When a $100,000 Salary Isn’t Enough

What Happens When 2/3 of Your Paycheck is Already Spent

Last updated: December 14, 2021

My wife and I make a little over six figures combined in gross household income, but our fixed expenses are eating up most of it.

That might look like the dream to some people.

Six figures? Hell yes! We’ll be living on Easy Street.

That’s what I would have thought 10 years ago when my wife and I were just dating. But life, it seems, is not without a sense of irony. (Hat tip to The Matrix.)

Fast forward to today, and the majority of our income is already spoken for every month. Let me walk you through the numbers.

FYI, the figures I’ll use in this article all reference our gross income. Why? Because that’s what everyone uses when talking about salaries.

Have you ever had a conversation about income and the other person says, “Well, you see after you take out the taxes and retirement and health insurance…”? No. It’s always, “I make $45,000 a year. How about you?”

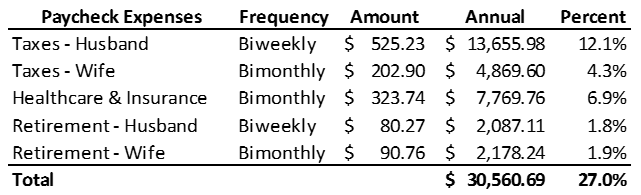

Paycheck Expenses

This first category contains all of the taxes, fees, and other expenses that get paid directly out of our paychecks. We don’t have a choice, but that’s a good thing.

Taxes

…but in this world nothing can be said to be certain, except death and taxes. Benjamin Franklin, 1789

Like running from Pepe Le Pew, there is no escape from taxes. We can maximize our use of tax-advantaged vehicles, but in the end, we must pay up.

But you know what? I pay for them happily.

I like roads to drive on. I like parks for my family to go to. And as a civil servant, I like my salary.

However, they are an expense, and a big one at that, so they can’t be ignored just because they’re mandatory.

Healthcare and Other Insurance

Understatement of the year: health insurance costs a lot.

Just the premiums alone cost a few thousand, and that’s cheap compared to the Affordable Care Act plans. Our medical premiums are currently $273 per month.

Full disclosure, I get a $65 “award” twice a month because I don’t take my employer’s insurance. I explain this in more detail in a previous article, but like everything, there’s a catch; it’s considered taxable income. And yes, I included this in my gross income calculation.

Health insurance premiums take a big chunk out of anyone’s paycheck, but they are not alone in this category. I have also included all the money we put towards our medical Flexible Spending Account (FSA) since we will use that money to pay for the deductible and out-of-pocket expenses required by our plan. We normally max this account, which was $2,650 in 2019, or $220.83 every month.

Other costs include the vision and dental premiums, along with life, accident, and dependent insurance premiums.

All told, the medical and insurance benefits cost us $647.58/month.

Retirement

Now, you might be wondering why we’re saving for retirement if this article is supposed to be about how little money I have.

Good point.

My response is two-fold.

First, both of our employers have mandatory minimums to contribute toward a retirement plan. My requirement is 3%, while my wife’s is 5%. That being said, my wife’s job contributes 10% of her annual salary on top of the mandatory 5%. Not too shabby.

Second, while you can see on the table that our current contribution level is not that much to retire on, it’s better than nothing. It disciplines us not to spend that money elsewhere, and we both have 25-ish years for it to grow.

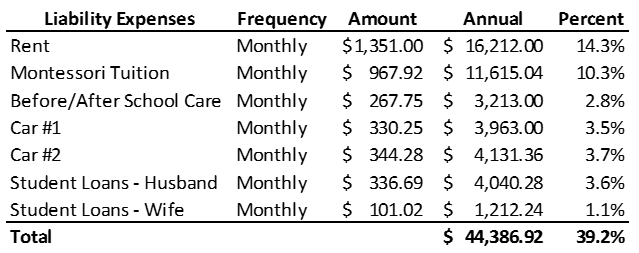

Liability Expenses

The next category is oftentimes referred to as “discretionary” spending. However, every payment listed below is going towards paying off a contract, or liability. Even our daughter’s tuition is a legally binding agreement to pay the total amount over 12 months.

Rent

Yes, we rent.

No, we won’t buy anytime soon.

And no, we aren’t going to change our minds.

There has been a vociferous debate about whether or not renting is the same as throwing away your money. While I disagree with that notion, I’ll let Ramit Sethi, Grant Cardone, Suze Orman, and even Dave Ramsey tell you why renting is better than buying for just about everyone.

Rent, plus pet fee, plus laundry machine rental (cheaper than a laundromat), plus carport rental (it snows a lot), plus water/sewer/trash fees = $1,351/month.

That might sound like a lot until you realize that we are only spending 14.3% of our gross income on renting when the rule of thumb is 30%. At that level, we would be spending $2,835 at our current income!

School

Let’s face it, the public education system in our country is a mess.

At no level — early childhood, K-12, higher ed — are we even in the top 10 internationally. And that should scare us. It is scary and it does not bode well for the future. — Arne Duncan, former Secretary of Education

While we know that the problem comes from both lack of political will and education funding based on property taxes, the system is not going to change during my daughter’s time in primary school. Because of that, we have decided to enroll her in a private Montessori school.

Does it suck having to pay almost $12,000/year intuition? Absolutely.

But you know what makes Montessori worth it? This story does.

I recently went into my daughter’s classroom to pick her up for a doctor’s appointment. When I entered, the children didn’t make a fuss, and half of them didn’t even look up. They were focused on their individual works, either at a desk or on the floor. The primary teacher was working with one child on a lesson plan for the week, and the teacher’s aide was assisting two students on a shared work. The environment was calm and peaceful, with the kids deeply understanding their lessons through activity rather than rote memorization.

That is the type of education that kids get at a Montessori school, which is so often lacking in packed classrooms led by underpaid and underappreciated public-school teachers.

Before/After Care

You may have heard that full-time childcare costs as much as college tuition. (Check out the Economic Policy Institute for a state-specific analysis.) What you may not know is that childcare before and after school can still cost a pretty penny.

Since both my wife and I are full-time professionals, we need our daughter to attend childcare for a little bit before and a little bit after school. Fortunately, there is just such a program at her school, but it still costs $267.75/month. Mind you, this is on top of her tuition.

So, for before/aftercare and tuition, we pay almost $15,000/year.

Let’s put that in perspective. We could put all that $15,000 into a 401k, have it start earning more money, and it would lower our tax bill by about $3,000.

Instead of investing in our retirement, we are investing in her education. All while paying taxes for schools we don’t use. Go figure.

Cars

We live in the non-Chicago part of the MidWest, so mass transit is sparse at best. Thus, two cars are kind of a necessity. (I’m sure the FIRE community will have a much different opinion on this, and I’m all ears.)

About three years ago, our trusty 2004 Honda Civic was totaled during a 500-year storm, when it was flooded with 3 feet of water.

Since we had used Dave Ramsey’s Total Money Makeover to pay off our credit cards several years back, we tried buying a car his way. Unfortunately, it completely backfired on us (forgive the pun).

Long story short, the 2006 Honda Accord we bought for $6,000 in cash after having it inspected by two reputable mechanics ended up having engine blow-by, requiring a $2,000 immediate repair, with several other repairs needed in the near-term.

Come to find out, used cars at the rock bottom prices that Ramsey espouses are a high stakes gamble; one that we lost.

After that debacle, we offloaded the Accord and instead, we chose to follow The Millionaire Next Door route and buy slightly used but still high-quality cars. They don’t have the new car premium, but they are still new enough that not much will go wrong with them.

We ultimately chose a Subaru due to their safety rating and all-wheel drive.

We currently have a 2014 Subaru Outback at $330/month and a 2017 Subaru Impreza Hatchback at $344/month.

That’s a little chunk of change just for cars, but they’re going to last until our 8-year old turns 18. And then, ta-da, our newly minted college freshman has a car!

Student Loans

I have written extensively about student loans (here, here, here, and here). I also believe that there is no student loan crisis, as student loans a) on average have a large positive ROI over a lifetime and b) can be forgiven through various methods.

Still, we have about $175,000 in student loans between the two of us, with total monthly payments of $437.71. That will soon be lower due to a new baby in 2020, but that’s for a later article.

Also, our student loan payments are less than 5% of our total gross income, so it’s not the huge burden that some borrowers have.

Discretionary Expenses

Finally, we arrive at the much-discussed discretionary category. This includes food, clothing, transportation, entertainment, travel, holiday and birthday gifts, etc. Oh, and electricity.

With only 33.8% of our budget left for all of this, we budget and track every dollar. We recently discovered You Need A Budget (YNAB) this year, and it’s been great.

2019 has been about categorizing and budgeting for every single expense we encounter throughout the year, from weekly grocery runs to annual car registration. 2020 will see a shift from merely tracking our spending in the past to assigning a job for every dollar in the future.

For more details, check out my ideas on how to attack your personal finances next year.

The Future

Overall, we’ve got a few years of being lean (e.g. no Disney World vacations), but then our debt starts falling off.

- The cars will be paid off in August 2023 and March 2024.

- My wife and I both have qualifying employment at an approved employer for Public Service Loan Forgiveness, so our balances will be erased after 120 payments. Mine are done in November 2025, with my wife’s in July 2026.

- Our 8-year-old will be done with primary and middle school in five years, so the private school tuition for her will stop in June 2025.

Sure, some expenses will go up, especially rent. But just remember, rent is a cap on how much we pay each month. The full PITI payment on a house is the floor.

On the other hand, as professionals, we haven’t even hit our prime earning years. We have annual raises to look forward to, all the while working towards the big income jumps due to promotions.

The long and the short of this is that a $100,000 income is not what it used to be. Overall, expenses today take a larger share of income than they did a couple of decades ago.

We’re not in the poor house, but we don’t have a golden ticket some might envision with an income over 100K.