The Effects From Geopolitics and Sanctions on Industrial Policies During the Russia-Ukraine Conflict

This story is specifically looking at how sanctions on Russia are bringing global commodities to the forefront of geopolitics, and thus revealing the changes to industrial polices among the world’s core areas and critical producers. If you want more content about the countries affected by the Russia-Ukraine conflict then read what I put together here about Russia’s impact in the publication Areas & Producers.

The Russia-Ukraine Conflict

Nato Enlargement

One of the fundamental problems between Russia and Ukraine is about NATO enlargement in Eastern Europe. Russia fears this would bring Ukraine into a Western security alliance that deters Russian influence in what is referred to as its “sphere of influence.” Russia demonstrated how far it was willing to go to protect its sphere of influence when Georgia fought a war against separatist territories, South Ossetia and Abkhazia, in 2008. After convincingly pushing Georgia’s military out, Russia recognized the separatists territories’ right to self-determination.

This fundamental problem of NATO enlargement has become more of a European-centric issue in recent years, as ideals for European strategic autonomy, security responsibilities and national sovereignty are being defined under the leadership of France and Germany in the European Union (EU). Since the United Kingdom left the EU, it’s likely that Russia is calculating whether the EU’s current defense posture can obstruct Russia’s advancements on Ukraine — for instance, the takeover of Crimea in 2014 left Russian forces unscathed, along with a new territory captured by Russia on the strategic area of the Black Sea.

United States Diplomatic Efforts in Ukraine

Here is a list of critical events I compiled from 2021 about the United States diplomatic efforts in Ukraine:

2. US ensures EU it won’t be affected by energy crisis

3. Russia halts gas exports to Europe via Yamal pipeline

4. Russia performs anti-Satellite test in outer space

5. USA sends extra weapons to Ukraine

These events serve as a backdrop to when the USA and NATO held talks with Russia in early January 2022 to discuss the situation in Ukraine. During these negotiations, it was reported that Russia initiated military exercises in the western regions of Voronezh, Belgorod, Bryansk and Smolensk, with about 3,000 troops participating in the exercises near the Russia-Ukraine border.

When talks between the USA and Russia failed, NATO countries prepared themselves for renewed Russian aggression toward Eastern Ukraine and possibly more. One of Europe’s biggest concerns leading up to these talks was the stability and flow of Russian natural gas. With dashed hopes of a diplomatic solution to Ukraine, the USA publicly announced that it would export its abundance of Liquified Natural Gas (LNG) to European countries, in light of its import dependency on Russian energy.

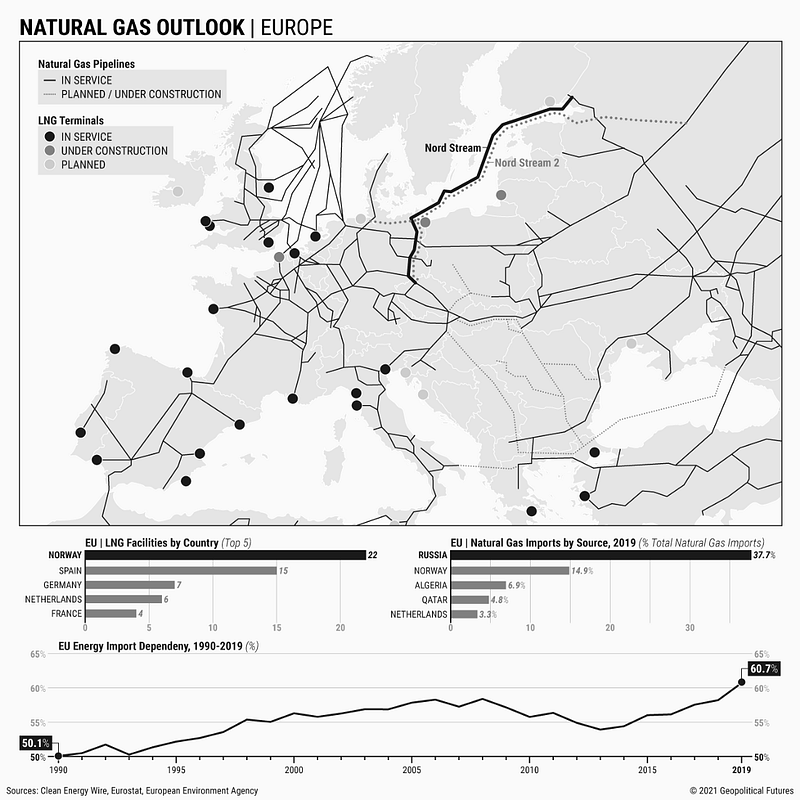

Europe’s Dependency on Gas Transiting Ukraine

Experts believe that the energy aspects of the Russia-Ukraine conflict are indisputable. According to Niall Ferguson of the Hoover Institution, “the consequence of Europe’s allowing itself to become so reliant on Russian natural gas and oil…that Vladimir Putin has been able to build up and modernize Russia’s military.” The problems surrounding transit fees from Russia to Europe through Ukraine’s territory has been a contentious issue since 2006, with the most notable dispute over gas transit fees occurring in 2009, when Russia’s Gazprom cut off gas supplies for Europe due to Ukraine’s failure to pay off debts.

This prompted the EU to launch an anti-monopoly investigation against Russia’s largest gas pipeline company, Gazprom, in September 2011. This was a significant setback to Russia’s economy, as Bruegel’s Georg Zachmann points out: “Russia has built its entire economy on the export of hydrocarbons, and Russia is not really able to sell natural gas anywhere else than to the European Union.”

In addition, Russia’s top LNG exporter, Novatek, was put on the US sanctions list in 2014, for what former US President Obama called Russia’s “continued provocations in Ukraine.” The remaining pipelines that Russia has the most influence over are the Caspian Pipeline Consortium (CPC) transiting Kazakhstan and the Nord Stream Pipeline and newly built Nord Stream 2 Pipeline transiting the Baltic Sea.

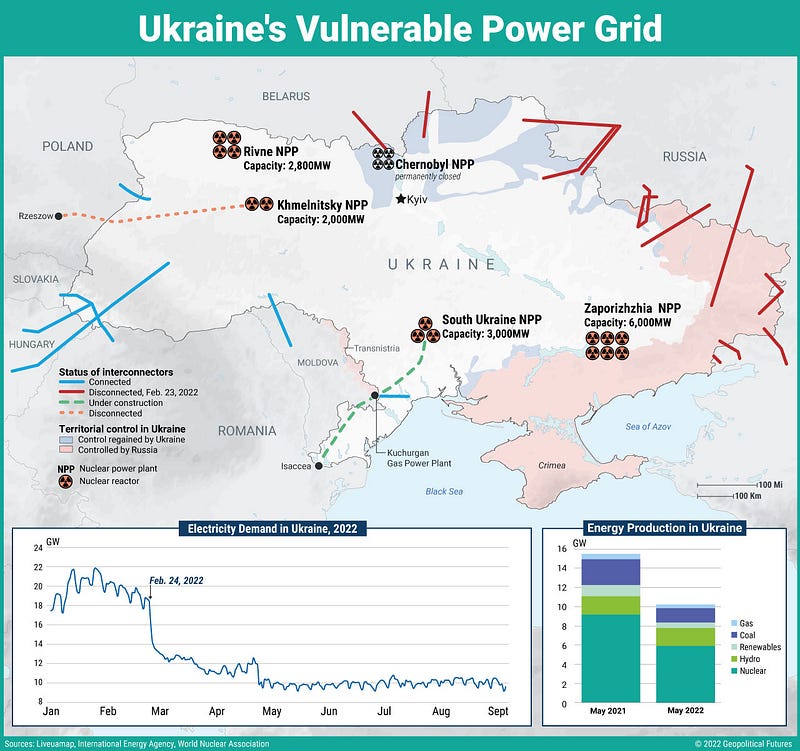

Just look at Geopolitical Futures (GF) map inserted below, with data compiled by the World Nuclear Association, which shows the drastic effects to Ukraine’s coal and gas infrastructure in the aftermath of conflict with Russia. Most of the intense fighting to territorial control have been around areas on the Black Sea and Sea of Azov, where the majority of nuclear reactors are based in Ukraine. Meanwhile, the pipelines from Russia to Ukraine have been disconnected; hence the primary cause to European energy supplies disruption since Feburary 24, 2022.

Russia Sanctions & Industrial Policies

Looking at the cause and effects from sanctions is one way to explain the USA’s response to military actions in Ukraine. It should also give us an idea of how USA will use sanctions to respond to future events as well.

In my view, the ability to wield sanctions is clearly one of the USA’s biggest advantages against other countries in the international system. They’ve proved to be effective in deterring countries from certain actions, such as doing business with Russian conglomerates, China’s Huawei and Iran’s state-owned oil companies.

Initially I think USA sanctions were used to target specific individuals and entities. But now what we’re seeing is a much broader use of the sanctions to target wide sectors of the Russian economy.

For instance,the two American agriculture and construction giants, John Deere and Caterpillar, both announced they would comply with sanctions, which means both Russia’s agricultural and construction sectors will be impacted. This is more significant, in my opinon, than the consumer-led brands (McDonalds and Starbucks) because Russia’s economic growth is more dependent on developing commodities at home and building infrastructure for others abroad.

One of the outstanding cases to emerge from this event is how Russia is responding to private jet and commercial aircraft lessors, a primarily Irish industry that has massive global effects. This is a global leasing business protected under international law conventions (Cape Town) worth billions, but Russia has publicly announced that all of those jets and aircraft will be nationalized if sanctions are imposed on that sector.

This is a major problem not only for those jet and aircraft lessors but for the whole international business environment. It’s situations like this that will deter businesses from operating globally, which I feel is what Russia would like to see happen. The sanctions have cut them off from many opportunities to operate globally which puts them at a disadvantage with most other countries.

Ultimately what we want to know is how are sanctions working in preventing the crisis and conflict in Ukraine?

As we know the conflict still looms large and it doesn’t look like sanctions against Russia are deterring their military invasion. It seems the sanctions are less intended to impact Russia’s military strategy, and more so to send a strong message that the USA regulatory regimes will not let their businesses do whatever they want (this is also a message to companies operating in China).

More importantly, USA sanctions are being used as a way to drum up domestic and international opposition to Putin’s regime. I question whether this political motive for the sanctions is working effectively. Clearly the invasion of Ukraine has already damaged Putin’s regime in the eyes of many people around the world. But those sanctions also hurt the Russian economy in a way that affects Russian citizens more than the regime itself; this has allowed the Russian government to bolster its argument that “anti-USA” or “anti-West” values should permeate Russian society and culture.

This is probably the most dangerous concept to industrial policies of the 21st century.

The Energy Dimension: Europe & USA

In the event that OPEC+ comes to an agreement over production and supply targets, it may be too late to make a difference on prices overall, as Americans and Europeans will continue paying for higher prices.

This is a lesson that many people tend to ignore.

On the news of Russia taking over the Sakhalin-2 Project, the effects on LNG production will have an impact on global supplies; therefore, Russia has once again disrupted energy supplies in a big way — Russia already disrupted oil supplies from the Caspian Pipeline Consortium (CPC) in Kazakhstan.

In fact, Russia has disrupted Energy and Commodities in unimaginable ways, which brought the discussion of Global Food Security to the G7 Summit.

Energy and Commodities are the biggest concerns of the global economy due to the Russia-Ukraine Conflict, among other factors, as Germany is preparing for more coal plants, the United States is preparing for more mining projects like the Copper World Complex in Arizona, and France’s President Macron is in talks with Romania to revive an old railroad transportation route from Odesa to the Danube River to increase grain exports from Ukraine to international markets.

All of this economic activity is occurring under the backdrop of USA and European sanctions on Russia’s critical LNG industry, such as Novatek’s Arctic LNG 2 project.

It’s essential to point out that even when the largest companies are pushing for ways to successfully carry out Energy Transition around the globe, that commitments to natural gas production and exports via LNG will continue to grow over time.

The Russia-Ukraine conflict has taught us that the international outlook is no longer as uncertain as before. The G7 has come together in solidarity to denounce and outmaneuver Russian aggression, while the developing world seeks to cooperate further with a more energy- and commodities-oriented economic power in Russia.

The Fertilizer Dimension: Brazil

But looking elsewhere in the fertilizer scenario puts a spotlight on potash. Russia stopped exporting potash due to the conflict in Ukraine. Brazil acted quickly on this circumstance by pushing ahead with one of the key strategic advancements in the National Fertilizer Plan: mining for large reserves of potash underground in the Amazon Rainforest.

It’s a fact that Brazil’s potash reserves lie within lands owned by indigenous peoples. And it’s the reason for why an indigenous mining bill has been held up in the Congress. A crowd gathered for the “Earth Event” during which legendary Brazilian musician and artist Caetano Veloso led the protest against the mining bill. It was reported that Veloso met with the Senate to plead for not letting the bill pass.

Where will Brazil fit into this future global fertilizer scenario? According to the USDA, a report compiled on March 6, 2022, outlines the following data about the outlook for Brazil’s National Fertilizer Plan.

- For Nitrogen Production: 1) increase nitrogen capacity to 2.8mnt by 2050; 2) attract 2 nitrogen producers to Brazil by 20230; 3) attract an additional 4 producers by 2050; 4) allocate $10 billion for nitrogen production and output by 2030; 5) allocate $10 billion for nitrogen production and output for 2030–2040 and 2040–2050.

- For Phosphate Production: 1) 5 auctions to be held for phosphate mining areas; 2) add 2 phosphate producers to new mining areas by 2030; 3) increase the number of phosphate producers to 10 by 2040; 4) increase phosphate rock exploration by 3% annually through 2030 and 2% annually from 2030–2050; 5) enhance phosphate rock production at 27mnt annually by 2050.

- For Potash Production: 1) 5 auctions to be held for potash mining areas; 2) raise national potash production to 6mnt by 2050; 3) increase the number of potash producers to 10 by 2030; 4) add an additional 10 potash producers by 2040.

Key Points: For nitrogen production the words increase, attract and allocate should mean that international investors and companies are welcomed to set up shop in Brazil’s fertilizer industry. For phospate production the words add, increase and enhance standout as if phosphates are in high demand for Brazil’s crops, so getting more of it is beneficial to short-term demand. For potash production the words raise, increase and add are necessary for the National Fertlizer Plan, because, as I’ve already mentioned before, potash production in Brazil is in high demand due to problems with Russia and Belarus imports to Brazil; it is possibly the biggest concern for long-term industry planning.

The current global fertilizer scenario reveals some intriguing data points about production and supply. Companies like Morocco’s OCP are expanding into Africa to solve many of the countries’ food problems. USA is restricting access to its fertilizer markets, while China looks to shut down many of its export operations for domestic supply and Russia uses its fertilizer diplomacy to achieve political ends.

Voting matters.

Whether at the UNGA or in Brazil’s Congress, votes are made that have far-reaching consequences. It’s votes like these that allow countries to push their strategies, such as Brazil’s abstention from the vote to suspend Russia from the Human Rights Council. In addition, countries from the Middle East and North Africa — Morocco, Qatar, Oman, Saudi Arabia and Algeria — have stepped in to fill the void of Brazil’s fertilizer import dilemma. While Jordan hopes to keep its potash fertilizer exports, valued at $70 million in 2021, replacing Russian exports for the forseeable future.

The Metals Dimension: China

In the case of Russia, combating sanctions is a key part of the country’s economic development in the future.

These metals are becoming so valuable to the global economy that Russia (plus others) must carefully consider how its industries will avoid sanctions from the United States and European Union. Avoiding the massive blow from sanctions due to its invasion of Ukraine would be a high achievement in their overall strategy to defend Russia’s nationalist policies.

Whatever happens with Russia’s commodities and the impact brought on by related industries from sanctions, will have an effect on the relationship between Russia and China, which will also cause great concern to the USA and European Union.

The fact is that the Russia-China strategy is still very uncertain to how far it will go, though China’s Chairman and President Xi Jin Ping did stand by Vladimir Putin’s side irrespective of the war in Ukraine, which in my view shows a lot about the direction of the two countries common interests in world politics.

The Olympics is certainly one of the largest stages to make such a statement.

I argue that China is likely to face tough decisions in the future about the consequences from increasing exposure to Russian commodities, particularly metals such as copper and nickel, for which Russia has production capacity and strategic reserves to keep supplying China with these critical metals in the future.

China is also less likely to get tangled up in the ESG paradigm shift and the related issues to their economic projects abroad with a dependence on these vital commodity exports from Russia. This would be an advantage to China’s strategic dilemmas vis-a-vis the United States in the future.

To understand what is happening more broadly in the metals industries, I suggest reading more about the nickel trading crisis on the London Metals Exchange (LME) in March 2022. Read the link below for more information about Indonesia, Australia, BHP Group and Tesla and how the industrial policies around metals could embolden the China-Russia relationship.

Conclusion: The Aftermath of Nord Stream 2

On October 18, 2021, a security pact was signed between U.S. Defense Secretary Lloyd Austin and Georgia’s Defense Minister Juansher Burchladze, in response to Russia’s expansion in the Black Sea. The meeting came after the Biden Administration approved foreign military sales (FMS) to Georgia worth $30 million, including Javelin anti-tank missiles and launchers. As the US had already been providing military assistance to Ukraine, the FMS to these countries proves that the United States is taking the Russian threat to these countries very seriously.

Speaking on the security pact with Georgia, Donald Jensen of the United States Institute for Peace (USIP) asserts that “even though the military situation is relatively at a standoff [in 2021] Russia tries to undermine Ukraine in other ways.” This implies that more military assistance might not be enough to deter Russia’s actions in the future. That’s why it has been the Biden Administration’s strategy to compel Russia by both military and economic means — a combination of military assistance to Russia’s neighbors, as well as forcefully applying economic sanctions on Russian individuals, entities and business sectors.

On March 29, 2022, peace talks were held in Istanbul, Turkey, whereby Ukraine President Volodymyr Zelenskyy acknowledged that, because Ukraine could not be allowed to join NATO, then a viable option would be for Ukraine to accept neutrality — under the condition that security guarantees would be provided by the United States, France and United Kingdom. However, in order to appease Russia, the Ukrainians offered not to apply such security guarantees to the Donbass region. The Donbass region of Ukraine, according to George Friedman of Geopolitical Futures, “was always a pro-Russian region, where the Russians have special forces there.” Due to Russia’s lack of progress with fighting in Donbass, Friedman claims that Russia’s overall invasion has weakened morale, and thus Russia intends to launch an offensive during this “window of opportunity” before USA’ military assistance arrives in Ukraine.

EU officials have called Russia’s demands for Ukraine to “demilitarize” unreasonable and that Ukraine needed more military assistance to stop the Russian invasion. At the same time, analysts have argued that a “proxy way” is being initiated by countries outside of Ukraine in response to Russia’s so-called “special military operation.” Proxy wars have been defined as a way to de-escalate conflict and increase leverage over the disadvantaged country in a conflict. In this case, Ukraine is the country seeking leverage at the negotiating table with Russia. In fact, former CIA director Leon Panetta is confident that the proxy war between USA and Russia has already begun, “[USA] are engaged in a conflict here. It’s a proxy war with Russia.”

I highlight these two events above — U.S. security pact with Georgia and the peace talks held in Turkey — because the experts have completely ignored the issues surrounding the Nord Stream 2 (NS2) pipeline. This is significant because the politcization of NS2 brings out all of the issues revolving around the future of industrial policies.

In the publication Transatlantic Perspectives, Michael Gorecki lays emphasis on NS2 as one of the main catalysts of the Russia-Ukraine conflict. This speaks to the misconceptions throughout world media about why the war intensified this year. I agree with this perspective completely.

However, I disagree with the idea of abandoning the NS2 pipeline. The politicization of the pipeline should not be intensified, otherwise, it is likely to serve as a symbol of the Russia-Ukraine conflict for decades to come.

The NS2 pipeline should serve as a means for cooperation and ensuring energy supplies to the European markets — I understand this notion sounds barbaric given the current circumstances — but the NS2 will not just simply dissappear, nor will the vasts amounts of investments and demand for energy worldwide, so some practical demands must be given over the nature of NS2’s role in the global economy. All we can do, it seems, is work toward de-polticizing the NS2 as much as possible, in hopes that NATO enlargement and natural gas issues are resolved accordingly.