Securitisation: An Introduction to Collateralised Loan Obligations (CLOs)

Background

A CLO is a securitised product that gives investors exposure to a diversified pool of senior secured corporate loans. As with most securitised products, as we have previously seen, CLOs allow investors to vary their risk-return profiles depending on the tranche they would like to get exposure on.

A single CLO can be thought of two different products, depending on whether you are looking at the debt or equity tranche. Note, however, that there are multiple debt tranches (different ratings) but only one equity tranche.

CLOs are characterised as an alternative investment and have low correlations with investment-grade corporate bonds and equities, making them attractive to include in one’s portfolios. They are, however, correlated to the economic cycles as they are backed by floating (variable) rate corporate loans.

CLOs: The Basics

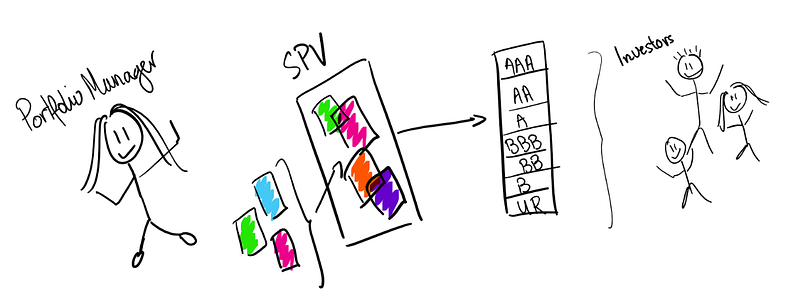

To start with, a special purpose vehicle (SPV) is established, and a portfolio manager is tasked with identifying the underlying loans to make up the securitisation process. The funds for the initial purchases usually come from the issuance of rated term debt and equity tranches.

The portfolio manager will actively manage the underlying loans that make up the CLO throughout the life of the investment. Any principal or interests payments (from underlying loan payments), will be paid out in a waterfall fashion as we have previously seen in this series.

The rated debt tranches will have fixed excess returns (i.e. LIBOR + X, where X will be a pre-agreed rate) and make up the majority (~90%) of the capital structure; leaving the equity portion of the CLO with variable returns. As expected, the rated debt tranches have lower returns but lower principal losses too.

CLOs: The Mechanics

Following from what we have learnt above, the burning question remains; how do CLOs allow investors to make money? What are the underlying mechanics of this complex product?

On the face of it, you can think of a CLO as two different products. You have the debt rated tranches that offer pre-agreed returns which, according to the FT, have never up until this point have ever defaulted.

On the other hand, you have the unrated equity tranches; riskier but with potentially much more significant, variable, returns. The returns for the equity tranches are generated through the arbitrage opportunity between the underlying variable loan returns and the pre-agreed debt tranches returns. Take for example that the debt rated tranches of the CLO have an average cost of LIBOR + 150 bps; while the underlying corporate loans return an average of LIBOR + 200 bps, leaving 50 bps on the table. Take away the management and facilitation fees, and whatever you’re left with is the investors’ payout. Fifty bps may not sound a lot, but you need to remember that the equity tranches are highly leveraged; although they are only ~10% of the whole capital structure of the CLO, the returns will be higher than 10% of the total CLO returns.

Risk Profile

When a portfolio manager considers taking a position in a CLO investment instrument, she will need to carry out extensive research to understand all the inherited risks of the investment.

Credit Risk

The underlying loans will all have credit risk; that is the exposure to whoever took out the loan. Depending on the counterparties’ credit quality, the next economic downturn may have a significant impact on the returns of the CLO, with potential defaults.

Market Risk

All the underlying loans that make up this securitised product have exposure to a variable floating index (most likely LIBOR). As such, the returns expected for CLOs are dependant upon the rate at which LIBOR is at.

Management Capability

CLOs are actively managed instruments with the underlying pool of loans changing depending on pre-payments of loans etc. The portfolio manager’s skills will have an impact on the final returns of a CLO.

If you liked this article, you might also like: