6 Quick Wins to Tame Your Student Loans

Don’t let the beast of student debt destroy your future.

Last updated: April 14, 2022

During the last few months of the year, former students around the country will exit their grace period and being to pay back their student loans, joining the legion of us who hold the $1.6 trillion in outstanding student loan debt.

Starting your repayment plan can be nerve-wracking, especially when you’re trying to pay off a six-figure debt.

However, there are some basic steps to take prior to your first payment, and they do not include wishing for mass student loan forgiveness. These also apply if you are several years out of college but struggling to get a grip on your loan situation.

Quick Win #1 — Get Your Loan Information

Find all the information from all your loans from all your servicers. You need to include public loans, private loans, and even personal loans.

Next, open up a Word document or other electronic means of writing down all this information. Just looking at individual loans will not lend itself to seeing your entire loan burden.

Write down the following info.

- Type of loan

- Current balance

- Interest rate

- Current repayment plan

- Disbursement date (this is mainly for borrowers with older loans)

Quick Win #2 — Sign Up for Auto-Deduct

For federal loans, signing up for the auto-deduct program reduces your interest rate by 0.25%. If that sound small, that’s because it is…on an annual basis.

However, it actually has quite a large impact once you apply it to the entire lifespan of your loans.

Average Example

Say you graduated with a shiny new bachelor’s degree that also comes with an average student loan balance of $37,000 and an average interest rate of 4.79% on the standard 10-year repayment plan. (Yes, I’m calling you average. In stocks, that’s not a bad thing.)

- Monthly payment amount: $389

- 10-year repayment total: $46,639

Now, let’s apply that 0.25% interest rate reduction due to the auto-deduct program.

- Monthly payment amount: $384

- 10-year repayment total: $46,101

That gives a 10-year cost savings of $538, not counting for inflation. It’s not super exciting, but it’s also not nothing considering you’re just paying a bill that needs to be paid.

Extreme Example

Now here an example from the upper bounds of student loan borrowing. Let’s say that you have finished just finished your master’s program with a loan balance of $150,000 and an interest rate of 6.36%. And let’s combine that with your $75,000 in undergraduate debt with the same interest rate as before. That leaves you with the following.

- Monthly payment amount: $2,480

- 10-year repayment total: $297,546

Again, signing up for auto-deduct and gaining the 0.25% interest rate reduction give us

- Monthly payment amount: $2,452

- 10-year repayment total: $294,182

That gives a savings of over $3,000.

Granted, the $3,000 in savings might seem trivial compared to the $300,000 in total payments (on a $225,000 original principal). But if you can afford to pay that money back, I’m sure you also care about the value of a dollar and know that the $3,000 invested over long periods of time will do nothing but grow.

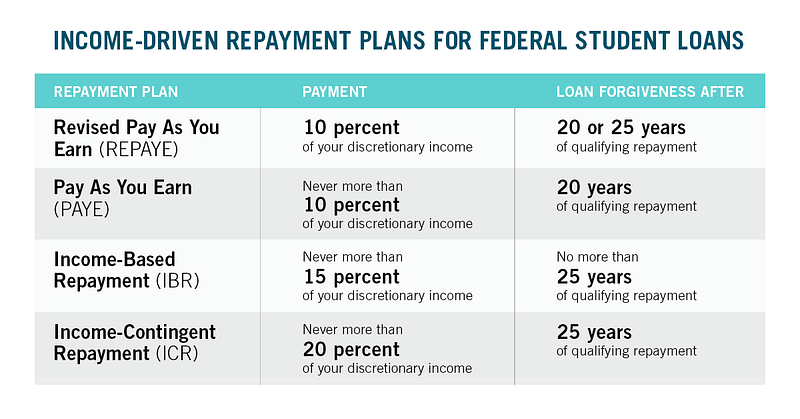

Quick Win #3 — Get on the Correct Repayment Plan

You might be on the standard 10-year plan in hopes of getting rid of your student debt relatively quickly and cheaply, but right now it’s breaking your budget into little tiny pieces. If you need a breather, Congress created the Extended, Graduated, and Extended Graduated plans that start low and increase automatically as time goes by.

Unfortunately, there is no control over any of these three plans. They are dependent upon your student loan balance and agreed upon payoff time. Plus, they are not eligible for Public Service Loan Forgiveness or forgiveness at the end of the repayment period, which is a super big drawback for a repayment plan that could take up to 30 years.

My suggestion is to forgo these plans and sign up for an Income-Driven Repayment (IDR) plan.

On the whole, these plans are a solid option and have the following benefits.

- Eligibility for PSLF (should you decide on a career in the public sector)

- Loan forgiveness at end of repayment period (but with a tax bomb)

- Consideration of income and family size into their calculations

Maybe you know your career will take off but can’t quite afford the standard payments yet.

Maybe you want to join the Peace Corps, take a post-graduate gap year, or whatever.

Maybe you had an unexpected set of triplets with your college sweetheart and need to divert money to your diaper fund for two years.

Instead of putting your loans into forbearance or deferment while on the 10-year plan while you are living your life (thus extending it past 10 years), get on one of the many IDR plans and keep making your payments.

Another benefit of this is that you might find that you want to be in the generally lower paying public sector for your entire career. Instead of paying the full amount, pay lower, then get everything forgiven with PSLF.

Quick Win #4 — Start Saving for the Tax Bomb at Forgiveness

One of the drawbacks of the IDR plans is the tax bomb upon forgiveness.

Just what is the tax bomb you may ask?

In short, you must pay federal and state income tax on any student loan debt that is forgiven at the end of your IDR repayment period. Per IRS Topic №431,

In general, if you have cancellation of debt income because your debt is canceled, forgiven, or discharged for less than the amount you must pay, the amount of the canceled debt is taxable and you must report the canceled debt on your tax return for the year the cancellation occurs.

Upon forgiveness, you will receive a 1099-C, Cancellation of Debt. This is just like any other 1099 you may have received in your career and will be treated as income.

If you are reading this article, the upside is that you are now armed with this information and can start preparing now. To calculate your tax bomb, simply put your information into this loan calculator I created. It will show your total amount forgiven and your tax bomb exposure using an estimated income tax level at forgiveness.

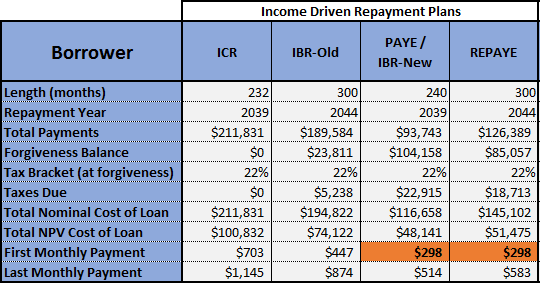

As a simple example, let’s say someone graduates with $150,000 in undergraduate loans at 6% interest, with a starting salary of $55,000. He stays single for the entire time and keeps with the PAYE plan.

After 20 years (plus six months of grace), he will owe $22,915 in taxes due to the forgiven amount of $104,158 being taxed as income.

Now, you might say that this completely sucks. But if you look at the Total NPV Cost of Loan, it is only $48,141 in today’s dollars.

So, our borrower has taken a loan of $150,000 today, and paid it off with less valuable future money that is only worth $48,000 today. And that’s including the tax bomb.

Now that you know what the tax bomb is and how to calculate it, just work backwards.

For our borrower, he will owe $23,000 in 20 years. That’s just under $100/month that he needs to save to pay off the tax bomb. He needs to start a savings or sub-savings account and start automatically putting money in there.

If you’re in a similar situation but can’t afford $100/month, then start with $50. Or even $20. Just start. Put in what you can and increase your monthly amount as you increase your income.

One thing to keep in mind though, you need to treat this as an actual expense, not some random money laying about that you can dip into whenever the mood strikes.

Quick Win #5 — Update Your Family Size

Life changes all the time: accidents, babies, accidental babies. You get the idea. The government finally allowed student loan repayment plans catch up to tax law and allow for changes to your family.

The IDR plans are actually quite humane, in that family size is not restricted to just immediate family, e.g. spouse and/or children. Family size can be quite different than that reported on your taxes.

The definition of family size is below, from studentloans.gov

Family size always includes you and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you.

For the PAYE, IBR, and ICR Plans, family size also always includes your spouse.

For the REPAYE plan, family size includes your spouse unless your spouse’s income is excluded from the calculation of your payment amount.

For all plans, family size also includes other people only if they live with you now, receive more than half their support from you now, and will continue to receive this support for the year that you certify your family size. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, and payment of college costs.

For the purposes of repayment plans, your family size may be different from the number of exemptions you claim on your federal income tax return.

This is pretty nice. If your mom dies and you have to take care of your dad, as long as you’re providing “more than half their support”, you can claim them as family and lower your monthly student loan payment.

However, there can be problems with this arrangement.

The leniency in family size is due to the fact that the only tax information that FedLoan uses is your reported AGI. Dependents/family size are self-reported. Unfortunately, that’s how this happened, from a recent GAO report.

About 40,900 IDR plans were approved based on family sizes of nine or more, which were atypical for IDR plans. Almost 1,200 of these 40,900 plans were approved based on family sizes of 16 or more, including two plans for different borrowers that were approved using a family size of 93. Borrowers with atypical family sizes of nine or more owed almost $2.1 billion in outstanding Direct Loans as of September 2017.

Yes, you could screw the system and claim 93 dependents. Just don’t do it. Let us all have the nice things and be honest.

As with most other student loan advice, update your family status regularly.

- Get married? Update your servicer.

- Get divorced? Update your servicer.

- Adopt a set of triplets? Update your servicer.

Fun fact: when updating your family size due to a new biological child, you can claim that child before birth, but only in the calendar year it is due. That’s great for parents of kids due in November, but it sucks if your due date is in January.

Quick Win #6 — Make Less Money

This step isn’t about going into poverty until your student loans are forgiven. Quite the opposite.

I want you to earn as much money as possible and report as little of it as (legally) possible to the IRS.

The primary benefit of lowering your AGI is a reduction of your student loan payments on the IDR plans. The secondary benefit is all the money that will be coming in from where you’re putting the tax-free funds, as well.

So, what can lower your AGI? Aside from the standard IRS deduction, lots of things!

- Pre-tax retirement contributions

- Post-tax medical expenses (if over 10% of your AGI)

- Mortgage interest

- Student loan interest (This is just all sorts of meta. Student loans payments can help reduce your student loan payment)

{kind=link}

While the size of your monthly student loan payment shouldn’t the primary influence on your tax returns, just be aware that there is a ripple effect of your financial decisions.

The Takeaway

These are some of the baseline steps to take when tackling your student loans. While not comprehensive, these will get you well on your way to seeing the big picture of your loan situation and put you on the right payoff path.

Remember, paying off your student loans means playing the long game. Do your own research and apply what works for your life. No one knows it better than you.

Best of luck!