Securitisation: An Introduction

This article will be the first in a series, covering the basics of securitisation. By the end of this article, you will have a good understanding of what securitisation is, what it is used for and the relevant background. You will then be ready to explore individual products that fall under this category; something that I will be covering in subsequent articles.

What do we mean by securitisation?

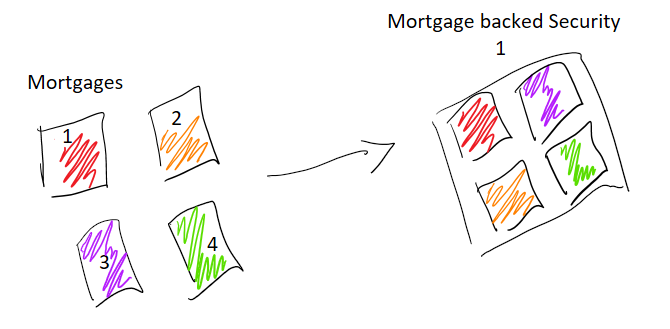

Securitisation is the process of bundling up together assets (or future cash flows) into marketable securities. This means that securitisation is the process where something of value (an asset) that is not usually traded, can be turned into a security that can be traded.

Examples of products that get securitised include loans (consumer loans, business loans, mortgages, etc.), credit card payments etc.

Why would anyone want to do this?

Firstly, we take a look at securitisation from the perspective of the party that owns the individual assets or future cash flows.

Let us first look at mortgages; they are generally originated and owned by banks or building societies. These institutions are generally limited by the central bank, funding money or relevant regulations as to how many loans (mortgages) they can extend (give out) based on how many deposits they hold.

As a bank, to refuse giving out mortgages to financially responsible people due to insufficient deposits held, is generally bad for business. Therefore, these institutions needed a way to increase funding so they can extend out more mortgages; they needed a way to move these loans out of their balance sheets. (Alternatively, they could issue more equity or more debt to get more funding).

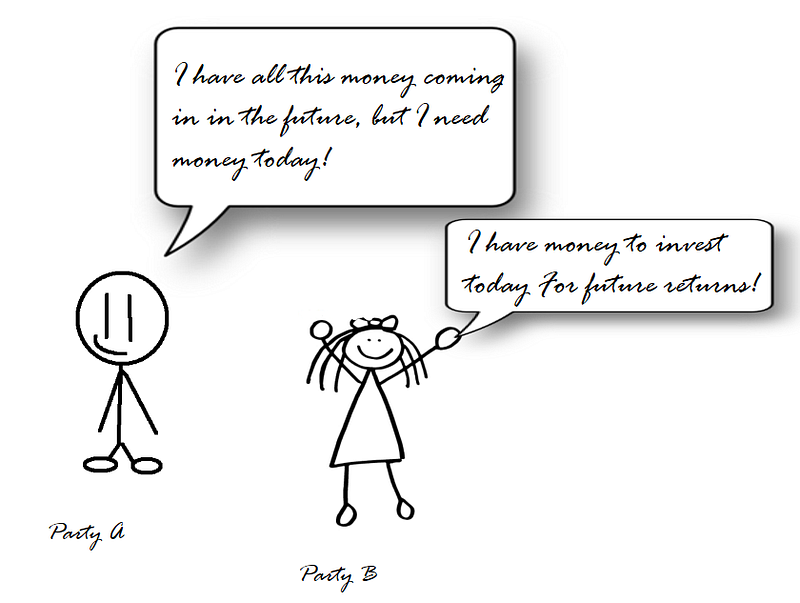

Another example is Credit Card payments. These are future cash flows that a credit card company knows will potentially be receiving in the future. If however, they need access to cash today, rather than having to wait for these payments to come through, they can Securitise these credit card payments and sell the resulting securities for cash now.

Now let’s take a look from the perspective of the party looking to buy a securitised product. Investors are generally always on the lookout for good opportunities where they can invest money today for some future returns. Securitised products often offer rates of return higher than similarly rated assets due to foregone liquidity.

What does the Securitisation process involve?

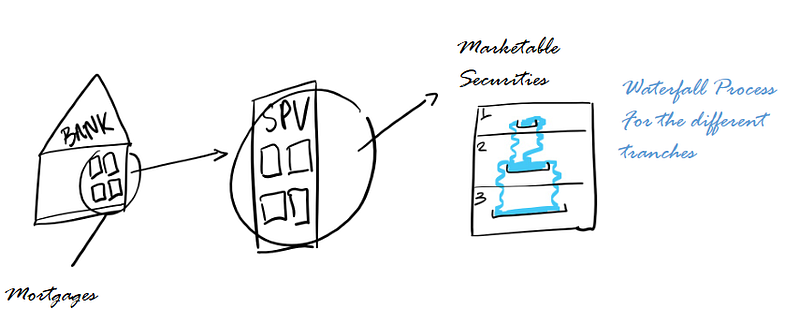

As we have seen so far, the first step in the securitisation process is to move the assets off the balance sheet. To do that, a new subsidiary company is set up known as a Special Purpose Vehicle (SPV), which also separates the financial obligations of the parent company. Then assets of similar characteristics (type, maturity profiles, etc.) are moved under the SPV, which will be responsible for collecting the returns from the assets. At the same time, also create marketable securities (Pass-Through Certificates (PCT)) for which the returns will be tied to.

Following the issue of the securities, rating agencies will review the underlying assets and will assign credit ratings to them. Worth noting here that the resulting securitised products will often be split into seniority classes (tranches of subordination). Each tranch will have different levels of credit protection, and generally, they follow a waterfall approach.

Why should you care about securitisation?

Securitised products were right in the middle of the 2008 credit crisis. Banks were heavily invested in Asset-Backed Securities (ABS) of subprime mortgages, and credit agencies were not valuing the different tranches correctly. Additionally to that, many credit derivatives were built on top of the ABSes, which created layers and layers of complexity, which became hard to risk manage.