Could Cancelling Student Loans Actually Save Money?

Finding the balance between servicing and forgiving debt.

For the past few years, the alarm has been sounding ever louder that student loan debt is causing massive economic harm, on both personally and nationally.

When saddled with too much debt, individuals find it hard to keep their more of their income to make the big purchases in life, such has homes and cars. Even if they do scrape together enough capital, getting a good mortgage or car loan can be difficult, since their outstanding loan balance dings their credit scores.

If this happens to one person, it affects that one person.

If this happens to millions of people, it effects millions more.

When homes and cars aren’t being bought (i.e. demand goes down), prices go down, jobs go down, and the economy goes down. This is the much-feared deflationary cycle that most economists worry about.

Sure, we’re living in a time of relatively high inflation, but that’s mostly because of COVID-induced shortages on the supply side that are outstripping. Plus, demand for goods will taper off once the stimulus money is spent and student loan payments resume.

This doom and gloom makes a good case for cancelling student loans at some level, allowing borrowers to reallocate their money into the general economy, therefore boosting the all-important consumption level, rather than repaying the government for an education that many aren’t even using.

I’ll make another case for cancelling student loans: saving taxpayer money.

The Cost of Student Loans

All told, the Department of Education services $1.58 trillion in student loan debt across 43 million borrowers. That is a lot of money lent to a lot of people.

Every year, the Congressional Budget Office (CBO) prepares a report on the cost of servicing all these loans (rather, the cost of hiring companies to service these loans), along with the forecasted income from repayment.

To generate these income projections, the CBO follows the accounting rules laid out by the Federal Credit Reform Act of 1990 (FCRA). Unfortunately, the FCRA assumes higher income stability than the standard fair-value estimates used in the private sector would show.

When using fair-value calculations, servicing student loans goes from a small revenue generator to a large cost sink.

The funny thing is, even the CBO knows that FCRA is outdated. Here is their actual description of the problem from their own latest update.

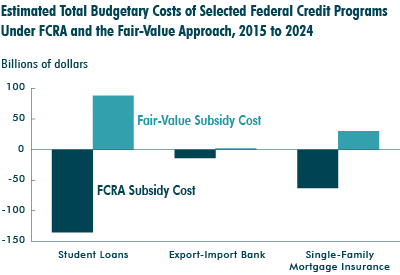

The Department of Education’s four largest student loan programs would yield budgetary savings of roughly $135 billion under FCRA accounting but cost roughly $88 billion on a fair-value basis (see the figure below).

The projected losses are confirmed every year when the Department of Education has to use money from other program budgets to cover the cost of student loan servicing.

Also, notice that the Export-Import Bank and mortgage insurance programs are also affected by this accounting debacle.

An even starker picture is painted by the Wall Street Journal.

The Education Department, with the help of two private consultants, looked at $1.37 trillion in student loans held by the government at the start of the year. Their conclusion: Borrowers will pay back $935 billion in principal and interest. That would leave taxpayers on the hook for $435 billion, according to documents reviewed by The Wall Street Journal.

Further in the article, they compare this to the total amount lost during the financial crisis.

After decades of no-questions-asked lending, the government is realizing that it has a pile of toxic debt on its books. By comparison, private lenders lost $535 billion on subprime-mortgages during the 2008 financial crisis, according to Mark Zandi, chief economist at Moody’s Analytics.

Uh oh.

It’s never a good sign when you start talking about “toxic debt”.

How Forgiveness Can Save Money

Costly Defaults Would Shrink Drastically

Year after year, accounts with the lowest student loan balances are consistently the ones that are the most complex, and therefore cost the most money.

Once you eliminate the current defaulters and reduce the number of future defaulters, you can stop spending money on processing the defaults. I know it’s more complicated than that, but that’s the overall idea.

Millions of Borrowers Would Be (Student) Debt Free

Imagine the buying power of millions of current borrowers unleashing their otherwise earmarked student loan payments into the general economy.

Sure, only a small amount of the total outstanding balance would get circulated, but it would be used every single month for years!

Pumping money into the economy, and paying taxes on every purchase, gives a much higher rate of return than just trying to collect on the debt.

Private Refinancing Would Shrink

The standard student loan repayment plan is 10 years. The income-driver repayment (IDR) plans are much longer, with some lasting 20 years or more.

That’s a long time, with only a mortgage lasting longer among all the standard consumer debt options.

One problem is that interest rates fluctuate over the years, and student loan borrowers with federal loans can refinance with private lenders at much lower rates, prohibiting the government to collect.

Federal law bars the Education Department from refinancing federal student loans at lower rates. Borrowers with strong credit and income can replace their federal loans with cheaper private loans from lenders such as Social Finance Inc.

Some have done so, costing the government forgone interest and leaving its portfolio more heavily weighted with borrowers who are less likely to repay, either because they didn’t graduate, they borrowed too heavily or have low-paying jobs.

Most loans that are refinanced are on the lower end of the scale, owned by people who can pay them off and don’t need the forbearance, deferment, IDR plans, and other programs offered by the federal government.

Forgiveness of even $10,000 would reduce those balances just enough to reduce private refinancing and keep them on the government’s books.

The Takeaway

Student loan forgiveness is a complex topic that deserves serious discussion, thought, and foresight. Reducing the overall cost of servicing these loans is just one aspect to be considered.

If you want a seat at the table (or at least a voice on the phone), call your congressional representatives and let them know your opinion.

Forgiveness? No forgiveness?

$10,000? $50,000? All of it?

Sooner or later, all of this will come to a head and we will get some type of student loan reform. Until then, learn how to work the system and protect yourself and your money.

Related Stories

- There is No Student Loan Crisis

- Student Loan Forgiveness Will Never Happen

- Conquer Your Student Loans

- 6 Quick Wins to Tame Your Student Loans

- Don’t Pay Off Your Student Loans

- How I Still Have $135,000 in Student Loan Debt (Even After 21 Years)

Most Recent Stories

- Biden’s $400 Billion Blunder

- I Just Found the Most Amazing, Honest, and Complete Report on US Government Finances

- Falling Birth Rates Will (Probably) Destroy the Economy

- The Forgotten Impact of the Booming Housing Market

- Biden’s Next “Big F***ing Deal”

Don’t miss my next article! Click here to get notified when I publish new material.

If you love the articles published in Money. Daily., then become a member of the Medium community and get full access to our full archives.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.