True Peer-to-peer Insurance Requires the Blockchain to Work

Rewritten excerpts updated

These two features have enticed men to their doom

The allure of blockchain technology with regard to insurance products can be summed up in just two key points. I would consider these two points as “siren sisters” because their allure has drawn people to become “shipwrecked” upon the “jagged reefs” of reality. Blockchain can do a lot of neato things but in terms of insurance you’ve got to capitalize on both of these two points to score a win:

Unimpeachable record keeping

If blockchain does one thing well it's record keeping. This is not something human beings are particularly good at. When it comes to money, the chance of there being a discrepancy between the record and the actual fact is a problem. What does the record say the money was used for? What was the money actually used for? These two things are not guaranteed to have a perfect correspondence. With blockchain, an entity’s money and its accounting can become the same thing and that has never happened in the entire history of money.

Even if the initial record is created honestly, updating the record requires constant vigilance. Trust is a challenge for all records that are not blockchains. Without the blockchain, there is no guarantee of data integrity. This means that people can always come along later and change, tweak, improve, fix or massage a record entry. Doing so would leave no trace of what the original values were. In addition, the record can also be destroyed, either willfully or accidentally.

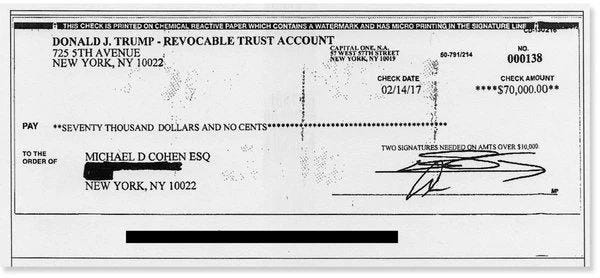

There is also no way to know for certain who created a record when humans do the record-keeping. In technical jargon, if you can know for certain who created an entry in a record then the database is said to have the property of non-repudiation. This is a very important property. Did one CEO sign the check or did two? Did one scribble on the second line to make it seem like two people signed the check? Who can understand these things? How can they even tell if that signature is even your signature anyways? What’s to prevent anybody from just stealing a check and scribbling on it? What’s to stop them from cashing it?

It’s when people start to actually look closely at how our financial system works that they realize it's all a bunch of smoke and mirrors. That’s why we spend so much money on audits and anti-fraud measures and that’s why they are of so little use in actually deterring fraud.

Immunity from unfavorable regulations

Given that human beings are not particularly good at record keeping, it comes as no surprise that keeping people honest requires frequent audits. Audits are the only way to ensure that an insurance company is investing your premiums wisely and paying legitimate claims. Audits are expensive because they require an army of auditors, accountants, and actuaries. This army of people is to records what security guards are to banks. To protect against theft you need guards to patrol a bank’s vaults. To protect against fraud you need accountants to patrol an institution’s records. Blockchains can do this better than humans can.

The goal is to automate trust. Can blockchains provide financial services without the expense of manual audits? If they could then they would be legally compliant by design. How much cheaper would it be to run a financial service on a platform with built-in legal compliance? Reducing the cost of legal compliance is very valuable. Blockchain technology is valuable because it has this superpower. Because audits are automated, a blockchain-enabled insurance app is like being in the carpool lane when all other forms of insurance are stuck in traffic.

Ideally, insurance on the blockchain will minimize regulatory liability using automation. By lowering the cost of compliance in this way, new financial services can be created. Specifically, the cost barriers for a small group of people to form their own insurance mutual can be drastically reduced. Previously if a group wanted to form a RRG or a discretionary mutual the initial legal costs involved were tremendous. The burdensome initial costs of time and money to create a nonprofit demonstrate the inefficiency of our regulatory system.

To mitigate the cost of this liability, groups have attempted to carve out exemptions for themselves in the law. This involved lobbying congress to change the law to create a specific exemption for their industry. Since no small groups can afford these huge up-front costs, this has effectively denied small groups access into insurance markets and removed their right to self-insure. This demonstrates how government regulation can become a crushing burden that prevents small groups from insuring each other.

By removing costly government regulations, people have access to new markets and opportunities. Do you like to save money? Lowering the cost of insurance is a great way to help the average person save money. I can’t think of a better way to save money in insurance markets than by avoiding the costs of unnecessary regulation. This is why regulatory arbitrage is like finding free money. If we can scale this model up in the future, peer-to-peer insurance may someday be able to compete directly with traditional insurers.

To read this post in its entirety see link.

How the technology accomplishes this task

Perfect data integrity and regulatory arbitrage are built upon two key technologies:

- Digital signatures: these provide the features of non-repudiation as described above. They also eliminate third party custodians by allowing policyholders to hold their funds directly.

- Blockchain protocols: these serve to solve the double spending problem that is inherent in all digital cash systems which rely on digital signatures to establish ownership.

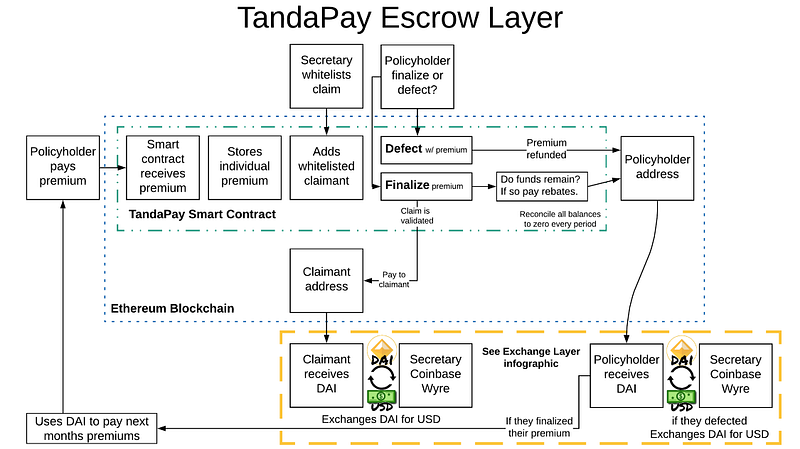

Blockchain protocols work in the background when we interact with smart contracts. This would be similar to how routing protocols on the internet allow us to get to websites. We are not required to understand how they work in order to understand how policyholders who use TandaPay retain custody of their premiums. To understand how custody of funds works in TandaPay we only need to understand how digital signatures work. TandaPay performs the following two primary tasks:

- Allowing policyholders to secure custody of their premiums

- Allowing policyholders to assign custody of their funds to claimants

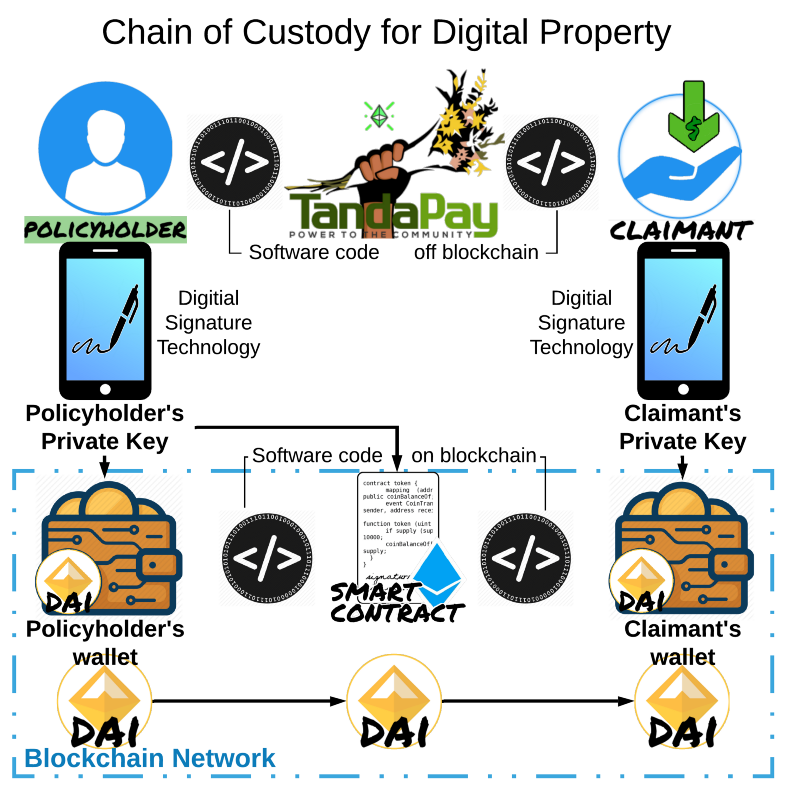

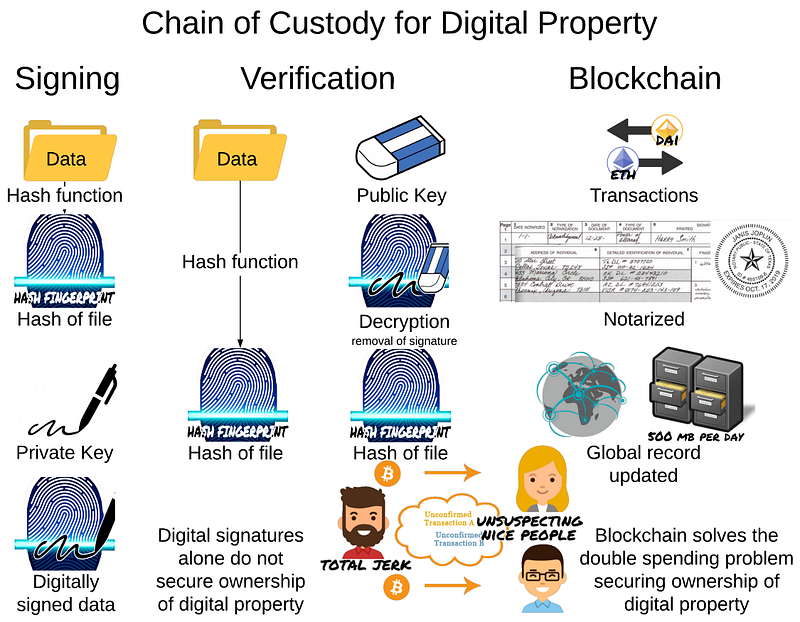

The below two images give us a high level overview of this process. The icon that ties these two images together is the pen icon. Digital signature technology establishes the following chain of custody:

- A policyholder is in custody of their phone

- A phone contains the private key (pen icon) needed to sign transactions which: * Authorizes payment of premiums to smart contracts * Authorizes payment of premiums from smart contracts to claimants

- The private key (pen icon) is directly tied to a wallet address on the blockchain which holds the policyholder’s funds. Only the private key can authorize transactions which move funds from the policyholder’s wallet to another wallet address (or smart contract address) on the blockchain.

- If the policyholder sends funds to the TandaPay smart contract the code gives them specific permissions. If a transaction using the policyholder’s private key (pen icon) is received it can: * Authorize that the premium be sent to the claimant. * Authorize that the premium be returned to the policyholder.

The image above focuses on how custody of funds works in TandaPay.

The image below focuses on how digital signatures work.

Use of public-key cryptographic systems and blockchain technology are the means by which we eliminate third party custodians. A Private key held inside of a phone is the means by which individuals are allowed to:

- Hold the authority to spend funds on the blockchain directly.

- Interact with smart contracts directly, allowing funds to be escrowed by smart contracts without giving up any authority over those funds.

To read this post in its entirety see link.

Do smart contracts become 3rd party custodians when they hold premiums?

{kind=link}

It depends. If everyone’s premiums are put into the same pool then smart contracts may allow other members of the group to become defacto 3rd party custodians. This is why TandaPay’s architecture specifically avoids this scenario.

The individual lock box analogy

Forget how insurance works normally, you send a payment to a provider and you have no idea what they do with it. The figure above is trying to create a clear set of rules for a step by step process that will determine ownership of a premium.

P2P insurance architecture has two options:

- Each premium goes into its own individual virtual lock box at the start of every month. - Authority to move the funds is with the individual policyholders.

- Premiums go into a shared pool of funds at the start of every month. - Authority to move the funds is determined by some form of governance.

In either case the funds are locked for one month and cannot move. After the month is over and the claimants have been whitelisted, then funds can move. Whoever has the authority to move funds is the defacto custodian of those funds. The smart contract in itself cannot move funds unless it receives instructions as to where those funds should go.

If the funds go into a pool and ownership of the funds is determined by:

- A vote, then the group is the custodian of those funds.

- An administrator, then the administrator is the custodian of those funds.

If the funds never go into a pool or are combined with other policyholders funds, there is no ambiguity. They belong to the policyholder until they are released by them for payment to a known claimant. Individual lock box architecture allows for custody to remain in the possession of the policyholder.

As a consequence, a policyholder must finalize their premium at the end of every month. They may also choose to defect with their monthly premium if they feel that a claim is fraudulent. The ramifications of permitting defections are discussed in great length in this post.

Why must all balances be reconciled to zero each month?

For some really technical reasons that you don’t want to trouble yourself with reading. If you are really interested you can read about it here (source of excerpt).

Why can’t we just use the banking system instead

The first decentralized insurance app which reaches a mainstream audience will undoubtedly be one which leverages the power of cryptocurrency to achieve regulatory arbitrage.

This is because there has never been, nor will there ever be, another payment technology in all of human history more uniquely suited to achieving regulatory arbitrage.

The reason why this is so is because of the special attributes the technology possesses. Cryptocurrency protocols enable the following unique features which no other payment system on earth can provide:

- Removal of third-party custodians. Blockchain escrows allow for the removal third-party custodians from holding funds that do not belong to them.

- Records that are transparent and fully auditable by anyone at any time.

- Funds that are transparent and fully auditable. This is because the funds themselves and the public record are one and the same thing.

- Auditing the rules that determine ownership of funds (smart contract code) is possible. This is because these rules operate within the same transparent public record which holds the funds.

- Protection from the misappropriation of funds. This requires that our insurance smart contracts which hold the funds are secure (caveat: the architecture must protect participants).

- Certainty about how specific aspects of the system will function. After auditing the smart contract code we can determine how specific aspects of the system will function in the future.

- Guarantees to those who want to participate in decentralized insurance.

As stated at the beginning of the article, the burdensome cost of regulation is the key factor that prevents small groups from providing coverage to each other. The crushing burden of regulation creates the insurance landscape that we see now. If you want to create new forms of insurance and enable more people to participate in the insurance process you have to leave the banking network entirely. This is because all current forms of regulation focus on third-party custodians of funds.

Use of the traditional banking network: * Prohibits direct ownership of funds. * Mandates a third-party custodial model which is subject to regulation.

Use of cryptocurrency networks: * Enables direct ownership of funds. * Removes third-party custodians and circumvents any regulations which apply to custodians holding funds.

If you can’t change the rules, change the game. These new insurance contracts don’t operate in an area where regulators have been granted permission to regulate, yet.

TandaPay Cannot Be Regulated

Direct payments are currently a protected first amendment right because:

- Court precedent establishes that financial regulation exists primarily to regulate custodians who hold funds and not the payments themselves.

- Payments of premiums and claims which pass directly between policyholders and claimants are not subject to regulation because there is no custodian to regulate.

- Direct payments of money between two parties for the purpose of building an ideologically motivated community is speech and cannot be regulated.

In a nutshell, that’s why peer-to-peer insurance needs to use the blockchain!