Does Family Size Effect Your Student Loan Payment?

How a big family can save you big(ish) money.

Unless you are one of the dwindling few student loan borrowers who are on a fixed payment plan, your monthly student loan amount is heavily dependent upon two main items: income and family size.

Most Income Drive Repayment (IDR) plans rely on calculating your family’s “discretionary income”, which is calculated by subtracting some multiple of the the federal poverty level from your annual salary.

The important thing to know is the baseline poverty level changes with the size of your family, increasing with every dependent, so it is important to count every last person that depends on you.

What is Discretionary Income?

There are four main IDR options in the repayment plan portfolio, each with their own maximum payment:

- Income-Contingent Repayment (ICR) — maximum of either 20% of discretionary income or 12-year standard payment

- Income-Based Repayment (IBR) — maximum of 10% of discretionary income (15% for loans taken prior to July 1, 2014)

- Pay As You Earn (PAYE) — max of 10% of discretionary income or 10-year standard payment

- Revised Pay As You Earn (REPAYE) — max of 10% of discretionary income, with no payment cap

There are various rules and requirements that define your ability to enroll in each of these plans. For instance, PAYE was originally created for new borrowers who took out student loans starting October 1, 2007 or later, and was created as a simpler, less expensive option to ICR or IBR.

REPAYE was created soon after to allow existing borrowers to take advantage of the lower 10% payment limit, with the caveat being that the 10% had no cap, so you could ultimately end up paying more than the standard 10-year monthly payment.

The key to these repayment plans, though, is the discretionary income calculation. So what is it?

Here is the official definition of discretionary income as found on the studentaid.gov website.

Pertaining to the Income-Based Repayment Plan, the Pay As You Earn Repayment Plan, [the Revised Pay As You Earn Repayment Plan], and loan rehabilitation, discretionary income is the difference between your annual income and 150 percent of the poverty guideline for your family size and state of residence.

Pertaining to the Income-Contingent Repayment Plan, discretionary income is the difference between your annual income and 100 percent of the poverty guideline for your family size and state of residence.

The poverty guidelines are maintained by the U.S. Department of Health and Human Services.

That seems simple enough. Discretionary income, or the amount earned above and beyond the absolute basics, is the difference between your salary and some percentage of the federal poverty guidelines.

The next question is: how does the government define “family size”?

Going Beyond Children

Once you are on the appropriate IDR plan, the next step is to update your family size as soon as you can to get an accurate monthly payment.

The definitions of family size for various IDR plans are below, per studentloans.gov.

- Family size always includes you and your children (including unborn children who will be born during the year for which you certify your family size), if the children will receive more than half their support from you.

- For the PAYE, IBR, and ICR Plans, family size also always includes your spouse.

- For the REPAYE plan, family size includes your spouse unless your spouse’s income is excluded from the calculation of your payment amount.

- For all plans, family size also includes other people only if they live with you now, receive more than half their support from you now, and will continue to receive this support for the year that you certify your family size. Support includes money, gifts, loans, housing, food, clothes, car, medical and dental care, and payment of college costs.

- For the purposes of repayment plans, your family size may be different from the number of exemptions you claim on your federal income tax return.

Unborn Children

I want you to focus on the first item;

Family size always includes…unborn children who will be born during the year for which you certify your family size.

If you are expecting a little bundle of joy, you can call up yourstudent loan servicer as soon as you feel comfortable (I know most people don’t like saying anything until after the 1st trimester) and report the unborn child as an additional family member.

Even if you wait until after the first three months, you will still receive an additional six months of lower payments.

Extended and Non-family “family”

Equally important is the fourth item in the list above. As you can see, family size does not just include adding a new baby, biologically born to a heterosexual couple. The concept of “family” is vast, and the student loan servicers have policies that reflect that. If you are adding anyone that could be considered a dependent, update your student loan profile to reflect that.

This could mean adding an ailing parent who recently moved in as a dependent.

This could mean adding a foster child for the months or years you are responsible for them.

This could mean adding your recently laid off best friend if you provide more than half the cost of living.

This could mean adding your career-changing brother-in-law who hasn’t landed a job in his new field yet.

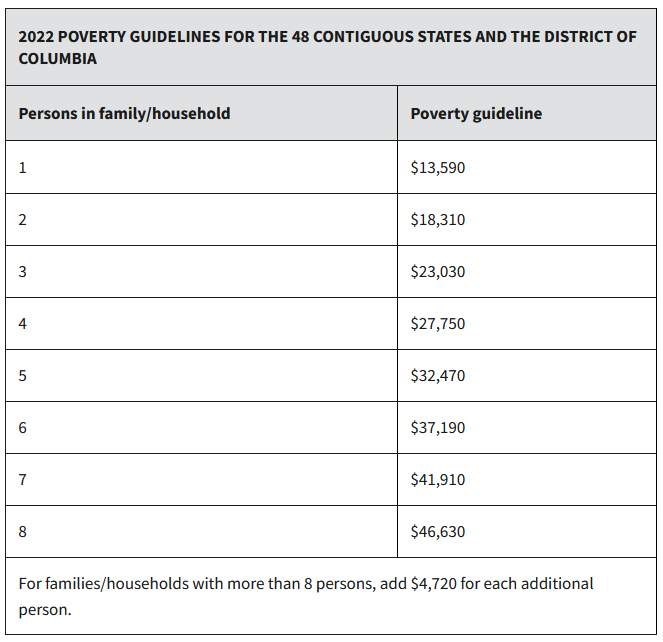

Running the Numbers

Below are the federal poverty guidelines for the continuous 48 states. Alaska and Hawaii are high cost of loving areas, so they have their own guidelines.

For each additional family member, the poverty limit increases by $4,720, reducing your discretionary income by that same amount.

Given the respective discretionary income calculations for each plan, here are the annual savings per person

- ICR (20% of discretionary income): $944/person/year

- IBR (15% of discretionary income): $708/person/year

- PAYE/REPAYE (10% of discretionary income): $472/person/year

This might not sound like a lot, but it adds up over the months and years of paying off your student loans.

For example, say you just got married and find out your wife is pregnant 4 weeks later (totally not pulling from real life).

You just went from a family of 1 to a family of 3, which will save you just under $1,000/year, every year, until you pay off your loans. I don’t know about you, but an extra $1,000 is nothing to sneeze at.

The Takeaway

With the increased prevalence of blended families, multi-generational families, non-traditional families, and every other kind of family unit you can think of, opportunities abound for you to claim someone as a dependent for the sake of student loans.

Don’t sell yourself short thinking that you’re “just helping someone get on their feet” by supporting them, even for a little bit. Take advantage of your generosity and report it to your student loan servicer.

Making sure you accurately account for everyone in your family is one of the many ways to lower your student loan payments. Other include contributing to your medical FSA/HSA or pre-tax retirement accounts are among many others.