Why am I working on police brutality insurance?

When I have never been brutalized by the police

UPDATE: I originally wrote this post last year. I’m updating it in light of the killing of George Floyd by police officers and the subsequent protests. Since that time I’ve done significantly more writing and research.

Finding my pilot group

The MVP for the TandaPay app will be ready in December. I’ve got to find a pilot group of 50+ people for one of these four use cases:

- A group seeking coverage for the $500 auto insurance deductible

- A group who wants a whistleblowing app for police brutality

- A group who wants a whistleblower reporting app for sexual assault

- A group who wants to approve workers’ compensation claims independent from their employer

I’m far more interested in the whistleblowing applications of TandaPay because:

- TandaPay can likely provide the greatest benefit to ideological groups.

- Police brutality is a blight on society. To work toward a solution for this problem feels far more meaningful than to work on the $500 deductible.

- Most people are surprised to find out how much power insurers have over the police. This results in a reassessment of the power of insurance.

- Potentially TandaPay can do the most good by tackling the problem of police brutality first, before attempting other types of coverage.

So being naive I call up LBSBaltimore and a few other groups with a hopeful attitude. I’m sure I probably came across as a white version of Steve Urkel, “hey guys, can you try out my cool new app for police brutality insurance.” I didn’t say that, but I’m sure that’s how I sounded like to people. Everyone was polite, no one was rude but it was clear that this inquiry was not welcome. I got a lot of, “just email me and I’ll take a look at it.” If I tried to call back I would go to voicemail.

I never intended to work on police brutality as a cause

I’m just trying to find a reasonable use case for peer-to-peer insurance that doesn’t suck. I began working on this problem five years ago with my first whitepaper and TandaPay is my final attempt at solving the problem. A lot of time has been consumed by trying to solve this problem. Depending on what happens with TandaPay the past five years could have been the best investment or a total waste.

Then that’s just five years that are gone. It’s not the sort of thing where there’s a consolation prize. I definitely won’t feel, “oh well I gave it a good try, it’s all fine anyway. It’s just trying that counts.” No, I don’t believe that. I believe getting it right is what counts.

A simple solution for a complex problem

You’ve got to consider the legal liabilities, the potential use cases, incentives for the participants to join, the cost of premiums relative to claims, available markets, and more. There might be 10 to 20 different constraining factors that need to be taken into careful consideration. This is not an easy problem to solve. In the end you don’t get to choose what types of products you can or can’t cover. The constraints upon the problem continue to limit your options until very few viable choices are left.

One thing becomes abundantly clear. Decentralized platforms for insurance must produce more value than anything centralized companies could ever provide. A cheaper, more transparent version of what we already have isn’t good enough. Besides, blockchain isn’t cheaper to use and it certainly isn’t more user friendly. This value likely comes in the form of new insurance products that don’t exist yet.

But why then use blockchain? If blockchain is so inconvenient and so awkward as a technology why then even bother?

The allure of Blockchain technology

Blockchain has two unique value propositions that other types of payment and accounting systems lack.

Unimpeachable record keeping

If blockchain does one thing well it’s record keeping. This is not something human beings are particularly good at. When it comes to money, the chance of there being a discrepancy between the record and the actual fact is a problem. What does the record say the money was used for? What was the money actually used for? These two things are not guaranteed to have a perfect correspondence. With blockchain, an entity’s money and its accounting can become the same thing and that has never happened in the entire history of money.

Even if the initial record is created honestly, updating the record requires constant vigilance. Trust is a challenge for all records that are not blockchains. Without the blockchain, there is no guarantee of data integrity. This means that people can always come along later and change, tweak, improve, fix or massage a record entry. Doing so would leave no trace of what the original values were. In addition, the record can also be destroyed, either willfully or accidentally.

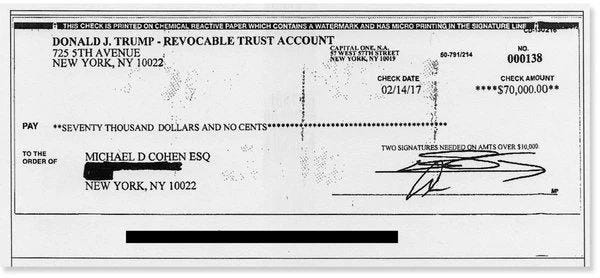

There is also no way to know for certain who created a record when humans do the record-keeping. In technical jargon, if you can know for certain who created an entry in a record then the database is said to have the property of non-repudiation. This is a very important property. Did one CEO sign the check or did two? Did one scribble on the second line to make it seem like two people signed the check? Who can understand these things? How can they even tell if that signature is even your signature anyways? What’s to prevent anybody from just stealing a check and scribbling on it? What’s to stop them from cashing it?

It’s when people start to actually look closely at how our financial system works that they realize it’s all a bunch of smoke and mirrors. That’s why we spend so much money on audits and anti-fraud measures and that’s why they are of so little use in actually deterring fraud.

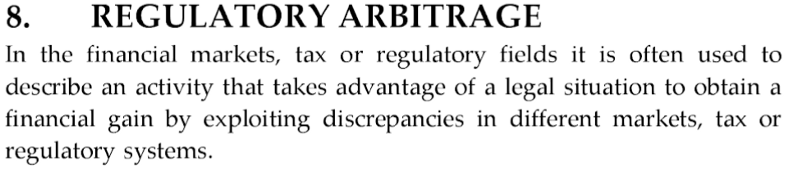

Immunity from unfavorable regulations

Given that human beings are not particularly good at record keeping, it comes as no surprise that keeping people honest requires frequent audits. Audits are the only way to ensure that an insurance company is investing your premiums wisely and paying legitimate claims. Audits are expensive because they require an army of auditors, accountants, and actuaries. This army of people is to records what security guards are to banks. To protect against theft you need guards to patrol a bank’s vaults. To protect against fraud you need accountants to patrol an institution’s records. Blockchains can do this better than humans can.

The goal is to automate trust. Can blockchains provide financial services without the expense of manual audits? If they could then they would be legally compliant by design. How much cheaper would it be to run a financial service on a platform with built-in legal compliance? Reducing the cost of legal compliance is very valuable. Blockchain technology is valuable because it has this superpower. Because audits are automated, a blockchain-enabled insurance app is like being in the carpool lane when all other forms of insurance are stuck in traffic.

Ideally, insurance on the blockchain will minimize regulatory liability using automation. By lowering the cost of compliance in this way, new financial services can be created. Specifically, the cost barriers for a small group of people to form their own insurance mutual can be drastically reduced. Previously if a group wanted to form a RRG or a discretionary mutual the initial legal costs involved were tremendous. The burdensome initial costs of time and money to create a nonprofit demonstrate the inefficiency of our regulatory system.

To mitigate the cost of this liability, groups have attempted to carve out exemptions for themselves in the law. This involved lobbying congress to change the law to create a specific exemption for their industry. Since no small groups can afford these huge up-front costs, this has effectively denied small groups access into insurance markets and removed their right to self-insure. This demonstrates how government regulation can become a crushing burden that prevents small groups from insuring each other.

By removing costly government regulations, people have access to new markets and opportunities. Do you like to save money? Lowering the cost of insurance is a great way to help the average person save money. I can’t think of a better way to save money in insurance markets than by avoiding the costs of unnecessary regulation. This is why regulatory arbitrage is like finding free money. If we can scale this model up in the future, peer-to-peer insurance may someday be able to compete directly with traditional insurers.

Sometimes you choose an idea and sometimes an idea chooses you

As I stated earlier I didn’t choose to create police brutality insurance. It resulted as the most promising option after studying various use cases. The initial concept of the $500 auto insurance deductible made logical sense but there was still several problems:

- Mutual insurance requires coordination, coordination requires time. People are effectively sacrificing two hours a month to get cheap deductible coverage.

- Acquiring and using cryptocurrency requires the group leader to take several hours to learn the technology and several hours each month to assist users.

- The technology is new and has its unique shortcomings and disadvantages. Is deductible coverage valuable enough for groups to persist and not give up?

I felt that the technology just wasn’t there yet to be able to provide sufficient value for this use case. I needed a use case that was more compelling than deductible coverage. I put aside everything I thought I knew about insurance and started thinking about what might be special about this type of insurance. That’s when I made my critical breakthrough.

Putting aside the value of covering a claim, can TandaPay do anything else? It creates an official, historical record of what everyone in a community believes. I thought about this for a while. Is this type of record keeping valuable? Out of all the people and groups in the country, is there anyone who could stand to benefit from being able to create a record when an event triggers an insurance claim? Is there any community who can’t rely merely on government records, social media or blogs to tell their personal story?

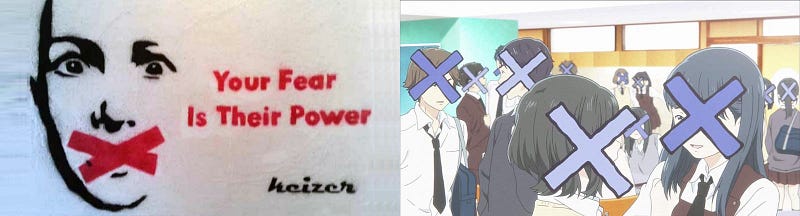

TandaPay’s records are censorship resistant

I remember hearing a podcast or reading a news article about how the posting of a police shooting video to youtube or social media was causing controversy. The violent content was in violation of the platforms ToS but if the content was taken down then the victims freedom of speech was being denied. Since the users didn’t have control over the platform this means they couldn’t be guaranteed their posts wouldn’t face censorship.

Bingo, the TandaPay protocol could provide users with a value going beyond the mere payment of an insurance claim. The creation of the record itself was valuable because it was censorship resistant and not subject to rules imposed by governments or other authorities.

Out of all the people and groups on the planet, who could stand to benefit the most from the ability to create an indisputable, censorship resistant record of history from the perspective of their local community? Insurance is a record of history documenting policyholders paying premiums and a policy paying out claims. But, if it exists on the blockchain it becomes a special type of record because it is granted the properties of data integrity and non-repudiation. The only record we have of what the police are doing in local neighborhoods today are:

- Official records kept by the police (not public)

- Unofficial records created by mainstream media outlets

- Blogs or social medial posts created by individuals

- Official records created when victims take the police to court, kept by the government

We seem to be missing a category of “official records kept by the community”

Conclusion

Blockchains are good at holding people’s money because they are good record keepers. They don’t permit any creative accounting and they can’t misplace people’s money. The best blockchain architectures for insurance are designed to be fully compliant with the law, without users needing to take any legal action to form a coverage group. This lowers the initial cost to start a group to nearly zero, which allows blockchain to provide new insurance products that could never be provided previously. When combined with the feature of censorship resistance, the value of offering police brutality coverage goes beyond merely paying a claim. Now communities have a censorship-resistant way of creating an unimpeachable, official record that represents the communities point of view.

UPDATE

I’ve written a lot over the past year. I’ve focused on effectively communicating this idea in these posts:

- Join the Financial Escrow Revolution

- The Kerner Commission’s Prescription for Effective Grievance-Response

- Information Escrows Get a Power-up

- The Politics of Sexual Harassment Data

- TandaPay is a weak insurance protocol — It is a powerful coordination protocol for galvanizing movements

- How P2P insurance can empower social justice in local communities

- Fraud Protections within TandaPay — How TandaPay safeguards policyholders from fraud

- True peer-to-peer insurance requires the blockchain to work

* Blockchains do not provide this by default. Just because policyholders give their premiums to a smart contract does not exempt the smart contract from acting as a third-party custodian of funds. Additional architecture is required to take advantage of blockchain’s capacity to eliminate custodial risk. TandaPay accomplishes this through the use of zero-reserve architecture.