Timeseries Methods: Kalman Filter from scratch in Python — Part 1

These posts will be focused on application of various method in analyzing timeseries dataset (stock market dataset).

This first post is about Kalman Filter. History and details can be found in the wiki. There will be several posts on Kalman Filter, starting with the basic linear Kalman Filter with 1D dataset to multidimension dataset in nonlinear space.

Using the equation from the wiki we could easily create a function in python using numpy.

def kalman_filter(x_init, F, Q, R, H, data, B=None, u=None, sd=0, num_state=1):

X_post = x_init

P_post = np.eye(num_state) * sd

num_steps = data.shape[1]

mean = []

covar = []

if B is None:

B = np.array([[0]])

u = np.array([[0]])

for i in range(num_steps):

print(i)

z_k = data[:,i]

#predict

X_prior = np.dot(F, X_post) + np.dot(B, u)

P_prior = np.dot(np.dot(F, P_post) , F.T) + Q

#update

resid = z_k - np.dot(H ,X_prior)

S_k = np.dot(np.dot(H, P_prior), H.T) + R

K_k = np.dot(np.dot(P_prior,H.T), np.linalg.inv(S_k))

X_post = X_prior + np.dot(K_k , resid)

P_post = np.dot(np.eye(num_state) - np.dot(K_k , H), P_prior)

mean.append(X_post)

covar.append(P_prior)

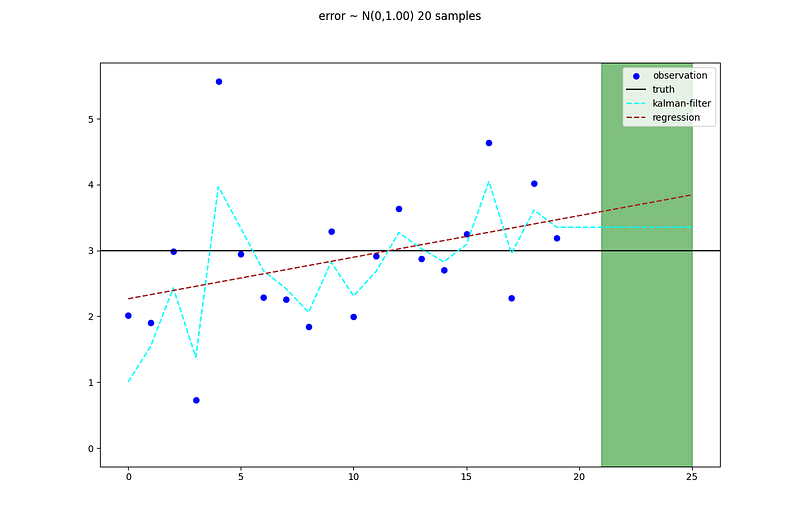

return mean, covarTo validate the result let’s assume that the true model is in the form of y = 3 with random white noise. initializing conditions are as follow:

x_init = np.array([[0]])

F = np.array([[1]])# state transition matrix

B = np.array([[0]]) # control input

u = np.array([[0]]) # control vector

Q = 1 # model noise

H = np.array([[1]]) # observation model

R = 1 # observation noise

truth = 3

observation = truth + np.random.normal(0, 1, size=20)

mean, std = kalman_filter(x_init, F, Q, R, H, data, B,u,0,1)we can see from the plot how kalman filter compares to a simple linear regression model.

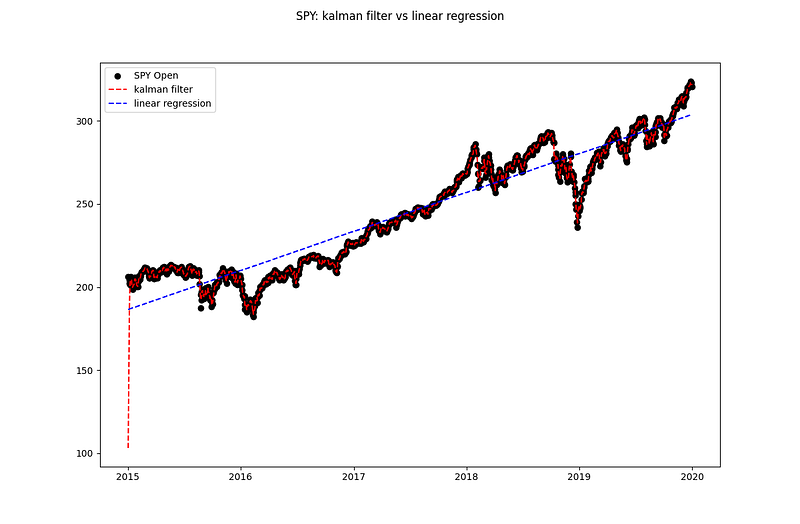

Applying to SPY dataset between 2015 to 2020. We can see how quickly the Kalman Filter is able to follow the trend even with a bad initial guess of 0

It is important to note, in-sample performance is not indicative for out of sample predictive power. Specifically for Kalman Filter, the prediction will be a constant for future period, when we know clearly there are trend and seasonality. We will adjust for these factors in future posts.