Uncovering Hidden Gems with Multi-Objective Portfolio Optimization: MPT, CAPM, Beta, Vol, Sharpe, PyPortfolioOpt & SciPy

- The subject of this quant trading study is the optimal selection process of financial instruments that maximizes the Return/Risk Ratio (RRR).

- Decision makers in fintech need to make trade-offs between the conflicting objectives. Therefore, it is important that the multiple objectives are to be considered explicitly, including the uncertainties in expected RRR.

- The objective typically maximizes factors such as expected return, and minimizes costs like financial risk, resulting in a multi-objective optimization problem.

- Investment portfolio optimization (IPO) involves using various simulation and multi-parameter minimization scenarios to construct an asset portfolio that geared towards maximizing ROI within given risk boundaries or minimizing risk for a desired level of return.

- In this article, we consider a multi-period IPO problem, which is an extension of the single-period IPO approach.

- Using an investment universe of global stock indices, bonds, and commodities, we test the performance of optimized portfolios and compare the results to the S&P 500 benchmark for multiple periods.

- For example, we may be interested in selecting a few stocks from the listed S&P 500 companies to ensure they make the most profit possible.

- IPO can also help diversify investments whilst minimizing risks. For example, the mean variance IPO may select a portfolio containing assets in tech, retail, healthcare and real estate instead of a single industry like tech.

- Modern Portfolio Theory (MPT) is one of the most popular IPO techniques focused on building portfolios which maximize expected return given a predefine level of risk.

- Here is a practical example of the Python IPO algorithm:

- We generate N random portfolios. That is N portfolios containing our M stocks with different weights (N>>M).

- We calculate portfolio returns, portfolio risk and the Sharpe Ratio for each of the randomly generated assets.

- Then, we visualize the portfolio returns, risks and Sharpe Ratio using Matplotlib, seaborn or Plotly.

- Finally, we determine the optimal portfolio with the highest return, lowest risk and the highest Sharpe Ratio as compared to the S&P benchmark.

- PyPortfolioOpt is a Python library specifically designed to solve IPO problems. It provides efficient algorithms for finding the portfolio with max(RRR) by calculating the efficient frontier.

- Conventionally, the pandas and numpy libraries can be used for handling data and mathematical operations, respectively, while scipy.optimize can be utilized for the optimization process itself.

Project Goals:

- The ultimate goal is to identify and remove low-value assets from a portfolio, or to allocate more budget towards securities that are high value.

- By building a well-diversified portfolio that holds multiple assets and asset classes, we’ll be better positioned to weather volatility and reduce the risk of losing all of our capital.

- We’ll address another key issue in the definition of asset allocation: how to articulate it across different time horizons.

Business Case:

- In today’s competitive, global economy, it is imperative that investors have a well-planned, balanced (growth) portfolio.

- IPO is an important tool to help investors reposition, grow, achieve sustainable long-term profits or get their products ready for sale.

- IPO stands among key enablers of the Risk Intelligent Enterprise, along with risk governance, risk sensing, and scenario planning.

Methods:

- Modern Portfolio Theory

- Mean-Variance Optimization

- Black-Litterman Model

- Monte Carlo Simulation

- Risk Parity

Scope:

- It is all about optimization analysis with constraints and uncertainty bounds. To optimize means to “make the best or most effective use of a situation, opportunity, or resource” (Dictionary.com).

- Virtually every investor has limited resources, and the goal is to generate as much business value (“bang”) with the limited resources available (“the buck”).

- Monte Carlo simulations offer a powerful tool to assess different asset allocation strategies and their potential outcomes under uncertain market conditions.

- We’ll test the performance of various stochastic simulation methods by examining a plethora of well-diversified assets for multiple time horizons.

Theoretical Background:

- The modern portfolio theory (MPT) is a practical method for selecting investments in order to maximize their overall returns within an acceptable level of risk. The MPT can be useful to investors trying to construct efficient and diversified portfolios.

- Among the most prominent approaches to IPO, Mean-Variance Optimization (MVO) pioneered by Markowitz (1952) stands as a cornerstone in MPT. Specifically, we will explore the Markowitz’s Efficient Frontier, a crucial concept that identifies the optimal combination of assets in a portfolio.

- The Black-Litterman (BL) model is an asset allocation tool that portfolio managers use to optimize investor portfolios according to their risk tolerance and market outlook. The model uses market equilibrium as a starting point and considers the investors’ subjective market views to calculate how the optimal asset weights should differ from the initial portfolio allocation. The model attempts to create more stable and efficient portfolios based on investors’ unique insight, which overcomes the issues of input sensitivity.

- Monte Carlo simulations offer a powerful tool to assess different asset allocation strategies and their potential outcomes under uncertain market conditions.

- The risk parity approach to portfolio construction seeks to allocate the capital in a portfolio based on a risk-weighted basis. Asset allocation is the process by which an investor divides the capital in a portfolio among different types of assets. Following the tenets of MPT, this approach makes use of the efficient frontier and security market line (SML) to find the optimal asset allocation.

Some Popular Methods:

- Market Cap Weighted

- Inverse Volatility

- Equal Risk

- Max Diversification & Min Variance

- Mean Variance Optimal.

A Few Challenges

- Typical optimal weights have too large a range.

- The mean return of a security changes due to time and other factors (so do covariances).

- Even if the mean (one-year, say) return is constant over time, it takes decades to get an accurate estimate.

- The optimal weights are sensitive to mean return estimates.

- The optimal weights usually produce disappointing results when used on a real-time, prospective basis.

- Besides, portfolio managers want to use their stock picking “skills.”

Let’s delve into the specifics of out IPO scenario testing aimed at max (RRR)!

Scenario 1: MPT Crypto

Stocks: Top 10 Cryptocurrencies by MC

tickers="BTC-USD ETH-USD USDT-USD USDC-USD BNB-USD BUSD-USD XRP-USD ADA-USD SOL-USD DOGE-USD"Time Horizon: start=”2022–01–03", end=”2024–05–11"

Methods: Monte Carlo

Objectives: Max Sharpe Ratio

Libraries: yfinance

- Let’s begin with cryptocurrency IPO using Markowitz theory. Markowitz put two parameters at the head of his theory — risk and profitability. An efficient frontier is one that defines the effective set of portfolios on it, respectively, between risk and return.

- Here’s the simple hands-on example:

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

# Basic Imports

import yfinance as yf

import numpy as np

import pandas as pd

import os

import seaborn as sns

#Fetching historical crypto data

data = yf.download("BTC-USD ETH-USD USDT-USD USDC-USD BNB-USD BUSD-USD XRP-USD ADA-USD SOL-USD DOGE-USD", start="2022-01-03", end="2024-05-11")

N_iterations = 15000

import matplotlib.pyplot as plt

#calculate percentage change between the current and a prior element - it will be daily returns

daily_returns = data['Adj Close'].pct_change()

num_assets = len(daily_returns.columns)

#calculate covariance matrix

cov_matrix = (daily_returns.cov())*365 # multiply by days in year to get annual covariance

# run optimization of portfolio weights

dict_portfolios = {"portfolio_std":[],"portfolio_returns":[],"weights":[], "sharpe_ratio":[]}

for i in range(N_iterations):

#get random weights and calculate returns and variance

weights = np.random.random(num_assets)

weights = weights/np.sum(weights)

expected_portfolio_return = np.sum(daily_returns.mean()*weights)

expected_portfolio_variance = np.dot(weights.T,np.dot(cov_matrix,weights))

sharpe_ratio = expected_portfolio_return / np.sqrt(expected_portfolio_variance)

# collect all portfolios in the dictionary

dict_portfolios['portfolio_std'].append(np.sqrt(expected_portfolio_variance)) # get standard deviation instead of variance

dict_portfolios['portfolio_returns'].append(expected_portfolio_return)

dict_portfolios['weights'].append(weights)

dict_portfolios['sharpe_ratio'].append(sharpe_ratio)

simulated_portfolios=pd.DataFrame(dict_portfolios)

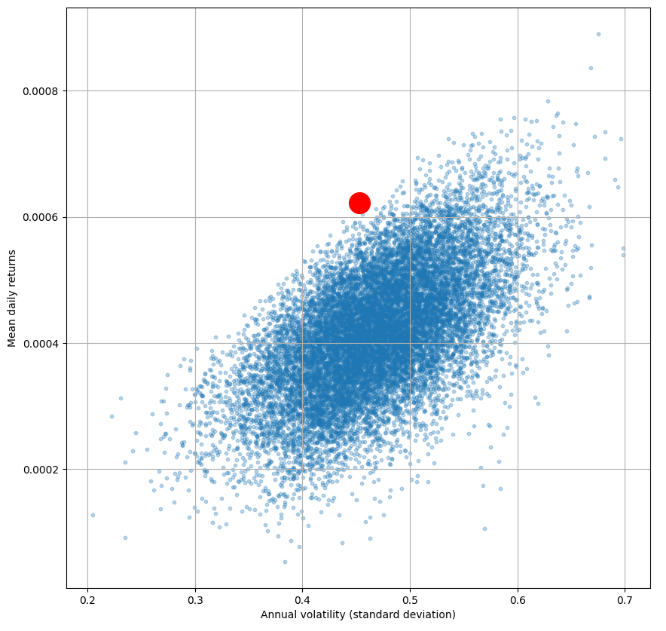

# Plot returns vs. standard deviation to find optimal portfolio (efficient frontier)

simulated_portfolios.plot.scatter(x='portfolio_std', y='portfolio_returns', marker='o', s=10, alpha=0.3, grid=True, figsize=[10,10])

max_sharpe_ratio = simulated_portfolios.query('sharpe_ratio == sharpe_ratio.max()')

# red dot for max sharpe ratio

plt.plot(max_sharpe_ratio['portfolio_std'],max_sharpe_ratio['portfolio_returns'],'ro',markersize=20)

plt.ylabel('Mean daily returns')

plt.xlabel('Annual volatility (standard deviation)')

plt.show()

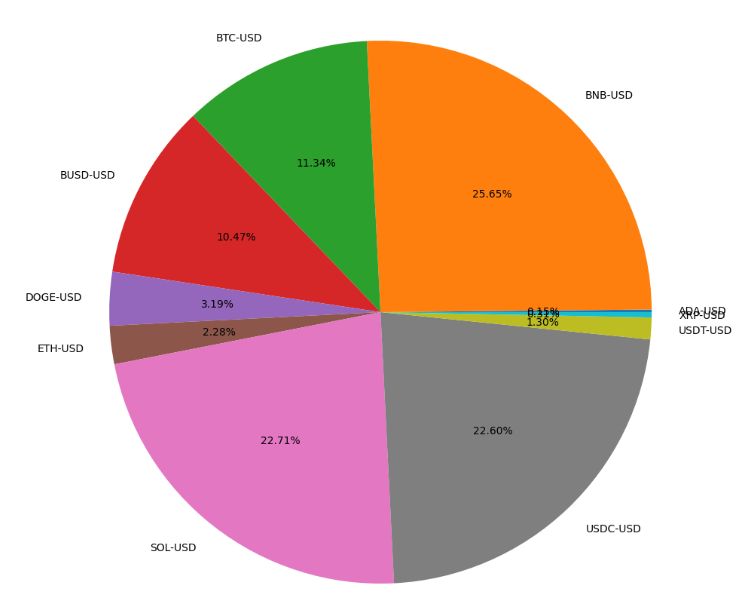

- Checking the portfolio weights

# check the portfolio weights

dictionary_of_weights = {}

for i in range(len(daily_returns.columns)):

dictionary_of_weights [daily_returns.columns[i]] = max_sharpe_ratio['weights'].values[0][i]

print('max sharpe ratio: \n')

efficient_frontier = pd.DataFrame.from_dict(dictionary_of_weights, orient='index').reset_index()

efficient_frontier.columns = ['crypto pair','weights']

display(efficient_frontier)

max sharpe ratio:

crypto pair weights

0 ADA-USD 0.001532

1 BNB-USD 0.256517

2 BTC-USD 0.113406

3 BUSD-USD 0.104682

4 DOGE-USD 0.031886

5 ETH-USD 0.022788

6 SOL-USD 0.227143

7 USDC-USD 0.225962

8 USDT-USD 0.012950

9 XRP-USD 0.003134- Plotting the portfolio weights

from matplotlib import pyplot as plt

import numpy as np

WIDTH_SIZE=9

HEIGHT_SIZE=9

fig = plt.figure(figsize=(WIDTH_SIZE,HEIGHT_SIZE))

ax = fig.add_axes([0,0,1,1])

ax.axis('equal')

langs = efficient_frontier['crypto pair']

students = efficient_frontier['weights']

ax.pie(students, labels = langs,autopct='%1.2f%%')

plt.show()

Scenario 2: Energy-Defense-ETF Diversification

Stocks: XOM, LMT, SCHD

Time Horizon: 1Y

Methods: Monte Carlo

Objectives: Max Sharpe Ratio

Libraries: yfinance

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

#BASIC IMPORTS

import pandas as pd

import requests

import numpy as np

import matplotlib.pyplot as plt

from math import floor

from termcolor import colored as cl

import yfinance as yf

from yahoofinancials import YahooFinancials

plt.rcParams['figure.figsize'] = (20, 10)

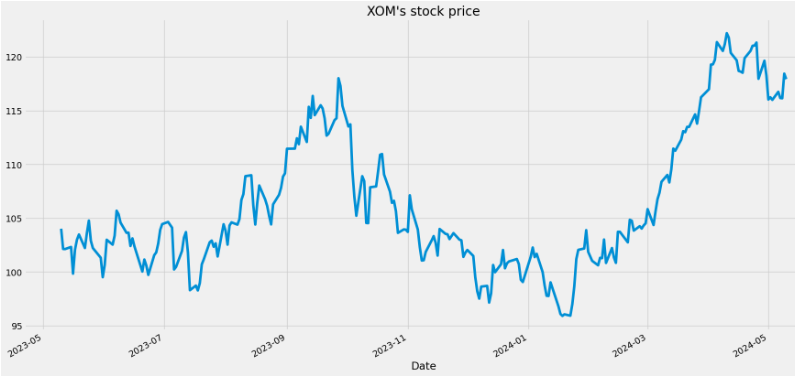

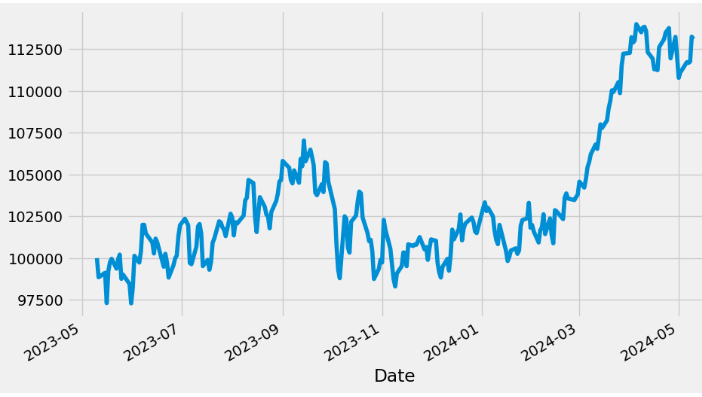

plt.style.use('fivethirtyeight')- Loading XOM historical data

ticker = yf.Ticker('XOM')

aapl_df = ticker.history(period="1y")

aapl_df['Close'].plot(title="XOM's stock price")

aapl_df.tail()

Open High Low Close Volume Dividends Stock Splits

Date

2024-05-06 00:00:00-04:00 116.669998 118.339996 116.400002 116.750000 31401300 0.0 0.0

2024-05-07 00:00:00-04:00 117.279999 117.580002 115.930000 116.169998 30122000 0.0 0.0

2024-05-08 00:00:00-04:00 115.709999 116.949997 115.410004 116.150002 18957200 0.0 0.0

2024-05-09 00:00:00-04:00 116.199997 118.529999 116.190002 118.440002 17561300 0.0 0.0

2024-05-10 00:00:00-04:00 118.540001 118.650002 117.809998 117.928001 4910616 0.0 0.0

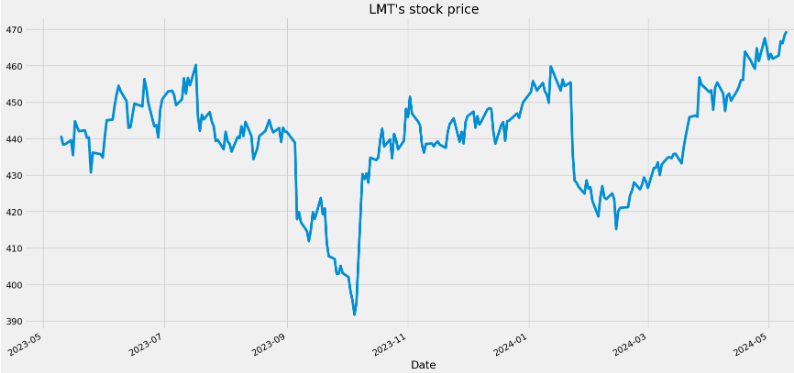

- Loading LMT historical data

ticker = yf.Ticker('LMT')

ibm_df = ticker.history(period="1y")

ibm_df['Close'].plot(title="LMT's stock price")

- Loading SCHD historical data

ticker = yf.Ticker('SCHD')

azn_df = ticker.history(period="1y")

azn_df['Close'].plot(title="SCHD's stock price")

- Normalizing the stock prices and calculating Normed Return

aapl = aapl_df[['Close']]

ibm = ibm_df[['Close']]

azn = azn_df[['Close']]

stock_df=aapl

stock_df['Normed Return'] = stock_df['Close']/ stock_df.iloc[0]['Close']

aapl=stock_df

aapl.tail()

Close Normed Return

Date

2024-05-06 00:00:00-04:00 116.750000 1.122402

2024-05-07 00:00:00-04:00 116.169998 1.116826

2024-05-08 00:00:00-04:00 116.150002 1.116634

2024-05-09 00:00:00-04:00 118.440002 1.138650

2024-05-10 00:00:00-04:00 117.928001 1.133727

stock_df=ibm

stock_df['Normed Return'] = stock_df['Close']/ stock_df.iloc[0]['Close']

ibm=stock_df

ibm.tail()

Close Normed Return

Date

2024-05-06 00:00:00-04:00 462.779999 1.050026

2024-05-07 00:00:00-04:00 466.679993 1.058875

2024-05-08 00:00:00-04:00 466.160004 1.057695

2024-05-09 00:00:00-04:00 468.390015 1.062755

2024-05-10 00:00:00-04:00 469.429993 1.065115

stock_df=azn

stock_df['Normed Return'] = stock_df['Close']/ stock_df.iloc[0]['Close']

azn=stock_df

azn.tail()

Close Normed Return

Date

2024-05-06 00:00:00-04:00 78.129997 1.153580

2024-05-07 00:00:00-04:00 78.250000 1.155352

2024-05-08 00:00:00-04:00 78.510002 1.159191

2024-05-09 00:00:00-04:00 79.160004 1.168788

2024-05-10 00:00:00-04:00 79.279999 1.170560- Assigning the portfolio allocation weights [0.5,0.2,0.3] and the investment amount $100k

for stock_df, allo in zip((aapl, ibm,azn),[0.5,0.2,0.3]):

stock_df['Allocation'] = stock_df['Normed Return']*allo

for stock_df in (aapl, ibm, azn):

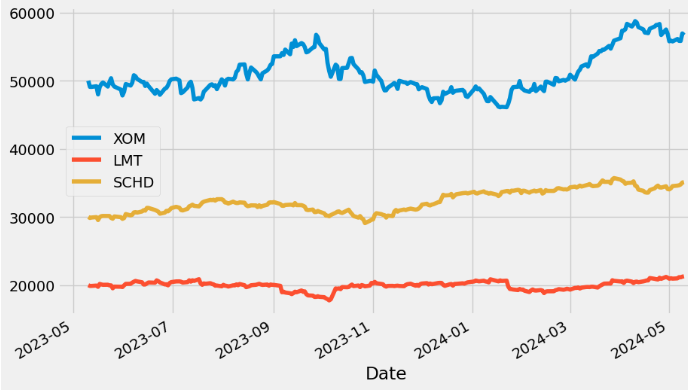

stock_df['Position Amount']= stock_df['Allocation']*100000- Plotting the cumulative return of the entire portfolio vs individual stocks

total_pos_vals = [aapl['Position Amount'], ibm['Position Amount'], azn['Position Amount']]

portf_vals = pd.concat(total_pos_vals, axis = 1)

portf_vals.columns = ['XOM', 'LMT', 'SCHD']

portf_vals['Total Pos'] = portf_vals.sum(axis=1)

portf_vals['Total Pos'].plot(figsize = (10,6))

portf_vals['2023-03-01':].drop('Total Pos', axis = 1).plot(figsize=(10,6));

- Calculating the mean portfolio daily return and std

portf_vals['Daily Return'] = portf_vals['Total Pos'].pct_change(1)

portf_vals.dropna(inplace = True)

print('Daily Return Average: ',portf_vals['Daily Return'].mean())

print('Daily Return Standard Deviation: ',portf_vals['Daily Return'].std())

Daily Return Average: 0.0005255601943780237

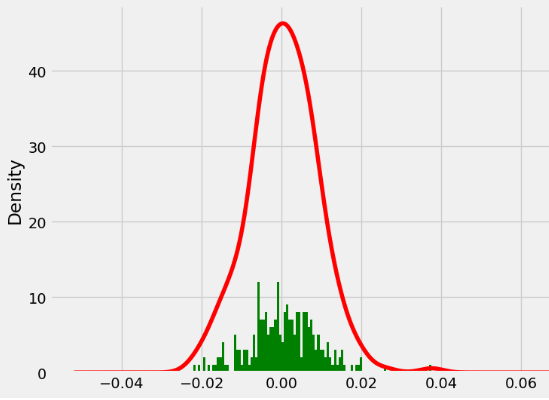

Daily Return Standard Deviation: 0.008596775975364407- Plotting the density vs histogram of the portfolio daily returns

portf_vals['Daily Return'].plot(kind = 'hist', bins=100, figsize = (6,8), color = 'green')

portf_vals['Daily Return'].plot(kind = 'kde', figsize = (8,6), color = 'r');

- Calculating the cumulative return of our portfolio

cumulative_return = 100*(portf_vals['Total Pos'][-1]/portf_vals['Total Pos'][0]-1)

print('Cumulative return: ', cumulative_return)

Cumulative return: 14.416636530936788- Calculating the portfolio Sharpe ratio

SR = portf_vals['Daily Return'].mean()/portf_vals['Daily Return'].std()

print('Sharpe Ratio = ', SR)

Sharpe Ratio = 0.06113456903891762

#Annual Sharpe Ratio:

ASR = (252**0.5) * SR

print('Annualized Sharpe Ratio = ', ASR)

Annualized Sharpe Ratio = 0.9704811971165102

- Stock close price preparation for IPO

stocks = pd.concat([aapl['Close'], ibm['Close'], azn['Close']], axis = 1)

stocks.columns = ['XOM', 'LMT', 'SCHD']

stocks.tail()

XOM LMT SCHD

Date

2024-05-06 00:00:00-04:00 116.750000 462.779999 78.129997

2024-05-07 00:00:00-04:00 116.169998 466.679993 78.250000

2024-05-08 00:00:00-04:00 116.150002 466.160004 78.510002

2024-05-09 00:00:00-04:00 118.440002 468.390015 79.160004

2024-05-10 00:00:00-04:00 117.928001 469.429993 79.279999- Comparing mean stock daily returns

stocks.pct_change(1).mean()

XOM 0.000584

LMT 0.000307

SCHD 0.000650

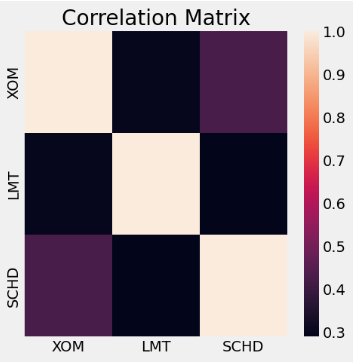

dtype: float64- Examining the stock daily return correlation matrix

stocks.pct_change(1).corr()

XOM LMT SCHD

XOM 1.000000 0.297715 0.426209

LMT 0.297715 1.000000 0.289254

SCHD 0.426209 0.289254 1.000000

import seaborn as sns

fig, ax = plt.subplots(figsize=(5, 5))

sns.heatmap(stocks.pct_change(1).corr(),ax=ax).set(title='Correlation Matrix')

plt.show()

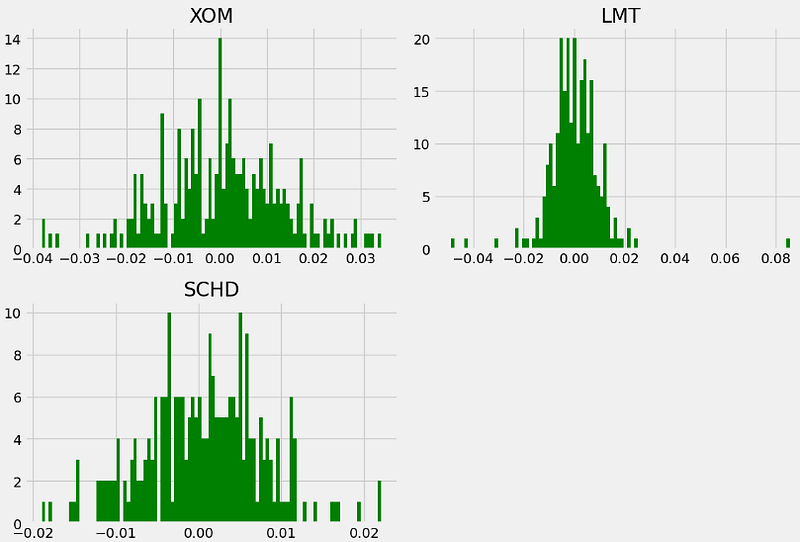

- Comparing the stock log returns histograms

log_returns = np.log(stocks/stocks.shift(1))

log_returns.hist(bins = 100, figsize = (12,8), color = 'g')

plt.tight_layout()

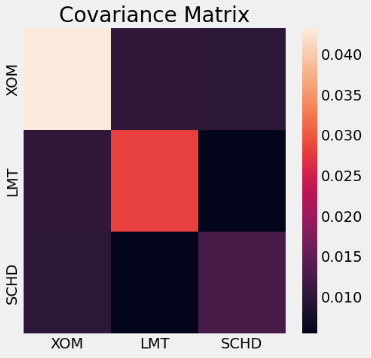

- Calculating and plotting the covariance matrix of stock log returns

log_returns.cov()*252

XOM LMT SCHD

XOM 0.043198 0.010293 0.009932

LMT 0.010293 0.028296 0.005459

SCHD 0.009932 0.005459 0.012576

import seaborn as sns

fig, ax = plt.subplots(figsize=(5, 5))

sns.heatmap(log_returns.cov()*252,ax=ax).set(title='Covariance Matrix')

plt.show()

- Choosing an optimal portfolio allocation within the MPT framework

np.random.seed(101)

print(stocks.columns)

weights = np.array(np.random.random(3))

print('Random Weights: ')

print(weights)

#However, their sum must be equal to 100

print('Rebalance')

weights = weights/np.sum(weights)

print(weights)

Index(['XOM', 'LMT', 'SCHD'], dtype='object')

Random Weights:

[0.51639863 0.57066759 0.02847423]

Rebalance

[0.46291341 0.51156154 0.02552505]

exp_ret = np.sum((log_returns.mean() * weights) * 252)

print('Expected Portfolio Return: ',exp_ret)

Expected Portfolio Return: 0.09439096736312266

exp_vol = np.sqrt(np.dot(weights.T,np.dot(log_returns.cov() * 252, weights)))

print('Expected Volatility: ', exp_vol)

Expected Volatility: 0.14806090936894675

SR = exp_ret/exp_vol

print('Sharpe Ratio: ', SR)

Sharpe Ratio: 0.6375144375745645

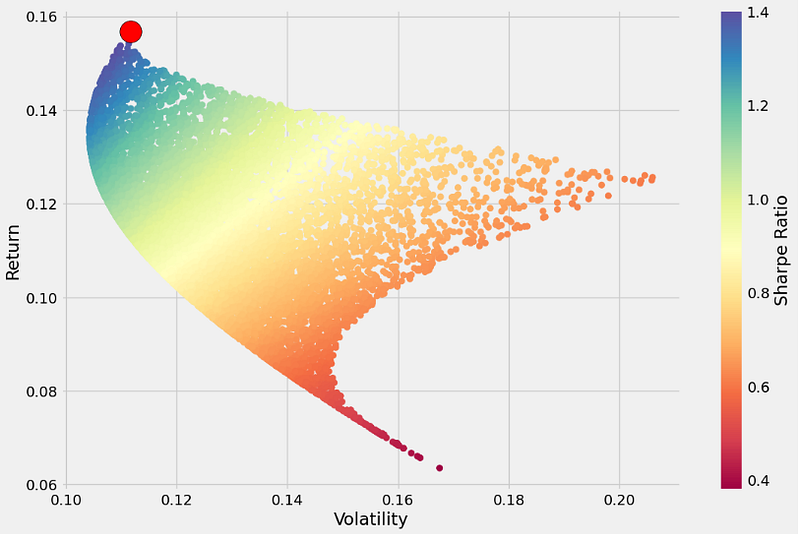

#Choosing an optimal portfolio allocation.

num_ports = 10000

all_weights = np.zeros((num_ports,len(stocks.columns)))

ret_arr = np.zeros(num_ports)

vol_arr = np.zeros(num_ports)

sharpe_arr = np.zeros(num_ports)

for ind in range(num_ports):

weights = np.array(np.random.random(3))

weights = weights / np.sum(weights)

all_weights[ind,:] = weights

ret_arr[ind] = np.sum((log_returns.mean() * weights) *252)

vol_arr[ind] = np.sqrt(np.dot(weights.T, np.dot(log_returns.cov() * 252, weights)))

sharpe_arr[ind] = ret_arr[ind]/vol_arr[ind]

sharpe_arr.max()

1.4038899601457429

sharpe_arr.argmax()

3761

all_weights[sharpe_arr.argmax(),:]

array([0.01272508, 0.0033809 , 0.98389403])

plt.figure(figsize = (12,8))

plt.scatter(vol_arr,ret_arr,c=sharpe_arr,cmap='Spectral')

plt.colorbar(label='Sharpe Ratio')

plt.xlabel('Volatility')

plt.ylabel('Return')

# Add red dot for max SR

max_sr_ret = ret_arr[sharpe_arr.argmax()]

max_sr_vol = vol_arr[sharpe_arr.argmax()]

plt.scatter(max_sr_vol,max_sr_ret,c='red',s=450,edgecolors='black');

Read More:

- Fin Analysis-Portfolio Allocation Optimization

- Portfolio Optimization: Using Python

- Get Financial Data from Yahoo Finance with Python

- Download Financial Dataset Using Yahoo Finance in Python | A Complete Guide

- Markowitz Portfolio Optimization — Gold and Amazon

Scenario 3: PyPortfolioOpt MPT

Stocks: PFE, WM, DIS, CLX

Time Horizon: 2010–2023

Methods: The Markowitz Mean-Variance Model

Objectives: Testing PyPortfolioOpt Efficient Frontier

Libraries: PyPortfolioOpt

# Setting working directory

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd()

#Installing pyportfolioopt

!pip install pyportfolioopt

- Preparing input stock data for IPO

import yfinance as yf

# Getting dataframes info for Stocks using yfinance

aapl_df = yf.download('PFE', start = '2010-01-01', end = '2023-04-09')

tsla_df = yf.download('WM', start = '2010-01-01', end = '2023-04-09')

dis_df = yf.download('DIS', start = '2010-01-01', end = '2023-04-09')

amd_df = yf.download('CLX', start = '2010-01-01', end = '2023-04-09')

# Extracting Adjusted Close for each stock

aapl_df = aapl_df['Adj Close']

tsla_df = tsla_df['Adj Close']

dis_df = dis_df['Adj Close']

amd_df = amd_df['Adj Close']

import pandas as pd

# Merging and creating an Adj Close dataframe for stocks

df = pd.concat([aapl_df, tsla_df, dis_df, amd_df], join = 'outer', axis = 1)

df.columns = ['pfe', 'wm', 'dis', 'clx']

df # Visualizing dataframe for input

pfe wm dis clx

Date

2010-01-04 11.026819 23.771673 27.933918 41.983829

2010-01-05 10.869543 23.667282 27.864237 42.441734

2010-01-06 10.834594 23.660328 27.716160 42.332390

2010-01-07 10.793817 23.716005 27.724873 41.929150

2010-01-08 10.881195 23.827343 27.768423 41.935989

... ... ... ... ...

2023-03-31 40.799999 163.169998 100.129997 158.240005

2023-04-03 41.349998 163.869995 99.760002 156.750000

2023-04-04 40.900002 163.529999 99.570000 155.899994

2023-04-05 41.549999 162.820007 99.910004 157.419998

2023-04-06 41.500000 163.660004 99.970001 157.759995

3338 rows × 4 columns

- Calculating the annualized expected returns and the sample covariance matrix

# Importing libraries for portfolio optimization

import pypfopt

from pypfopt.efficient_frontier import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

# Calculating the annualized expected returns and the annualized sample covariance matrix

mu = expected_returns.mean_historical_return(df) #expected returns

S = risk_models.sample_cov(df) #Covariance matrix

# Visualizing the annualized expected returns

mu

pfe 0.105267

wm 0.156843

dis 0.101074

clx 0.105136

dtype: float64

# Visualizing the covariance matrix

S

pfe wm dis clx

pfe 0.046326 0.017478 0.020015 0.012002

wm 0.017478 0.035693 0.021444 0.014009

dis 0.020015 0.021444 0.068004 0.010278

clx 0.012002 0.014009 0.010278 0.043615- Using Efficient Frontier to maximize the Sharpe ratio

# Optimizing for max Sharpe ratio

ef = EfficientFrontier(mu, S) # Providing expected returns and covariance matrix as input

weights = ef.max_sharpe() # Optimizing weights for Sharpe ratio maximization

clean_weights = ef.clean_weights() # clean_weights rounds the weights and clips near-zeros

# Printing optimized weights and expected performance for portfolio

clean_weights

OrderedDict([('pfe', 0.0841), ('wm', 0.7439), ('dis', 0.0), ('clx', 0.172)])- Creating the new portfolio with optimized weights

new_weights = [0.7439, 0.172]

optimized_portfolio = tsla_df.pct_change()*new_weights[0] + amd_df.pct_change()*new_weights[1]

optimized_portfolio # Visualizing daily returns

Date

2010-01-04 NaN

2010-01-05 -0.001391

2010-01-06 -0.000662

2010-01-07 0.000112

2010-01-08 0.003520

...

2023-03-31 0.011785

2023-04-03 0.001572

2023-04-04 -0.002476

2023-04-05 -0.001553

2023-04-06 0.004209

Name: Adj Close, Length: 3338, dtype: float64- Using Efficient Frontier to maximize the Sharpe ratio

import pandas as pd

from pypfopt.efficient_frontier import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

# Calculate expected returns and sample covariance

mu = expected_returns.mean_historical_return(df)

S = risk_models.sample_cov(df)

# Optimize for maximal Sharpe ratio

ef = EfficientFrontier(mu, S)

weights = ef.max_sharpe()

ef.portfolio_performance(verbose=True)

Expected annual return: 14.4%

Annual volatility: 16.6%

Sharpe Ratio: 0.75

(0.1436115518882465, 0.16579845571388344, 0.7455530955098978)

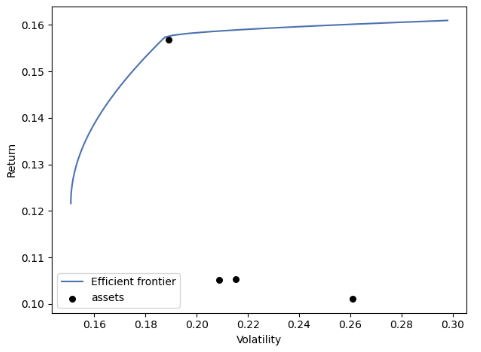

# Plotting results in the Return-Volatility domain

import matplotlib.pyplot as plt

from pypfopt import plotting

ef = EfficientFrontier(mu, S, weight_bounds=(None, None))

fig, ax = plt.subplots()

plotting.plot_efficient_frontier(ef, ax=ax, show_assets=True)

plt.show()

Read More:

Scenario 4: PyPortfolioOpt Risk Models & IPO

Stocks: Well-Diversified Portfolios of 15 and 20 Assets

portfolio1=['GOOG', 'AAPL', 'FB', 'BABA', 'AMZN', 'GE', 'AMD', 'WMT', 'BAC', 'GM',

'T', 'UAA', 'SHLD', 'XOM', 'RRC', 'BBY', 'MA', 'PFE', 'JPM', 'SBUX']

portfolio2 = ["MSFT", "AMZN", "KO", "MA", "COST",

"LUV", "XOM", "PFE", "JPM", "UNH",

"ACN", "DIS", "GILD", "F", "TSLA"]Time Horizons: 1989–2018 (portfolio 1) & 2014–2023 (portfolio 2)

Methods: Covariance-Based Risk Models & Available IPO Algorithms, viz.

CLA, dirichlet, EfficientFrontier, EfficientCVaR, sector constraints, L2 objective function, efficient risk, Discrete Allocation, Covariance Shrinkage, Efficient Semivariance

Objectives: Predicting Future Variance, mean/EMA historical and CAPM returns

Libraries: PyPortfolioOpt Cookbook

Read More:

Portfolio 1

- Importing libraries and preparing input stock data (portfolio 1) for IPO

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import pypfopt

from pypfopt import risk_models, expected_returns, plotting

pypfopt.__version__

'1.5.3'

#Portfolio 1

df = pd.read_csv("stock_prices.csv", parse_dates=True, index_col="date")

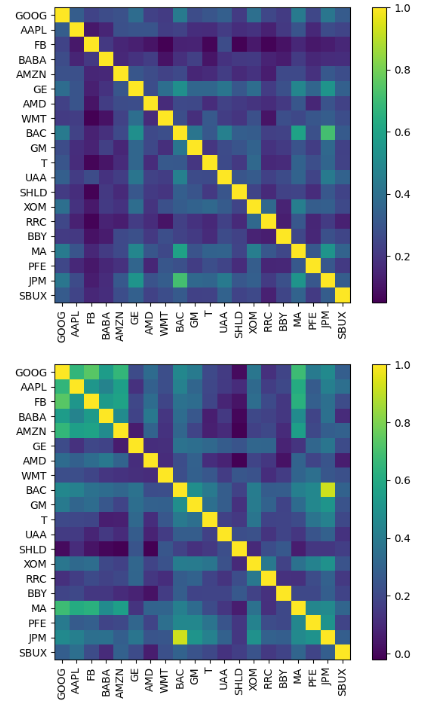

past_df, future_df = df.iloc[:-250], df.iloc[-250:]- Applying the sample_cov risk model to the past and future DataFrames

future_cov = risk_models.sample_cov(future_df)

sample_cov = risk_models.sample_cov(past_df)

plotting.plot_covariance(sample_cov, plot_correlation=True)

plotting.plot_covariance(future_cov, plot_correlation=True)

plt.show()

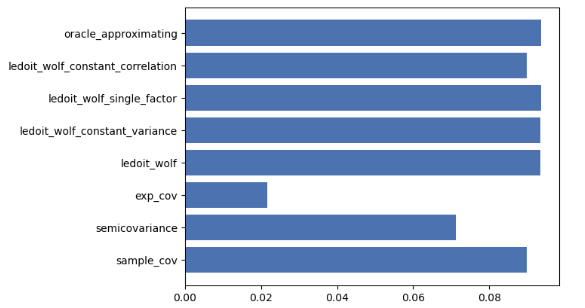

- Comparing MAE of different risk models

future_variance = np.diag(future_cov)

mean_abs_errors = []

risk_methods = [

"sample_cov",

"semicovariance",

"exp_cov",

"ledoit_wolf",

"ledoit_wolf_constant_variance",

"ledoit_wolf_single_factor",

"ledoit_wolf_constant_correlation",

"oracle_approximating",

]

for method in risk_methods:

S = risk_models.risk_matrix(df, method=method)

variance = np.diag(S)

mean_abs_errors.append(np.sum(np.abs(variance - future_variance)) / len(variance))

xrange = range(len(mean_abs_errors))

plt.barh(xrange, mean_abs_errors)

plt.yticks(xrange, risk_methods)

plt.show()

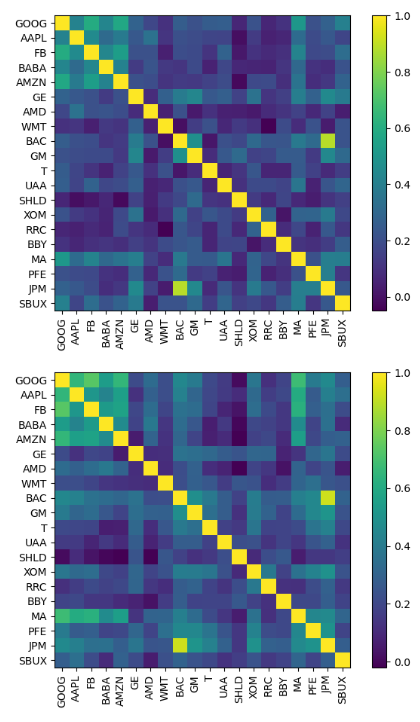

- Applying the exp_cov risk model to the past and future DataFrames

exp_cov = risk_models.exp_cov(past_df)

plotting.plot_covariance(exp_cov, plot_correlation=True)

plotting.plot_covariance(future_cov, plot_correlation=True)

plt.show()

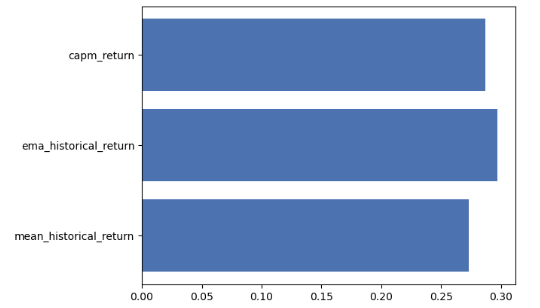

- Comparing MAE of different expected returns applied to the future DataFrame

future_rets = expected_returns.mean_historical_return(future_df)

mean_abs_errors = []

return_methods = [

"mean_historical_return",

"ema_historical_return",

"capm_return",

]

for method in return_methods:

mu = expected_returns.return_model(past_df, method=method)

mean_abs_errors.append(np.sum(np.abs(mu - future_rets)) / len(mu))

xrange = range(len(mean_abs_errors))

plt.barh(xrange, mean_abs_errors)

plt.yticks(xrange, return_methods)

plt.show()

print(mean_abs_errors)

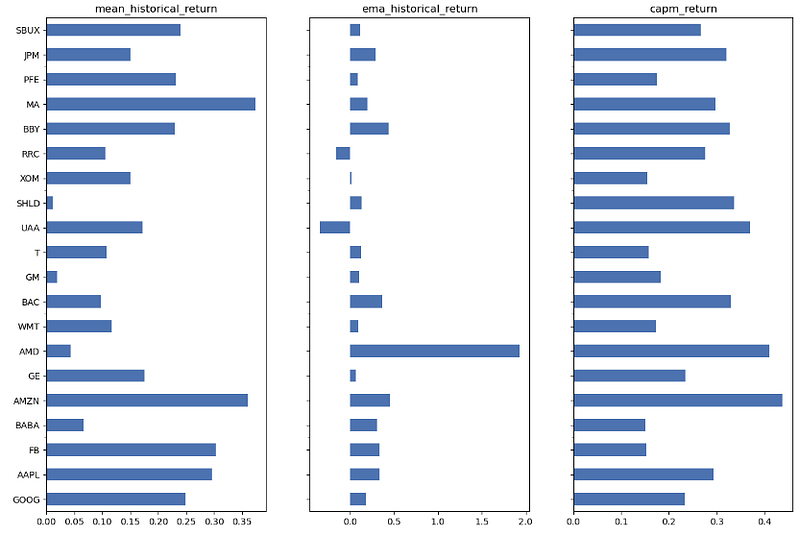

[0.2732675295106071, 0.29740354389638524, 0.28701847303235856]- Comparing the mean/ema historical return and CAPM returns for each individual stock

fig, axs = plt.subplots( 1, len(return_methods),sharey=True, figsize=(15,10))

for i, method in enumerate(return_methods):

mu = expected_returns.return_model(past_df, method=method)

axs[i].set_title(method)

mu.plot.barh(ax=axs[i])

Portfolio 2

- Importing libraries and loading input stock data

import yfinance as yf

import matplotlib.pyplot as plt

import pandas as pd

import numpy as np

tickers = ["MSFT", "AMZN", "KO", "MA", "COST",

"LUV", "XOM", "PFE", "JPM", "UNH",

"ACN", "DIS", "GILD", "F", "TSLA"]

ohlc = yf.download(tickers, period="max")

prices = ohlc["Adj Close"].dropna(how="all")

prices.tail()

ACN AMZN COST DIS F GILD JPM KO LUV MA MSFT PFE TSLA UNH XOM

Date

2023-03-31 285.809998 103.290001 496.869995 100.129997 12.60 82.970001 129.295288 62.029999 32.540001 362.840790 288.299988 40.799999 207.460007 472.589996 109.660004

2023-04-03 285.839996 102.410004 497.029999 99.760002 12.68 83.239998 129.146454 62.400002 31.690001 365.895966 287.230011 41.349998 194.770004 494.190002 116.129997

2023-04-04 285.839996 103.949997 497.730011 99.570000 12.72 82.120003 127.419998 62.209999 31.719999 363.329987 287.179993 40.900002 192.580002 493.250000 115.019997

2023-04-05 281.329987 101.099998 497.130005 99.910004 12.43 83.650002 127.610001 62.799999 31.580000 363.790009 284.339996 41.549999 185.520004 509.230011 116.989998

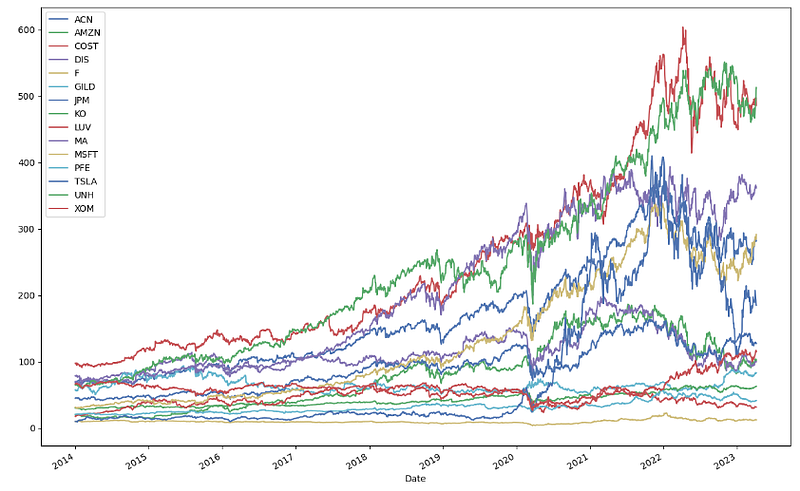

2023-04-06 281.700012 102.059998 485.980011 99.970001 12.33 83.370003 127.470001 62.840000 31.590000 361.470001 291.600006 41.500000 185.059998 512.809998 115.050003- Plotting stock prices

prices[prices.index >= "2014-01-01"].plot(figsize=(15,10));

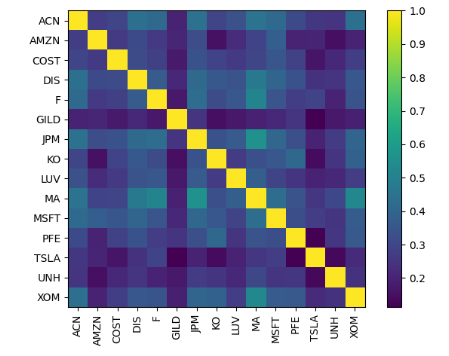

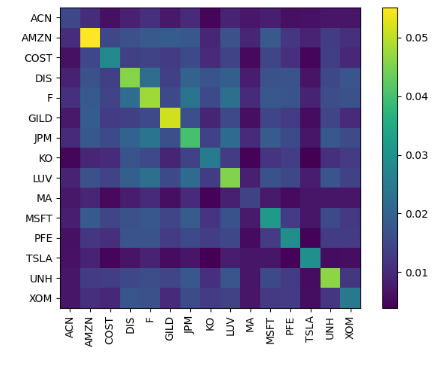

- Applying the risk_models.sample_cov model to these prices

from pypfopt import risk_models

from pypfopt import plotting

sample_cov = risk_models.sample_cov(prices, frequency=252)

sample_cov

ACN AMZN COST DIS F GILD JPM KO LUV MA MSFT PFE TSLA UNH XOM

ACN 0.091047 0.047368 0.028694 0.041800 0.044966 0.028891 0.048398 0.020706 0.037365 0.046675 0.042606 0.025994 0.044706 0.030261 0.030249

AMZN 0.047368 0.328223 0.048238 0.056593 0.054212 0.057143 0.065805 0.020285 0.048216 0.057188 0.073389 0.031130 0.067031 0.034342 0.026733

COST 0.028694 0.048238 0.100966 0.032023 0.031947 0.026906 0.038356 0.021385 0.031193 0.032501 0.037554 0.025261 0.029679 0.027355 0.020312

DIS 0.041800 0.056593 0.032023 0.099784 0.041566 0.032046 0.047258 0.026103 0.039905 0.050994 0.043187 0.029207 0.044257 0.031657 0.025691

F 0.044966 0.054212 0.031947 0.041566 0.127992 0.030105 0.054766 0.026286 0.047190 0.062689 0.042048 0.027026 0.059955 0.029009 0.028220

GILD 0.028891 0.057143 0.026906 0.032046 0.030105 0.230470 0.042154 0.016764 0.030781 0.032162 0.034975 0.032445 0.031617 0.033702 0.021003

JPM 0.048398 0.065805 0.038356 0.047258 0.054766 0.042154 0.127442 0.027653 0.049041 0.068555 0.049036 0.032597 0.041645 0.038364 0.033168

KO 0.020706 0.020285 0.021385 0.026103 0.026286 0.016764 0.027653 0.053362 0.022847 0.026121 0.027759 0.025953 0.018689 0.022953 0.020577

LUV 0.037365 0.048216 0.031193 0.039905 0.047190 0.030781 0.049041 0.022847 0.138311 0.048528 0.036969 0.025762 0.043051 0.032155 0.023438

MA 0.046675 0.057188 0.032501 0.050994 0.062689 0.032162 0.068555 0.026121 0.048528 0.116744 0.049793 0.031913 0.049745 0.042009 0.041492

MSFT 0.042606 0.073389 0.037554 0.043187 0.042048 0.034975 0.049036 0.027759 0.036969 0.049793 0.114527 0.030579 0.053099 0.033850 0.028928

PFE 0.025994 0.031130 0.025261 0.029207 0.027026 0.032445 0.032597 0.025953 0.025762 0.031913 0.030579 0.075916 0.017928 0.028178 0.022933

TSLA 0.044706 0.067031 0.029679 0.044257 0.059955 0.031617 0.041645 0.018689 0.043051 0.049745 0.053099 0.017928 0.329399 0.030690 0.029405

UNH 0.030261 0.034342 0.027355 0.031657 0.029009 0.033702 0.038364 0.022953 0.032155 0.042009 0.033850 0.028178 0.030690 0.160524 0.022458

XOM 0.030249 0.026733 0.020312 0.025691 0.028220 0.021003 0.033168 0.020577 0.023438 0.041492 0.028928 0.022933 0.029405 0.022458 0.052893- Plotting the sample covariance matrix

plotting.plot_covariance(sample_cov, plot_correlation=True);

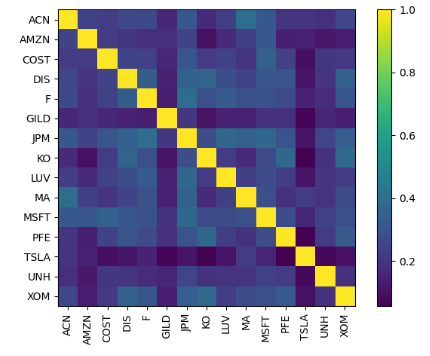

- Applying the isk_models.CovarianceShrinkage model to the stock prices

S = risk_models.CovarianceShrinkage(prices).ledoit_wolf()

plotting.plot_covariance(S, plot_correlation=True);

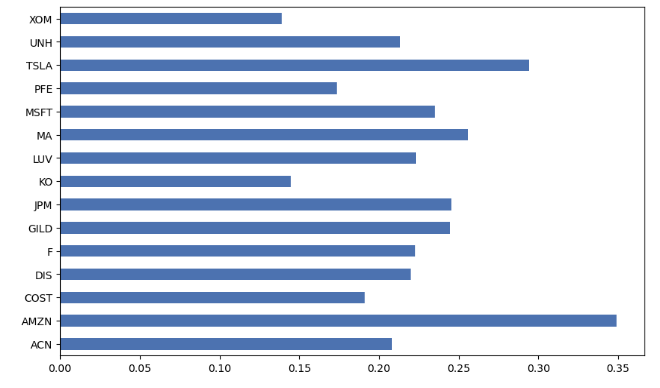

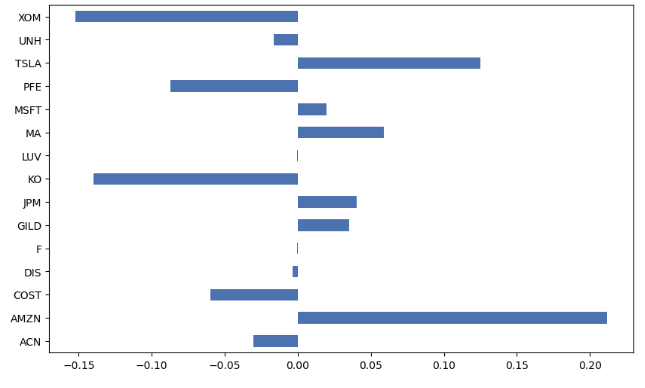

- Computing CAPM expected returns of portfolio 2

from pypfopt import expected_returns

mu = expected_returns.capm_return(prices)

mu

ACN 0.208064

AMZN 0.349090

COST 0.190865

DIS 0.219967

F 0.222607

GILD 0.244659

JPM 0.245611

KO 0.144716

LUV 0.223131

MA 0.255686

MSFT 0.234936

PFE 0.173457

TSLA 0.294081

UNH 0.213354

XOM 0.138895

Name: mkt, dtype: float64

mu.plot.barh(figsize=(10,6));

- Applying the EfficientFrontier IPO method with the Covariance Shrinkage risk model to portfolio 2

from pypfopt import EfficientFrontier

S = risk_models.CovarianceShrinkage(prices).ledoit_wolf()

# You don't have to provide expected returns in this case

ef = EfficientFrontier(None, S, weight_bounds=(None, None))

ef.min_volatility()

weights = ef.clean_weights()

weights

OrderedDict([('ACN', 0.22843),

('AMZN', 0.00616),

('COST', 0.09999),

('DIS', -0.02036),

('F', -0.02273),

('GILD', 0.04898),

('JPM', -0.04691),

('KO', 0.13455),

('LUV', 0.02459),

('MA', 0.23496),

('MSFT', -0.00235),

('PFE', 0.07144),

('TSLA', 0.12347),

('UNH', 0.0355),

('XOM', 0.08427)])

pd.Series(weights).plot.barh();

- Portfolio 2 performance

ef.portfolio_performance(verbose=True);

Annual volatility: 12.2%- Applying Discrete Allocation to portfolio 2

from pypfopt import DiscreteAllocation

latest_prices = prices.iloc[-1] # prices as of the day you are allocating

da = DiscreteAllocation(weights, latest_prices, total_portfolio_value=20000, short_ratio=0.3)

alloc, leftover = da.lp_portfolio()

print(f"Discrete allocation performed with ${leftover:.2f} leftover")

alloc

Discrete allocation performed with $58.92 leftover

{'ACN': 15,

'AMZN': 1,

'COST': 4,

'GILD': 11,

'KO': 39,

'LUV': 14,

'MA': 12,

'PFE': 32,

'TSLA': 12,

'UNH': 1,

'XOM': 13,

'F': -178,

'JPM': -25,

'MSFT': -2}- Performing sector mapping to include group industry constraints

sector_mapper = {

"MSFT": "Tech",

"AMZN": "Consumer Discretionary",

"KO": "Consumer Staples",

"MA": "Financial Services",

"COST": "Consumer Staples",

"LUV": "Aerospace",

"XOM": "Energy",

"PFE": "Healthcare",

"JPM": "Financial Services",

"UNH": "Healthcare",

"ACN": "Misc",

"DIS": "Media",

"GILD": "Healthcare",

"F": "Auto",

"TSLA": "Auto"

}

sector_lower = {

"Consumer Staples": 0.1, # at least 10% to staples

"Tech": 0.05 # at least 5% to tech

# For all other sectors, it will be assumed there is no lower bound

}

sector_upper = {

"Tech": 0.2,

"Aerospace":0.1,

"Energy": 0.1,

"Auto":0.15

}- Optimizing portfolio weights by adding constraints

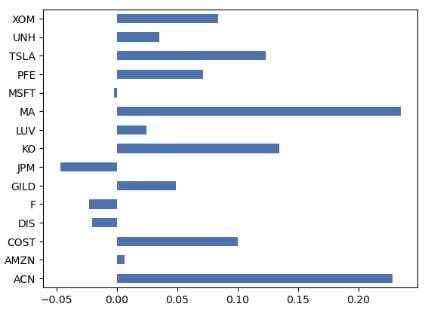

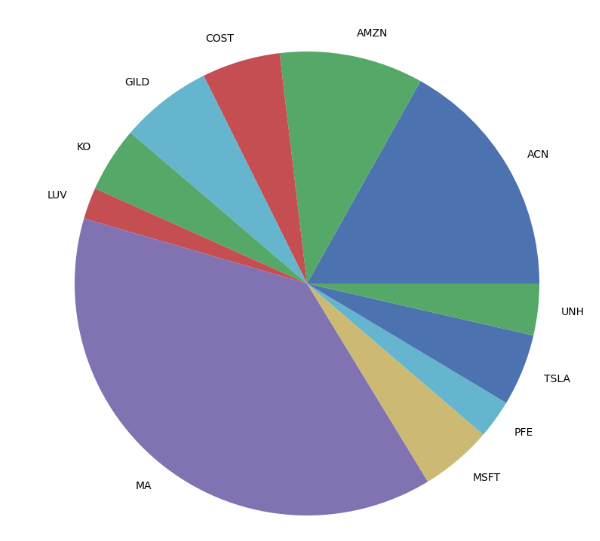

mu = expected_returns.capm_return(prices)

S = risk_models.CovarianceShrinkage(prices).ledoit_wolf()

ef = EfficientFrontier(mu, S) # weight_bounds automatically set to (0, 1)

ef.add_sector_constraints(sector_mapper, sector_lower, sector_upper)

amzn_index = ef.tickers.index("AMZN")

ef.add_constraint(lambda w: w[amzn_index] == 0.10)

tsla_index = ef.tickers.index("TSLA")

ef.add_constraint(lambda w: w[tsla_index] <= 0.05)

ef.add_constraint(lambda w: w[10] >= 0.05)

ef.max_sharpe()

weights = ef.clean_weights()- Plotting the ordered dictionary of optimized weights

weights

OrderedDict([('ACN', 0.16879),

('AMZN', 0.1),

('COST', 0.05458),

('DIS', 0.0),

('F', 0.0),

('GILD', 0.06404),

('JPM', 0.0),

('KO', 0.04542),

('LUV', 0.02193),

('MA', 0.3823),

('MSFT', 0.05),

('PFE', 0.02692),

('TSLA', 0.05),

('UNH', 0.03601),

('XOM', 0.0)])

pd.Series(weights).plot.pie(figsize=(10,10));

- Defining the optimal weight constraint per sector

for sector in set(sector_mapper.values()):

total_weight = 0

for t,w in weights.items():

if sector_mapper[t] == sector:

total_weight += w

print(f"{sector}: {total_weight:.3f}")

Financial Services: 0.382

Consumer Staples: 0.100

Aerospace: 0.022

Auto: 0.050

Misc: 0.169

Consumer Discretionary: 0.100

Media: 0.000

Healthcare: 0.127

Tech: 0.050

Energy: 0.000- Running EfficientFrontier IPO with sector constraints and efficient_risk

ef = EfficientFrontier(mu, S)

ef.add_sector_constraints(sector_mapper, sector_lower, sector_upper)

ef.efficient_risk(target_volatility=0.15)

weights = ef.clean_weights()

weights

OrderedDict([('ACN', 0.00967),

('AMZN', 0.16383),

('COST', 0.09374),

('DIS', 0.0),

('F', 0.0),

('GILD', 0.06523),

('JPM', 0.0),

('KO', 0.00626),

('LUV', 0.00466),

('MA', 0.444),

('MSFT', 0.05),

('PFE', 0.0),

('TSLA', 0.15),

('UNH', 0.01261),

('XOM', 0.0)])- Counting stocks with zero weights

num_small = len([k for k in weights if weights[k] <= 1e-4])

print(f"{num_small}/{len(ef.tickers)} tickers have zero weight")

5/15 tickers have zero weight- Examining the portfolio performance

ef.portfolio_performance(verbose=True);

Expected annual return: 26.7%

Annual volatility: 15.0%

Sharpe Ratio: 1.65- Adding the L2 regularization objective function with the tuning parameter gamma=0.1

from pypfopt import objective_functions

# You must always create a new efficient frontier object

ef = EfficientFrontier(mu, S)

ef.add_sector_constraints(sector_mapper, sector_lower, sector_upper)

ef.add_objective(objective_functions.L2_reg, gamma=0.1) # gamma is the tuning parameter

ef.efficient_risk(0.15)

weights = ef.clean_weights()

weights

OrderedDict([('ACN', 0.06921),

('AMZN', 0.18629),

('COST', 0.08355),

('DIS', 0.01489),

('F', 0.0),

('GILD', 0.07874),

('JPM', 0.04271),

('KO', 0.01645),

('LUV', 0.03281),

('MA', 0.23867),

('MSFT', 0.05),

('PFE', 0.0),

('TSLA', 0.15),

('UNH', 0.03668),

('XOM', 0.0)])

- Counting the zero-weight tickers

num_small = len([k for k in weights if weights[k] <= 1e-4])

print(f"{num_small}/{len(ef.tickers)} tickers have zero weight")

3/15 tickers have zero weight- Running EfficientFrontier by adding constraints, the efficient risk model, and L2 regularization with the tuning parameter gamma=1.0

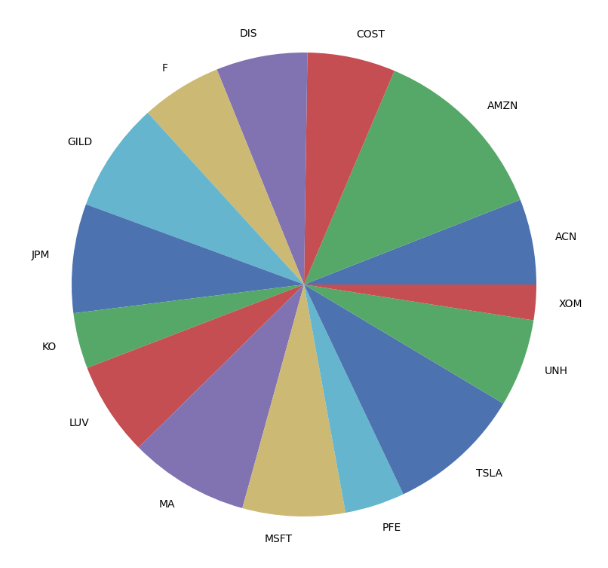

ef = EfficientFrontier(mu, S)

ef.add_sector_constraints(sector_mapper, sector_lower, sector_upper)

ef.add_objective(objective_functions.L2_reg, gamma=1) # gamma is the tuning parameter

ef.efficient_risk(0.15)

weights = ef.clean_weights()

weights

OrderedDict([('ACN', 0.05956),

('AMZN', 0.12684),

('COST', 0.06125),

('DIS', 0.06355),

('F', 0.05615),

('GILD', 0.07647),

('JPM', 0.07598),

('KO', 0.03875),

('LUV', 0.0654),

('MA', 0.08332),

('MSFT', 0.07136),

('PFE', 0.04172),

('TSLA', 0.09385),

('UNH', 0.06112),

('XOM', 0.02469)])

pd.Series(weights).plot.pie(figsize=(10, 10));

- Portfolio performance summary

ef.portfolio_performance(verbose=True);

Expected annual return: 24.2%

Annual volatility: 15.0%

Sharpe Ratio: 1.48- Running EfficientFrontier without weights bounds by adding the L2 regularization and the market-neutral efficient return with target_return=0.07

ef = EfficientFrontier(mu, S, weight_bounds=(None, None))

ef.add_objective(objective_functions.L2_reg)

ef.efficient_return(target_return=0.07, market_neutral=True)

weights = ef.clean_weights()

weights

OrderedDict([('ACN', -0.03031),

('AMZN', 0.21164),

('COST', -0.05977),

('DIS', -0.00357),

('F', -0.00038),

('GILD', 0.03495),

('JPM', 0.04047),

('KO', -0.13985),

('LUV', -0.00028),

('MA', 0.0588),

('MSFT', 0.01942),

('PFE', -0.08738),

('TSLA', 0.12484),

('UNH', -0.01647),

('XOM', -0.15212)])- Portfolio performance summary

ef.portfolio_performance(verbose=True);

Expected annual return: 7.0%

Annual volatility: 10.6%

Sharpe Ratio: 0.47- Plotting the optimized weights and the semicovariance matrix

pd.Series(weights).plot.barh(figsize=(10,6));

print(f"Net weight: {sum(weights.values()):.2f}")

Net weight: -0.00

semicov = risk_models.semicovariance(prices, benchmark=0)

plotting.plot_covariance(semicov);

- Running EfficientFrontier with semicov

ef = EfficientFrontier(mu, semicov)

ef.efficient_return(0.2)

weights = ef.clean_weights()

weights

OrderedDict([('ACN', 0.25277),

('AMZN', 0.0),

('COST', 0.08549),

('DIS', 0.0),

('F', 0.0),

('GILD', 0.01648),

('JPM', 0.0),

('KO', 0.14564),

('LUV', 0.0),

('MA', 0.31895),

('MSFT', 0.0),

('PFE', 0.05079),

('TSLA', 0.11332),

('UNH', 0.00218),

('XOM', 0.01438)])- Portfolio performance summary

ef.portfolio_performance(verbose=True);

Expected annual return: 22.0%

Annual volatility: 9.3%

Sharpe Ratio: 2.16

- Running EfficientSemivariance with expected returns while checking the portfolio performance

returns = expected_returns.returns_from_prices(prices)

returns = returns.dropna()

from pypfopt import EfficientSemivariance

es = EfficientSemivariance(mu, returns)

es.efficient_return(0.2)

es.portfolio_performance(verbose=True);

Expected annual return: 20.0%

Annual semi-deviation: 10.7%

Sortino Ratio: 1.69

es.weights = ef.weights

es.portfolio_performance(verbose=True);

xpected annual return: 22.0%

Annual semi-deviation: 14.0%

Sortino Ratio: 1.43- Printing expected returns per stock

returns = expected_returns.returns_from_prices(prices).dropna()

returns.head()

ACN AMZN COST DIS F GILD JPM KO LUV MA MSFT PFE TSLA UNH XOM

Date

2010-06-30 0.000000 0.005985 -0.014381 -0.024768 0.020243 -0.019731 -0.012143 -0.004172 0.000000 -0.017045 -0.012870 -0.001401 -0.002511 -0.008034 -0.003840

2010-07-01 -0.009573 0.015559 0.001277 -0.000317 0.048611 -0.004084 -0.013129 -0.001796 -0.010801 0.016652 0.006519 -0.002104 -0.078473 -0.019366 -0.008060

2010-07-02 -0.008882 -0.016402 -0.012205 -0.003493 -0.027436 0.021383 -0.006929 0.000400 -0.021838 0.000345 0.004749 -0.006325 -0.125683 0.016158 -0.000706

2010-07-06 0.012388 0.008430 -0.004241 0.010835 -0.011673 -0.002868 0.013955 0.007592 -0.011163 -0.013513 0.023636 0.010608 -0.160937 0.020848 0.015732

2010-07-07 0.022130 0.030620 0.005370 0.044767 0.042323 0.004889 0.050096 0.020623 0.062089 0.037694 0.020151 0.023093 -0.019243 0.010730 0.016881- Running EfficientFrontier with max Sharpe ratio while examining the portfolio performance

ef = EfficientFrontier(mu, S)

ef.max_sharpe()

weight_arr = ef.weights

ef.portfolio_performance(verbose=True);

Expected annual return: 25.1%

Annual volatility: 13.4%

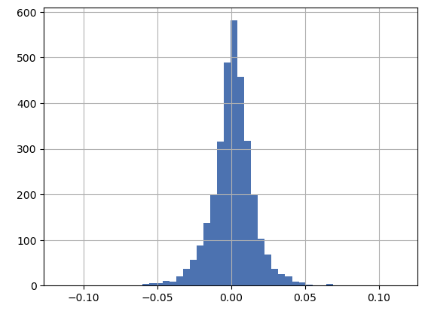

Sharpe Ratio: 1.73- Plotting the portfolio returns histogram

portfolio_rets = (returns * weight_arr).sum(axis=1)

portfolio_rets.hist(bins=50);

- Comparing VaR and CVaR

var = portfolio_rets.quantile(0.05)

cvar = portfolio_rets[portfolio_rets <= var].mean()

print("VaR: {:.2f}%".format(100*var))

print("CVaR: {:.2f}%".format(100*cvar))

VaR: -2.26%

CVaR: -3.35%- Running EfficientCVaR with the performance summary

from pypfopt import EfficientCVaR

ec = EfficientCVaR(mu, returns)

ec.efficient_risk(target_cvar=0.025)

ec.portfolio_performance(verbose=True);

Expected annual return: 23.2%

Conditional Value at Risk: 2.50%- Running the Critical Line Algorithm

from pypfopt import CLA, plotting

cla = CLA(mu, S)

cla.max_sharpe()

cla.portfolio_performance(verbose=True);

from pypfopt import CLA, plotting

cla = CLA(mu, S)

cla.max_sharpe()

cla.portfolio_performance(verbose=True);

Expected annual return: 24.8%

Annual volatility: 13.2%

Sharpe Ratio: 1.73

ax = plotting.plot_efficient_frontier(cla, showfig=False)

- Running Efficient Frontier with random portfolios (Monte Carlo)

n_samples = 10000

w = np.random.dirichlet(np.ones(len(mu)), n_samples)

rets = w.dot(mu)

stds = np.sqrt((w.T * (S @ w.T)).sum(axis=0))

sharpes = rets / stds

print("Sample portfolio returns:", rets)

print("Sample portfolio volatilities:", stds)

Sample portfolio returns: [0.23104048 0.24957187 0.22126853 ... 0.22765487 0.21850872 0.23138569]

Sample portfolio volatilities: 0 0.159978

1 0.163969

2 0.146534

3 0.158051

4 0.147951

...

9995 0.145396

9996 0.146341

9997 0.168378

9998 0.193611

9999 0.152335

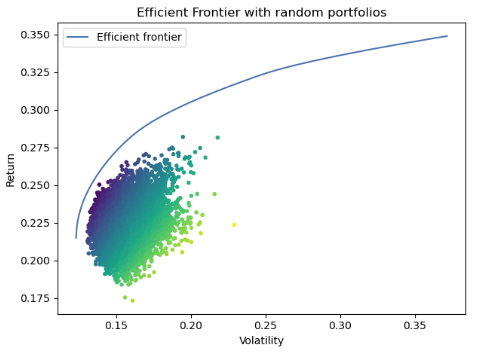

Length: 10000, dtype: float64# Plot efficient frontier with Monte Carlo sim

ef = EfficientFrontier(mu, S)

fig, ax = plt.subplots()

plotting.plot_efficient_frontier(ef, ax=ax, show_assets=False)

# Find and plot the tangency portfolio

ef2 = EfficientFrontier(mu, S)

ef2.max_sharpe()

ret_tangent, std_tangent, _ = ef2.portfolio_performance()

# Plot random portfolios

ax.scatter(stds, rets, marker=".", c=sharpes, cmap="viridis_r")

# Format

ax.set_title("Efficient Frontier with random portfolios")

ax.legend()

plt.tight_layout()

plt.show()

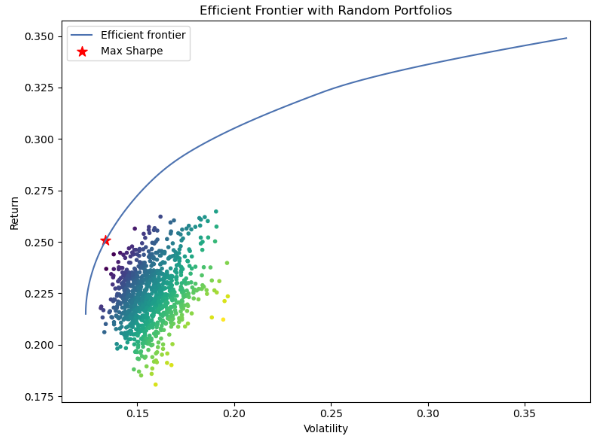

def plot_efficient_frontier_and_max_sharpe(mu, S):

# Optimize portfolio for maximal Sharpe ratio

ef = EfficientFrontier(mu, S)

fig, ax = plt.subplots(figsize=(8,6))

ef_max_sharpe = copy.deepcopy(ef)

plotting.plot_efficient_frontier(ef, ax=ax, show_assets=False)

# Find the max sharpe portfolio

ef_max_sharpe.max_sharpe(risk_free_rate=0.02)

ret_tangent, std_tangent, _ = ef_max_sharpe.portfolio_performance()

ax.scatter(std_tangent, ret_tangent, marker="*", s=100, c="r", label="Max Sharpe")

# Generate random portfolios

n_samples = 1000

w = np.random.dirichlet(np.ones(ef.n_assets), n_samples)

rets = w.dot(ef.expected_returns)

stds = np.sqrt(np.diag(w @ ef.cov_matrix @ w.T))

sharpes = rets / stds

ax.scatter(stds, rets, marker=".", c=sharpes, cmap="viridis_r")

# Output

ax.set_title("Efficient Frontier with Random Portfolios")

ax.legend()

plt.tight_layout()

plt.show()

plot_efficient_frontier_and_max_sharpe(mu, S)

Scenario 5: Mean-Variance MPT

Stocks: Well-diversified portfolio of 6 assets

stocks = ['MA', 'WM', 'AZN', 'SBUX', 'CLX', 'XOM']Time Horizon: start=”2013–01–01", end=”2023–04–06"

Methods: Monte Carlo Efficient Frontier

Objectives: max Sharpe ratio

Libraries: yfinance, PyPortfolioOpt

- Importing libraries and reading input stock data

from pypfopt.discrete_allocation import DiscreteAllocation, get_latest_prices

from pypfopt import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

from pypfopt import plotting

import copy

import numpy as np

import pandas as pd

import plotly.express as px

import matplotlib.pyplot as plt

import seaborn as sns

from pandas_datareader import data as pdr

import pandas_datareader.data as web

import datetime as dt

import yfinance as yf

stocks_df = yf.download("MA WM AZN SBUX CLX XOM", start="2013-01-01", end="2023-04-06")['Adj Close']

stocks_df.tail()

AZN CLX MA SBUX WM XOM

Date

2023-03-30 69.199997 154.440002 358.697296 101.320000 161.529999 109.489998

2023-03-31 69.410004 158.240005 362.840790 104.129997 163.169998 109.660004

2023-04-03 69.910004 156.750000 365.895966 104.849998 163.869995 116.129997

2023-04-04 70.250000 155.899994 363.329987 104.000000 163.529999 115.019997

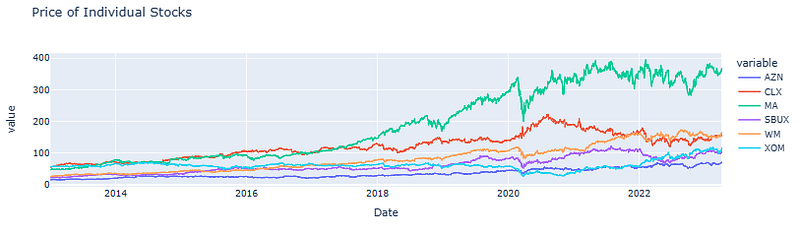

2023-04-05 72.050003 157.419998 363.790009 104.900002 162.820007 116.989998- Plotting the Adj Close price of individual stocks with Plotly

fig_price = px.line(stocks_df, title='Price of Individual Stocks')

fig_price.show()

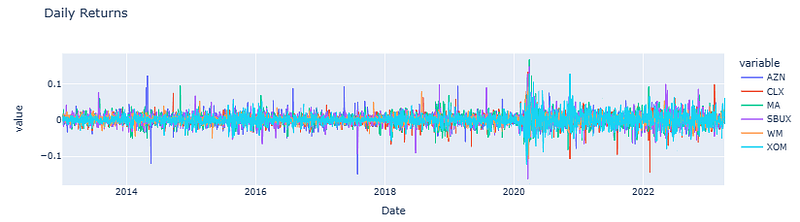

- Calculating and plotting daily returns of individual stocks

daily_returns = stocks_df.pct_change().dropna()

daily_returns.tail()

AZN CLX MA SBUX WM XOM

Date

2023-03-30 0.008158 -0.006817 -0.000751 0.006957 0.028591 0.004864

2023-03-31 0.003035 0.024605 0.011552 0.027734 0.010153 0.001553

2023-04-03 0.007204 -0.009416 0.008420 0.006914 0.004290 0.059000

2023-04-04 0.004863 -0.005423 -0.007013 -0.008107 -0.002075 -0.009558

2023-04-05 0.025623 0.009750 0.001266 0.008654 -0.004342 0.017127

- Calculating std of daily returns

daily_returns.std()

AZN 0.015491

CLX 0.013763

MA 0.017123

SBUX 0.016214

WM 0.011630

XOM 0.016923

dtype: float64

- Examining the seaborn distribution plot of daily returns

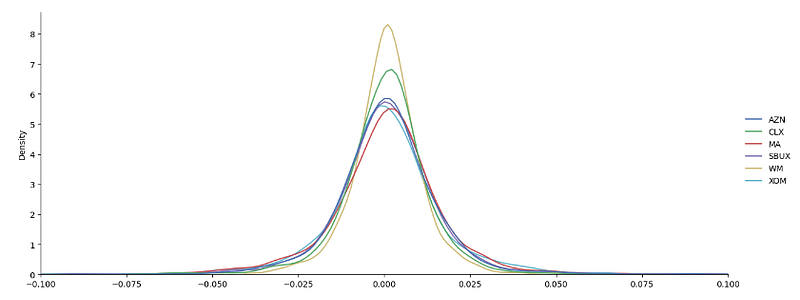

sns.displot(data=daily_returns[['AZN', 'CLX','MA','SBUX','WM','XOM']], kind = 'kde', aspect = 2.5)

plt.xlim(-0.1, 0.1)

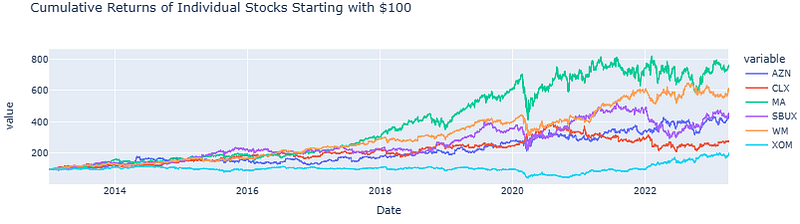

- Plotting the Cumulative Returns of Individual Stocks Starting with $100

def plot_cum_returns(data, title):

daily_cum_returns = (1 + daily_returns).cumprod()*100

fig = px.line(daily_cum_returns, title=title)

return fig

fig_cum_returns = plot_cum_returns(stocks_df, 'Cumulative Returns of Individual Stocks Starting with $100')

fig_cum_returns.show()

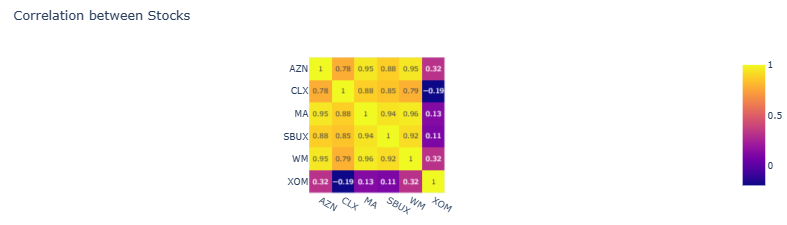

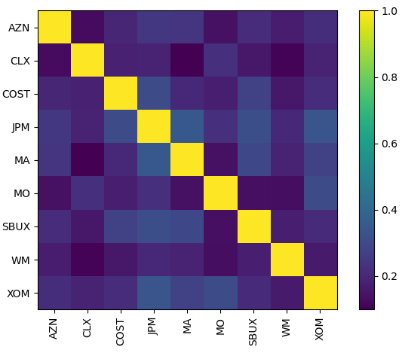

- Plotting the stock correlation matrix

corr_df = stocks_df.corr().round(2) # round to 2 decimal places

fig_corr = px.imshow(corr_df, text_auto=True, title = 'Correlation between Stocks')

fig_corr.show()

- Calculating expected returns and sample covariance matrix

# Calculate expected returns and sample covariance matrix

mu = expected_returns.mean_historical_return(stocks_df)

S = risk_models.sample_cov(stocks_df)

print(mu)

AZN 0.156955

CLX 0.106144

MA 0.218699

SBUX 0.159896

WM 0.193191

XOM 0.071530

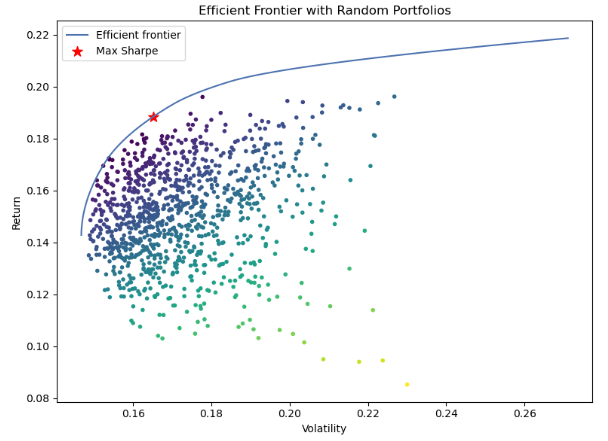

dtype: float64- Plotting the MPT efficient frontier with random portfolios vs max Sharpe ratio

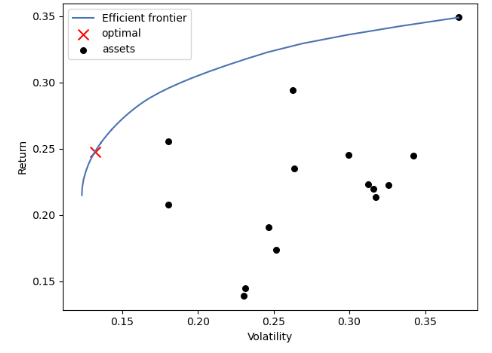

def plot_efficient_frontier_and_max_sharpe(mu, S):

# Optimize portfolio for maximal Sharpe ratio

ef = EfficientFrontier(mu, S)

fig, ax = plt.subplots(figsize=(8,6))

ef_max_sharpe = copy.deepcopy(ef)

plotting.plot_efficient_frontier(ef, ax=ax, show_assets=False)

# Find the max sharpe portfolio

ef_max_sharpe.max_sharpe(risk_free_rate=0.02)

ret_tangent, std_tangent, _ = ef_max_sharpe.portfolio_performance()

ax.scatter(std_tangent, ret_tangent, marker="*", s=100, c="r", label="Max Sharpe")

# Generate random portfolios

n_samples = 1000

w = np.random.dirichlet(np.ones(ef.n_assets), n_samples)

rets = w.dot(ef.expected_returns)

stds = np.sqrt(np.diag(w @ ef.cov_matrix @ w.T))

sharpes = rets / stds

ax.scatter(stds, rets, marker=".", c=sharpes, cmap="viridis_r")

# Output

ax.set_title("Efficient Frontier with Random Portfolios")

ax.legend()

plt.tight_layout()

plt.show()

plot_efficient_frontier_and_max_sharpe(mu, S)

- Calculating the optimized portfolio weights

ef = EfficientFrontier(mu, S)

ef.max_sharpe(risk_free_rate=0.02)

weights = ef.clean_weights()

print(weights)

OrderedDict([('AZN', 0.15466), ('CLX', 0.04592), ('MA', 0.18582), ('SBUX', 0.0), ('WM', 0.61359), ('XOM', 0.0)])

weights_df = pd.DataFrame.from_dict(weights, orient = 'index')

weights_df.columns = ['weights']

weights_df

weights

AZN 0.15466

CLX 0.04592

MA 0.18582

SBUX 0.00000

WM 0.61359

XOM 0.00000- Calculating the Expected annual return, Annual volatility, the Sharpe ratio, and the Optimized Portfolio

expected_annual_return, annual_volatility, sharpe_ratio = ef.portfolio_performance()

print('Expected annual return: {}%'.format((expected_annual_return*100).round(2)))

print('Annual volatility: {}%'.format((annual_volatility*100).round(2)))

print('Sharpe ratio: {}'.format(sharpe_ratio.round(2)))

Expected annual return: 18.83%

Annual volatility: 16.51%

Sharpe ratio: 1.02

stocks_df['Optimized Portfolio'] = 0

for ticker, weight in weights.items():

stocks_df['Optimized Portfolio'] += stocks_df[ticker]*weight

stocks_df.head()

AZN CLX MA SBUX WM XOM Optimized Portfolio

Date

2013-01-02 16.17679 55.996990 47.946114 22.947464 26.652275 57.639828 30.336200

2013-01-03 16.14661 55.845818 48.014702 23.101843 26.746429 57.535881 30.395108

2013-01-04 16.14661 56.465561 48.012817 23.235355 26.738588 57.802296 30.418405

2013-01-07 16.13320 56.238838 48.844879 23.247875 26.652275 57.133026 30.507573

2013-01-08 16.14661 56.405109 48.684109 23.206150 26.707193 57.490395 30.521105- Plotting the Cumulative Returns of Optimized Portfolio Starting with $100

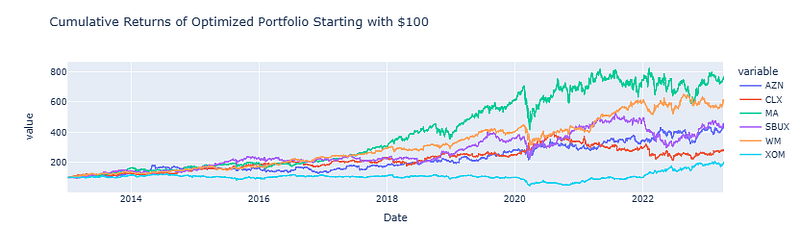

fig_cum_returns_optimized = plot_cum_returns(stocks_df['Optimized Portfolio'], 'Cumulative Returns of Optimized Portfolio Starting with $100')

fig_cum_returns_optimized.show()

Read More

- Mean-Variance Optimization

- Max Sharpe Ratio Portfolio Optimization for Stocks Using PyPortfolioOpt.ipynb

Scenario 6: Black-Litterman (BL) & Covariance Shrinkage

Stocks: Well-diversified portfolio of 9 assets vs SPY ETF benchmark

tickers = ["XOM", "AZN", "CLX", "MA", "SBUX", "WM", "MO", "JPM", "COST"]Time Horizon: 1993–2023, period=”max”

Methods: the Black-Litterman Model

Objectives: Combining BL & Risk Models

Libraries: yfinance, PyPortfolioOpt

- Importing libraries and reading input stock data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

tickers = ["XOM", "AZN", "CLX", "MA", "SBUX", "WM", "MO", "JPM", "COST"]

ohlc = yf.download(tickers, period="max")

prices = ohlc["Adj Close"]

prices.tail()

AZN CLX COST JPM MA MO SBUX WM XOM

Date

2023-03-31 69.410004 158.240005 496.869995 129.295288 362.840790 44.619999 104.129997 163.169998 109.660004

2023-04-03 69.910004 156.750000 497.029999 129.146454 365.895966 44.980000 104.849998 163.869995 116.129997

2023-04-04 70.250000 155.899994 497.730011 127.419998 363.329987 44.450001 104.000000 163.529999 115.019997

2023-04-05 72.050003 157.419998 497.130005 127.610001 363.790009 44.430000 104.900002 162.820007 116.989998

2023-04-06 72.339996 157.759995 485.980011 127.470001 361.470001 44.430000 104.680000 163.660004 115.050003- Comparing to the SPY ETF Adj Close price

market_prices = yf.download("SPY", period="max")["Adj Close"]

market_prices.head()

Date

1993-01-29 25.122337

1993-02-01 25.301022

1993-02-02 25.354639

1993-02-03 25.622641

1993-02-04 25.729851

Name: Adj Close, dtype: float64- Examining the market cap of individual stocks (cf. market capitalization-weighted portfolio)

mcaps = {}

import pandas_datareader as web

mcaps = web.get_quote_yahoo(tickers)['marketCap']

print(mcaps)

XOM 468366262272

AZN 225498234880

CLX 19487303680

MA 344568758272

SBUX 120308719616

WM 66571489280

MO 79358648320

JPM 373673230336

COST 215523885056

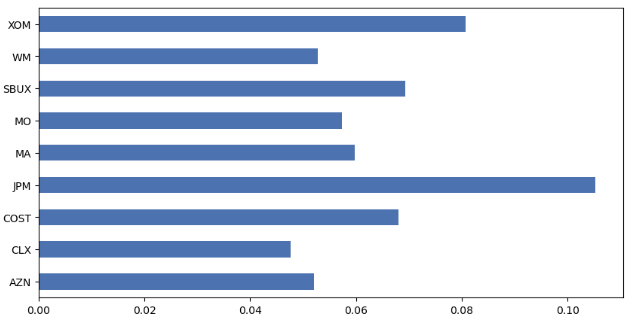

Name: marketCap, dtype: int64- Using the BL market implied risk aversion and the Covariance Shrinkage risk model

from pypfopt import black_litterman, risk_models

from pypfopt import BlackLittermanModel, plotting

S = risk_models.CovarianceShrinkage(prices).ledoit_wolf()

delta = black_litterman.market_implied_risk_aversion(market_prices)

delta

2.5290120773891447

- Plotting the stock correlation matrix

plotting.plot_covariance(S, plot_correlation=True);

- Calculating the BL market implied prior returns

market_prior = black_litterman.market_implied_prior_returns(mcaps, delta, S)

market_prior

AZN 0.052048

CLX 0.047593

COST 0.068028

JPM 0.105222

MA 0.059766

MO 0.057295

SBUX 0.069242

WM 0.052832

XOM 0.080756

dtype: float64- Plotting the BL market implied prior returns

market_prior.plot.barh(figsize=(10,5));

- Adding absolute views and view confidences options to the BL model

viewdict = {

"AZN": 0.40,

"CLX": 0.30,

"MA": 0.7,

"SBUX": 0.4,

"WM": 0.6,

"XOM": 0.2

}

bl = BlackLittermanModel(S, pi=market_prior, absolute_views=viewdict)

confidences = [

0.1,

0.1,

0.2,

0.1,

0.2,

0.3

]

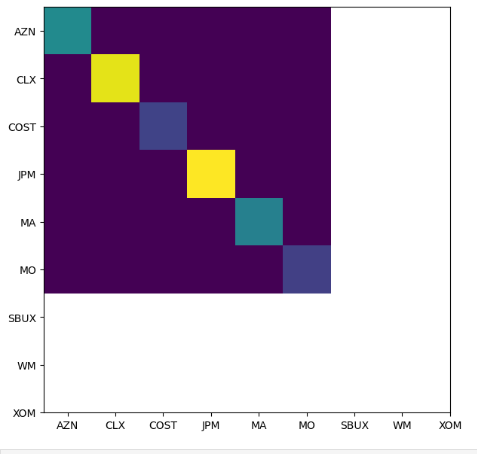

bl = BlackLittermanModel(S, pi=market_prior, absolute_views=viewdict, omega="idzorek", view_confidences=confidences)- The BL model outputs posterior estimates of the returns and covariance matrix

np.diag(bl.omega)

array([0.01546742, 0.03113534, 0.00648636, 0.03241998, 0.01408768,

0.00617762])

fig, ax = plt.subplots(figsize=(7,7))

im = ax.imshow(bl.omega)

ax.set_xticks(np.arange(len(bl.tickers)))

ax.set_yticks(np.arange(len(bl.tickers)))

ax.set_xticklabels(bl.tickers)

ax.set_yticklabels(bl.tickers)

plt.show()

Scenario 7: Hierarchical Risk Parity

Stocks: Well-diversified portfolio of 15 assets

tickers = ["BLK", "BAC", "AAPL", "TM", "WMT",

"JD", "INTU", "MA", "UL", "CVS",

"DIS", "AMD", "NVDA", "PBI", "TGT"]Time Horizon: 1993–2023, period=”max”

Methods: HRPOpt

Objectives: Portfolio Performance Analysis

Libraries: yfinance, PyPortfolioOpt

- Importing libraries and reading input stock data

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import yfinance as yf

import pypfopt

pypfopt.__version__

'1.5.3'

tickers = ["BLK", "BAC", "AAPL", "TM", "WMT",

"JD", "INTU", "MA", "UL", "CVS",

"DIS", "AMD", "NVDA", "PBI", "TGT"]

ohlc = yf.download(tickers, period="max")

prices = ohlc["Adj Close"]

prices.tail()

AAPL AMD BAC BLK CVS DIS INTU JD MA NVDA PBI TGT TM UL WMT

Date

2023-03-31 164.899994 98.010002 28.600000 669.119995 74.309998 100.129997 445.038116 43.239620 362.840790 277.769989 3.89 165.630005 141.690002 51.930000 147.449997

2023-04-03 166.169998 96.559998 28.590000 666.409973 76.089996 99.760002 439.887299 41.771702 365.895966 279.649994 3.83 166.059998 142.339996 52.700001 148.690002

2023-04-04 165.630005 95.870003 27.980000 659.109985 76.250000 99.570000 439.028839 41.220001 363.329987 274.529999 3.83 166.050003 142.139999 52.939999 147.229996

2023-04-05 163.759995 92.559998 27.639999 656.039978 77.750000 99.910004 438.369995 40.500000 363.790009 268.809998 3.67 165.240005 140.419998 53.320000 149.669998

2023-04-06 164.660004 92.470001 27.840000 656.400024 77.540001 99.970001 446.760010 40.759998 361.470001 270.369995 3.69 165.580002 138.869995 53.580002 150.800003- Calculating expected returns of individual stocks

from pypfopt import expected_returns

rets = expected_returns.returns_from_prices(prices)

rets.tail()

AAPL AMD BAC BLK CVS DIS INTU JD MA NVDA PBI TGT TM UL WMT

Date

2023-03-31 0.015644 0.001328 0.010601 0.012223 -0.005221 0.020693 0.013043 -0.011487 0.011552 0.014388 0.031830 0.033444 0.014826 -0.000962 0.012219

2023-04-03 0.007702 -0.014794 -0.000350 -0.004050 0.023954 -0.003695 -0.011574 -0.033948 0.008420 0.006768 -0.015424 0.002596 0.004587 0.014828 0.008410

2023-04-04 -0.003250 -0.007146 -0.021336 -0.010954 0.002103 -0.001905 -0.001952 -0.013208 -0.007013 -0.018309 0.000000 -0.000060 -0.001405 0.004554 -0.009819

2023-04-05 -0.011290 -0.034526 -0.012152 -0.004658 0.019672 0.003415 -0.001501 -0.017467 0.001266 -0.020836 -0.041775 -0.004878 -0.012101 0.007178 0.016573

2023-04-06 0.005496 -0.000972 0.007236 0.000549 -0.002701 0.000601 0.019139 0.006420 -0.006377 0.005803 0.005450 0.002058 -0.011038 0.004876 0.007550- Running HRPOpt

from pypfopt import HRPOpt

hrp = HRPOpt(rets)

hrp.optimize()

weights = hrp.clean_weights()

weights

OrderedDict([('AAPL', 0.035),

('AMD', 0.01749),

('BAC', 0.04611),

('BLK', 0.04911),

('CVS', 0.09596),

('DIS', 0.067),

('INTU', 0.03228),

('JD', 0.04162),

('MA', 0.0504),

('NVDA', 0.01686),

('PBI', 0.08016),

('TGT', 0.08755),

('TM', 0.11493),

('UL', 0.15636),

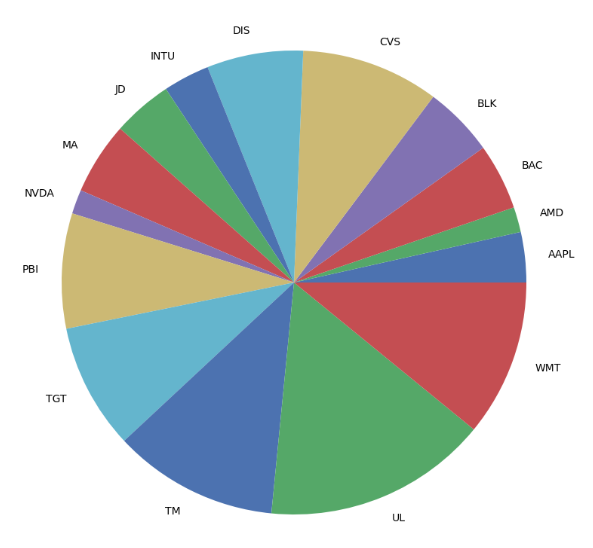

('WMT', 0.10916)])- Plotting the optimized portfolio weights

pd.Series(weights).plot.pie(figsize=(10, 10));

- Plotting the HRPOpt portfolio performance

hrp.portfolio_performance(verbose=True);

Expected annual return: 18.7%

Annual volatility: 19.1%

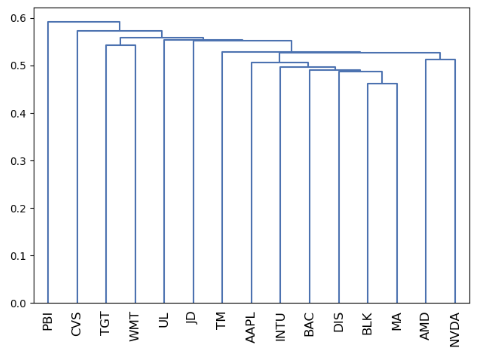

Sharpe Ratio: 0.87- Plotting the HRPOpt portfolio dendrogram

from pypfopt import plotting

plotting.plot_dendrogram(hrp);

Discussion

- In this article, different aspects of the investment portfolio optimization (IPO) process were studied in great detail.

- We addressed the following two problems: (1) For a given portfolio return, we estimated portfolio weights that minimize the risk level of the portfolio; (2) For a given portfolio risk level, we determined portfolio weights that maximize the portfolio’s return.

- We tested both the traditional mean-variance (MV) optimization (Markowitz, 1952) and Black-Litterman (BL) IPO.

- The main focus was on the PyPortfolioOpt library that implements portfolio optimization methods, including classical efficient frontier techniques and BL allocation, as well as more recent developments in the field like shrinkage and Hierarchical Risk Parity.

Final Word

- In this study we implemented several IPO models in a multi-asset portfolio context.

- We have shown how multi-objective IPO be used efficiently in the decision support for investment portfolio planning under market uncertainty and friction.

- The resulting portfolios are less risky, are more diversified across asset classes, and have less extreme asset allocations.

- By analyzing stock historical data across multiple assets, objectives and time horizons, it is possible to quantitatively evaluate financial investments such as stocks and make correct investment decisions.

- Python largely facilitates the calculation of expected returns/variance, and can quickly find the optimal product, which is of great value for the asset portfolio management.

Explore More

- Stock Portfolio Risk/Return Optimization

- Risk/Return QC via Portfolio Optimization — Current Positions of The Dividend Breeder

- Portfolio Optimization Risk/Return QC — Positions of Humble Div vs Dividend Glenn

- Risk/Return POA — Dr. Dividend’s Positions

- Bear vs. Bull Portfolio Risk/Return Optimization QC Analysis

- Portfolio Optimization of 20 Dividend Growth Stocks

- Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

- Joint Analysis of Bitcoin, Gold and Crude Oil Prices

- Risk-Aware Strategies for DCA Investors

- Oracle Monte Carlo Stock Simulations

- A Market-Neutral Strategy

- Dividend-NG-BTC Diversify Big Tech

- IQR-Based Log Price Volatility Ranking of Top 19 Blue Chips

- Towards Max(ROI/Risk) Trading

- Top 6 Reliability/Risk Engineering Learnings

References

- Markowitz, Harry, 1952, Portfolio selection, Journal of Finance 7, 1, 77–91.

- Qullamaggie || Risk & Reward, Win Rate

- Portfolio optimization using Python

- An Introduction to Portfolio Optimization in Python

- Enhancing Investment Strategies Portfolio Optimization and Analysis

- Portfolio Optimization in Python 101 — SciPy edition

- Unlock the Power of AI-Driven Portfolio Optimization: Discover How DDPG and PPO Can Transform Your Investments

- Understanding Portfolio Optimization with Mean-Variance Analysis in Python

- Portfolio Optimization: The Black-Litterman Allocation Method

- Leveraging Python for Your Investment Portfolio Optimization

- MULTI-OBJECTIVE PORTFOLIO OPTIMISATION

- Portfolio Optimization using Python and Modern Portfolio Theory

- Portfolio Optimization: A Beginner’s Guide.

- Portfolio Optimization using Monte Carlo Simulation

- Optimize portfolio for max Sharpe ratio plot it out with efficient frontier curve

Contacts

Embed Socials

Infographics