The Fatal Mistake That Stops Most People From Getting Ahead

Your city doesn’t have a cost of living, you have a cost of living

I write many of my articles from the nation’s 5th most expensive zip code, 90402 in Santa Monica, California. As of September, the median price of a home here is $3.62 million. I used to live on the other side of the tracks — 90403. The average rent in this neighborhood for a one-bedroom apartment is $2,598.

A street called Montana Avenue divides these two zip codes. 90402 sits North of Montana. 90403 south. By and large, 90402 contains single-family homes, while apartment buildings of various sizes dominate 90403. I love it in Santa Monica. I still spend a lot of time there. However, I no longer live there. It doesn’t make financial sense of me to pay the average for a studio in 90403 — $1,897.

Could I afford $1,897 a month for an apartment? Yes. Why do I choose to pay $1,350 a month in not-nearly-as-tony East Hollywood? Because I can do other things with the $550 I save each month. And I’m still not happy with my cost of living. So I’m taking steps to reduce it even more.

Because it’s my cost of living. It’s not my city’s cost of living. I own it. I’m responsible for it. I can make it work — within my desired budget — no matter where I live.

If I really wanted to be in Santa Monica, I’d find a two-bedroom apartment, get a roommate, and pay what I pay now. Remember, these are average prices and we’re in a renter’s market. On the ground, I can tell you that you can get a nice two-bedroom in Santa Monica for between $2,600 and $2,800 these days. But I don’t want a roommate. I don’t think that would work out well.

So I made the decision to make it work how I want it to work in Los Angeles by living in a less expensive neighborhood. Because I’d like to upgrade my apartment without paying more, I plan on eventually moving to Portland. I can live in the Portland neighborhood that’s the equivalent of 90403/90402 in Santa Monica for what I pay now. It’s not complicated at all.

You Won’t Get Rich Making Excuses

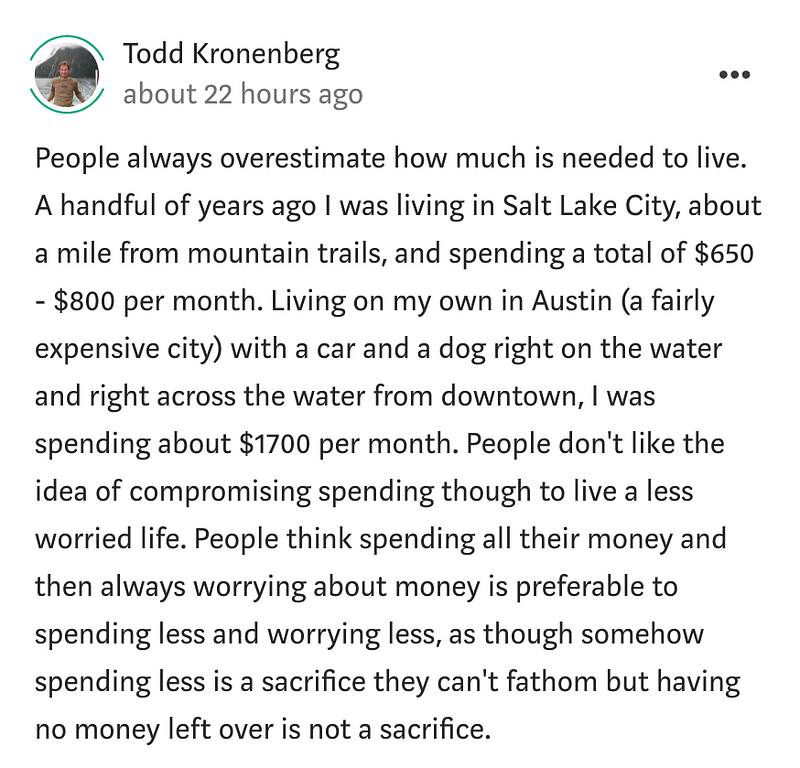

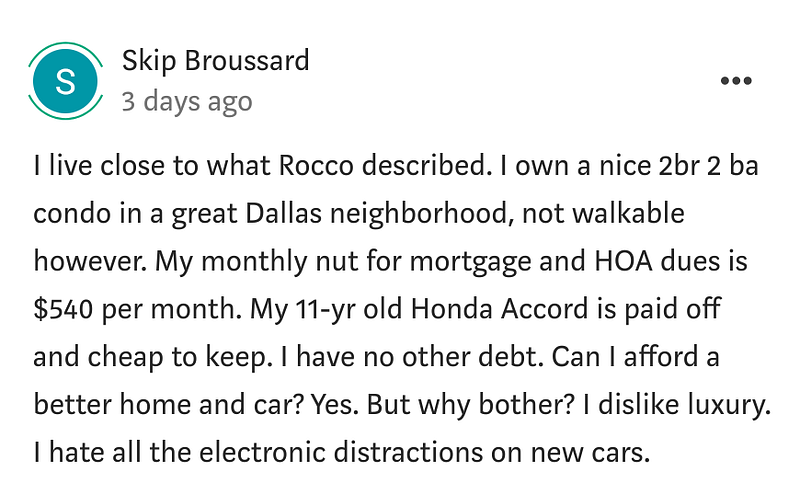

As I write about the cost of living on Medium and Seeking Alpha — and detail how my monthly expenses only come to roughly $2,500 — I’m encouraged and inspired by the incredible feedback. People telling amazing stories as they relay their experiences with cost of living and attendant frugality.

Here are two excellent examples from my most popular Medium article yet, You Can Have an Insanely Low Cost of Living (and a Great Life):

Boom. And boom.

However, detractors exist. A paraphrased sampling.

There’s no way you can do that in LA County. You must live like a homeless person.

That’s offensive. And also untrue.

Sure, you’re single, but you can’t do that with family.

Also, untrue.

I won’t overcome those obstacles here. I already have in the “insanely” article. But I will say it’s easier to make excuses than difficult decisions and compromises. Any of us who achieve an insanely low cost of living — and work to make it even lower — understand you must make compromises. Not sacrifices. Compromises.

Compromise isn’t a bad word. It’ll make you wealthy ahead of schedule.

If you have never lived in a big city, I can see why it might be hard to believe. But you absolutely do not have to pay the published cost of living. It’s no different than looking to buy a house in a blue-chip suburb. You can make compromises to come in below whatever the median price is. Maybe you compromise on square footage, lot size, or neighborhood. In some cases, you might have to “settle” for a condo.

As always, it comes down to what’s more important to you — having a low cost of living or maintaining the going lifestyle.

Your Spending Doesn’t Have to Go Up

There’s another misnomer I see on full display when I sit outside in my camping chair, working on the border of 90402 and 90403. The notion that the lavishness of your lifestyle should have a positive correlation with how much money you make.

Every car in Santa Monica is an Audi, Mercedes, BMW, or Tesla. Can the people driving these cars afford them? Probably. Just like I can afford to pay more for rent. Do they need these cars? Probably not. Just like I don’t need to rent a more expensive apartment. I can wait for the ideal situation.

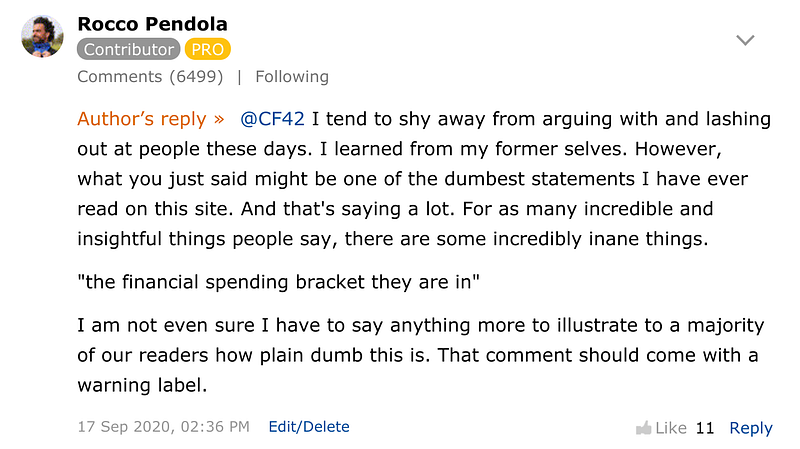

This is just an illustration of the choices people make. The folks with these cars choose to use their money to obtain and maintain them. Money that could go elsewhere. It’s a personal choice. It’s a perfectly fine choice to make. If everyone was as frugal as me, our economy would tank. But as much as it’s an individual choice, it’s heavily influenced by the process of socialization. Here’s what a reader said in response to my $2,500 cost of living:

Great question, and why would we expect someone to have a grip on the financial markets if truly this is the financial spending bracket they are in?

Here’s what I said in response:

I don’t like to “rip” people anymore. I used to do it for a living. However, occasionally, you gotta do it. The comment that because I write about “the financial markets” I should have a higher cost of living absolutely requires a warning label. But it’s not too far off from the way most people think. Look around at how many people live beyond their means and use credit to buy things they can’t afford to pay for with cash. I’ve been there before.

I used to subscribe to the empty dream that as I made more money, I could have more things. As in that’s the reason why I needed to make more money. To elevate my status materially. What else are you supposed to with financial success? With this mindset, you dangerously increase your lifestyle risk. One global pandemic and you could find yourself in serious financial trouble.

It’s the fatal mistake that keeps people from getting ahead financially and building wealth. They pace expenses with income. As income increases, they take on a higher cost of living. This is a risky game to play.

The way to secure your present and future is to determine, control, and own your cost of living by making compromises, not sacrifices. And to use your cash flow to become cash secure, not to fall victim to lifestyle inflation.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.