Fraud Protections within TandaPay

How TandaPay safeguards policyholders from fraud

Since new users don’t know or trust the developers, it is reasonable for users to be worried that the software might misappropriate funds. Blockchain technology provides specific guarantees about how the system will hold users money. This guarantee safeguards users from any potential fraud committed by the developers. More careful analysis is required to determine if the guarantee safeguards them from fraud committed by their own community of policyholders.

Trust in one’s community seems to be a foundational requirement for TandaPay to work. Although most issues within TandaPay are framed as disagreements, certainly more serious violations of trust do occur. It is not unreasonable for a policyholder to require protections from these types of risks. TandaPay’s architecture is required to provide the highest level of safeguards to policyholders to maintain a legal status. I have frequently framed the question of fairness in terms of, “how am I protected from an invalid claim being approved or a valid claim being denied?”

TandaPay’s protections are robust enough to help all types of groups. Whether you are in a group that is sympathetic to your viewpoint or one where there is conflict, TandaPay’s protections provide a way for every type of community to reach agreement.

Issues addressed by the architecture

This post covers two primary concerns people have:

- What if my group approves a fraudulent claim?

- What if my claim is unfairly denied?

The software only permits premiums to be used to either pay claims or pay refunds which are fairly shared by everyone. 100% of premiums are used for claims and refunds. If someone wanted to “steal” premiums from the group, the only way to do it would be to approve an invalid claim. So by addressing the above two issues, we are able to address every possible scenario where fraud and abuse could potentially occur.

In order to fully benefit from the protections provided by the software, policyholders are instructed to join groups where they know and trust a good number of the participants. At a minimum, all policyholders must join groups where the following requirements are true:

- They personally know and trust the secretary who coordinates the group.

- They personally know and trust 3 to 6 participants with whom they form a subgroup.

- They have read and understood the community’s charter: - They agree that the requirements for submitting a claim are fair. - They understand the procedure everyone must follow in order to submit a valid claim. - The charter clearly outlines reasons why a seemingly legitimate claim might not be eligible for payment (known edge cases).

Additionally, although not a requirement, it is recommended that more conservative participants should seek out groups with less than 50 people. They should consider the ideological composition of a group’s participants. The more closely associated a group’s members are ideologically, the more likely they are to quickly resolve disputes in ways that are mutually beneficial. The best way for groups to provide fair outcomes in the future is to start with the right initial composition. A strongly-linked community with a well-written charter is more likely to resolve disputes fairly than a loosely-knit community with a poorly-written charter. Finally, no TandaPay group should ever be allowed to exceed more than 110 people until further modifications are made to the protocol.

Protection from fraudulent or invalid claims

The first concern people have is that they will be forced to pay a claim that they believe is fraudulent or invalid. This never happens in TandaPay. Every participant is given the right to deny payment to any claim they believe is fraudulent or invalid. This action is called defection. To better understand how defections work, let’s consider the steps the group takes to pay a claim.

- Policyholders use the app to pay their premiums into a smart contract.

- The smart contract holds these funds until the end of the month.

- When a policyholder has a claim, the group uses the software to discuss if the claim should be approved for a payment.

- If a claim is approved by the secretary, then the smart contract is authorized to use the premiums to pay funds to the claimant.

- The smart contract allows people to make a choice at the end of the month: * Finalize their premium payment by sending it directly to the claimants * Defect with their premium payment and walk away from the Tanda * Do nothing, in which case their payment is still sent to the claimants

- After paying out all of the claims, any remaining premiums are repaid to policyholders as rebates.

- Defectors are barred from further participation and the process repeats.

Defections are the ultimate tool for keeping secretaries honest. They are a powerful check on any secretary who might act corruptly by approving an invalid claim. Any type of dishonest behavior will result in too many policyholders defecting. If more than 1/3 of policyholders defect, then the group will become unstable and in many cases will be unable to function. This would cause the group to terminate (discussed below).

To find out more about how defections work, you can read about them in this post.

Protection from valid claims being unfairly denied

Does the group have an incentive for denying payment to valid claims? It’s important to reduce this incentive as much as possible so that groups will do the right thing. To understand why Tandas are at low risk for this type of behavior, we first need to see how the insurance industry handles claims today.

The three key motivators which drive insurance companies to deny or underpay valid claims:

- Profit motive: A reduction of premiums used to pay claims allows providers to maximize profits for shareholders of the company.

- Avoiding insolvency: The denial of claims as a strategy for remaining solvent is such a well-known industry tactic that movies such as The Rainmaker have theatricized it.

- Maximizing the ability to pay future claims: Even the best insurance companies who don’t seek to maximize profits or deny claims to avoid bankruptcy still want to maximize their reserves. Insurance tries to manage risk associated with future unknowns. There is always a small chance that a large number of valid claims might appear within a short period of time. Someday this type of event will happen, and a large reserve pool will keep the company solvent when it does. For instance, auto insurers may worry that an outbreak of freak hail storms might cause claims to spike in the future.

These factors contribute to why insurers may underpay valid claims or use bureaucratic reasons to deny or delay payments.

This is how TandaPay’s architecture reduces these incentives to deny valid claims:

- Profit motive: The potential profit a group leader can gain by denying a valid claim is trivial compared to the downside risk of having their entire group terminate (discussed below). A group leader can never gain more than a fraction of their monthly premium when they deny a valid claim.

- Avoiding insolvency: TandaPay groups don’t hold reserves. They return to a zero balance at the end of each period. Because these groups operate on completely different principles, there is no incentive to unfairly deny valid claims. Unfairly denying valid claims can cause your group to disband.

- Maximizing the ability to pay future claims: Since the group does not hold reserves, it cannot maximize them to enable the community to pay future claims. There is no fear that a TandaPay group could potentially go bankrupt, which would drive the decisions that the group makes. The group has every incentive to approve all valid claims in the period that they are submitted.

Tandapay can still underpay claims if the total value of claims exceed the value of premiums that were paid in that month (see illustration). This encourages groups to pay monthly premiums that provide them with the best coverage. But the good news is that every claim in the same period will always be paid the same amount. This will guarantee that everyone is treated fairly. If it seems strange that every claim should have the same value, you might want to familiarize yourself with the architecture a bit more to better understand how claims work.

The following illustration makes this clear:

Inspired by a broken healthcare system

TandaPay’s approach was developed in response to a fundamental flaw in markets for healthcare insurance.

The most obvious flaw in healthcare insurance markets

Traditional insurance is flawed in that it uses one premium to both pay claims, and provide profit for the insurer. In healthcare this has led to a volume-based payment system. Such a system incentivizes insurers to focus on the total number of tests, operations, surgeries and treatments administered to patients. This focus on volume seems to confuse patient outcomes with the volume of services required to reach those outcomes.

If you are an insurer and you want to increase your profits what do you do? Insurers cannot make their slice of the pie bigger by increasing the share of a premium that is used for administrative costs. The Affordable Care Act places specific limits on what percentage of a premium becomes an insurer’s profits. Insurers can only make the entire pie bigger which gives all of the providers in the system (the insurer included) more pie. This requires an insurer to increase the total volume of services consumed by policyholders.

When the ACA fixed the percentage of a premium which could be used for administrative costs it didn’t lower the total cost of insurance. On the contrary it resulted in an increase in consumption of healthcare services. After the ACA passed the only way an insurer could increase their profit was if the total spent on healthcare increased.

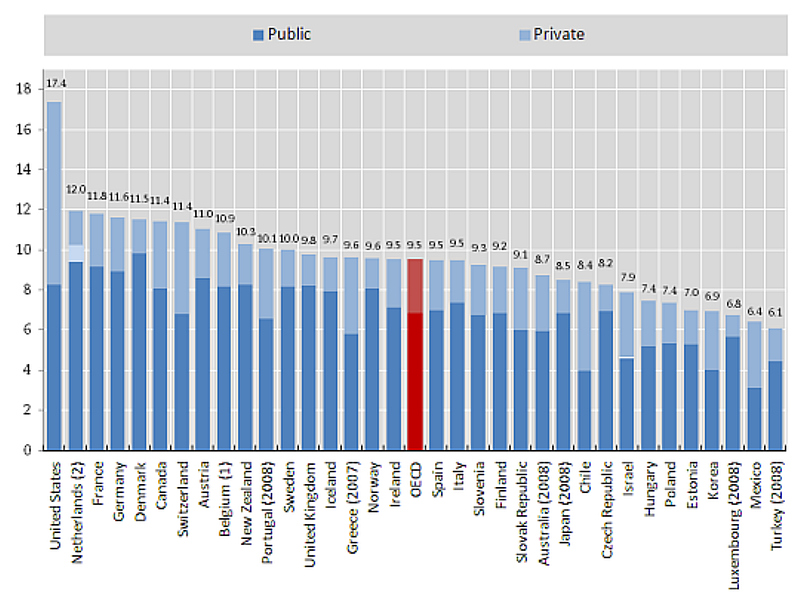

The chart below gives you a clear visualization of this effect and you can watch this video if you need further explanation. If you want to watch a great documentary on this subject I highly recommend Money and Medicine and the associated viewer’s guide.

The most obvious solution

It’s clear that we need to decouple premiums used to pay claims from administrative fees paid to providers. This change would require that 100% of every premium dollar must be used to pay claims and rebates to policyholders. It means that an insurer can’t make more profit simply by increasing the volume of services consumed.

What would happen if we built a system where 100% of the premiums were used to pay claims and rebates?

This was the starting point of all of my research into peer-to-peer insurance. What would happen if we built a system where 100% of the premiums were used to pay claims and rebates? Once I started down this path, however, the results led me in a totally unexpected direction. That direction not only eliminated the profit motive but also the sunk costs. This is how TandaPay was born.

Groups can terminate if things go south

A well-written charter should make it easy for any member of the group to determine if a claim is valid. If a policyholder cannot easily determine if a claim is valid, then they will be unable to decide if they should finalize payment to the claimant. If policyholders cannot participate in the claims approval process, they have no way to mitigate fraudulent claims.

The goal is that no group should be able to continue to operate after approving a fraudulent claim. Given this goal, allowing policyholders to defect effectively gives them the right to veto any invalid or fraudulent claim. To defect is to permit a policyholder to walk away with their premium for the purpose of denying payment to an invalid claim.

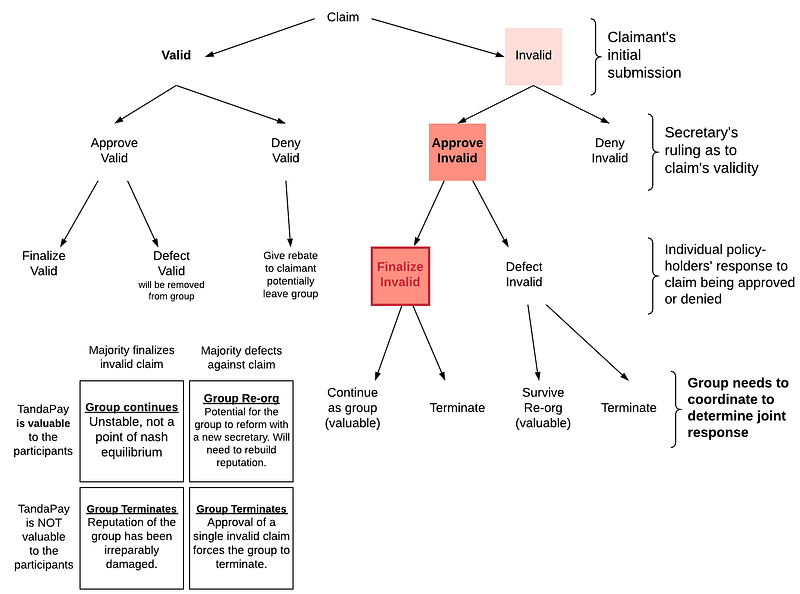

Furthermore, there are no sunk costs, which makes the decision to leave at any time easier for the participants. By removing sunk costs, there is no reason a policyholder should stick around if a valid claim has been denied. The easier it is for a group to disband (terminate), the more authorities will take actions that match the group’s standard for fairness. In this way, the secretary as a delegated authority is strongly incentivized to act honestly. This would mean that they should never approve invalid claims or deny valid ones. This dynamic is illustrated by the graphic below.

TandaPay has the strongest protections against fraud possible

TandaPay gives policyholders the power to defect and it removes the profit motive from the insurance model. This is the means by which TandaPay provides policyholders the strongest protections against fraud and abuse possible. It may not provide the best coverage possible, but it definitely provides the highest degree of protections against fraud.