Timeseries Methods: Kalman Filter from Scratch Part 4

Introduction

So far, we focused on linear transition and observation matrix. However, there are times when we are likely to believe that nonlinear models will better describe the system. Given Kalman Filter is the best linear filter an option is for us to linearize the nonlinearity.

Background

We can linearize nonlinear function using First-Order Taylor Approximate. Details can be found here. We are stating that for a nonlinear and differentiable function f

Thus, for the nonlinear transition model F and nonlinear observation model H at each step of update we will compute the partial derivative of each state variable evaluated at the prior estimate. Everything else remain the same as the linear counterpart, except the F and H at each update step is no longer constant. They become time dependent.

Code

From the original class we kalman_filter class we created in here, we just need to update the input such that F and H are no longer constant, but functions return a constant given input. Note that given B and u are arbitrary predetermined control vector whether or not they are linear is not of concern here.

Below is the updated class. Please note the structure did not change. The L and M deals with non-additive noise component. it will be ignored in the case of additive noise components. Alternatively, you can use the override methods from FilterPy package’s ExtendedKalmanFilter. Since it only allows for nonlinear in the transition matrix.

class extend_kalman_filter:

def __init__(self, x_init, transition_model, observation_model, F_partial, Q, R, H_partial,

L_partial, M_partial

, B=None, u=None, sd=np.array([[0]])):

self.x_init = x_init

self.F = F_partial

self.Q = Q

self.R = R

self.H = H_partial

self.L = L_partial

self.M = M_partial

self.transition_model = transition_model

self.observation_model = observation_model

self.X_post = self.x_init

self.P_post = sd

self.X_prior = None

self.P_prior = None

if B is not None and u is not None:

self.B = B

self.u = u

else:

self.B = np.array([[0]])

self.u = np.array([[0]])

self.mean = np.zeros_like(self.x_init)

self.covar = np.zeros((sd.shape[0], sd.shape[1]))

def fit(self, data, num_state=1, fit_step=None):

self.num_state = num_state

fit_step = fit_step if fit_step is not None and fit_step < data.shape[1] else data.shape[1]

for i in range(fit_step):

z_k = data[:, i]

# predict

self._predict(self.X_post, self.P_post)

self._update(z_k)

# update

self.mean = np.append(self.mean, self.X_post, axis=1)

self.covar = np.append(self.covar, self.P_post, axis=0)

def _predict(self, X_post, P_post):

self.F_current = self.F(X_post)

self.L_current = self.L(X_post)

self.X_prior = self.transition_model(X_post, self.B, self.u)

self.X_prior = self.X_prior.reshape(X_post.shape)

self.P_prior = np.dot(np.dot(self.F_current, P_post), self.F_current.T) + \

np.dot(np.dot(self.L_current,self.Q),self.L_current.T)

def _update(self, observation):

self.H_current = self.H(self.X_prior)

self.M_current = self.M(self.X_prior)

resid = observation - self.observation_model(self.X_prior)

S_k = np.dot(np.dot(self.H_current, self.P_prior), self.H_current.T) + \

np.dot(np.dot(self.M_current,self.R),self.M_current)

K_k = np.dot(np.dot(self.P_prior, self.H_current.T), np.linalg.inv(S_k))

self.X_post = self.X_prior + np.dot(K_k, resid).reshape(self.X_prior.shape)

self.P_post = np.dot(np.eye(self.num_state) - np.dot(K_k, self.H_current), self.P_prior)

def new_observation(self, observation):

num_new_obs = observation.shape(self.num_state)

for i in range(num_new_obs):

obs = observation[:,i]

self._predict(self.X_post, self.P_post)

self._update(self, obs)

def predict(self, n_step=1, B_new=None, u_new = None):

## assume no control

pred_array = np.zeros((self.H_current.shape[0], n_step))

X_cur = self.X_post

for i in range(n_step):

X_new = self.transition_model(X_cur)

Y_new = self.observation_model(X_new)

pred_array[:,i] = Y_new

X_cur = X_new

return pred_arrayApplication

Let us assume that the model is defined as below

In code it looks like this

x_init = np.ones((4, 1))

def x_new(inputs, *args):

return_mat = np.zeros_like(inputs)

return_mat[0] = inputs[0]

return_mat[1] = -inputs[1]*np.cos(inputs[2]) - inputs[3] * np.sin(inputs[2])

return_mat[2] = inputs[2]

return_mat[3] = inputs[3]

return return_mat

def y_new(inputs):

return inputs[0] + inputs[1]*inputs[0]

def F_partial(inputs):

return_mat = np.eye(inputs.shape[0])

return_mat[1,1:] = [-np.cos(inputs[2]), inputs[1]*np.sin(inputs[2])-inputs[3]*np.cos(inputs[2]),

-np.sin(inputs[2])]

return return_mat

def H_partial(inputs):

return np.array([inputs[1,0],inputs[0,0],0,0]).reshape(1,4)

def L_partial(inputs):

return np.eye(inputs.shape[0])

def M_partial(inputs):

return 1

Q = np.eye(4)

R = 1

kf = extend_kalman_filter(x_init, x_new, y_new, F_partial, Q, R, H_partial,

L_partial, M_partial

, B=None, u=None, sd=Q)

n_train = int(len(data) * 0.9)

n_test = len(data) - n_train

kf.fit(observation[:,:n_train], 4, n_train)

fittedvalues = kf.get_observation()

pred_ = kf.predict(n_test)To make it a fair comparison with the linear version, a linear version with exactly 3 states is chosen (as opposed to the 6 states from the previous two posts are multistate and multidimensional)

Results

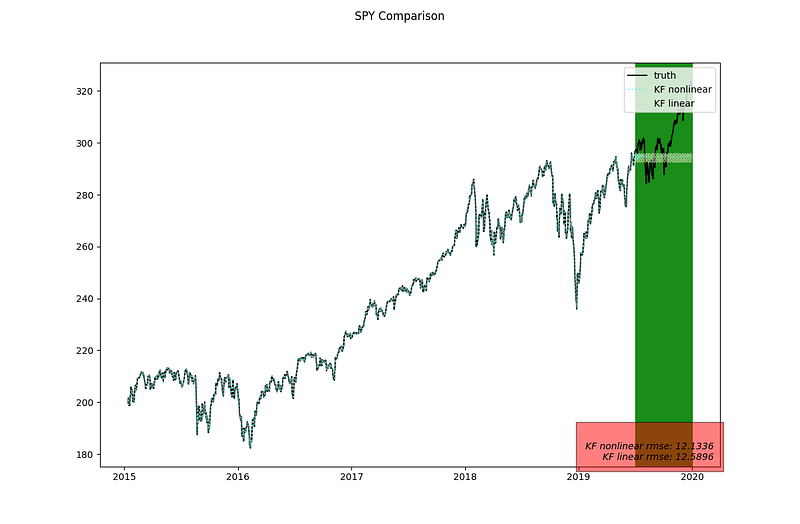

This is the complete plot over the training and testing periods.

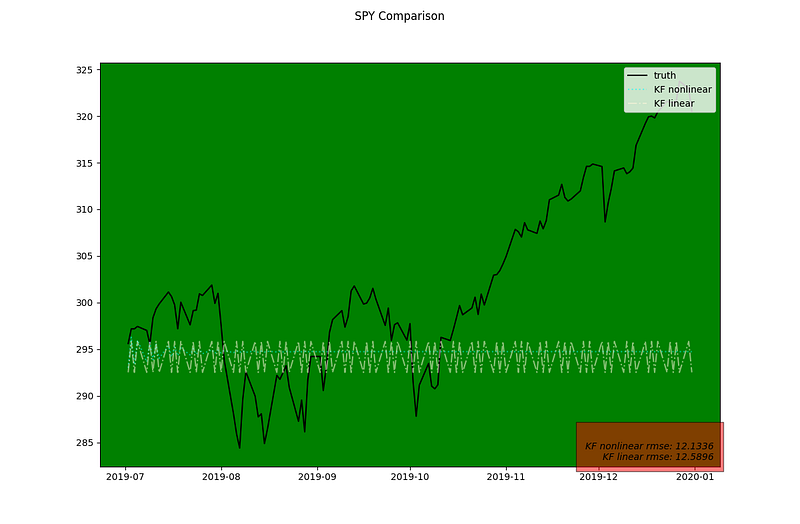

This is the result for just the testing period

What we can notice that in the first few time-step post training it has more of a variance period to period and then flattens out to an average for time periods further out.

There is an alternative option to deal with nonlinear setup, it is the unscented kalman filter. We will explore this in future post.

Thank you for reading. Please follow and subscribe if you are interested in more posts on time series analysis.