How a Low Cost of Living and Freelancing Makes You ‘Rich’ on a Modest ‘Salary’

I overshare my personal financial situation in this article

I get off on oversharing in my writing.

At first, I thought this signaled something horribly wrong with me. However, on second and subsequent looks, it makes perfectly balanced sense.

There’s no doubt I get something out of being vulnerable. Being vulnerable doesn’t come naturally to most people, especially around the core issues where I overshare — money, love, and sex. Over the last couple years, I have succeeded in shedding the remnants of the unproductive masculinity I carried with me from childhood.

But, beyond and bigger than that, you accomplish very little if you write articles for the internet — especially articles about money, love, and sex for the internet — and you don’t overshare from a position of vulnerability. You do the reader little more than zero good. You do yourself — as a writer and human — zero good.

It’s in this spirit that I write this article, looking at my February/March anticipated cash flow with a focus on how I budget and ensure I’m making the most effective use of my monthly cash surplus.

You don’t have to earn a lot of money to feel like you have a lot of money. Of course, the vague statement “a lot of money” means different things to different people. It’s all relative.

I don’t think I make “a lot of money.” However, I also live in Southern California, where I see true affluence alongside more than a few people living beyond their means. If I still lived in my hometown — Buffalo — I’d probably consider myself objectively rich.

So it’s pointless to even think about this in the first place. You make what you make. Maybe it ebbs and flows. You just need to conceptualize and execute on whatever cash flow you bring through the door each month.

It comes to down to three critical factors:

- Having a thoughtful, replicable strategy.

- Having a low cost of living.

- Having a clear vision of what you want (and a partner who shares this vision).

I’m all-in as a freelancer. While I have freelanced for roughly 12 years, I have only been all-in once before. In part because the investing sites I freelanced for asked me to come on full-time. In part because I (once) liked the perceived comfort of a “regular” paycheck.

I always knew there were constraints associated with a fixed salary. I recently wrote about this for The Post-Grad Survival Guide:

Had I kept one job forever, I would have chosen stability over creativity. I could not have succeeded as the person who works the same job all day, every day and, then, if I’m not too sleepy, works on my passions at night. I work my passion all day, every day. And I can do this because I traded stability and security for the excitement and growth only living different lives within one lifetime can bring.

…I would have capped my earnings potential by staying in one career for too long. I would not have been able to jump into the flexible world of freelance writing, where limits on how much you can make exist in ways decidedly different from traditional employment.

Unless you make a shit ton of money, these “limits” hold you back financially. Because you know — usually to the penny — how much you make every two weeks, you budget to fit inside this number. While a perfectly sane and logical approach, I found that it made it more difficult to achieve an insanely low cost of living.

When you freelance, there’s more inherent uncertainty. So you tend to pay closer attention to things such as keeping an ample cash cushion and directing your money to various pots of money each month.

For insight into how I do this, see this Making of a Millionaire article:

In the present article, we focus on how as freelance income flows, you can earmark it throughout the month and anticipate how you allocate your surplus cash.

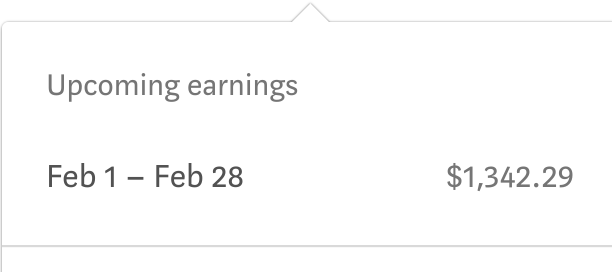

First things first:

As of February 14, 2021, that’s where I am for February on Medium. That number — $1342.29 — is 18 cents more than my rent payment.

So, rent’s paid. Feels good.

If the monthly trend holds, I’ll beat (maybe blow away) last month’s number on Medium, which will put me over $3,000 in Medium income (my months tend to gain momentum as the days get longer — or shorter). Since I started on Medium, I have increased my income every month, month over month.

If I stop here, I pay my bills with money left over.

Except I have several other freelance gigs at the moment. I won’t identify them because I don’t think the clients would appreciate it. However, it shakes out roughly like this:

- Freelance client #1: February: $600 / March: $900

- Freelance client #2: February: $532 / March: ~$500

- Freelance client #3: February: $1,000 / March: ???

For February, that’s $2,132 on top of what I’m near certain I’ll make on Medium. So we’ll total February’s cash flow to $5,132 (and hopefully more). However, this is a nice number to work with.

Of course, I keep a modest cash cushion in my checking account, an emergency fund, a travel fund, savings and investing funds for my daughter, and my own investment account(s).

As indicated, my rent’s paid. After I account for the remainder of my fixed monthly expenses (including groceries and automatic transfers to several savings accounts — funds), I’m out approximately $2,500 for February. This leaves me with $2,632 leftover.

In recent months, I went hard buying stocks. I plan to slow that pace over the next several weeks. I’ll direct surplus elsewhere. It’ll look a little something like this:

- Taxes: $300

- Travel fund: $1,000 (A small trip is on the horizon)

- Emergency fund: $1,000 (I drew from it to buy stocks, anticipating my ability to replenish it over the next few months)

- Investing: $332

If you’re paying close attention, you might ask, what about discretionary spending, such as eating out (take out these days), drinking, and whatever else?

I satisfy discretionary spending in two ways.

One, the my checking account didn’t feel a thing method:

When you spend money, does your checking account even notice?

I do this with small, mostly everyday purchases such as coffee. My checking account has no clue. It’s like I was sleeping beside it and, as I slowly slid my arm out from underneath its body, it’s breathing never changed. So I comfortably “throw money away” each day at local coffee shops.

I do this with bigger, less frequent purchases. Like the other day, I decided I needed new sneakers. Partially guapa-inspired, I bought a $130 pair of shoes.

Do I need them? Yes and no. Do I want them? Absolutely. Will I get something out of the purchase? Pretty sure I will. Did my checking account flinch? Nope.

This is one reason why I keep the modest cash cushion in my checking account. To satisfy discretionary spending and pay my rent on time (because Medium tends to pay around the 5th of the month).

Two, a good bit of March’s income will come early in the month, effectively replenishing my checking account cash cushion. I also anticipate — with near certainty — renewing my contract with freelance client #1 (for anywhere between $600 and $1,200).

With close to near certainty on freelance client #2 and the realistic possibility of an increase in income.

And possibly with freelance client #3 for how much, I don’t know.

I also have freelance client #4, who I didn’t do anything with this month. However, as it stands today, I can turn that income stream on and off. I can reasonably expect to generate somewhere between a few hundred dollars to roughly $1,500, depending on how much time I devote to it. I keep it in my back pocket.

And there’s freelance client #5, who I actually earned $180 with in February, but I forgot when I was outlining this article and didn’t want to go back and add it in! I’ll split that money between my travel fund and daughter’s core savings account. This client will likely call this month or next with more work.

All of this to say, I don’t make a lot of money. There’s no way I could afford a house in Los Angeles. I don’t want one anyway! Even if I reach my freelance earning goals — which would add a considerable bit of monthly surplus — I won’t buy a house.

This brings us to the last — and maybe most important — point.

Having a clear vision of what you want and surrounding yourself with people — most importantly, a partner — who has a clear vision of what they want that pretty much aligns with your outlook.

I keep a super low cost of living. Generally, $2,500 a month. This can increase on the basis of temporary or longer-duration circumstances. It can also decrease. For example, I bought a car nearly three years ago. Soon, I hope to eliminate the bulk of that expense and drive my Hyundai into the ground.

I intend to not drive my car nearly as much as I do now come the second half of 2021. It’s unlikely to see 100,000 miles anytime soon, if ever (it’s at about 36,000 miles now, I think).

I feel creepy bringing this up, though my girlfriend (“guapa”) and I openly discuss it. There’s a chance we’ll end up living together. If we do, we’ll both have sub-$1,000 rent. In Los Angeles, this is the stuff dreams are made of.

Creepy or not, it’s a possibility that must enter this equation, even if only for the sake of the current illustration.

Guapa and I can do whatever we want. And we really mean it.

We’ll both be in a position soon to pretty much pick up and go whenever we like.

It might be a relatively quick road trip to start. Then a visit to my hometown and a handful of surrounding places. Shortly thereafter, we plan on going big. We’re toying with the idea of Seoul, South Korea.

All of this, assuming the pandemic cooperates.

In a nutshell, we see absolutely eye-to-eye (which is amazing for a girl who only stands “collarbone high” — thanks Rhett Miller and Old 97’s for the wordsmithing). We’re on the same page in terms of maintaining cheap rent (however that looks) and using our resources to travel.

As I have riffed recently, we communicate so well on everything that we don’t necessarily require the intense money talk. It’s a pretty incredible feeling.

Without going all-in on freelance work (or making an out-sized amount of money in a super flexible, salaried job), there’s no way I could execute the way I’m am right now. For me, it just wouldn’t be possible — for two reasons:

- Again, I’d budget traditionally and end up backing my expenses right into my fixed monthly income. The way you pull a car into a garage and inch up to the wall to the point just ahead of hitting it.

- There’d be limits on my earning potential. While a whole host of things can go wrong when you write as a freelancer, I have a reasonably clear idea of where they’re headed. If the plan doesn’t work out as I anticipate, have options — a plan B or two.

As with every word I sling about money, I hope this helps.

I truly get off on relaying conceptual and concrete details of my personal experience. The writers I enjoy most do likewise. They’re a daily inspiration. I fully realize that we live in different worlds quite possibly and, most definitely, have different situations. Therefore, the goal — you take what you can carry and adapt to your situation and leave the rest (thanks, Bruce Springsteen, for the words there!)

This article is for informational and entertainment purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.