The CEOs Leading in the Transition to Future Facing Commodities

On the new of Disney’s Bob Iger returning to the head of The Walt Disney Company I have decided to put together this content piece about CEO Transitions and the Future Facing Commodities.

I introduce and explain the situations of three CEOs: Mike Henry of BHP Group; Ken Seitz of Nutrien Ltd.; and Elon Musk of Tesla.

All three of these CEOs are leading in one or more aspects of the transition to Future Facing Commodities — copper, nickel, potash.

— Why is the world’s largest metal miner BHP Group pushing for future facing commodities on the frontlines of ESG?

A sign of the times for the global economy. Not only was ESG a driving topic for all industries at the end of 2019, but BHP’s rival Rio Tinto was slammed by the global public for its mining blunder in Papua New Guinea in 2020, in addition to ongoing disputes over financing issues in Mongolia’s Oyu Tolgoi copper mine.

BHP group plans to mine and produce metals while taking a more sustainable and environmental focus on their operations globally. There are basically three main commodities in this future facing commodities space: copper, nickel and potash. The former two are both metals directly related to metal mining and stainless steel production, while the latter is primarily used as a source of fertilizer.

Now for more on the role of BHP Group CEO Mike Henry…

Backstory: Arriving At A Critical Juncture — “We’ve needed to demonstrate ESG leadership over time. Not only do we need to be aware of what the needs of today are; we need to be able to look into the future and gauge how societal expectations are likely to change.”

The newest CEO of BHP couldn’t have arrived at a more critical time for the world’s largest metal miner. Mike Henry was officially transitioned into CEO of BHP Group in November 2019 when it was announced that he would succeed then-CEO Andrew Mackenzie. It should be pointed out that Mr. Henry had already been working for BHP in a variety of roles since 2003. This is in contrast to what happend with the recent CEO transition at the world’s largest fertilizer company Nutrien Ltd.

There was high speculation among reporting agencies and commodity analysts about a Nutrien Ltd.-BHP Group partnership for the development of a potash mine in Jansen, Saskatchewan, Canada. It’s true that BHP has been divesting its oil and gas assets for “future facing commodities” such as potash. In a statement to The Financial Post the company said “Potash provides BHP with increased leverage to key global mega-trends, including rising population, changing diets, decarbonization and improving environmental stewardship.” However, most of the talk about a proposed partnership or joint-venture has died down since sanctions were targeted at Belarus’ potash industry in December 2021.

Transition: Facing Crises and Sustainability Goals — “The reality of our industry is that you can’t sacrifice one E, S and G, for another, we need to hold high standards across all three of those dimensions…as the world seeks to de-carbonize, the act of de-carbonization is going to be incredibly metals-intensive.”

Mike Henry assumed the role of CEO on Janurary 1, 2020, as the former CEO of BHP told the public on his way out the door, “Fresh leadership will deliver an acceleration…that will come from BHP’s next wave of transformation. Choosing the right time to retire has not been an easy decision, however the Company is in a good position. I am confident Mike and BHP will seize the many opportunities that lie ahead.”

Little did anyone know what really lied ahead for the company: the global outbreak of COVID-19.

But before the global pandemic it was becoming well known to the public that Mr. Henry was “fully committed” to BHP’s climate change action plan and sustainability strategy. This was indicated by merger talks with Australia’s Woodside Petroleum for BHP’s oil and gas assets in the Gulf of Mexico and Western Australia. Not only is this about lowering the company’s GHG emissions and carbon footprint, as the name of the game since the Financial Times Mining Summit on October 8, 2021, has been about the company’s push to explore and produce future facing commodities.

Transformation: Future Facing Commodities Concept — “We will be led by what’s happening in the world around us.”

No wonder CEO Mike Henry has treaded carefully when discussing the nature of the company’s expansion into future facing commodities — copper, nickel and potash. The concept is still new to most people in the global economy and public sectors. It has already become synonomous in global business news with “tougher jurisdictions” that are associated with geopolitics and the global economy. Nevertheless, Mr. Henry told the FT Mining Summit in 2021 that BHP Group wants half of its revenues to come from the production and exports of these future facing commodities by 2030.

This implies that that the company will have to venture out to new areas containing the copper, nickel and potash production capabilities desired for such results.

It’s already known that the company has valuable production assets in Chile and Ecuador. So what’s uncertain at this point is how the company plans to expand into other places, for instance the Democratic Republic of Congo (DRC), where some of the world’s largest copper mines are available. To this point, geopolitical trends are likely to have an impact on BHP Group’s strategy to produce more copper, nickel and potash — witness recent events in China’s metal industry to explain this essential truth.

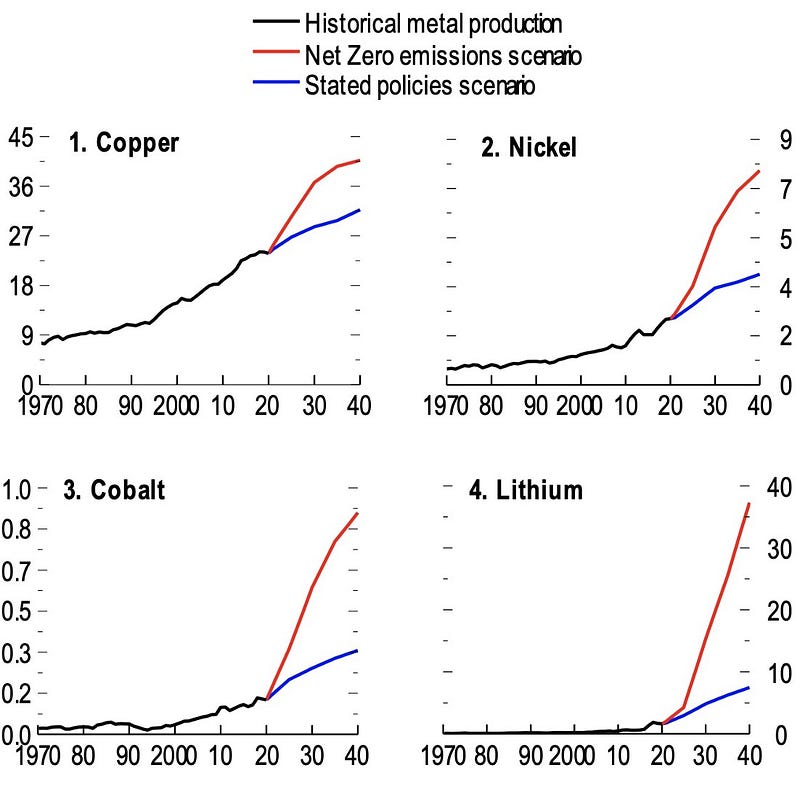

Opportunity: A More Profitable and Sustainable Future? — “For the world to de-carbonize it’s going to need a lot more metals, so something like two-times as much copper in the next thirty years…four-times as much nickel…two-times as much steel, and I think that’s an underappreciated fact.”

BHP Group intends to produce more metals while adhering to ESG practices and GHG emissions reductions. That’s why the company believes producing future facing commodities is not only a more profitable venture but also a sustainable option going forward. In an interview with CNBC’s David Faber on March 4, 2021, CEO Mike Henry elaborated on the company’s climate investment program established in 2019, which he claimed gave the company “the lowest emissions intensity footprint of any of the major mining companies…in terms of Scope 1 and Scope 2 emissions…with a $400 million climate investment program” to reach Net Zero by 2050.

Along with the company’s ambitions to be more sustainable, however, comes with an increase in mining activity that was aided by a sharp demand for commodities around the world in 2021–2022. In early 2022, it was reported that BHP Group profits would increase to $9.72 billon for the first half of 2022, compared to $6.20 billion in the first half of 2021. This is mostly attributed to a booming global demand for metals, iron ore and renewable energy products.

Explanation: Future Facing Commodities and Their Contributions to Sustainable Development — “I believe a comprehensive focus on ESG is actually going to play to BHP’s advantage.”

What all three of these future facing commodities have in common are their connections to the Energy Transition, with a growing demand for Clean Energy Technologies and Electric Vehicles (EV). Nickel is a critical battery material; Copper conducts the electricity for a wide-range of nascent products; and Potash is one of the main fertilizers that can be mined and produced throughout areas of the world and that do not need to be combined with natural gas.

In BHP’s 2022 economic and commodity outlook report it was stated clearly that: “Longer–term, we see potash as a future–facing commodity with attractive fundamentals. Demand for potash stands to benefit from the intersection of a number of global megatrends: rising population,changing diets and the need for the sustainable intensification of agriculture.” This reveals the essence of BHP’s push to lead in the future facing commodities space.

Potash production forms a vital source of fertilizer for food production and agriculture products all over the world, which is also a completely new segment for the world’s largest metal miner to undertake. With the global mega-trends listed above, it’s not hard to tell that BHP Group’s strategy to search for future facing commodities is a redefining concept about industry and environment — hence, the focal point of the company’s sustainablity strategy.

Moreover, as a result of what was announced by the Biden Administration on April 1, 2022, the Defense Production Act (DPA) and critical minerals supply in the United States is likely to become a politicized issue that will impact the trajectory of the global economy going forward. Already signaling disruptions from China the United States’ Coalition for a Prosperous America (CPA) published a story about Revere Copper’s renewed investments into original sources of copper, nickel and other critical materials.

— Where does Tesla get their Critical Metals from?

On the news of Elon Musk’s Twitter fiasco, people are losing sight of what’s happening with Tesla in the Global Economy. Tesla’s market share of Electric Vehicles (EV) comes down to technological superiority and first-mover advantage. Elon Musk hasn’t been shy about the raw materials needed for producing the batteries: nickel, copper, cobalt and lithium. He has been warning the world about global shortages of critical metals since May 2019.

According to Tesla’s global supply manager for battery metals, Sarah Maryssael, Tesla would take necessary measures to ensure key supply of nickel and cut down on the use of cobalt for the company’s EV production — citing a “huge potential” to increase supply of nickel from Australia and United States.

Under the backdrop of underinvestment in the raw materials needed for an industry that depends on critical metals for the so-called electric revolution, the shortages were certainly exacerbated by the global outbreak of COVID-19. Back in 2019, however, Elon Musk already pointed out an essential truth for Tesla: “There’s not much point in adding product complexity if we don’t have enough batteries.”

https://www.youtube.com/watch?v=vpNZhKSfrKE

It’s well-known among industry insiders that Tesla has sought to produce its own vehicle components ever since rolling out EVs. But the supply of raw materials, such as nickel, must be procured from areas outside of Tesla’s geographic and market reach. The company simply does not have the capability to mine its own raw materials.

Where does Tesla get these critical metals from?

In Janurary 2020, Tesla began negotiations with Switzerland-based Glencore plc to purchase long-term supplies of cobalt at its Shanghai Gigafactory.

One of Tesla’s most important lithium suppliers is a Chinese company, Contemporary Amperex Technology (CATL). The two companies partnered up on a deal for CATL to supply Tesla with lithium-ion batteries from 2022–2025. This is possibly the most important partnership in the EV sector, as far as raw materials procurement is concerned.

This was soon followed up by Elon Musk’s famous quote to global metal miners: “Any mining companies out there … wherever you are in the world, please mine more nickel…Tesla will give you a giant contract for a long period of time if you mine nickel efficiently and in an environmentally sensitive way.”

On July 21, 2021, BHP Group answered the call by signing a deal with Tesla to sustainably produce and supply battery metals from its Nickel West project in Western Australia. This was followed by another deal with USA-based Talon Metals to secure nickel supplies for a mine projected to begin production in 2026.

All of these developments in the critical metals space can’t be overstated for Tesla’s success as the world’s largest EV producer — the continuation of procuring raw materials will be the highest priority for the company going forward as new companies expand production and new partnerships emerge. It’s already been reported that automakers Ford and GM have secured lithium and coblat supplies to enhance EV production.

While other news surrounds product launches. Nissan and NASA teamed up to develop an all-solid-state battery that intends to replace lithium-ion batteries. And surprisingly, GM and Honda will jointly produce EVs based on a new global platform that will allow the companies to sell at a more affordable price in the American market.

Now that we’ve entered the 2022 era, the EV consumer market it projected to become a much more competitive sector. One of Tesla’s rivals, Rivian, announced on March 10, 2022, it would follow suit with the world’s biggest EV producer and seller by adopting lithium iron phosphate (LFP) batteries.

On the legislative front, California regulatory bodies proposed to ban the sale of new gasolne-fueled vehicles by 2035. I argue that, if this proposal is passed by relevant legal authorities, it would be a major boon for the rollout of EVs and clean energy products in USA.

With some analysts calling the this era “a gold rush to metals” the world is headed for a revolutionary expansion of renewable energy power and clean energy technologies that pass off on the fossil-fuels industry. That’s why metals are so critical to the world’s Net Zero ambitions. And to get there, Elon Musk is going to need more critical metals; while Mike Henry is going to have to prove that BHP Group is taking its ESG leadership to the next level.

— What went down at the world’s largest fertilizer company Nutrien Ltd.?

I decided to write this story in response to a hot topic in global business news about Disney’s CEO transition. The Nutrien Ltd. CEO transition has received little-to-no attention in the USA, and that’s why most of the sources come from Canadian media and news outlets. If anything this story about the Nutrien CEO transition should shed light on how critical the global fertilizer industry has become for the global economy and overall international business environment since the outbreak of the Covid-19 global pandemic.

Pour another cup of coffee or tea for this one…

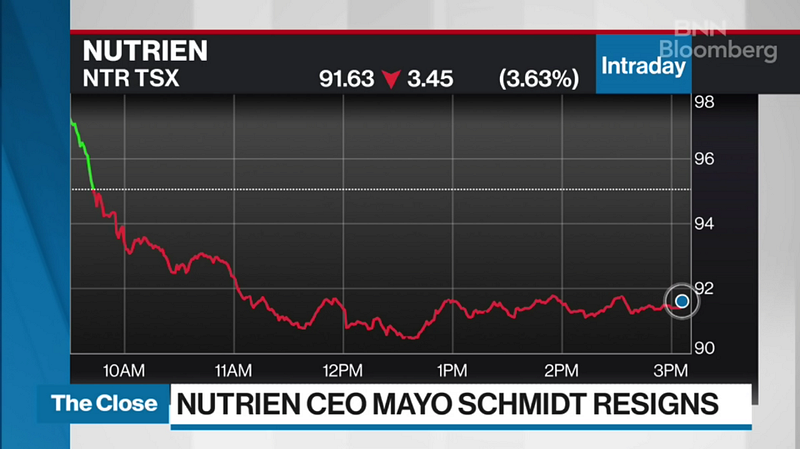

On March 19, 2022, it was reported on The Globe and Mail that former CEO Mayo Schmidt was asked to step down by the Board of Directors due to both cultural and strategic issues facing the future of Nutrien Ltd.’s leadership in the global fertilizer market.

This story comes at a time when Nutrien Ltd. had already announced that it would increase output of its potash fertilizer capabilities from approximately 14 million tonnes to 15 million tonnes in response to the ongoing global fertilizer shortage and supply crisis, which was further illustrated by farmers protesting in areas of Eastern Europe during the same week. If you need to get caught up with what’s happening with the broader global fertilizer industry’s shortage and supply crisis, here are two relevant articles about China and India.

In a press release on April 18, 2021, Nutrien officially announced Mayo Schmidt would become the new CEO of “the world’s largest provider of crop inputs and services” and that “Mr. Schmidt brings over 30 years of agricultural business experience to his leadership of Nutrien.”

https://www.youtube.com/watch?v=UUmWrXYE9v0

But as the piece from The Globe and Mail indicates Schmidt was only expected to serve as CEO for two years — an order that wasn’t fulfilled.

During the time of Schmidt’s transition to CEO there was high speculation among reporting agencies and commodity analysts about a Nutrien Ltd.-BHP Group partnership for the development of a potash mine in Jansen, Saskatchewan, Canada. It’s true that BHP has been divesting its oil and gas assets for “future facing commodities” such as potash. In a statement to The Financial Post the company said “Potash provides BHP with increased leverage to key global mega-trends, including rising population, changing diets, decarbonization and improving environmental stewardship.” However, most of the talk about a proposed partnership or joint-venture has died down since sanctions were targeted at Belarus’ potash industry and largest producer and exporter in December 2021. (Belaruskali is one of Nutrien’s biggest rivals in the potash fertilizer segment. It makes you wonder doesen’t it?)

This bring us back to the question: What went down at the world’s largest potash producer, Nutrien Ltd.? Even though the story is being thoroughly analyzed and reported on we still can’t be sure what actually caused the fall out.

According to Brian Madden, Senior Vice President of Goodreid Investment Council, “with the resources companies in particular…the leaders can’t add a single ounce, pound or tonne to the resource in the ground…they can only manage it more or less efficiently and effectively…” which means that the abrupt CEO transition announced for Nutrien “is very unusual” for these type of industries.

Although there was no specific reason given for Schmidt’s departure to date, a spokesperson for Nutrien told CBC on January 4, 2022, “This change will not impact the strategic direction of the company. We will continue to advance our strategy of helping growers sustainability feed a growing population by leveraging the competitive advantages of our integrated business model.” Thus Madden’s comments about the regularities facing resource companies, such as Nutrien in the fertilizer industry, holds true to their value as global suppliers of key crop inputs for modern agricultural production.

In other words, leadership changes at these companies have generally been viewed as an issue of strategy and development for profitable natural resources — not value-creation over time. Companies such as Nutrien and BHP have led in their specific market segments based on this ethos. That’s why in hindsight a joint venture between Nutrien and BHP seems like a perfect fit.

But is it really?

No. It’s not. There’s already major pushback from American farmers about the fertilizer industry’s alleged consolidation and monopolistic tactics to make farmers pay more for fertilizer.

On the International Fertilizer Association’s (IFA) new sustainability series “A Minute With A CEO” former Nutrien CEO Mayo Schmidt spoke on behalf of the company’s sustainability and ESG strategy. About the company’s purpose to ensure farmers around the world grow crops more sustainably, he noted that “intital pilot targets of 100,000 acres is now at more than 200,000 acres.”

https://www.youtube.com/watch?v=yJKopBVHhpo

The key to this interview came in at Question 3: Nutrien is moving toward low carbon fertilizers to create a low carbon process through the production of ammonia: What’s the opportunity here? In order to meet Nutrien’s 2030 strategy of reducing GHG emssions by 30%, Schmidt announced the building of a Department of Energy Partnership which aims to create a small-to-medium sclae Ammonia Plant. The plant is intended to increase energy-efficent production and eliminate carbon footprint — with less capital. As energy prices are skyrocketing, the new ammonia plant could be a boon or a disaster for Nutrien’s bottom line. Former CEO Chuck Magro told BNN Bloomberg on September 29, 2020 that Nutrien’s stance on climate change perspectives in agriculture is to be produce fertilizer more efficently and roll out new technologies such as Precision Rate Variable Technology.

According to what both former Nutrien CEOs offered about sustainbility plans and climate change it’s plausible to view this latest CEO transition from two angles: 1.) Nutrien’s Board of Directors are looking for a leader to take on what Chuck Magro has been pushing for since 2020; or 2.) Due to recent international events Nutrien might be changing its direction on how to operate the company’s sustainability-oriented agenda under what appears to be a very capital-intensive fertilizer production scenario going foward.

I think there’s a bigger story behind all of the uncertainties over Mayo Schmidt’s resignation; this is a story about a search for a new leader who will not only lead on Nutrien’s strategy and development, but also create value in a global fertilizer market that is expanding more than ever before. Morocco is leading Africa’s push to apply more fertilizers, while Kazakhstan looks to become a more agile supplier in Europe, and USA’s Mosaic Company seeks to expand into the potash sector with its new K3 mine in Saskatechwan.

A novel approach to the market is needed for one of the global fertilizer industry’s biggest and most profitable companies. While searching for a new leader, the public should start looking to answers from interim CEO Ken Seitz.

Geopolitical Trends & Future Facing Commodities

Indigenous groups are coming out in opposition as more and more mining projects are being planned by coroporations and governments to spur economic activity during the Global Commodity Supercycle.

I define the Paradigm Shift here:

The aspects of producer economies, the areas where they operate and the indigenous groups’ issues that are specific to their communities, all of which are at the nexus of commodities and geopolitics in the future.

As the world is grappling with the global food crisis governments want Brazil to produce more food, because it is already one of the world’s largest food-producing countries along with Ukraine.

These trends are part of the much larger geopolitical trends that have been kickstarted by the global COVID-19 pandemic. The global pandemic has caused several countries to unravel, with socio-political instability that was building up for decades, and causing the global economy to be shaken up with uncertainties, putting the world’s largest companies in some of the most vulnerable areas.

I argue that these issues about geopolitical trends and producer economies commodities are defined by a new Paradigm Shift.

All of these trends, including the references and stories I’ve included here about Brazil, should give us a broader understanding of what’s happening in geopolitics and the global economy after the COVID-19 pandemic.

Whether or not we can overcome our pre-conceived ideas about energy and commodities is going to be a key problem facing the world’s population after the global pandemic. We need to get more serious about Climate Change, but also look at how the world’s most valuable commodities are going to be needed and secured in the future.

Water is at the heart of the globe, from both a geographical vantage point and global economic perspective. While from the perspective of the Energy Transition, it’s the lifeline to save industrial production and mitigate the grave effects to humanity derived from Climate Change.

No wonder some of the world’s largest corporations and entities are betting big on their investments in Energy Transition and E-mobility, such as hydrogen, ammonia and carbon-capture, utilization and storage (CCUS) technologies, among others, while formulating industrial policies that are conducive to Electric Vehicle (EV) charging networks and supply chains for battery metals.

According to British Petroleum (BP) CEO Bernard Looney, capital spending on hydrogen development forms part of the company’s strategy to invest only in “low carbon energy” projects while taking the once-oil producing major and transforming it into an “integrated energy company.”

Those collaborations are particularly prevalent in the Asia-Pacific and Oceania areas, which is now collectively referred to as the Indo-Pacific (along with the India sub-continent and its surrounding maritime neibours and areas). In other words, from both a geographical and industrial point of view, the future of the world is being transformed to meet the needs of both corporations and humanity; hence the importance of Environment, Social, Governance (ESG) frameworks.

The potential success of outcomes in the Energy Transition and ESG frameworks hold the key to humanity’s race to cut down on carbon emissions through the Net Zero 2050 Strategy, which has been called for by climate scientists, industrial advocates and environmental activists from all around the world.

To illustrate, in a significant step toward Scope 1 Emissions, the world’s first decarbonized commercial CO2 transport and storage service was launched in conjunction with the mutual interests of Europe’s supermajor oil and gas producers — Shell, TotalEnergies (NA) — as well as Yara International.

The Nord Stream 2 and South China Sea are two examples that explain how energy, commodities and maritime areas will form a synthetic issue-area in determining dispute resolutions within the framework of international conflicts in the future.

Moreover, both of these disputes will continue to face dynamic maritime threats from non-state actors, such as extremists and pirates, who have been given very little attention to maritime law issues due to the significant interstate tensions in international politics.

In fact, these tensions have become so outstanding that two grand strategies have been developed and publicized as a vision for the future of World Order: the Indo-Pacific Strategy (IPS) and the Maritime Silk Road Initiative (MSRI) (part of the Belt and Road Initiative), of which the maritime dimension is the focal point of these strategies.

Significantly, during the time in which the 2022 Paris Auto Show was held there was a deal made by a French lithium miner, Imerys, to develop a new mine located in Beauvoir, France. This mining project aims to make France one of the European Union’s (EU) top lithium suppliers under the backdrop of increasingly higher demand for EU domestic production of EVs.

The significance of this announcement comes during a time of higher geopolitical tensions with China and Russia over global commodities, raw materials supply chains and the effects from sanctions on industrial policies during the conflict in Ukraine.

The uncertainties caused by geopolitical trends are manifested between the EU’s industrial policies and Russia’s Arctic Strategy. It points to this conclusion: the future of global economic development is going to depend heavily on the effective production and supply of global commodities around the world, during increased geopolitical tensions over sovereignty.

It was reported on 13 September 2022 that the United Nations (UN) is seeking to arrange a deal whereby Russia and Ukraine would allow ammonia exported from Russia through Ukraine to global markets. The ammonia is intended for international markets in a worldwide effort to combat the global food crisis amid a sharp rise in global fertilizer prices and tight supplies.

Devex wrote an in-depth report about this latest deal to send ammonia from Russia through Ukraine. Per their report, a UN task force, led by the United Nations Conference for Trade and Development’s (UNCTAD) Rebeca Grynspan, is supposed to ensure negotiations continue unabated by visiting with Russian officials in Moscow.

This proposal is being touted as a viable option for Russia to commit to the “landmark grain deal” orginally put together in cooperation between Turkey’s President Recep Tayyip Erdogan and Russia’s President Vladimir Putin, under the auspices of the UN with Ukraine’s President Volodymyr Zelensky, on 22 July 2022.

Heralded as a “beacon of hope” UN Secretary General António Guterres posted on Twitter: “It will help avoid a food shortage catastrophe for millions worldwide.”

This alternative form of Fertilizer Diplomacy, of course, would benefit Russia’s fertilizer producer Uralchem as the company would be responsible for sending the ammonia via pipeline to Urkaine. This means that Uralchem controls the amount of production and supply, irrespective of any arrangements made with Ukraine and other third-party actors. It’s ultimately another barganing chip for Russia to exploit and use to its advantage in the international system; hence the critical nature of Fertilizer Diplomacy.