This content discusses a strategy for predicting JPM stock prices using a combination of autoregressive, Fourier, and deep learning models, along with technical indicators, for robust stock price prediction and backtesting.

Abstract

The content focuses on a holistic strategy for predicting JPM stock prices using a combination of autoregressive, Fourier, and deep learning models, along with technical indicators. The approach aims to integrate predictive analytics and technical indicators into a single decision-making framework for detecting and predicting financial asset price breakouts and trends. The ultimate goal is to apply financial risk management to stock trading and investments, maximizing ROI while minimizing the likelihood of losing money on investment decisions. The content also discusses the use of SaaS products to automate trading and generate profits at a speed and frequency unattainable for human traders.

Opinions

The content emphasizes the importance of integrating predictive analytics and technical indicators into a single decision-making framework for stock price prediction and backtesting.

The authors believe that a combination of autoregressive, Fourier, and deep learning models, along with technical indicators, can provide a more robust and accurate prediction of stock prices.

The authors argue that the use of SaaS products to automate trading can generate profits at a speed and frequency unattainable for human traders.

The authors suggest that the ultimate goal of algorithmic trading is to apply financial risk management to stock trading and investments, maximizing ROI while minimizing the likelihood of losing money on investment decisions.

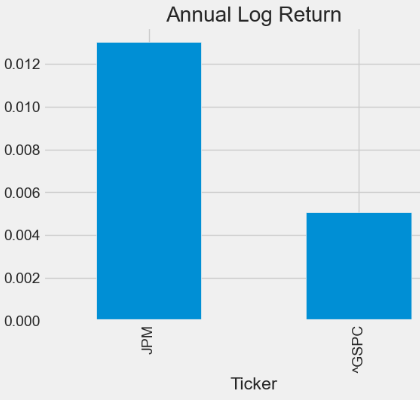

The authors highlight the importance of calculating and comparing risk-adjusted returns, beta, annual volatility, and standard deviation against the S&P 500 benchmark to maximize the (ROI/Risk) ratio.

The authors predict that the key trends, case examples, and best industry practices will accelerate the algorithmic trading market growth in the near future.

The authors suggest that factors such as the increasing adoption of ML/AI, real-time data analytics, interactive visualizations, and the rising demand for automated trading systems substantiate the current rapid algorithmic trading industry growth in North America, Europe, and Asia.

Combining ARIMA, LSTM and Fourier Models with Technical Indicators for JPM Price Prediction and Backtesting

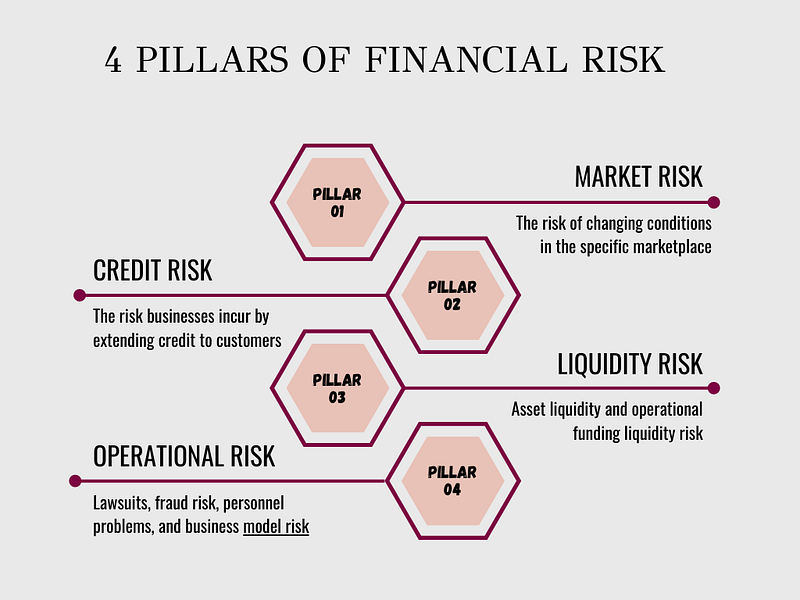

Four Pillars of Financial Risk: Market Risk, Credit Risk, Liquidity Risk, and Operational Risk

Business Motivation: Banks have always been vulnerable to quickly shifting sentiment among investors, depositors, and regulators. In the year since authorities in the U.S. and Switzerland stepped in to quell contagion risk after the collapse of SVB, Signature, and Credit Suisse, regulators remain acutely aware of the sector’s sensitivities.

Unlike other papers that concentrate on a one-size-fits-all technique, in this paper we follow a more holistic strategy that integrates predictive analytics and TI into a single decision-making framework aimed at detecting and predicting financial asset price breakouts and trends to make informed decisions.

The ultimate business goal of AT is the systematic application of Financial Risk Management to stock (algorithmic) trading and investments. In fact, traders always strive to maximize ROI while minimizing the likelihood of losing money on investment decisions. This is where AT comes into play.

Simply put, AT is when you use SaaS products to open and close trades according to set rules such as points of price movement in an underlying market. Once the current market conditions match any predetermined criteria, trading algorithms (algos) can execute a buy or sell order on your behalf.

In principle, AT can generate profits at a speed and frequency that is impossible for a human trader. To earn profits at an unattainable frequency for a human trader, algorithms are used to automate trading.

While TI-powered technical analysis is just one approach to risk-aware time-series analysis, it can complement other quantitative methods such as statistical/ML price forecasting and provide credible fintech BI insights into securities.

Let’s dive into further details of this integrated model-based TI methodology.

Setting the working directory YOURPATH and importing/installing Python libraries

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

!pip install pmdarima, yfinance, statsmodels, matplotlib, sklearn, keras,quantstats

import yfinance as yf

import pandas as pd

import numpy as np

from pmdarima.arima import auto_arima

from statsmodels.tsa.arima.model import ARIMA

import matplotlib.pyplot as plt

from pandas_datareader.data import DataReader

from pandas_datareader import data as pdr

from keras.models import Sequential

from keras.layers import Dense, LSTM

# For time stampsfrom datetime import datetime

from datetime import datetime as dt, timedelta as td

import quantstats as qs

from sklearn.preprocessing import MinMaxScaler

from sklearn.metrics import mean_squared_error,mean_absolute_error,explained_variance_score,r2_score

Reading Input Stock Data

Option 1: Use yf.download

# Download data

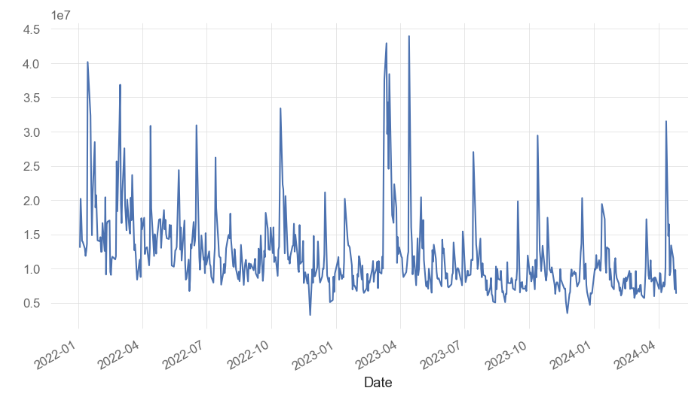

gs = yf.download("JPM", start="2022-01-03", end="2024-04-26")

gs

Open High Low Close Adj Close Volume

Date

2022-01-03 159.860001162.639999159.509995161.699997150.404938131209002022-01-04 164.309998168.580002164.229996167.830002156.106750201958002022-01-05 167.820007168.360001163.729996163.779999153.252762175394002022-01-06 166.910004167.369995163.869995165.520004154.880951140475002022-01-07 165.669998167.529999165.059998167.160004156.41554313913300... ... ... ... ... ... ...

2024-04-22185.990005190.130005185.979996189.410004189.410004115297002024-04-23191.130005192.229996190.520004192.139999192.13999991444002024-04-24190.529999193.229996190.169998193.080002193.08000269649002024-04-25192.250000193.940002191.179993193.369995193.36999598023002024-04-26193.570007194.869995193.059998193.490005193.4900056408600582 rows × 6 columns

defget_sharpe(stock):

start=dt.today()-td(365*2)

df = yf.download(stock,start=start)['Adj Close']

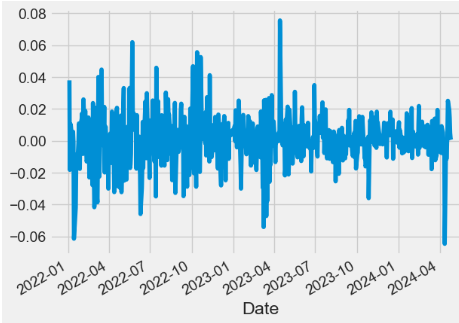

ret = df.pct_change()

ri = ret.mean()

rf = (.0467 / 365) # 10 Year Treasury Rate of 4.67% for Apr 26 2024

sigma = ret.std()

sr = (ri - rf) * 250 ** .5 / sigma # annualize the sharpe ratioprint(f'Sharpe Ratio of {stock.upper()} is : {sr}')

return sr

get_sharpe('JPM')

Sharpe Ratio of JPM is : 1.13994216822035

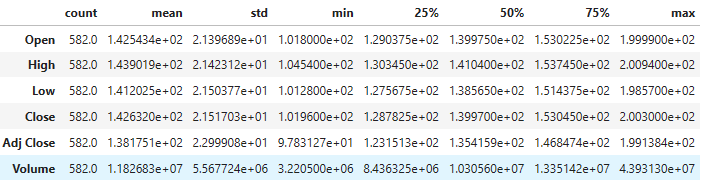

Comparing 2Y kurtosis, skewness and std: JPM vs ^GSPC benchmark

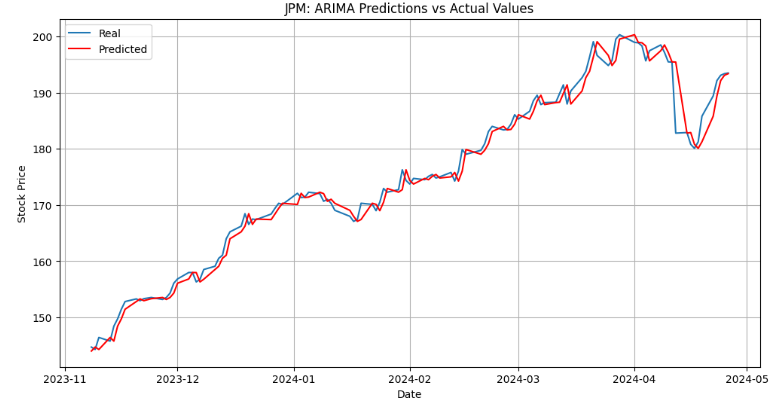

Running ARIMA model forecasting with 80:20 % train/test split

# Define the ARIMA modeldefarima_forecast(history):

# Fit the model

model = ARIMA(history, order=(0,1,0))

model_fit = model.fit()

# Make the prediction

output = model_fit.forecast()

yhat = output[0]

return yhat

# Split data into train and test sets

X = dataset_ex_df.values

size = int(len(X) * 0.8)

train, test = X[0:size], X[size:len(X)]

# Walk-forward validation

history = [x for x in train]

predictions = list()

for t inrange(len(test)):

# Generate a prediction

yhat = arima_forecast(history)

predictions.append(yhat)

# Add the predicted value to the training set

obs = test[t]

history.append(obs)

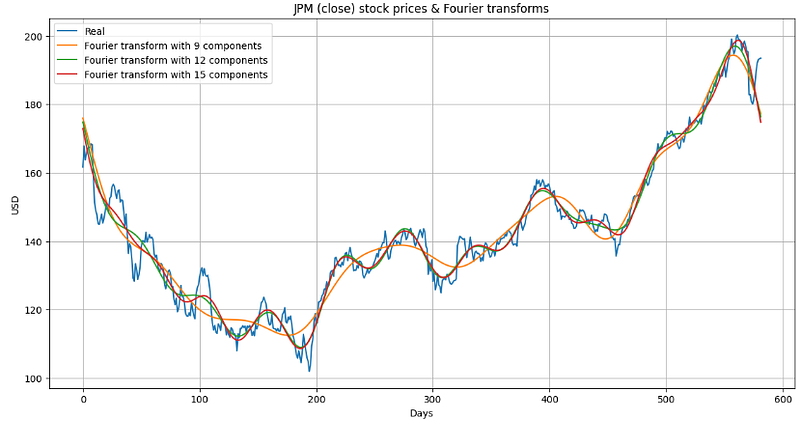

By applying FFT to stock market data, we can decompose the data into its harmonic components and examine trends, cycles, and other patterns in the data that may not be apparent by simply looking at the time-domain stock prices.

# Create a new dataframe with only the 'Close column

data = df.filter(['Close'])

# Convert the dataframe to a numpy array

dataset = data.values

# Get the number of rows to train the model on

training_data_len = int(np.ceil( len(dataset) * .95 ))

training_data_len

553# Scale the data

scaler = MinMaxScaler(feature_range=(0,1))

scaled_data = scaler.fit_transform(dataset)

# Create the scaled training data set

train_data = scaled_data[0:int(training_data_len), :]

# Split the data into x_train and y_train data sets

x_train = []

y_train = []

for i inrange(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])

if i<= 61:

print(x_train)

print(y_train)

print()

# Convert the x_train and y_train to numpy arrays

x_train, y_train = np.array(x_train), np.array(y_train)

# Reshape the data

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

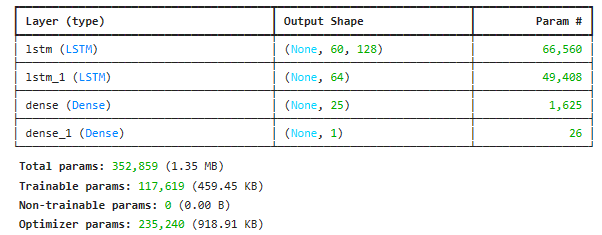

Building, compiling and running the LSTM model

from keras.models import Sequential

from keras.layers import Dense, LSTM

# Build the LSTM model

model = Sequential()

model.add(LSTM(128, return_sequences=True, input_shape= (x_train.shape[1], 1)))

model.add(LSTM(64, return_sequences=False))

model.add(Dense(25))

model.add(Dense(1))

# Compile the model

model.compile(optimizer='adam', loss='mean_squared_error')

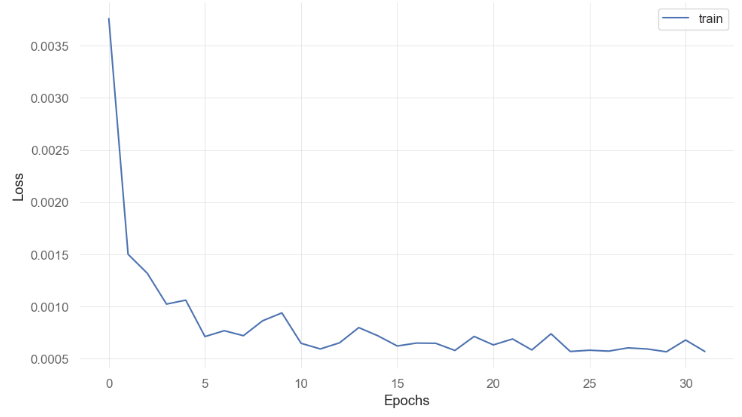

# Train the model

history=model.fit(x_train, y_train, batch_size=1, epochs=32)

493/493 ━━━━━━━━━━━━━━━━━━━━ 8s 12ms/step - loss: 0.0067

Epoch 2/32

..................

Epoch 30/32493/493 ━━━━━━━━━━━━━━━━━━━━ 7s 15ms/step - loss: 5.1676e-04

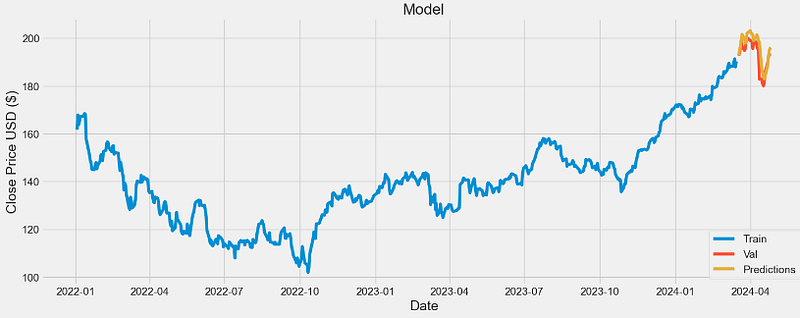

# Create a new array containing scaled values from index 1543 to 2002

test_data = scaled_data[training_data_len - 60: , :]

# Create the data sets x_test and y_test

x_test = []

y_test = dataset[training_data_len:, :]

for i inrange(60, len(test_data)):

x_test.append(test_data[i-60:i, 0])

# Convert the data to a numpy array

x_test = np.array(x_test)

# Reshape the data

x_test = np.reshape(x_test, (x_test.shape[0], x_test.shape[1], 1 ))

# Get the models predicted price values

predictions = model.predict(x_test)

predictions = scaler.inverse_transform(predictions)

# Get the root mean squared error (RMSE)

rmse = np.sqrt(np.mean(((predictions - y_test) ** 2)))

rmse

4.21706997838837

We have addressed a very challenging task of predicting trends in JPM prices and calculating future value of this asset.

We believe that the well known challenges of highly volatile and dynamic financial markets can be reduced by incorporating model-based time-series forecasting methods, fintech data analytics and TI-powered stock screening into a single Python-based algo-trading (AT) platform.

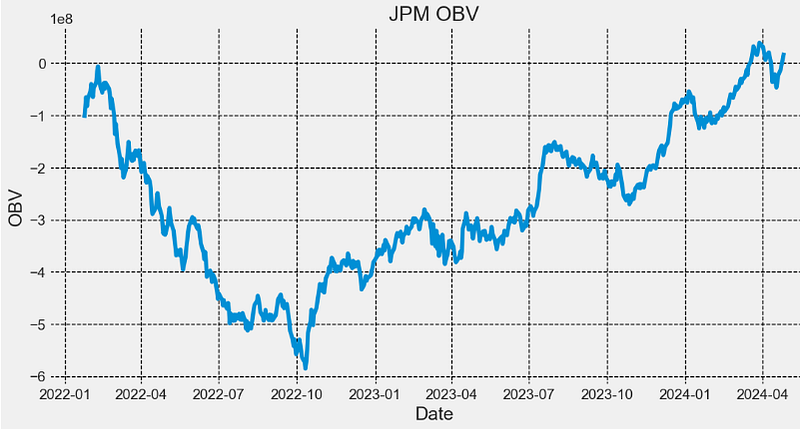

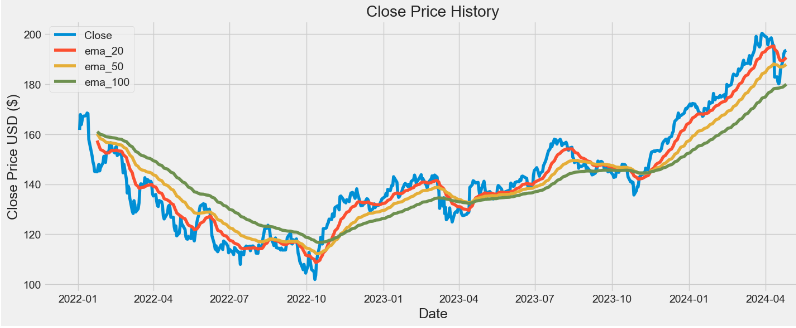

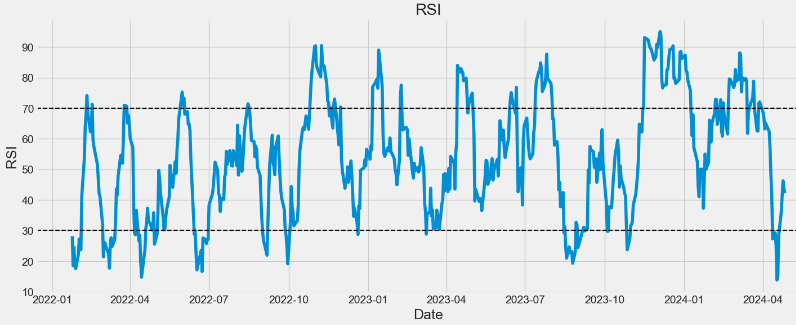

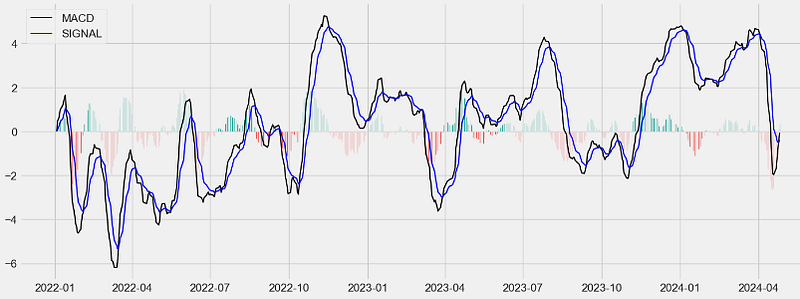

This paper proposes trading strategies based on quantitative analysis of time series data using ARIMA, FFT, LSTM, and popular TI such as EMA, RSI, MACD, and OBV.

We have also calculated and compared against the S&P 500 benchmark the JPM risk-adjusted returns, beta, annual volatility and std aimed at maximizing the (ROI/Risk) ratio.

The Road Ahead: we will continue looking at the key trends, case examples and best industry practices that set to accelerate the AT market growth in the near future. Factors such as the increasing adoption of ML/AI, real-time data analytics, interactive visualizations, and the rising demand for automated trading systems do substantiate the current rapid AT industry growth in 3 key regions such as North America, Europe, and Asia.