How Much Income is “Enough”?

A simple guide to figure out your ideal salary.

Last updated: May 10, 2022

How much income is “enough”?

On the surface, it’s an easy answer.

Growing up, “enough” meant that you could

- Put food on the table.

- Provide a roof over your head.

- Sleep in a warm bed at night.

But dig a little deeper (or grow a little older), and you will quickly find that “enough” isn’t enough.

The next easy answer was that the mythical six-figure salary was “enough”.

Not true.

I want to highlight that, while my family is getting along pretty well, a six-figure income is not the magic bullet it once was.

I especially want to draw attention to the millions of families that are struggling with the same or higher family size, but earn much less.

If my family has financial issues, then other families are experiencing real hardship.

Which begs the question: How much income is “enough”?

The answers vary widely, and I will attempt to parse them out here.

(Note: The examples throughout this article will be for my family, which includes a married couple (both of whom are both fully employed), one grade school child, and one infant.)

Baseline Income

There are several measures of “basic” income bandied about when discussing household finances. Some of them are strictly defined (however poorly they are sourced), while some rely on emotion rather than dollars.

Let’s review the basics.

Federal Poverty Level

When Lyndon Johnson announced the “War on Poverty” during his 1964 State of the Union Address, he described several new policies to help those citizens in need of financial resources.

To determine who qualified for that assistance, the government needed a barometer to measure a family’s financial health.

Enter, the federal poverty guidelines, probably the most well-known measure of “adequate” income in the United States.

These guidelines are used to determine eligibility for government assistance programs, such as

- Supplemental Nutrition Assistance Program (SNAP, formerly known as “food stamps”)

- Temporary Aid for Needy Family (TANF, formerly known as “welfare”)

- Special Supplemental Nutrition Program for Women, Infants, and Children (WIC)

The official numbers were created by an employee as the Social Security Administration named Mollie Orshansky.

She did the best she could, which resulted in a number that was derived using a 1961 calculation based on a 1959 assumption that “…there is no generally accepted standard of adequacy for essentials of living except food,” that used 1955 data.

That’s all well and good for 1964.

But these numbers are horribly outdated. Fast forward 60 years, and we find that they are not a great, or even good, evaluation tool for 21st century families. (The West Wing has a great summary of the problems with the existing standard.)

Plus, there are no adjustments for location, outside of Hawaii and Alaska.

Now, don’t get me wrong…the poverty guidelines were fantastic when they first came out. And Mollie Orshansky’s work should be lauded.

But until these numbers are updated, the poverty guidelines just don’t provide an accurate reading of the minimum level of income to survive.

For example, for my family of 4, the poverty level is $26,200.

That number, along with the realization that these levels are used for determining assistance, tells us that we can definitely say that the poverty level is “not enough”.

So what’s next?

Living Wage

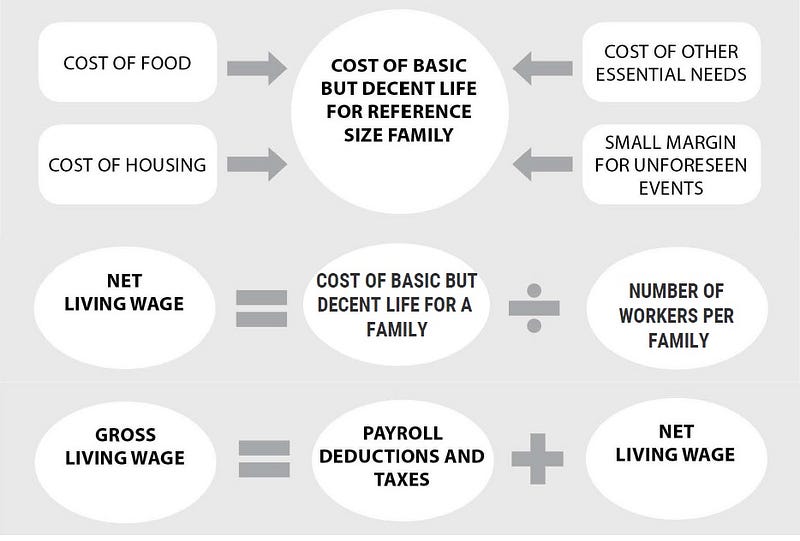

If “survival” is the word most associated with the poverty guidelines, then “decent” is the word attached to a living wage. By definition, a living wage is

The remuneration received for a standard workweek by a worker in a particular place sufficient to afford a decent standard of living for the worker and her or his family. Elements of a decent standard of living include food, water, housing, education, health care, transportation, clothing, and other essential needs including provision for unexpected events.

This begs the question, “What is a decent level?” Definitions vary but are all very basic.

- Decent housing has permanent walls, a non-leaking roof, electrical hookups, sanitary toilets, enough rooms for parents and children to sleep apart, and not located in a slum.

- Decent food is “a low cost nutritious diet that meets World Health Organization (WHO) recommendations on calories, macronutrients, and micronutrients.”

In short, a living wage includes the big three of household spending (housing, food, and transportation), along with a few other necessary items.

The image below sums it up quite nicely.

The MIT Living Wage calculator gives us a much better idea of how much income a family needs to provide the basics, with a little cushion.

The living wage model generates a cost of living estimate that exceeds the federal poverty thresholds. As calculated, the living wage estimate accounts for the basic needs of a family. The living wage model does not include funds that cover what many may consider as necessities enjoyed by many Americans.

The tool does not include funds for pre-prepared meals or those eaten in restaurants.

We do not add funds for entertainment, nor do we incorporate leisure time for unpaid vacations or holidays.

Lastly, the calculated living wage does not provide a financial means to enable savings and investment or for the purchase of capital assets (e.g., provisions for retirement or home purchases).

The living wage is the minimum income standard that, if met, draws a very fine line between the financial independence of the working poor and the need to seek out public assistance or suffer consistent and severe housing and food insecurity. In light of this fact, the living wage is perhaps better defined as a minimum subsistence wage for persons living in the United States. (Emphasis added)

(For the full list of assumptions, data sources, and calculations, check out their Technical Notes.)

“Minimum subsistence wage” doesn’t sound much like living. It’s not exactly the bare bones level that the povery guideline is, but it is far from ideal.

Also, by definition, there is nothing left over for investing in the future.

For example, this calculator has determined that for my family (two adults, 2 dependent children, both adults working), a living wage for my location comes out to $50,739, which is slightly less than double the federal poverty levels.

And I live in a relatively cheap area of the country.

Okay, so a living wage lets us “survive in comfort” (maybe), but that’s “not enough” to get ahead and plan for the future.

So what’s next?

Life Evaluation and Subjective Well-Being

Here’s where things get a little sticky.

Anything above a living wage allows you to allot your money towards “wants” rather than “needs”. (I’ll let you argue semantics over retirement funding being a “want” in the responses.)

So we move from a purely subsistence model to an emotional one.

The “Happiness” Maximum

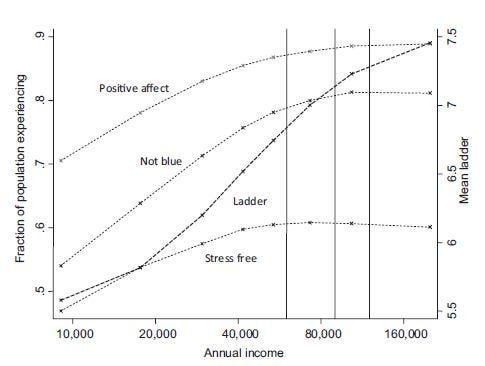

In 2012, Angus Deaton and Daniel Kahneman published a paper that stated emotional well-being (i.e. experienced happiness) did not increase after the $75,000 household income level.

As a result, this paper was widely referenced to advocate for both a ceiling and a floor at $75,000.

- Rich people should reduce their salary to this level.

- Poor people should receive assistance up to this level.

Okay, so $75,000 is “enough”, right?

Not quite.

Most everyone forgot about the second part of the study.

While day-to-day happiness stagnated, life-evaluation (i.e. overall life satisfaction) steadily increased with higher income, with no inflection point or leveling off.

In the words of the authors:

We conclude that high income buys life satisfaction but not happiness, and that low income is associated both with low life evaluation and low emotional well-being.

Okay, so $75,000 will give me all that I need and a little more, but it won’t give me all the life satisfaction that is available.

We can determine this level is also “not enough.”

So what’s next?

Basics, Plus Extras, Plus Savings

So what does it take to feel like you have enough? Industry researchers asked that very question in 2012, and the results are insightful.

The survey asked respondents to choose which of four categories best described them: I can’t even afford the basics; I can barely afford the basics and nothing else; I can afford the basics plus some extras; and I can afford the basics, the extras, and I’m able to save too. It is only at that $150,000 level that the survey found the vast majority of consumers, 88 percent, saying they could buy what they need, afford some extras, and still be able to save a bit.

Furthermore,

…nearly 30% of Americans in the $100–150K income bracket [claim] they can only afford the basics. Once considered affluent, six-figure income shoppers are now identifying themselves as middle-income.

Now we’re talking.

In 2020, my wife and I earn just over $110,000 combined, but we feel like we’re financially stagnant.

This may sound like a bit of financial truthiness, but it’s reality.

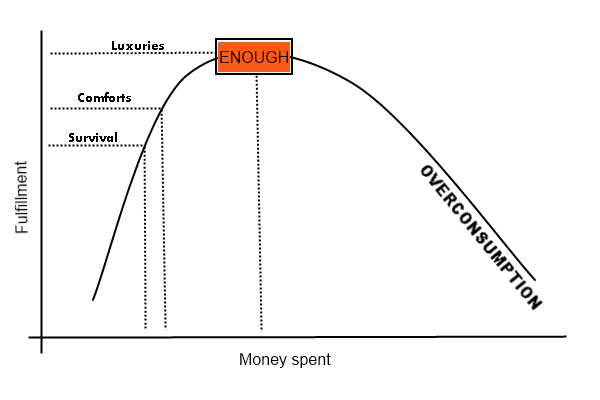

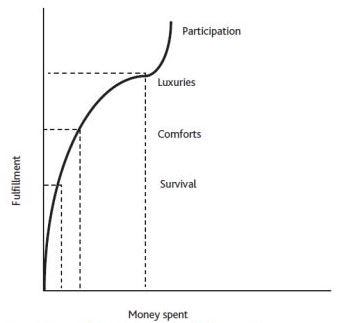

So what is the actual number to finally reach “enough”? This graph might shed some light.

If we assume that Money Earned is a proxy for Money Spent, it looks like we finally found our (undefined) inflection point of “enough” money.

From the discussions earlier in the article, I would define the points on this chart as follows:

- Below Survival = Federal Poverty Guidelines

- Survival = Living Wage

- Comforts = Happiness Maximum (~$75,000)

- Luxuries = Saving for the Future

Given these definitions, the Fulfillment Curve bolsters the argument that $150,000 of annual income is just about right to feel like “enough”.

And what does that 150k buy you?

It all depends, but it goes beyond financial goals and physical purchases.

Sure, we all want to fully fund our retirement accounts and eat wild caught salmon with organic brussel sprouts for dinner. But as you get closer to the peak of the curve, the luxuries progress from physical objects to mental states.

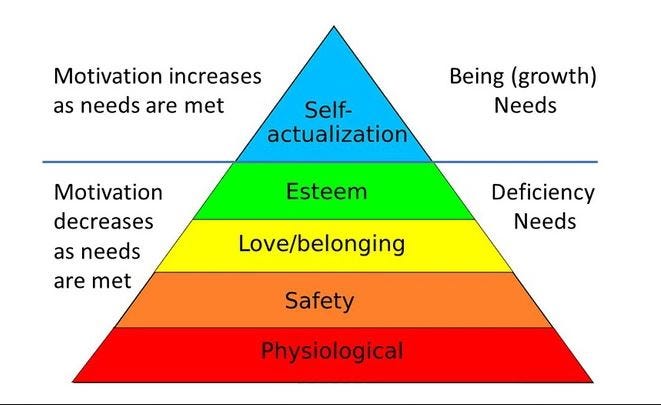

If the evolution of what your salary can buy seems familiar, that is because it has already been defined by Maslow’s Hierarchy of Needs.

Revisiting the definitions from above, we find that:

- Below Survival = Physiological Needs = Federal Poverty Guidelines

- Survival = Safety Needs = Living Wage

- Comforts = Love and Belonging = Happiness Maximum (~$75,000)

- Luxuries = Esteem = Saving for the Future

Beyond the Physical

“What about Self-Actualization?”, you might ask.

Well, that’s another instance of where the pattern breaks. Just take a look the two images below.

Somewhere along the line, there will be a point where you will no longer want for anything, much less need it.

At this point, money will determine who you are rather than what you have.

The Takeaway

In short, there is no magic number that will make everyone both financially well off and happy.

Even the Happiness Maximum of $75,000 is a national average, not accounting for family size, location, etc.

The good news? There is a magic number for you.

And that’s huge.

Just knowing how much you need to earn to truly meet your goals is a huge win for your financial future. After all,

Life can only be understood backwards; but it must be lived forwards.

- Soren Kierkegaard

How can we move forward if we don’t know where we are going?

To help determine your path forward, here is an exercise you can do at home.

Assume you just won the lottery, and the grand prize was $500,000,000 in after-tax, lump sum winnings.

Now, write down 100 things you would do with this money. There are no rules for this, just whatever you would spend your money on.

For most people, this assignment will follow a pattern.

- The first third of the list will be very easy to write down. These are the things you will want to buy.

- The next third will be more difficult to think of. This is where you move from buying things to doing things (i.e. experiences).

- The last third will be the hardest portion of all. This part of the list will show you who you want to be.

It may sounds hokey, but it will help determine your current goals and define what level of income you will need to get there.