Industrial Policies Around Electric Vehicles (EVs) Promote New Ideals On E-Mobility

This writing seeks to promote many of my fellow Medium writers out there who have been revealing insights into the most significant aspects of Electric Vehicles (EVs). Most notably, Will Lockett, Yury Erofeev and Marc Amblard who have directly inspired this writing on EV Industrial Policies and the pressing breakthroughs in electric mobility (E-mobility).

My objective is to share some ideals about the future direction of industrial policies, and how the geopolitical trends would have an effect on electric mobility (E-mobility).

I offer three breakthroughs in the following writing:

1.) EV Charging Networks redefine how transportation and mobility is viewed as a mode of transportation on a global scale;

2.) Raw Materials have taken on a newer, more prescient position in how EVs are produced as the regulatory environment is still uncertain;

3.) Batteries are evolving into a large-scale industry where producers are striving to ensure supply security in some of the world most vulnerable areas

Redefining EV Charging Networks

In 2020 a new partnership emerged in the form of a joint-venture to design and produce electric vehicle batteries. Led by TotalEnergies and Stellantis, the Automotive Cells Company (ACC) brought on a new partner, Mercedes-Benz, in 2021 to become an equal shareholder in the venture. To produce top-grade battery cells and modules, they agreed to increase industrial capacity to approximately 120 GWh by 2030.

According to the CEO of Saft (a subsidiary of Total), “ACC is a joint venture between TotalEnergies and Stellantis to design and produce automotive batteries, and to become a leader in Europe and an international groundbreaker in its field.”

Prior to co-establishing ACC, Total’s electric mobility strategy was laid out in 2019 with the goal to operate more than 150,000 electric vehicle (EV) charge points throughout European cities by 2025, including 22,000 in Amsterdam, 3,000 in Antwerp, 1,700 in London, and 2,300 in Paris.

In addition, Total has taken its commitments outside of the European continent by establishing joint ventures with China’s largest clean energy company, China Three Gorges (CTG), operator of the China Three Gorges Dam, to expand on initiatives for electric mobility in Asia.

The ACC seeks to ensure that battery design is efficient and that battery demand is met for electric vehicles as well as other transport modes such as satellites, trains and planes. Research and Development (R&D) centers have been set up Bruges, France, to design the latest battery cell technologies, while a pilot line at Nersac, France, is being launched as a battery production site.

The ACC is spearheaded by Total’s push to become an international player in electric and sustainable mobility. This began in November 2020 with Total’s acquisition of 2,000 EV charge points from Viessmann group of Charging Solution in Germany, giving it one of the most significant electric mobility markets in Europe.

The company then made a deal with Singapore’s Bollore Group in July 2021 to acquire more than 1,500 EV charge points, making Total the owner and operator of Singapore’s largest EV charging network — Blue Charge. After the deal was made, President of Marketing & Services at TotalEnergies said: “With this acquisition, TotalEnergies is pursuing its transformation and adds a new name on the list of global cities, such as Paris, Amsterdam, London and Brussels, where the Company is already developing its EV charge points installing and operating activities.”

Prescient Raw Materials

According to Tesla’s global supply manager for battery metals, Sarah Maryssael, Tesla would take necessary measures to ensure key supply of nickel and cut down on the use of cobalt for the company’s EV production — citing a “huge potential” to increase supply of nickel from Australia and United States.

Under the backdrop of underinvestment in the raw materials needed for an industry that depends on critical metals for the so-called electric revolution, the shortages were certainly exacerbated by the global outbreak of COVID-19. Back in 2019, however, Elon Musk already pointed out an essential truth for Tesla: “There’s not much point in adding product complexity if we don’t have enough batteries.”

https://www.youtube.com/watch?v=vpNZhKSfrKE

It’s well-known among industry insiders that Tesla has sought to produce its own vehicle components ever since rolling out EVs. But the supply of raw materials, such as nickel, must be procured from areas outside of Tesla’s geographic and market reach. The company simply does not have the capability to mine its own raw materials.

Where does Tesla get these critical metals from?

In Janurary 2020, Tesla began negotiations with Switzerland-based Glencore plc to purchase long-term supplies of cobalt at its Shanghai Gigafactory.

One of Tesla’s most important lithium suppliers is a Chinese company, Contemporary Amperex Technology (CATL). The two companies partnered up on a deal for CATL to supply Tesla with lithium-ion batteries from 2022–2025. This is possibly the most important partnership in the EV sector, as far as raw materials procurement is concerned.

This was soon followed up by Elon Musk’s famous quote to global metal miners: “Any mining companies out there … wherever you are in the world, please mine more nickel…Tesla will give you a giant contract for a long period of time if you mine nickel efficiently and in an environmentally sensitive way.”

On July 21, 2021, BHP Group answered the call by signing a deal with Tesla to sustainably produce and supply battery metals from its Nickel West project in Western Australia. This was followed by another deal with USA-based Talon Metals to secure nickel supplies for a mine projected to begin production in 2026.

All of these developments in the critical metals space can’t be overstated for Tesla’s success as the world’s largest EV producer — the continuation of procuring raw materials will be the highest priority for the company going forward as new companies expand production and new partnerships emerge. It’s already been reported that automakers Ford and GM have secured lithium and coblat supplies to enhance EV production.

While other news surrounds product launches. Nissan and NASA teamed up to develop an all-solid-state battery that intends to replace lithium-ion batteries. And surprisingly, GM and Honda will jointly produce EVs based on a new global platform that will allow the companies to sell at a more affordable price in the American market.

Now that we’ve entered the 2022 era, the EV consumer market it projected to become a much more competitive sector. One of Tesla’s rivals, Rivian, announced on March 10, 2022, it would follow suit with the world’s biggest EV producer and seller by adopting lithium iron phosphate (LFP) batteries.

On the legislative front, California regulatory bodies proposed to ban the sale of new gasolne-fueled vehicles by 2035. I argue that, if this proposal is passed by relevant legal authorities, it would be a major boon for the rollout of EVs and clean energy products in USA.

With some analysts calling the this era “a gold rush to metals” the world is headed for a revolutionary expansion of renewable energy power and clean energy technologies that pass off on the fossil-fuels industry. That’s why metals are so critical to the world’s Net Zero ambitions. And to get there, Elon Musk is going to need more critical metals; while Mike Henry is going to have to prove that BHP Group is taking its ESG leadership to the next level.

Future Facing Commodities — Supply Security

The geopolitical trends point to this conclusion: the future of global economic development is going to depend heavily on the effective production and supply of global commodities around the world. That’s why one of the biggest industrial trends for global mining projects is related to Environment, Social, Governance (ESG) frameworks.

The aspects of producer economy areas and indigenous groups’ issues play a big role in this phenomenon — and rightly so in my view. These trends are part of the much larger geopolitical trends that have been kickstarted by the global COVID-19 pandemic. The global pandemic has caused several countries to unravel, with socio-political instability that was building up for decades, and causing the global economy to be shaken up with uncertainties, putting the world’s largest companies in some of the most vulnerable areas.

Many of these mining projects, especially the ones for copper and nickel, are critical to achieving both the Energy Transition, most notably for renewable energy installations and Electric Vehicles (EV) production rollout.

The world’s largest metal miner BHP group plans to source and produce metals while taking a more sustainable and environmental focus on their operations globally. There are basically three main commodities in this future facing commodities space: copper, nickel and potash. The former two are both metals directly related to metal mining and stainless steel production, while the latter is primarily used as a source of fertilizer.

It’s true that BHP has been divesting its oil and gas assets for “future facing commodities” such as copper, nickel and potash.

The concept of future facing commodities is still new to many people. It has already become synonomous in global business news with “tougher jurisdictions” that are associated with vulnerable areas of political control and regulatory corruption. Read more about the Glencore case below.

This implies that that the company will have to venture out to new areas — i.e. “tougher jurisdictions” — containing the high-grade copper, nickel and potash production capabilities desired for such results. CEO Mike Henry also announced atthe FT Mining Summit in 2021 that BHP Group wants half of its revenues to come from the production and exports of these future facing commodities by 2030.

I argue that these issues about future facing commodities and global mining projects, as well as how indigenous groups and governments are responding to the Global Commodity Supercycle, are defined by a new paradigm shift: The aspects of producer economies, the areas where they operate and the indigenous groups’ issues that are specific to their communities, all of which are at the nexus of commodities and geopolitics in the future.

Whether or not we can overcome our pre-conceived ideas about energy and commodities is going to be a key problem facing the world. We need to get more serious about Climate Change, but also look at how the world’s most valuable commodities are going to be needed and secured in the future — hence, the critical nature of the future facing commodities.

Per Quartz, Goldman Sachs predicts automakers will find some relief from metal shortages in the near term, but with the global consumption of battery metals continuing in the long term, that demand is likely to catch up with supply and send metal prices soaring in the future.

This story is related to global commodities and metals, specifically, the supply and demand for Electric Vehicles (EVs) and the nascent Energy Transition.

But knowing the price volatility of these metals is key to understanding the overall issues with the Global Commodity Supercycle.

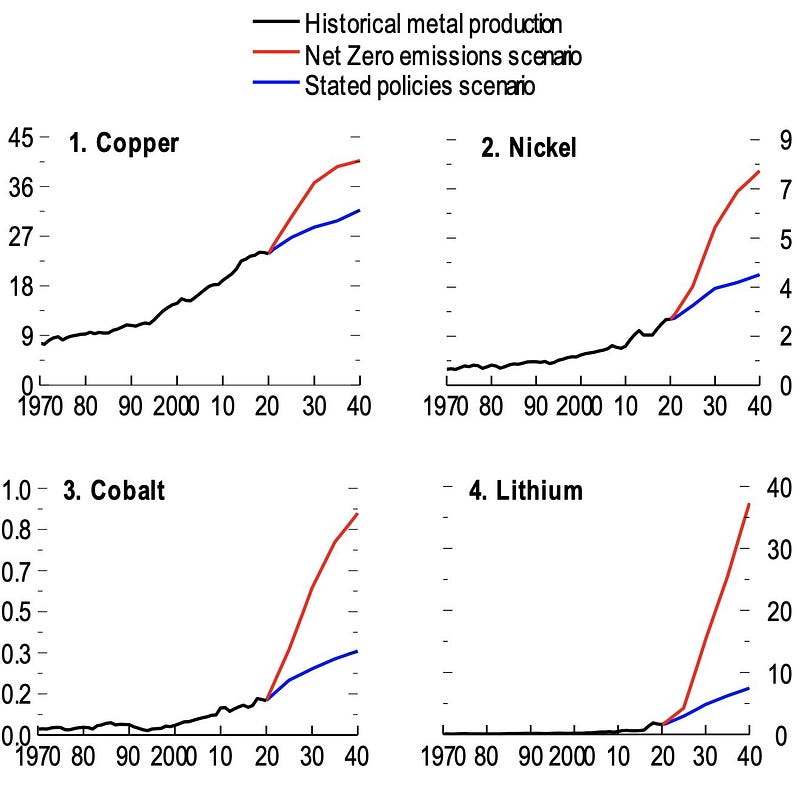

The most commonly produced battery metals are nickel, cobalt and lithium.

Though most importantly the current situation of battery metals is linked to what happened on the London Metals Exchange (LME) in March 2022 when the price of nickel hit $100,000 a tonne — forcing the LME to shut down its commodity trading platform.

The metals markets have yet to fully recover from what happened on the LME this year, due to the ongoing Russia-Ukraine conflict and Shanghai lockdowns in China. Legal disputes are pending, too.

Many analysts are pointing to the so-called “old economy’s revenge” as a way to understand market forces along with the sharp rise in prices of global commodities across the board.

According to Jeff Currie of the Financial Times,

“the 2000s and ’70s have a lot in common and it’s a whole idea of redistributional policies.”

By this remark, Jeff Currie asserts that the global economy is currently undergoing a third global commodity supercycle since the 1970’s.

He argues that the global economy underwent the same underinvestment theme — i.e., “the revenge of the old economy” — during the late 1960s and early 1970s which meant that poor capital investments in the old economy led to more capital in the new economy.

Watch the full interview with Jeff Currie on the Hidden Forces podcast with Demetri Kofinas.

Final Thoughts

I conclude by saying that the demand for raw materials, commodities and energy are producing effects in the foreign policy area of many countries today, including in both developing and developed areas — I’ve already written extensively about the illustrations of this theory from the perspective of how countries and corporations are formulating industrial policies around oil and gas while preparing for the Energy Transition in the future.

These strategies are being carried out under the backdrop of increasingly volatile global markets and diverging geopolitical trends, which have put global commodities at the forefront of geopolitics. For instance, the of future industrial production revolves around future facing commodities which means that industrial policies are also being regulated by Environment, Social, Governance (ESG) framework with respect to global commodities.

Moreover, the China-Russia relationship is not only a cause of concern for the United States and European Union but also enhances the narrative around geopolitics and commodities: a paradigm shift whereby global commodities are at the forefront of geopolitics and ESG corporate frameworks.

The strategic dilemmas for both China and Russia reveal that advancements and achievements in the new Space Race are a top priority for their geopolitical objectives vis-a-vis the United States and European Union.

The competition for this new Space Race allows for China and Russia to use this adversarial geopolitical scenario as a political tool of information to use against the United States and European Union, to the effect of bolstering “anti-Western” values of their domestic populations. While both countries seek to dominate the production and supply of raw materials, of which those commodities are directly linked to the aerospace industry, and therefore are susceptible to geopolitical tensions. The evidence of this trend is apparent in legal cases revolving around global issues related to food security and energy dependence.