The Politicization of Copper, Nickel, Lithium & Iron-Ore Is Playing a Greater Role in Industrial Policies and Global Mining Projects

This story in an extension of what I recently wrote about The CEOs Leading in the Transition to Future Facing Commodities.

The critical metals discussed here — copper, nickel, lithium, iron-ore — pertain to geopolitical trends which have resulted in a worldwide politicization effort, notably in two latest news stories about Canada’s Indo-Pacific Strategy and a new trade route via Tunisia for Russian exports to South Korea.

For a deeper understanding of the geopolitical trends, I suggest first reading this story about A New Era of Adversarial Geopolitics Is Beginning on the Indo-Pacific & Arctic Oceans.

Copper Is A Game-Changer for China and Russia

The People’s Republic of China (PRC) has tremendous political, economic and strategic interests to maintain the strong momentum of the copper industry both now and in the future. With copper prices hitting an all-time high in 2020 the world’s largest consumer of copper raised the level of its production activity to its highest levels since 2011, while importing 656,483 tonnes in June 2020 while continuing at record pace all the way through 2021–H12022.

In addition to the expansion of its domestic copper production, China’s international influence over metals can be seen from in Africa (cobalt and lithium), Southeast Asia (nickel) and South America (copper).

The Las Bambas mine in Peru is a case in point. Already this year China’s MMG is facing restraint from the local indigenous population in Las Bambas.

The history of this relationship between the People’s Republic of China (PRC) and Peru’s indigenous groups is very relevant to the copper industry.

Ever since China’s MMG bought the Las Bambas mine from Glencore for $5.85 billion in April 2014 the mining company has faced continuous opposition from Peruvian indigenous groups over the control status of the mine’s production — e.g. force majeure declared in 2019 and roadblock obstruction in 2021 — that has devestated output for a country who consumes over half of the world’s copper.

There have been many reasons cited for why Las Bambas’ indigenous groups have put up a struggle against China’s mining activities and businesses, such as labor and payment concerns; environmental issues and local grievances toward the destruction of the mine itself.

But China’s MMG has stated that it wants to take this opportunity to contribute to Peru’s economy. They have strived to give the indigenous groups ample reasons to cooperate. They were consequently invited to have talks with the company on May 6, 2022.

Domestically, most of the copper is being dug out of extremely politically sensitive areas on the Chinese Mainland — Tibet, Xinjiang, Inner Mongolia — so the political costs to the Chinese Communist Party (CCP) are tremendous. Not to mention the cobalt and lithium being extracted out of risky countries in the Democractic Republic of Congo (DRC).

Deep pockets come with high political costs. The PRC also doesn’t want to give this advantage up to the USA or any other country. But the backlash we’ve seen from the oil and gas industry against Russia’s actions in Ukraine, prompts a new discussion about global metal miners and producers — and to what extent the PRC has influence over the geopolitical trends that are significant to the China’s industrial policies.

Valuable production assets of copper can be found in Chile and Ecuador but the Democratic Republic of Congo (DRC) are where some of the world’s largest copper mines are being planned for future facing commodities. To this point, geopolitical trends are likely to have an impact on companies such as BHP and Tesla that are both key players in the developments of future facing commodities.

Anyone following metals mining and political transitions would know that metals such as copper and nickel are correlated with Chile’s and Indonesia’s politics. Click on this link to learn why the new administation in Chile is getting tougher on copper mines.

It was reported that a huge sinkhole appeared in a field around a Canadian company Lundin Mining’s operation in Indonesia. For this reason the Chilean mining regulators forced the company to halt all mining activities in the area. An investigation is still being carried out as to what happened but it is being speculated that it is possible the area was over exploited by copper mining.

This is a classic story about how governments and companies are coming under more pressure as a result of Environment, Social, Governance (ESG) frameworks and the impacts on local communities from mining operations. Chile’s new administration under President Gariel Boric already finalized a new constitution after calls from the public to address social inequality.

It was announced by Indonesia’s investment minister that Indonesia President Joko Widodo revokes mining licenses. There were reportedly more than 2,000 mining permits were revoked due to the government’s land redistribution plan. Citing non-compliance from coal mining companies such as PT Bayan Resources, the government claims that the land redistributon plan will help level the playing field for newer enterprises in the mining sector.

Indonesian politics and economy are synonomous with mining operations, foreign investment, and a wide range of ethnic disputes over territories with natural resources. Battery metals have become quite an important part of Indonesia’s future economic development. It is also making them more vulnerable to sanctions on China and Russia.

The Widodo government is under pressure both domestically and internationally for how it is handling political opposition. It is being debated on whether Widodo would be willing to step down per the results of an upcoming democratic election in Indonesia. How and if there is a political transition in Indonesia would be a major sign for how some of the world’s most critical metals are supplied in the near-future.

The SCO Summit of 2022

Here I have compiled some of the most significant analyses about the results of the Shanghai Cooperation Organization (SCO) Summit in 2022:

- The growing mutual interests in trade between China and Russia’s Far Eastern region

- China and Russia want to disrupt oil markets by axing the US Dollar

- Russia’s invasion of Ukraine reveals divergences within Central Asia

- President Xi’s decision to not assist Russia’s war effort

- The dilemma or China’s gas supplies via Power of Sibera 2 pipeline

The Shanghai Cooperation Organization (SCO) is a regional initiative that promotes military and security cooperation as well as economic development, among other things of a multilateral nature.

It is a classic example of economic regionalism.

To illustrate further, all of the talk about economic regionalism, and the subsequent focus on regional development is over-sold by political analysts and economists alike.

Commodities are global in nature. The only attention being truly paid to regional development is about large investments in infrastructure — these investments do not seek to enhance regional connectivity, but give an advantage to a producing country so that it can more efficiently transport raw materials to markets far away from the original source.

This is the essence of the Arctic Strategy, Belt and Road Initiative (BRI) and Indo-Pacific Strategy: all of them revolve around the maritime domain while also seeking defense mechanisms through military cooperation.

In my view, this is the future trends for which the world is headed. Whereas countries are rethinking industrial policies, while also emphasizing the need for new security measures to industrial assets as a result of nascent, unpredictable cyber threats from adversaries. An adversary, or group of adversaries, can target an industrial asset because it has immediate results, and which the perpetrator can determine the trajectory of action on the cyberattack. Governments, corporations or even individuals could be consumed in a cyberattack that effectively shuts down an industrial asset or network which it is operating on.

It’s very important to undertand this phenomenon in the context of sanctions on Russia and China. Under the backdrop of a resurgence in global commodities, the legal aspects of Russia’s sanctions include industrial asset seizures and targeted oil and gas mergers with Russia’s national companies. Both of these aspects have a cybersecurity dimension

What this means at a political level is that Russia intends to transform its industrial policies in a way that favors the “anti-West” rhetoric; from a geographical point of view, raw materials are located in vulnerable areas where supply chains are being disrupted by sanctions. This is why Russia must expand its “sovereignty” over global commodities.

Simply put, this is Russia’s geopolitical objective within the context of global commodities, hence the critical nature of the China-Russia relationship. China basically has the same geopolitical objective within the context of global commodities, which is why the two countries could seek to dominate raw materials in some of the world’s most vulnerable areas.

The question of whether China and Russia will align industrial policies shall be determined by the outcomes of the Arctic Strategy and BRI — not the Shanghai Cooperation Organization (SCO) — and how the defense and security interests of the United States converge with other actors in the Indo-Pacific. This is the long game of geopolitics for decades to come.

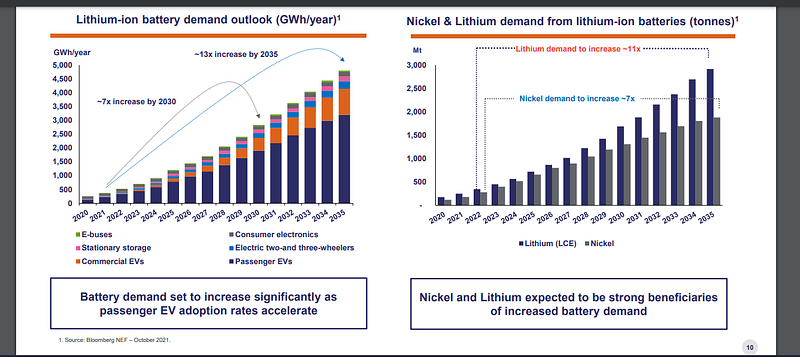

LME Regulations on Nickel & Lithium Trading

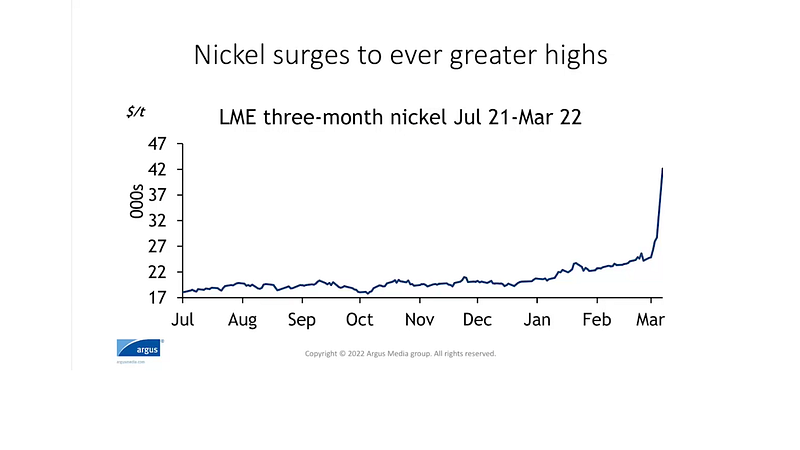

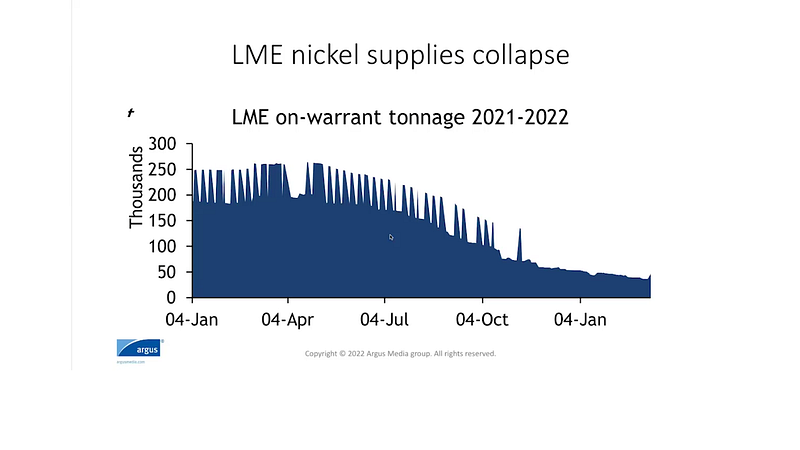

In March 2022, there was a substantial crisis for China’s nickel trading giant — Tsingshan Holding Group — led by Chinese Wenzhounese billonaire Xiang Guangda who bet zealously on the growth of nickel production and supply this year at the London Metals Exchange (LME). When the price of nickel surpassed $100,000 per tonne the LME had to stop nickel trading at an instant.

In response to the EV battery production shortages, Tsingshan Holding Group devised a strategy that would keep prices lower, and thus allow for cheaper production of battery ingredients, especially from areas of Southeast Asia like Indonesia. But unfortuantely the events in Ukraine have caused the markets to act in an extraordinary way — a way that was adverse to Tsingshan’s nickel production investment strategy.

Since March 8, 2022, international investors and bankers have been awaiting Tsingshan’s response. It wasn’t until March 15, 2022, that they finally announced an agreement with bank creditors, such as JP Morgan and CCBI Global Markets, to discuss a “standby secured liquidity facility” arrangement to solve the company’s problems. This agreement is being referred to by most sources as a standstill agreement for which it is expected that the haphazard nickel trading will once again stabilize.

The company released a statement, saying:

“As an integral feature of the agreement, there is provision for the existing hedge positions to be reduced by the Tsingshan group in a fair and orderly manner as abnormal market conditions subside.”

Any new rules will be applied by regulatory authorties in Great Britain: the Financial Conduct Authority (FCA) and the Bank of England.

This story about China’s Tsingshan Holdings Group sheds light on how critical the metals markets are becoming for global finance and investment banks.

With China’s capabilities to produce cheaply in Indonesia, and raise capital from the world’s largest international banks and financial institutions, I’d call this a recipe for stability and disaster offset by the production and supply of metals. This essential truth is even hidden within this story about the nickel industry: the whole point of the standstill agreement was to stabilize pricing and trading mechanisms to prevent a disaster in global markets.

Next, this story continues with a scheme implementation deed (SID) agreed to in December 2021 when Australia’s IGO Ltd sought to acquire another Australian metals miner outfit, Western Areas Ltd, to boost its nickel and lithium portfolio. By adding some of the highest-grade nickel and lithium mines that Western Australia has to offer, IGO would be able to significantly take on the metal production base that is crucial to Electric Vehicles (EV) and Clean Energy Technologies.

Originally valued at A$1.096 billion, IGO would takeover Western Areas Ltd assets with a 100% interest in the mines in Western Australia. IGO appeared to be on its way to a massive acquisition that would put it at the top of Western Australia’s nickel production capacity. Until recently when the nickel trading mechanisms on the London Metals Exchange (LME) got out of control, causing China’s Tsingshan Holdings Group to hedge production against a surging nickel price that hit a whopping $100,000 a tonne.

Due to the events on LME the company was expecting only a “relatively short delay” for the takeover deal at first. It was then reported on April 5, 2022, that IGO would completely back out of the deal to acquire Western Areas — citing only an independent expert report as the rationale for foregoing the acquisition.

Russia’s Proposed Metal Merger

Norilsk Nickel «Норникеля» is a Class 1 nickel producer and the world’s largest producer of the base metal. The company is also Europe’s largest supply of nickel, which has deterred the European Union (EU) from applying sanctions on the company and its affiliates. But it didn’t stop the United Kingdom (UK) from sanctioning Nornickel executive Vladimir Potanine on 29 June 2022.

Potanine responded after the sanctions were announed by the UK goverment with this statement:

We have a fairly huge volume of mutual relations with UK banks and UK entities that arranged loans for us. Therefore, we are analyzing now the extent of the effect on the company. We definitely understand there will be no negative impact on its stability but certain loans will probably have to be repaid in advance.

Due to sanctions Nornickel is seeking to merge with Rusal «Русала» in what has been heralded by Potanine as a “national champion” to defend Russia’s nickel industry against the economic impact of sanctions from USA and EU as a result of the war in Ukraine.

According to Reuters, the metal merger has the potential to reach a revenue of $30 billion due to the two companies’ exposure to palladium, nickel and aluminum. These three metals are crucial to the global economy as the world strives for Energy Transition and a more commodity-centric investor marketplace.

It was reported by several sources that the sanctioned Nornickel executive, Vladimir Potanin, must step down as an executive of the company in order the the Nornickel-Rusal merger to be successfully completed.

Mining.com then reported on 22 July 2022 that the London Metals Exchange (LME) announced publicly that it would not immediately ban the prosposed metal merger and would instead carry out an investigation of the sanctions.

An LME spokesperson issued this statement to S&P Global Platts, “We are looking into the detail of the sanctions and what it may mean for the LME, its participants and Norilsk brands.” But this hasn’t affected the UK government’s position on sanctioning one of Russia’s richest persons.

Potanin continues to amass wealth as he supports Putin’s regime, acquiring PJSC ROSBANK, and shares in JSC Tinkoff Bank in the period since Russia’s invasion of Ukraine. As long as Putin continues his abhorrent assault on Ukraine, we will use sanctions to weaken the Russian war machine. Today’s sanctions show that nothing and no one is off the table, including Putin’s inner circle.

To understand the significance of this massive metal merger, however, requires an in-depth look at how geopolitics and commodities coalesce into a country’s overall strategy.

In the case of Russia, combating sanctions is a key part of the country’s economic development in the future. This metal merger intends to succeed in the strategy of combining two large (national) companies into one massive entity controlled by the Russian state itself.

These metals are becoming so valuable to the global economy that Russia (plus others) must carefully consider how its industries will avoid sanctions from the United States and European Union. Avoiding the massive blow from sanctions due to its invasion of Ukraine would be a high achievement in their overall strategy to defend Russia’s nationalist policies.

However, the company would be forced to reconsider its supply chains in the aftermath of sanctions as a broad base of Russian industries have been hit with sanctions from the United States and European Union. For instance, Argus Media reported that Nornickel has considered re-structuring its logistical partners by sending more shipment through the Middle East and North Africa (MENA), an area which is critical to the sustainability of Russian exports through the eastern corridor.

The talks about reconfiguring supply routes has come in tandem with one of the Russia’s strategic dilemmas: the Arctic Strategy. Russia’s Northern Sea Route (part of the Arctic Strategy) seeks to increase exports via transshipments of products through North African ports that will reach Asian markets that have a high demand for the base metals of nickel, aluminum and copper, where Nornickel and Rusal could increase production from plants on the Kola Peninsula and in Monchegorsk of the Murmansk region on the Arctic Ocean.

Iron-Ore Is A Massive Opportunity

On 18 May 2022 Kazakhstan’s largest iron-ore exporter and enricher, Sokolov-Sarybai Mining Production Association (SSGPO), decided to temporarily stop supplying Russia’s Magnitogorsk Iron and Steelworks (MMK) located in Siberia.

Russia’s MMK responded by blaming the situation on USA and Western sanctions.

Although the World Steel Association has projected low growth for steel demand, ~0.4% in 2022 with a rise of ~2.2% in 2023, the Short Range Outlook was compiled in response to an uncertain atmosphere as a result of geopolitcal tensions and China’s recovery from Covid-19 lockdowns in Shanghai.

Meanwhile, energy has taken the center stage over Europe’s dependency for Russian natural gas. Gazprom reduced natural gas supplies to Germany by 33% while also disrupting supplies to Italy’s Eni via the Nord Stream pipeline. It was reported that this was due to operational issues with some of the pipeline’s turbines at the Portovaya compressor station in the Baltic Sea, and, due to the maintanence issues, Gazprom blamed Siemens Energy for withdrawing its services to the pipeline in response to Western sanctions.

Iron-ore mining projects in Guinea (more on this case next) reveal that strong demand for metals is going to see an upside during the global commodity supercycle, irrespective of geopolitics, as countries like China and Australia compete for supply and demand of iron-ore and other metals.

That’s why this most recent situation between Kazakhstan and Russia should not be taken lightly. Just look at what happend on the Caspian Pipeline Consortium to understand the geopolitical nature of energy and commodities right now.

Due to Russia-Ukraine war, energy and commodities are the biggest concerns of the global economy. Germany is now firing up coal plants, Canada’s mining company issued a preliminary economic assessment (PEA) for its Copper World Complex located in Arizona of the United States, and France’s President Macron is in talks with Romania to revive an old railroad transportation route from Odesa to the Danube River to increase grain exports from Ukraine to international markets.

All of this economic activity is occuring under the backdrop of USA and European sanctions on Russia’s critical LNG industry, such as Novatek’s Arctic LNG 2 project.

The St. Petersburg International Economic Forum is being used as a stage for Russia to show the world how it is commited to its political agenda.

In the words of Russia President Vladimir Putin:

The Forum’s anniversary is taking place at a difficult time for the entire international community. The mistakes of Western countries in economic policy over many years and illegitimate sanctions have led to a wave of global inflation, the disruption of usual supply chains, and a sharp increase in poverty and food shortages. Yet, as can be the case, along with these challenges, new prospects are emerging. This is why the Forum’s slogan — New Opportunities in a New World — seems so relevant.

“New Opportunities in a New World” sounds like classic revisionism, but it also indicates how important Russia is — or at least thinks it is — to the global commodity supercycle. For instance, China’s President and Chairman Xi Jin Ping stood by Russia at the St. Petersburg Forum in claiming that “the era of the unipolar world” being led by the United States was over.

While most people will understandably focus on the inhumane war effort launched by Russia against Ukraine, with the surge of international refugees and internally displaced peoples (IDPs) all over the world, the global commodity supercyle is driving the economic power of countries like Russia.

This allows Russua to revise the whole situation in the post-Soviet territories of Central Asia. Kazakhstan is worried — extremely. It has had to use the St. Petersburg Forum as a way to committ to the world its territorial integrity in the face of looming Russia threat on its border.

This is in many ways of desperate plea to the world — The United States? — for promoting the cause of Kazakhstan’s sovereignty for a country that has much to lose from USA and European sanctions on Russia’s oil and gas industries.

Australia’s and China’s Simandou Mine in Guinea

Iron ore production at the Simadou mine in southeast Guinea began in 2015. It is being developed by Rio Tinto, Aluminum Corporation of China, the government of Guinea and the International Finance Corporation (IFC).

The Simandou project demands increased investments in Guinea’s infrastructure development as the production takes place in a distant, mountainous region. The new trans-Guinean railway was propsed to link up Simandou to the coastal parts of Guinea. Since then, the Winning Consortium Simandou (WCS) was formed to build the railway and port. WCS hired China Railway 18th Bureau Group Co Ltd for the work.

Ecological issues with a critically endangered chimpanzee have raised concerns about the railway and port building projects, but it seems that the government of Guinea was not happy with the terms of the agreement with Rio Tinto and Chinalco all along.

A significant development to this story was the military coup carried out in Guinea on 5 September 2021. Read about it here.

New terms of the agreement were established on 28 March 2022 whereby the government of Guinea would take full control of the railway and port after the project was completed. It was later announced that the government of Guinea reserved the right to cancel mining licenses if the iron-ore project was not completed by 2024–2025.

David Thomas, writing for African Business, claims that one of the key reasons for the Simandou iron-ore project’s delay is because of a lack of agreement on the trans-Guinean railway between Rio Tinto and the government in Guinea. Thomas indicates that the main purpose of the project is to mine iron-ore, that is then to be sold to China in an effort for the country to decrease exposure to Australia’s massive iron-ore exports.

Thus, the Simandou iron-ore project has major geopolitical implications — not only for the entire region of Africa, but also for the growing tensions between China and Australia.

Another issue was put into focus by Diawo Barry of The Africa Report of which Rio Tinto has run into investor fears over ESG concerns in developing the iron-ore project. The inability to get funds for building the railway and ports will have an effect on the company’s timeline to complete the project.

ExxonMobil and Rio Tinto are two of the world’s largest companies. The examples of Guyana and Guinea reveal how each company is dealing with ESG concerns.

The Greater Guyana Initiative was established by ExxonMobil, Hess and CNOOC to commit funds to projects that contribute to the sustainable development of Guyana’s economy and people, including regional initiatives that suppoer development work in the country’s modern agriculture and health.

ExxonMobil’s offshore discoveries are also going to provide jobs for 3,500 Guyanese people while directly working with a number of local suppliers on the projects.

Rio Tinto, on the other hand, can’t seem to get anything right for the local governments and population in regards to mining projects abroad — Papua New Guinea, Mongolia and Guinea (West Africa) are all cases that have caused Rio Tinto to take major losses. It’s even plausible to say that all of the cases have destroyed Rio Tinto’s image and put it on the forefront of ESG corporate accountability for mining activities around the world.

Concluding Thoughts

The examples of China and Russia do indeed prove how crucial commodities are becoming to geopolitics. One aspect of the China-Russia relationship depends on how much damage the sanctions from the United States and European Union will cause to the global metals industries.

The world has seen numerous export bans on critical inputs to fertilizer and food production since the outbreak of Covid-19 in 2020. This circumstance has created a massive ripple effect on economies of the underdeveloped and undeveloped worlds, where civil unrest has become a source of tension for government stability in many countries of Middle East, Sub-Saharan Africa and South Asia.

Ukraine’s agriculture production has had an impact on the world’s food supply, notably due to wheat cultivation and production. Sanctions on China would only exacerbate the ongoing global food crisis which has seen significant strain to economic production all over the world, including in developing economies, where the historical highs in fertilizer prices has led to high crop prices and thus higher consumer prices at the wholesale and broader marketplace levels.

Imagine if the same tactics were applied by countries to target China’s metals production and supply? It would be disastorous for the Global Economy, as the massive rollout of EVs, renewable energy installations and more construction projects require massive amounts of copper and nickel — among other metals.

As the world is grappling with the global food crisis the world needs Brazil to produce more food, because it is already one of the world’s largest food-producing countries along with Ukraine.

These trends are part of the much larger geopolitical trends that have been kickstarted by the global COVID-19 pandemic. The global pandemic has caused several countries to unravel, with socio-political instability that was building up for decades, and causing the global economy to be shaken up with uncertainties, putting the world’s largest companies in some of the most vulnerable areas.

I argue that these issues about ESG and global mining projects, as well as how indigenous groups and governments are responding to the Global Commodity Supercycle, are defined by a new Paradigm Shift.

The aspects of producer economies, the areas where they operate and the indigenous groups’ issues that are specific to their communities, all of which are at the nexus of commodities and geopolitics in the future.

All of these trends, including the references and stories I’ve included here, should give us a broader understanding of what’s happening in geopolitics and the global economy after the COVID-19 pandemic.

Whether or not we can overcome our pre-conceived ideas about Energy and Commodities is going to be a key problem facing the world’s population after the global pandemic. We need to get more serious about Climate Change, but also look at how the world’s most valuable commodities are going to be needed and secured in the future — hence the critical nature of Future-Facing Commodities.

I’ll be publishing The Weekend Brief (TWB) regularly touching on aspects of the global markets (including stock markets) which are at the nexus of tech, industrials and global commodities. Please follow the publication Areas & Producers to read more content about the future of core areas and critical producers of the global economy.