.at[n,'ypred'] = ypred

#result = result_add_metrics(result, n, ytest, ypred)

return result, model_opt, ypred

def get_optimal_model_and_forecasting(result, main_metrics, start_points):

# Choosion the optimal model from dataframe result by main_metrics

# Tuning optimal model for big dataset train+valid

# Test forecasting and drawing it

# Returns the optimal model and it's name

if len(result) > 0:

# Get parameters of the optimal model from dataframe result by main_metrics

opt_name_model, opt_type_model, opt_params_model = get_params_optimal_model(result,

main_metrics)

# Set datasets for the final tuning and testing by optimal model

if (opt_type_model=='Prophet') or (opt_type_model=='ARIMA'):

train_valid = train_valid_ts.copy()

y_train_valid = train_valid_ts['y'].copy()

test = test_ts.copy()

ytest = test_ts['y'].copy()

else:

# Multi-factors ML models

train_valid = train_valid_mf.copy()

y_train_valid = y_train_valid_mf.copy()

test = test_mf.copy()

ytest = ytest_mf.copy()

# Optimal model training for train+valid and test forecasting

result, model_opt, ypred = model_training_forecasting(result, train_valid, y_train_valid,

test, ytest,

opt_name_model, opt_type_model,

opt_params_model, '1')

# Calculation metrics for recovering prediction ypred for test dataset by the optimal model

result = result_recover_and_metrics(result, test_ts, 'test', start_points)

# Drawing plot for prediction for the test data

if not ((opt_type_model=='Prophet') or (opt_type_model=='ARIMA')):

# Recovery values "Close"

ytest_plot = recovery_prediction(ytest.values, start_points['test_start_point'])

ypred_plot = recovery_prediction(ypred, start_points['test_start_point'])

else:

ytest_plot = ytest.copy()

ypred_plot = ypred.copy()

# Drawing

plt.figure(figsize=(12,8))

x = np.arange(len(ytest_plot))

plt.scatter(x, ytest_plot, label = "Target test data", color = 'g', s=100)

plt.scatter(x, ypred_plot, label = f"{opt_name_model} forecasting", color = 'r', s=50)

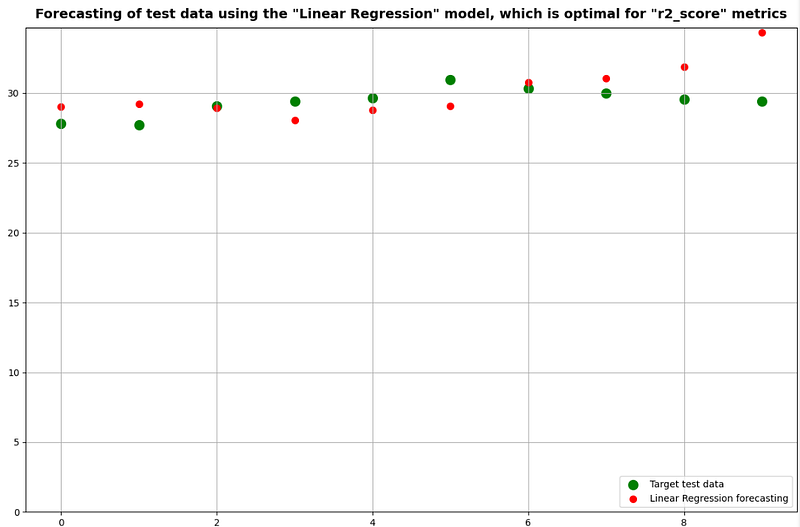

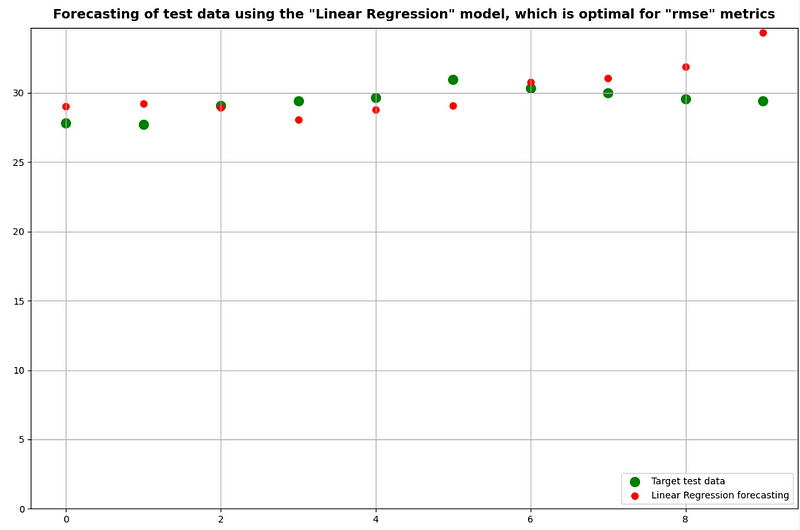

plt.title(f'Forecasting of test data using the "{opt_name_model}" model, which is optimal for "{main_metrics}" metrics')

plt.ylim(0)

plt.legend(loc='lower right')

plt.grid(True)

return opt_name_model

# Get the optimal model by different metrics

if len(result) > 0:

for valid_metrics in ['r2_score', 'rmse', 'mape']:

get_optimal_model_and_forecasting(result, valid_metrics, starting_point)

- Getting the best Linear Regression model

if is_other_ML:

main_metrics = 'r2_score'

if (len(result) > 0) and (len(models) > 0):

result_nonTS = result[(result['type_model']!='Prophet') & (result['type_model']!='ARIMA')].reset_index(drop=True)

opt_name_model2, opt_type_model2, opt_params_model2 = get_params_optimal_model(result_nonTS,

main_metrics)

result, model_opt, ypred = model_training_forecasting(result,

train_valid_mf,

y_train_valid_mf,

test_mf,

ytest_mf,

opt_name_model2,

opt_type_model2,

opt_params_model2,

'2')

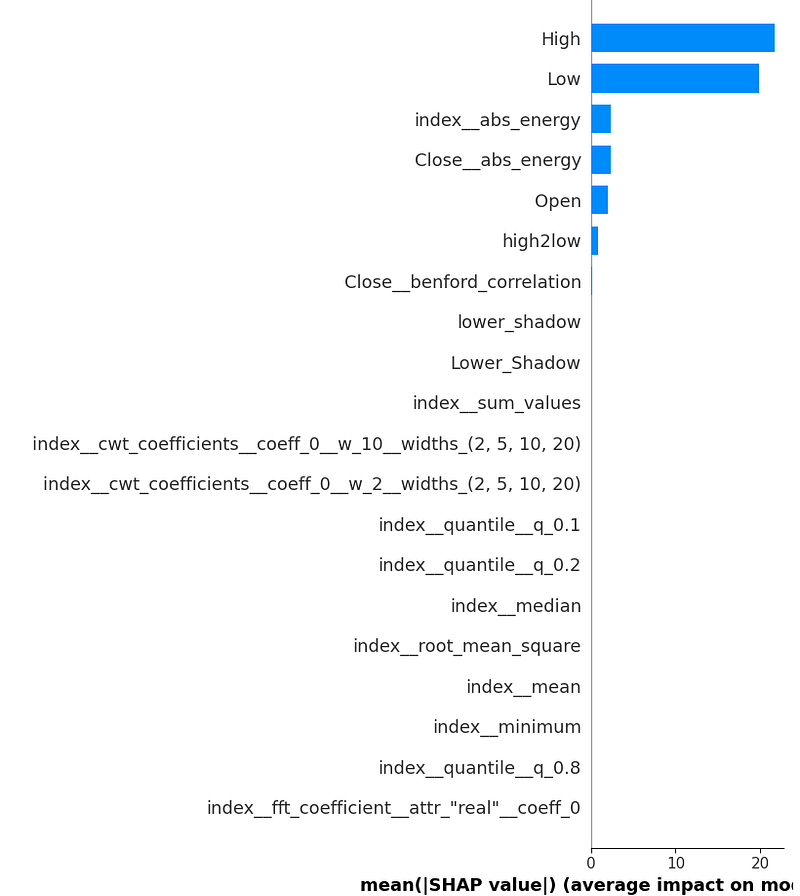

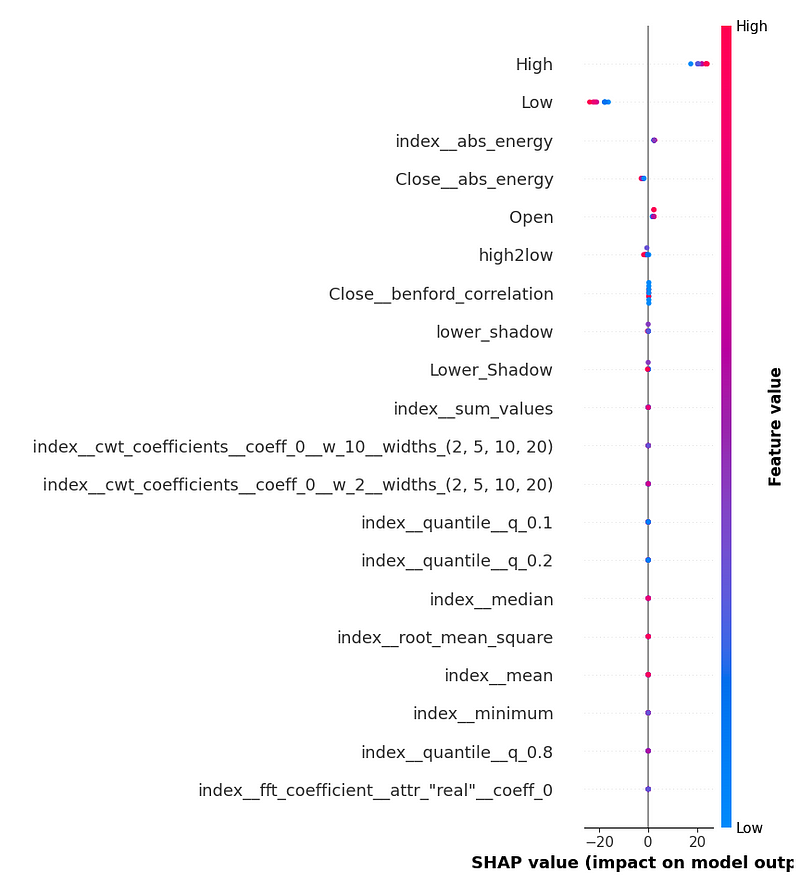

SHAP Feature Dominance Analysis

- Let’s use the SHAP package to calculate feature importance [1, 6]. The most common way of understanding ML models is to examine the coefficients learned for each feature.

- Plotting the feature importance diagrams with SHAP [1]

# All features names

if is_other_ML:

coeff = pd.DataFrame(train_valid_mf.columns)

coeff.columns = ['feature']

def add_fi_coeff(coeff, col, list_new_fi_coeff=None, df_new_fi_coeff=None):

# Adds new importance of features as feature col

# from list list_new_fi_coeff or dataframe df_new_fi_coeff

# to the resulting dataframe coeff with feature names

# Missed importance values are replaced by zero

if list_new_fi_coeff is not None:

df_new_fi_coeff = coeff[['feature']].copy()

df_new_fi_coeff["score"] = pd.Series(list_new_fi_coeff)

if df_new_fi_coeff is not None:

# Rename df_new_fi_coeff

df_new_fi_coeff.columns = ['feature', 'score'] # to the plot drawing

df_new_fi_coeff[col] = df_new_fi_coeff['score'] # to the merging and saving

# Merging dataframes - coeff of all features with new_fi_coeff

coeff = coeff.merge(df_new_fi_coeff[['feature', col]], on='feature', how='left').fillna(0)

is_score = True

else:

print(f'Data is absent fol {col}')

is_score = False

coeff = None

return coeff, df_new_fi_coeff, is_score

# Feature importance diagram with SHAP

if is_other_ML:

if (len(result) > 0) and (len(models) > 0):

print('Feature importance diagram with SHAP:')

try:

# Trees

explainer = shap.TreeExplainer(model_opt)

shap_values = explainer.shap_values(test_mf)

shap.summary_plot(shap_values, test_mf, plot_type="bar", feature_names=coeff['feature'].tolist())

shap.summary_plot(shap_values, test_mf)

# Save permutation feature importance values

coeff, _, is_SHAP_successfully = add_fi_coeff(coeff, 'shap_fi_score', shap_values)

except:

try:

# Other types of models

explainer = shap.KernelExplainer(model_opt.predict, train_valid_mf)

shap_values = explainer.shap_values(test_mf)

# Plot drawing

shap.summary_plot(shap_values, test_mf, plot_type="bar", feature_names=coeff['feature'].tolist())

shap.summary_plot(shap_values, test_mf)

# Get feature importance values from shap_values format

# Thanks to https://stackoverflow.com/a/69523421/12301574

shap_values_all = pd.DataFrame(shap_values, columns = test_mf.columns)

vals = np.abs(shap_values_all.values).mean(0)

shap_importance = pd.DataFrame(list(zip(test_mf.columns, vals)),

columns=['feature','score'])

# Saving feature importance values

coeff, _, is_SHAP_successfully = add_fi_coeff(coeff, 'shap_fi_score', None, shap_importance)

except:

is_SHAP_successfully = False

if not is_SHAP_successfully:

print('Feature importance diagram for this optimal model is not supported in SHAP')

- Creating the Feature importance diagram as the Force plot with SHAP

LSTM Prediction & Validation QC

- LSTMs are an improved version of recurrent neural networks (RNNs).

- Here, we demonstrate how the LSTM algorithm [7] can be used to predict NVDA stock prices by training on historical data.

- Importing the relevant Python libraries and reading the stock data

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

sns.set_style('whitegrid')

plt.style.use("fivethirtyeight")

%matplotlib inline

# For reading stock data from yahoo

from pandas_datareader.data import DataReader

# For time stamps

from datetime import datetime

from math import sqrt

from math import sqrt

from sklearn.metrics import mean_squared_error

from sklearn.preprocessing import MinMaxScaler

#ignore the warnings

import warnings

warnings.filterwarnings('ignore')

from keras.models import Sequential

from keras.layers import Dense, LSTM

import tensorflow as tf

#!pip install keras

#!pip install tensorflow

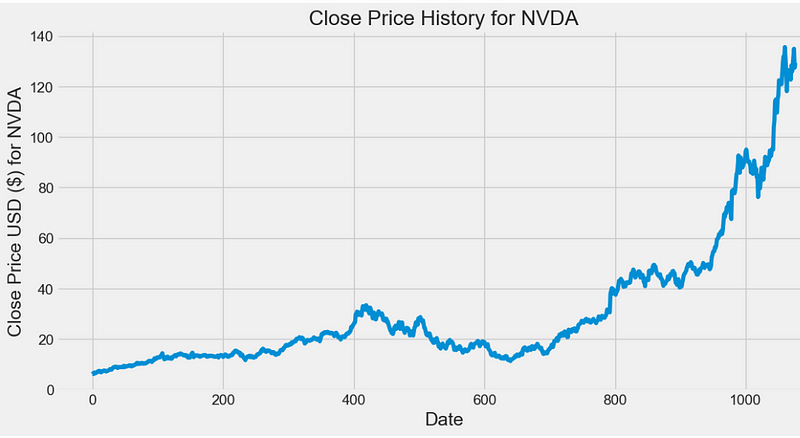

def plot_close_val(data_frame, column, stock):

plt.figure(figsize=(12,6))

plt.title(column + ' Price History for ' + stock )

plt.plot(data_frame[column])

plt.xlabel('Date', fontsize=18)

plt.ylabel(column + ' Price USD ($) for ' + stock, fontsize=18)

plt.show()

#Test the function

plot_close_val(df, 'Close', 'NVDA')

- Preparing the input data for LSTM model training

def build_training_dataset(input_ds):

# Create a new dataframe with only the 'Close column

input_ds.reset_index()

data = input_ds.filter(items=['Close'])

# Convert the dataframe to a numpy array

dataset = data.values

# Get the number of rows to train the model on

training_data_len = int(np.ceil( len(dataset) * .90 ))

return data, dataset, training_data_len

#Test the function

training_data_df, training_dataset_np, training_data_len = build_training_dataset(df)

dataset=training_dataset_np

data=training_data_df

# Scale the data

from sklearn.preprocessing import MinMaxScaler

def scale_the_data(dataset):

scaler = MinMaxScaler(feature_range=(0,1))

scaled_data = scaler.fit_transform(dataset)

return scaler, scaled_data

#Test the function

scaler, scaled_data = scale_the_data(training_dataset_np)

# Create the training data set

# Create the scaled training data set

def split_train_dataset(training_data_len):

train_data = scaled_data[0:int(training_data_len), :]

# Split the data into x_train and y_train data sets

x_train = []

y_train = []

for i in range(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])

if i<= 61:

#print(x_train)

#print(y_train)

print('.')

# Convert the x_train and y_train to numpy arrays

x_train, y_train = np.array(x_train), np.array(y_train)

# Reshape the data

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

# x_train.shape

return x_train, y_train

#Test the function

x_train,y_train = split_train_dataset(training_data_len)- Building the LSTM model

def build_lstm_model(x_train,y_train):

# Build the LSTM model

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

# Compile the model

model.compile(optimizer='adam', loss='mean_squared_error')

#model.compile(optimizer='lion', loss='mean_squared_error')

#model.compile(optimizer='adamw', loss='mean_squared_error')

# Train the model

model.fit(x_train, y_train, batch_size=2, epochs=10)

return model

#Test the function

lstm_model = build_lstm_model(x_train,y_train)

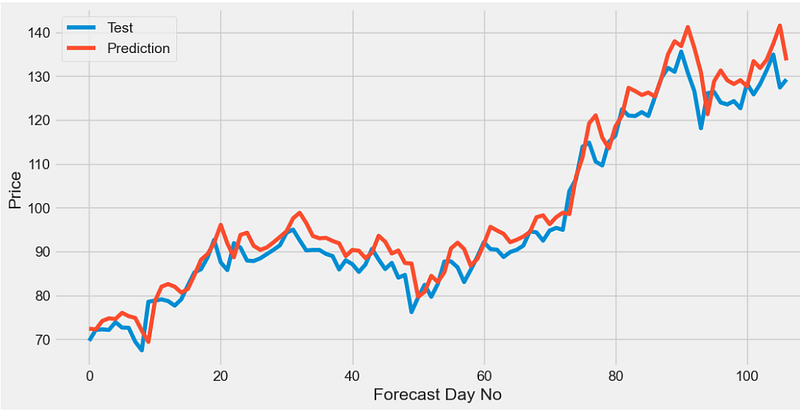

- Making test data predictions with TEST_DATA_LENGTH = 100

def create_testing_data_set(model, scaler, training_data_len,test_data_len):

# Create the testing data set

#

test_data = scaled_data[training_data_len - test_data_len: , :]

# Create the data sets x_test and y_test

x_test = []

y_test = dataset[training_data_len:, :]

for i in range(test_data_len, len(test_data)):

x_test.append(test_data[i-test_data_len:i, 0])

# Convert the data to a numpy array

x_test = np.array(x_test)

# Reshape the data

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1 ))

# Get the models predicted price values

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

# Get the root mean squared error (RMSE)

rmse = np.sqrt(np.mean(((predictions - y_test) ** 2)))

print(rmse)

return (x_test, y_test, predictions, rmse)

#Test the function

TEST_DATA_LENGTH = 100

x_test,y_test, predictions, rmse = create_testing_data_set(lstm_model,scaler,training_data_len, TEST_DATA_LENGTH)

4.706425009397595- Comparing test data vs LSTM predictions

plt.figure(figsize=(12,6))

plt.plot(y_test,label='Test')

plt.plot(predictions,label='Prediction')

plt.xlabel('Forecast Day No')

plt.ylabel('Price')

plt.legend()

- Comparing validation data vs LSTM predictions

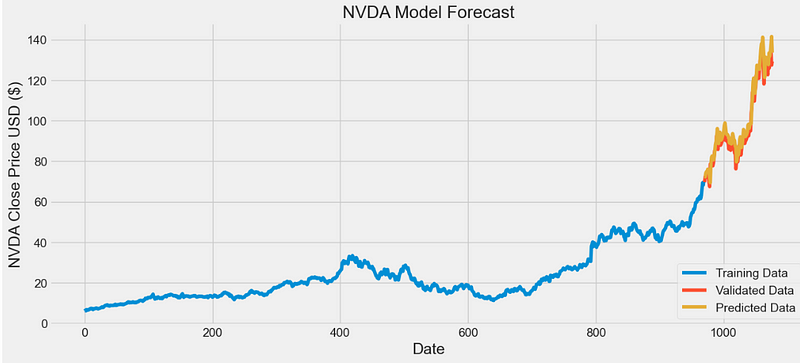

def plot_predictions(stock, data,training_data_len):

#Plot the data

train = data[:training_data_len]

valid = data[training_data_len:]

valid['Predictions'] = predictions

# Visualize the data

plt.figure(figsize=(14,6))

title = stock + ' Model Forecast'

ylabel = stock + ' Close Price USD ($)'

plt.title(title)

plt.xlabel('Date', fontsize=18)

plt.ylabel(ylabel, fontsize=18)

plt.plot(train['Close'])

plt.plot(valid[['Close', 'Predictions']])

plt.legend(['Training Data', 'Validated Data', 'Predicted Data'], loc='lower right')

plt.show()

return valid

#Test the function

valid = plot_predictions('NVDA',data,training_data_len)

- Calculating the LSTM error metrics

from sklearn.metrics import r2_score

r2_score(y_test, predictions)

0.9375826947059053

from sklearn.metrics import root_mean_squared_error

root_mean_squared_error(y_test, predictions)

4.706425009397595

from sklearn.metrics import mean_absolute_error

mean_absolute_error(y_test, predictions)

3.7365759733681365

from sklearn.metrics import mean_absolute_percentage_error

mean_absolute_percentage_error(y_test, predictions)

0.03859417843438189

from sklearn.metrics import explained_variance_score

explained_variance_score(y_test, predictions)

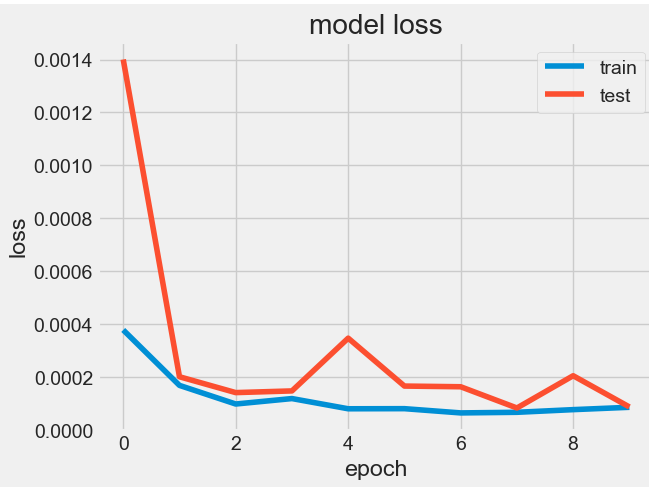

0.9638450129795046- Plotting the LSTM model loss vs epochs for both train and test data

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

# Compile the model

model.compile(optimizer='adam', loss='mean_squared_error',metrics=['accuracy'])

#model.compile(optimizer='lion', loss='mean_squared_error')

#model.compile(optimizer='adamw', loss='mean_squared_error')

# Train the model

history=model.fit(x_train, y_train, batch_size=2, epochs=10,validation_split=0.5)

# summarize history for loss

plt.plot(history.history['loss'])

plt.plot(history.history['val_loss'])

plt.title('model loss')

plt.ylabel('loss')

plt.xlabel('epoch')

plt.legend(['train', 'test'], loc='upper right')

plt.show()

Conclusions

- In this article, we have applied the the concept of algorithmic trading to the NVIDIA Short-Term Stock Price Forecasting.

- We’ve walked through the following topics:

- Exploratory Data Analysis (EDA) of Input Stock Data

- Basic Linear Regression with Time-Step & Lag Features

- TSFRESH Feature Engineering [1]

- Multi-Seasonal FB Prophet Prediction & HPO

- Auto-ARIMA Model Fitting & SARIMAX QC Summary

- SciKit-Learn Supervised ML Regression & HPO

- SHAP Feature Dominance Analysis

- TF LSTM Keras Prediction & Validation QC

- We have shown that time series forecasting (predicting future values based on historical values) applies well to NVIDIA stock forecasting.

- Since stock prices prediction is essentially a regression problem, the R2-Score, RMSE, MAE, and MAPE have been our key model evaluation metrics.

- Using the LSTM algorithm [7] and the basic Linear Regression [2] of 10-day Lags, our results showed that the forecasting model has a high accuracy of >95% for most of the stock data used, demonstrating the appropriateness of the ML model and the test set data is used to evaluate the model’s performance.

- Our ongoing efforts focus on addressing the following challenges:

- Market Uncertainty: Financial markets can be highly unpredictable, making accurate predictions challenging.

- External Factors: Models may not account for sudden geopolitical events or economic shifts.

- Overfitting: Models may perform well on historical data but struggle with new, unforeseen patterns.

Acknowledgements

- The main code of this notebook was written or compiled from many notebooks by Kaggle Grandmaster, Dr. Eng. Sc., Prof. Vitalii Mokin.

References

- Crypto — BTC : Analysis & Forecasting

- Linear Regression With Time Series

- NVIDIA Stock Price Prediction

- SciKit-Learn Supervised Learning

- Forecasting Time Series with Auto-Arima

- Explaining individual predictions when features are dependent: More accurate approximations to Shapley values

- NASDAQ Stock Price Prediction using LSTM

Explore More

- An Integrated Quant Trading Analysis of US Big Techs using Quantstats, TA, PyPortfolioOpt, and FinanceToolkit

- NVDA Technical Analysis using 75 Simplified FinTA Indicators

- Backtesting Hull Moving Average (HMA) Algo-Trading: NVDA Price vs Volume Buy/Sell Signals & Expected Returns

- NVIDIA Returns-Drawdowns MVA & RNN Mean Reversal Trading

- NVIDIA Rolling Volatility: GARCH & XGBoost

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Returns-Volatility Domain K-Means Clustering and LSTM Anomaly Detection of S&P 500 Stocks

Contacts

Disclaimer

- The following disclaimer clarifies that the information provided in this article is for educational use only and should not be considered financial or investment advice.

- The information provided does not take into account your individual financial situation, objectives, or risk tolerance.

- Any investment decisions or actions you undertake are solely your responsibility.

- You should independently evaluate the suitability of any investment based on your financial objectives, risk tolerance, and investment timeframe.

- It is recommended to seek advice from a certified financial professional who can provide personalized guidance tailored to your specific needs.

- The tools, data, content, and information offered are impersonal and not customized to meet the investment needs of any individual. As such, the tools, data, content, and information are provided solely for informational and educational purposes only.