How to Attack Your Finances

Stop being a pushover and take control of your money.

How many times have you heard the following advice?

- Make coffee at home, as those $5 lattes are destroying your budget and your retirement savings!

- Find the cheapest gas with an app; it’s worth the time driving all over town to save $0.02/gallon.

- Buy in bulk from Costclub, since single servings are for suckers.

All of these are protective in nature; failed attempts to hoard the money you have.

And all of them will make you poor.

You need to go on offense, find the big wins, and fight against the powers that be who are conspiring to take your money.

This mindset lets you take on the persona of the financial underdog, waging war against the mechanisms that are insatiably stealing your money.

If you know about the Miracle on Ice, you know that the US men’s hockey team was a vast underdog in the 1980 Olympics, especially against the undefeated Soviet Union.

There is a scene in the movie about this game, Miracle, where the team is watching film of the Soviets and witnessing firsthand just how good they are. Afterward, coach Herb Brooks states the following:

You don’t defend them…you attack them.

This is equally true when it comes to your money. Everyone else is scurrying along, hiding from the big, bad sharks, especially after the hellacious 2020 we had.

You need to overcome this temptation and come out swinging. You’ve got to stand and fight for every penny that you’re owed.

If that description sounds like a fairy tale, then you’re right on target. Because that’s what this is; except it’s more of a horror story for most people.

So, start learning the system and stop being the victim that gets eaten by the zombie companies. Then you can attack and get the money you have rightly earned.

Defense

Offense wins games. Defense wins championships.

This quote is oftentimes naively used to keep people from taking action. The advice? “Just huddle up at home and try your best not to overspend.”.

But think about the great defensive players in sports history.

- Mike Singletary might be the greatest middle linebacker in NFL history. Aside from his athleticism, his sheer intensity intimidated offenses and stoked the fires of competition in the entire defense. He didn’t “defend” his end zone. He attacked the offense.

- Michael Jordan scored 30.1 points per game (tied with Wilt Chamberlain for the most in history), but he is also second on the all-time steals list. Nothing says defense like making sure your opponent can’t even get the ball.

- Ozzie Smith amassed 2,460 hits during his baseball career, but it was the 13 Gold Gloves that he is best known for. How many hitters wound up walking to the dugout instead of standing on first because of his defensive effort.

This is the attacking mindset you need to protect your finances from those who would otherwise take it without emotion.

Savings

Pay yourself first.

The only way you’re going to actually save something is if you never touch it in the first place. Willpower doesn’t work, so you need to attack your psychology and kill any impulse to immediately spend money you would otherwise tag for purchases down the road.

How do you do it? You automate your savings. If you never see it, then you never spend it.

- For a quick win, use my hack and pretend you’re a smoker.

The average pack of cigarettes costs $5. Assume you smoke one pack a day, and that’s $35 from your weekly paycheck. Set up the automatic transfer from checking to savings at your bank, and Viola! That’s $1,820 saved in one year.

- If you want to go further, make a budget using YNAB.

It’s awesome. When I started using YNAB, I realized that I am redlining my spending right now.

Yes, I’m saving money, but it’s only for annual expenses, like car registrations. I’m still not actively putting money away to get my emergency fund up to the recommended 6 months. This needs to change in 2020.

Retirement

This is a huge topic, but there are only a few things I want to review here.

- First, get the company 401k match.

You may have heard it one before, but it bears repeating. Get the company match. It’s not just free money; it’s free money that grows! If you know nothing about investment accounts, just go with one of the standard target-date funds that your company probably offers.

- Second, ruthlessly lower your investment fees.

They are the number one killer of market returns for investors. If you don’t have access to a 401k at work, go with low-cost Vanguard fund.

- Make sure you’re vested.

Many employers require you work there for a certain amount of time before their contribution is officially added. Before you split for another job, make sure you’re not leaving thousands on the table.

Health Insurance

Everyone hates health insurance, but it’s a great spot to actively save money. For example, I get paid $130 every month by my own company for going on my wife’s insurance. Another source of free money!

The total cost of health insurance includes

- Insurance premiums

- Deductibles and total out-of-pocket costs

- Copays

- Tax burden

You can’t just look at each of these independently. They need to be calculated as a total cost so you can make an educated decision.

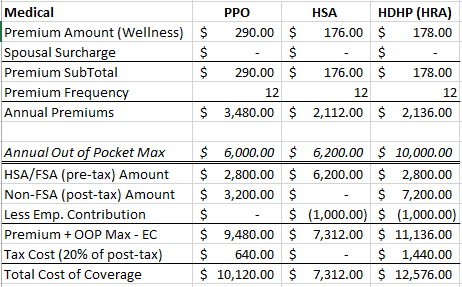

Below is a quick spreadsheet that shows the options my wife and I had for 2020, along with the total annual exposure.

Since we have two children, we assume that our total costs will equal the out-of-pocket maximums.

By choosing the high-deductible plan with the HSA option, we saved $2,800 in annual health care costs.

Student Loans

I’ve written a lot about student loans (here, here, here, here, here, here, and here), but here’s the long and the short of it.

There are myriad student loan forgiveness programs out there, with the big kahuna being the Public Service Loan Forgivness (PSLF) program. Check out my guide to the PSLF program.

If you work in the public or non-profit sector, take a good, hard look to see if this is right for you.

Also, check out this link for a big list of other loan forgiveness plans.

If that fails, there are many companies that are starting to add student loan payment assistance to their benefits packages.

By the way, if you’re waiting for Congress to pass legislation forgiving all student debt, don’t hold your break. It’s a pipe dream.

Credit Cards

These are the absolute worst. But if you’ve got credit card debt, learn how to use them correctly. Here’s a quick rundown of actions to take.

- If you have a large balance with a high interest rate, use a balance transfer.

The secret to this plan is having a plan to pay it down. Some cards have a 0% interest rate for up to 18 months, so you’ll have time. Just don’t get complacent on the payments.

- If you have a small balance, pay it off ASAP.

Use your tax return if you have to. Just get it off your books. In the short term, paying off debt with a high interest rate is like investing with an equal rate of return.

- If you have no credit card debt, congratulations!

You might want to look into playing the points game and earning some sweet rewards. I started doing this with my Costco Citi card, and it’s earned me several hundred in rewards so far.

Offense

Now that we’ve covered ways to minimize money that’s going out, let’s start talking about maximizing money that’s coming in.

Salary

When it comes to your salary, don’t wait until your annual review to ask for more money. Like anything else worth doing, it takes time and effort to reap the rewards.

- If you love your job but want (or need) a higher income, then I highly recommend The Briefcase Technique.

In short, you prep your boss month in advance by establishing agreed-upon metrics that would deserve a raise. You then work your ass off to meet those metrics and submit the results.

After the review, you ask your now-impressed boss for a “compensation adjustment”. If they say yes, congratulations! If they say no, then you know that’s not the company for you.

- If you hate your job and your salary, then it’s time to move on, my friend.

Don’t be afraid to leave your job. Ever since the advent of corporate raiding and using people to balance the books (aka, layoffs), companies have been disloyal to their employees. So why should you treat your company any different?

- If you’re stuck in a bad job but with a good salary, use the benefits to their maximum (e.g. educational money), then get the hell out of there.

Look into maximizing your job benefits. You can not only increase your take home pay but also acquire skills and/or experience that can lead to a salary increase at your next job.

Side Hustle

There has been a lot of talk about starting a side hustle in the past few years. The so-called gig economy has never fully taken off as a replacement of a full-time job. Instead, people have found that they can supplement their income while keeping the benefits of their career.

While I won’t go through a list of side hustles (those can be found here, here, here, here, and here), I will say that a side hustle can benefit you many ways outside of income.

After you get over the first hump of actually starting something on the side, you’ll find that you start performing better at your day job, appreciate the hard work of the entrepreneurs you read about, and realize that life is not just 40-hour work weeks until you die.

The Takeaway

YOU have control over your money. No, you can’t go from broke to six figures next week, but you can definitely start the process.

- Master the fundamentals of personal finance.

- Make sure you have an internal locus of control.

- Be proactive.

Your destiny is up to you. Go out there and take it. (Can you tell I love this movie?)

The Latest Stories From Money. Daily.

- Increasing Returns with Covered Calls

- The Basics of Budgeting

- Americans Are Drowning in Medical Debt

- Are You Prepared If Your House Floods?

- Mortgage Prepayments

Don’t miss my next article! Click here to get notified when I publish new material.

If you love the articles published in Money. Daily. become a member of the Medium and get full access to our full archives.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.