A Simple Guide to Public Service Loan Forgiveness

After years of being vilified, PSLF is easier than ever.

There has been plenty of ink spilled about the Public Service Loan Forgiveness (PSLF) program in the past couple of years, and some of it is quite fear-inducing. Coverage about the PSLF program has picked up since October 2017, which marked the first month of eligibility for loan forgiveness in the program.

- Problems plague student loan forgiveness program — USA Today

- Data Shows 99% Of Applicants For A Student Loan Forgiveness Program Were Denied — NPR

- The Incredible, Rage-Inducing Inside Story of America’s Student Debt Machine — Mother Jones

- Just 5% of people who applied for public service loan forgiveness have qualified — CBS

The overall thesis is that, unsurprisingly, the government agency in charge of the program (Department of Education) and the government contractor paid to service the loans (FedLoan Servicing) vastly underrated both the popularity of this program and the complexity of executing the actual forgiveness.

In fact, things got to bad for FedLoan that they cried “Uncle” and gave up on servicing the PSLF program. Already, the DOE is moving those borrowers who have already made progress towards forgiveness to the new servicer, MOHELA, with the migration of all borrowers to be complete by May 2022.

While this may paint a dim picture of the validity of the PSLF program, it is still a viable path to eliminate your student loans in a relatively short amount of time. We will discuss further shortcomings later, but know that the brunt of the problems were born by the first group of forgiveness applicants.

This article is for those who are either still working towards their 120 payments or are interested to if they qualify. It covers the basics of what the PSLF program is and how to avoid the major pitfalls to qualify for forgiveness.

How to Qualify for PSLF

As with any program, there are certain things you need to do to receive the benefit. For PSLF, you need to have the following four qualifying items:

1. Qualifying Employment

2. Qualifying Loans

3. Qualifying Repayment Plan

4. Qualifying Number of Payments

However, like any government program, this one has had its share of problems over the year, some of which will be addressed further.

Qualifying Employment

There are two main things that make your job qualified for PSLF.

1. The type of employer you work for

2. Your employment status

You need to get them both correct to receive PSLF. Too many people received too many wrong answers to the qualifying employment question at the beginning of this program, and then were refused forgiveness. Don’t let that be you!

Type of Employer

From studentaid.gov, the following types of full-time employment are eligible for the PSLF program.

- Government organizations at any level (federal, state, local, or tribal)

- Not-for-profit organizations that are tax-exempt under Section 501(c)(3) of the Internal Revenue Code

- Other types of not-for-profit organizations that are not tax-exempt under Section 501(c)(3) of the Internal Revenue Code, if their primary purpose is to provide certain types of qualifying public services

The website also notes that a “full-time AmeriCorps and Peace Corps volunteer” also counts as qualifying employment. The IRS even has a Tax Exempt Organization Search to help verify qualifying non-profits employers.

This all seems pretty straightforward.

- Government job? No problem.

- Not-for-profit? Good to go.

- Peace Corps? Fantastic.

However, problems arise from the last bullet point above: non 501(c)(3) companies that provide “qualifying public services” and the determination of those services. This article from Forbes describes how some lawyers worked for a non-501(c)(3) organization that provided these services, then were told after submitting their forgiveness applications that the services, in fact, did not qualify.

Being lawyers, they sued the DOE and won. The two main takeaways from this are a) ensure your employment qualifies (which they did) and b) consistently check up on FedLoan Servicing and the DOE. In the judgment, the court found that both entities acted “arbitrarily and capriciously”, with neither term inducing confidence. Don’t depend on anyone to keep track of your forgiveness; it’s up to you.

Fortunately, there is a handy search tool to help verify that your employer is qualified for the PSLF program.

You may have also noticed that the term “full-time” is used as an employment descriptor. We will address that in more detail below.

Employment Status

In the previous section, we discussed the type of employment. There is also an employment status requirement, in that payments must be made during full-time employment at a PSLF qualifying employer. Full-time employment is defined as meeting “your employer’s definition of full-time or work at least 30 hours per week, whichever is greater.”

Now, I understand that many of you are part of the gig economy. This was especially true during the Great Recession when loads of overqualified college graduates were holding down multiple part-time jobs. The good news is that the PSLF program does allow for part-time work to count towards full-time employment.

Per studentaid.ed.gov:

If you are employed in more than one qualifying part-time job at the same time, you may meet the full-time employment requirement if you work a combined average of at least 30 hours per week with your employers.

Bear in mind that any part-time employment must be at a qualified employer for the PSLF program.

For example, you can’t work 40 hours a week in the private sector then spend your Saturdays as a janitor for 8 hours at your local government offices, then claim full-time employment under PSLF. This situation would only allow 8 hours of qualifying employment, with an unapproved employment certification application.

Lastly, don’t fall into the 29-hour workweek trap that has become so popular since the advent of ObamaCare. The same workaround that employers use to workaround required healthcare will screw you out of loan forgiveness if you’re not careful.

Qualifying Loan

Originally, only one type of loan was available for PSLF, and that was a loan that was made under the William D. Ford Direct Loan Program. The Direct Loan program was created by the Health Care and Education Reconciliation Act of 2010, with the first loans disbursed under the program the fall of that year.

This is the important part. If you have loans that were taken out before July 1, 2010, then they will need to be consolidated into a Direct Loan to be eligible for PSLF forgiveness.

Only Direct Loans are eligible for PSLF.

This is a nasty little detail that so many people in the first cohort realized only after 10 years of payments.

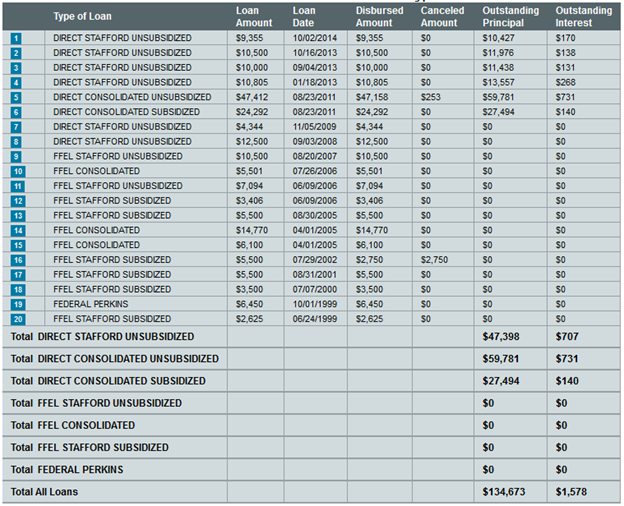

Below is a history of my student loans along with current balances from the National Student Loan Data System. Long story short: I started school in 1999; dropped out in 2002; went back in 2005; graduated undergrad in 2009; went to business school in 2012; graduated business school in 2013.

In August of 2011, I put all my undergraduate loans (#7 through #20) into subsidized and unsubsidized Direct Consolidation Loans (#5 and #6). Since they were made after 2010, all my graduate loans (#1 through #4) are Direct Loans, too.

Imagine for a minute, that I failed to consolidate those undergraduate loans. I’m chugging right along thinking that everything will be gone in 10 years. When I submit my forgiveness application and finally get a response, I am told that only $47,000 out of $135,000 had been forgiven, leaving me on the hook for the remaining $88,000. Yowzah!

But that’s exactly what happened in late 2017. And now those poor bastards are completely starting the clock over again, with a minimum of another decade of payments ahead.

Fortunately, the Department of Education has since added a limited waiver to the PSLF program so that “…borrowers may receive credit for past periods of repayment that would otherwise not qualify for PSLF.” This waiver expires October 31, 2022. That may seem like a long time, but given the historically bad response rate from all student loan servicers added to the transition to MOHELA means you should start applying ASAP.

Qualifying Repayment Plan

As you might already be aware, student loan debt is not like a mortgage or credit card debt. It is a unique beast unto itself. This section goes over the requirements for each qualifying payment as well as common mistakes.

To be eligible for PSLF, you need to be on any of the income-driven repayment (IDR) plans available. Using statistics, IRS data, and voodoo magic, these plans base your monthly payments on your income.

The four IDR plans available are

- Income-Contingent Repayment Plan (ICR)

- Income-Based Repayment Plan (IBR)

- Pay As Your Earn Repayment Plan (PAYE)

- Revised Pay As You Earn Repayment Plan (REPAYE)

The reason for this requirement can, amazingly, be explained quite fully by the government financial aid website.

Even though the 10-year Standard Repayment Plan is also a qualifying repayment plan for PSLF, you cannot receive PSLF unless you enter an income-driven repayment plan. Here’s why: If you are in repayment on the 10-year Standard Repayment Plan during the entire time you are working toward PSLF, you will have no remaining balance left to forgive after you have made 120 qualifying PSLF payments. Therefore, if you are seeking PSLF and are not already repaying under an income-driven repayment plan, you should change to an income-driven repayment plan as soon as possible.

For the most part, that makes sense.

Note that while the IBR and PAYE plans will never allow your monthly payment to go above the 10-year standard repayment amount, ICR and REPAYE do not have such a clause. That means that if you and/or your spouse are very high earners, it is feasible that your monthly payment will be much higher than you might have planned.

Given that the IBR plan was created via the same bill that created PSLF, it was hard to get on the IBR plan even if working for a PSLF eligible employer. Additionally, the employer certification form was not even available until three years after the program was created, so there were no verifications for either employer or repayment plan until 2010.

There is little wonder, then, that many people applying for PSLF in October 2017 found out that they had been on the wrong repayment plan the whole time.

Fortunately, there was enough hubbub about this oversight that the DOE created the Temporary Expanded Public Service Loan Forgiveness program. In short, it allows for otherwise eligible borrowers to apply for forgiveness even though they were not on an approved repayment plan.

For those who have not started or are in the early stages of earning your monthly payments, I would encourage you not to depend on TEPSLF being around in 10 years. Get a Direct Consolidation Loan and you won’t have to worry about it.

Number of Payments

“Debt free in 10 years!”

The PSLF program markets itself as a way to get out from under your student loan debt in 10 years with minimal monthly payments. The exact requirement is that you make 120 qualified payments while employed by a qualified employer. The 10-year timeline is based on making those 120 monthly payments on-time every month, without fail. However, like anything else that sounds too good to be true, it’s not quite that simple.

Grace Period

As mentioned above, payments made during your 6-month grace period after leaving school, either by graduating or dropping out (I’ve done both), do not count as qualifying PSLF payments. Take advantage of this six months to review your income (read: job prospects) and expenses.

If you are employed at a qualifying employer, I encourage you to apply for an IDR repayment plan and then the PSLF program during your grace period. That way, by the seventh month after graduation, you should not have to worry about FedLoan Servicing needing to retroactively apply payments.

Forgiveness Application Period

One of the many things that caught the first PSLF cohort off-guard was the fact that they still needed to be employed at a qualifying employer while FedLoan Servicing and the DOE made their forgiveness decision. This is in the fine print, again per Federal Student Aid:

You must be working for a qualifying employer at the time you submit the application for forgiveness and at the time the remaining balance on your loan is forgiven.

That also means that you need to keep paying your monthly loan payments during this time.

So, don’t just assume that your loans will be forgiven after you make the 120th payment, then run off and get that sweet hedge fund job. Nothing is official until it is. Stick it out until you get the paperwork, have called FedLoan, talked with DOE, and whatever else it takes for you to ensure, come hell or high water, that you have in fact received your loan forgiveness.

Given that forgiveness verification can take up to another 6 months, the total minimum time for PSLF forgiveness is 11 years.

Other Pitfalls

We have just run through the main qualifications for PSLF, but there are mistakes that can happen along they way even if you do check all the boxes detailed above.

Amount and Date

First and foremost, like just about any other type of debt, the payments need to be on-time and in-full. No surprise there. As an FYI, on-time is defined as a payment that is “received no later than 15 days after the payment due date.” However, as a best practice, it is best to sign up for direct debit and have your loan payment debited automatically from your checking account.

As a bonus, you get a 0.25% interest rate reduction for signing up for direct debit. That may not equate to much if you are planning on PSLF, but life has a way of changing your plans. Best to take advantage.

Qualifying Repayment Periods

Next, your payments only qualify towards your 120 if you make them during a time when you are actually in repayment. Any payments made during grace, deferment, or forbearance periods do not count.

I had a personal experience with this, as I made qualifying payments on my undergraduate loans while my graduate loans were in their grace period. Now I have different totals of PSLF payments for two different groups of loans. This adds a layer of complexity to forgiveness, but I will repeat that you need to track this yourself. Don’t rely on anyone else to do this for you.

Paying Ahead

Now, if you have gone through all these hurdles, there is yet another trap that some people fall into: paying ahead.

It used to be that you absolutely could not make forward payments on your PSLF eligible loans. The loans would be considered in “pay ahead” status, and any less-than-full payment paid the next month would not be counted.

The DOE fixed this problem in January 2020. Kind of.

You can now pay ahead up to 12 months in advance, but only those 12 months. If your payment is $100/month, you can pay up to $1,200 in a single deposit for the whole year. However, if you pay $2,400, you will still only receive 12 months’ worth of credit towards PSLF. The remaining $1,200 will just be credited towards your loan amount.

My suggestion is to just pay the monthly amounts when they are due to avoid any possible conflicts that could jeopardize your forgiveness.

The Takeaway

At the moment, the PSLF program is up and running, albeit creakily. While it might seem like a huge burden, the steps outlined above will make sure that you are not making unqualified payments.

To recap, make sure you

- Are working for a qualified employer

- Have a qualified, full-time position at that employer

- Have qualified loans

- Are making qualified payments

- Are certifying annually

If you track your payments, certify annually, and don’t pay ahead, then the PSLF is actually quite easy. The round of applicants was always going to have the toughest time, but unfortunately a “tough time” turned into a national embarrassment.

Now that the DOE is working out the kinks and the student loan servicers are finally getting their acts together, the program will see much higher approval rates in the near future.