Mortgage Prepayments

Not that you asked, but a penny spent is a penny saved.

Check with the mortgage lender on prepayment penalties, if any, and that extra payments pay down the principal, and not toward interest.

While I have striven to be accurate, these figures are illustrative, and can differ based upon timing of payments, the mortgage itself, and other factors.

The basics of a mortgage is that there is borrowed money (the capital) at a given interest rate, with payments due over a preset time period. The mortgage payment is broken into two parts:

- Principal

- Interest

The easiest way to save money on interest paid is to pay more of the outstanding loan per month. Paying more per month can save thousands of dollars without a large impact to a budget. Let’s take a look.

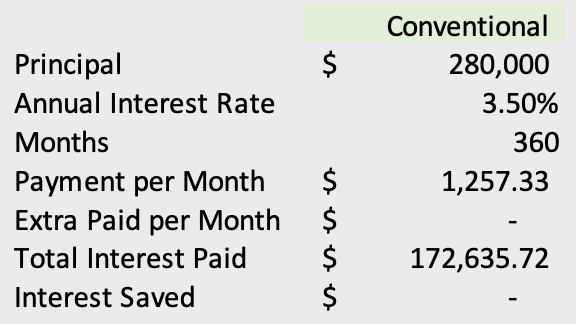

Conventional Mortgage

For the comparisons, a conventional 30 year mortgage is used. The same principals apply to other mortgage types, but the results will differ.

That is a 30 year mortgage of $280,000 at 3.5%. The payments per month are set at $1,257.33, and the total interest paid will be $172,635.72. There are no extra monies paid per month, and the interest saved is zero; those are used to compare other repayment strategies.

The $280,000 owed does not change regardless if you pay it across 360 months, or if you increase your payments: you borrowed $280,000, so you get to pay back $280,000.

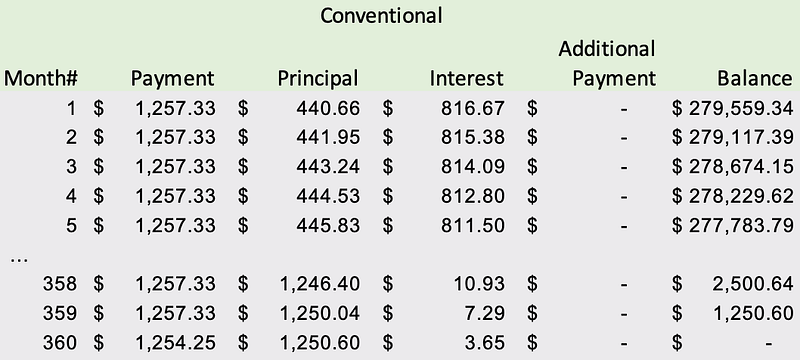

The start and end of the loan amortization schedule looks like:

Amortization schedule is loan-speak for how your loan is repaid. It is the total amount paid per month, and how much is applied toward Principal and how much toward Interest. In this scenario, it is 360 payments (12 per year for 30 years). Very conventional.

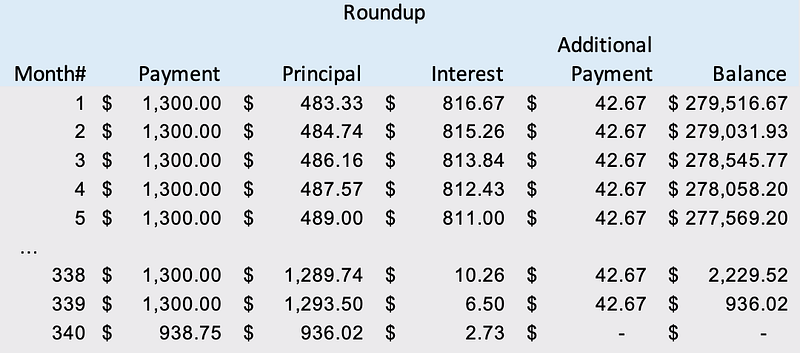

Rounding Up

Using the same loan, the amount paid per month is rounded-up. Instead of paying $1,257.33 per month, pay $1,300 (which is an additional $42.67 per month).

The new payment schedule includes the Additional Payment.

The Balance is paid down quicker, the number of payments are fewer, and the amount of interest paid decreases.

The Additional Payment helps pay off the loan quicker. That $42 extra paid each month no longer has interest due on it. The quicker the outstanding balance decreases the more savings there are in interest paid.

For example, in the Conventional loan, the second month of interest is $815.38 compared to $815.26 for the Rounding Up scenario. That is only saving $.12, but those pennies add up over the life of the loan, as shown further in the article.

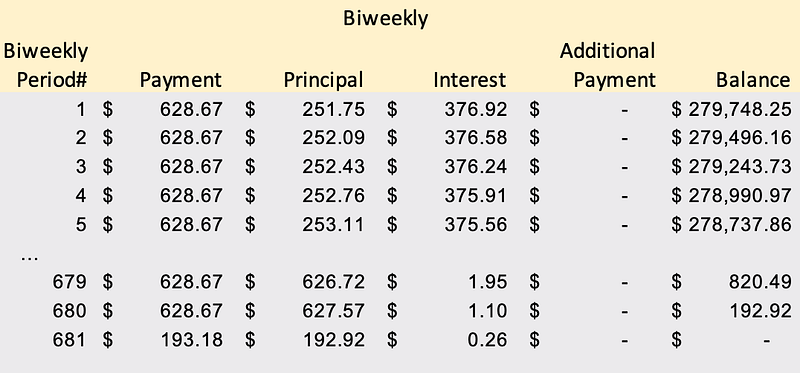

Biweekly Payments

In this accelerated payment plan, mortgage payments are every two weeks instead on monthly. This works well if you have 26 paychecks in a year (paid every two weeks). Instead of 12 monthly payments, it is equivalent to 13 monthly payments over the year.

The number of payments increased as it is counting number of Biweekly payments instead of months. 681 payments is just over 26 years, so this shaves off nearly four years of payments compared to the Conventional repayment plan.

As with the other options presented, this will save interest paid over time, and shorten the loan.

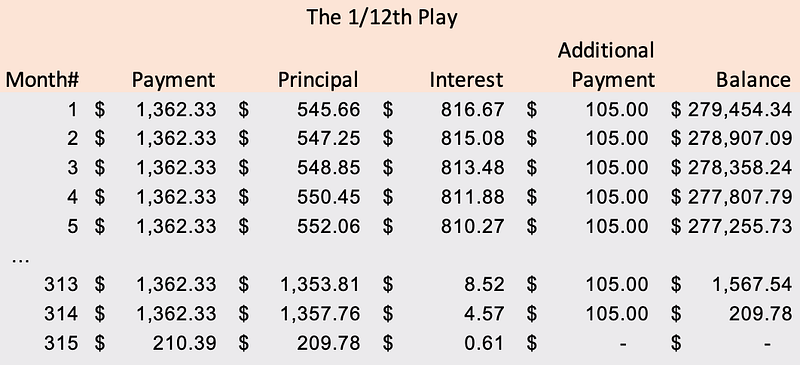

The 1/12th Play

This is very similar to the paying the mortgage Biweekly, but instead of sending payments every two weeks, it is still a monthly obligation like a Conventional payment. The difference is that the extra payment is added to the standard monthly amount.

The Conventional payment is $1,257.33 per month, and a 13th payment is wanted. To spread that payment over the year, $1,257 is divided by 12, which is $104.78. Instead of sending one extra payment of $1,257.33 during the year, we add $104.78 to the monthly amount.

In this example, $105 (rounding up) is added to the Conventional payment.

This is very comparable to the Biweekly scenario, as expected — they both result in the equivalent of 13 payments per year. This option is included as many people prefer 12 monthly payments versus 26 biweekly payments.

A Penny Spent is a Penny Saved

Fair enough, this is spending dollars to save dollars. All of these options are paying down a loan faster to reduce the interest cost, and the length of the loan.

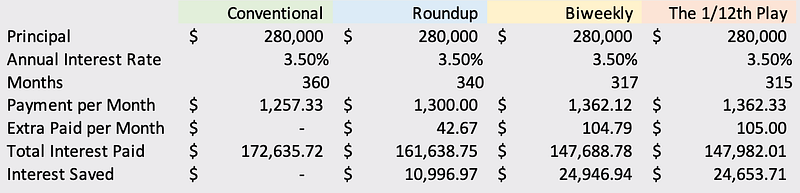

The final comparison:

Solely rounding up to $1300 per month will save nearly $11,000 in interest. Moving to Biweekly or 1/12th Play will save nearly $25,000 in interest.

Wrapping Up

The borrower is still paying $280,000 of principal regardless of the plan, as that is the amount borrowed. It is a matter of how quick that is paid and how that reduces total interest paid.

In the Roundup scenario, the monthly mortgage is increased by $42 per month, or roughly 3% extra per year. In both the Biweekly or 1/12th Play there is the equivalent of 13 monthly payments paid per year, which is roughly 8% extra paid per year.

There is an impact to your monthly budget regardless of the chosen path, so you would only pay extra if you can afford to.

The extra payments can add up to thousands saved so paying extra is worth investigating.

The Latest Stories From Money. Daily.

- 5 Reasons Why Aldi is So Goddamned Awesome

- A New Day for the Public Service Loan Forgiveness Program

- Do You Really Need a Savings Account?

- The Simple and Shocking Truth About Climate Change

- Evaluating Returns, CAGR style

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.