Flash Introduction to LIBOR

Get the basics of LIBOR in under 3 minutes

Background

As we saw in ‘Flash Introduction to the Money Market’, the interbank lending market refers to the market of short term borrowing and lending between banks. The rate at which banks lend unsecured funds between them, is known as LIBOR.

What is LIBOR?

LIBOR stands for London Interbank Offered Rate and it is a range of short term rate indices that reflects the average rate at which banks (in London) can borrow unsecured funds in the interbank lending market.

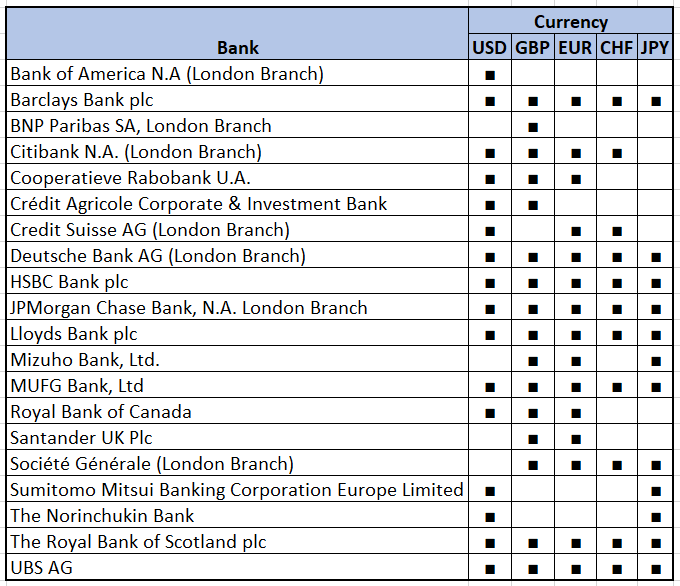

As you would expect, depending on the currency and length of the loan, there are different LIBOR rates quoted. LIBOR Rates are calculated and quoted daily based on London’s business days and are quoted for 5 currencies and 7 maturities for a total of 35 quoted rates. There is an Overnight/Spot LIBOR rate, 1 week, 1 month (M), 2M, 3M, 6M, 12M for GBP, USD, EUR, CHF and JPY.

LIBOR is also used as a quick way to gauge the health of the financial system and an indicator of market expectations around the central bank interest rate setting.

How is LIBOR calculated?

LIBOR is calculated by the Intercontinental Exchange (ICE) on a daily basis and published at 11:55 AM London time. ICE is currently in a transitional period in regards to how it asks banks to calculate their LIBOR submissions. The current process that banks will be transitioned out off is as followed:

Every day, ICE will ask a panel of 11 to 16 contributor banks the following question:

“At what rate could you borrow funds, were you to do so by asking for and then accepting interbank offers in a reasonable market size just prior to 11 am?”

The contributor banks will then have the chance to submit their annualised interest rates between the time of 11:05 AM and 11:40 AM. Once the rates have been submitted, ICE will then sort them by value and exclude the top and bottom 25%. The final LIBOR value for each currency and maturity pair will be the arithmetic average of the remaining numbers.

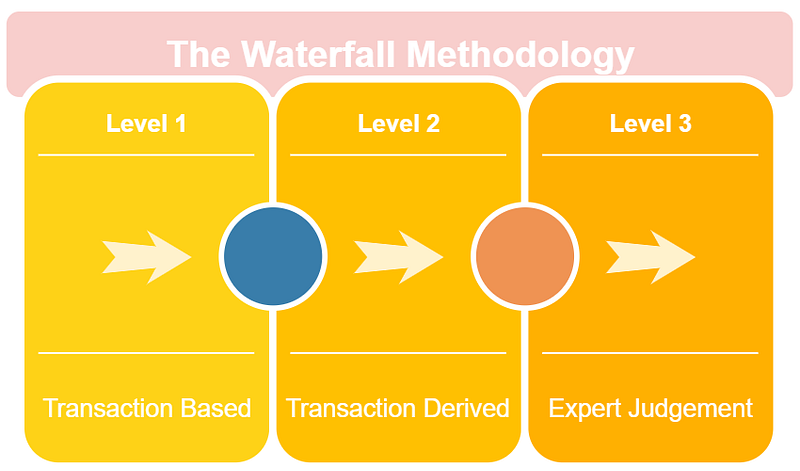

The ICE administration is hoping to transition all banks in 2019 to a new submission method, following a Waterfall methodology. This new methodology was put together on the back of the LIBOR scandal, where banks were caught manipulating the rates and will allow for less wiggle room and ‘expert judgement’. A new definition of LIBOR has also been put together to go with the new methodology:

“A wholesale funding rate anchored in LIBOR panel banks’ unsecured wholesale transactions to the greatest extent possible, with a waterfall to enable a rate to be published in all market circumstances”

Level 1 — Transaction Based

Banks will be able to calculate the LIBOR rate by following a volume weighted average price of eligible¹ transactions with higher weighting for transactions closer to 11:00 AM.

¹: Unsecured deposits and primary issuances of commercial paper and certificates of deposit since the previous submission

Level 2 — Transaction Derived

Where a bank is not in a position to make a Level 1 Transaction Based submission, it will attempt to derive a rate through time weighted past transactions using linear interpolation.

Level 3 — Expert Judgement

Assuming the bank cannot calculate a Level 1 or Level 2 submissions, then it submit the rate at which it can fund itself at 11AM with reference to the unsecured wholesale funding market.

Disclaimer

All data and information provided on this blog post is for informational purposes only. The author makes no representations as to accuracy, completeness, correctness, suitability, or validity of any information on this site and will not be liable for any errors, omissions, or delays in this information or any losses, injuries, or damages arising from its display or use. All information is provided on an as-is basis.

Any referenced links to internal or external website content are not owned by the blog post author and there is no affiliation. Use at your own discretion.