Securitization: An Introduction to Mortgage-Backed Securities

In this article, we will endeavor to learn the basics about Mortgage-Backed Securities (MBS) building on our knowledge from ‘Securitisation: An Introduction.’ We will begin by understanding the basics of Mortgage loans, which is the basis of the product before we start looking at MBSes.

What is Mortgages?

Mortgages are loans which are originated for the whole purpose of financing the purchase of real assets (properties). For our purposes, four main characteristics describe mortgages:

- Loan Type

- Mortgage Rate

- Date of Origination

- Repayment Period

Loan Types include things like whether the mortgage rate is Fixed or Variable (also known as Adjustable Rate Mortgage) and whether the loan allows for pre-payment.

When evaluating mortgages, one crucial ratio is the Loan-To-Value ratio, which allows comparing the value of the loan to the underlying asset (the real estate), which is acting as collateral. Another critical piece of information is the creditworthiness of the person taking the loan, often quoted as the FICO score.

What are Mortgage-Backed Securities?

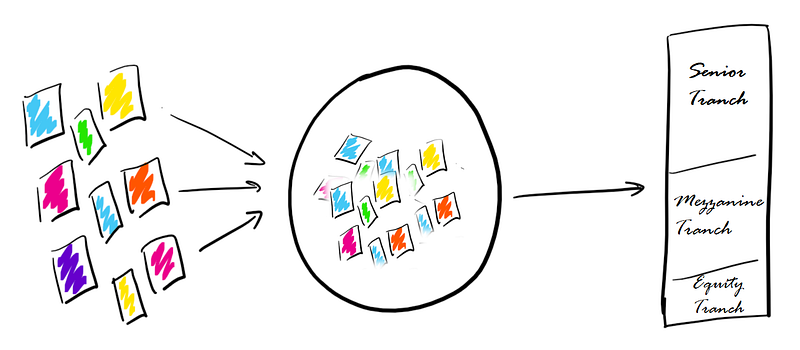

In the introductory article, we saw that securitization is the process of bundling up assets together into marketable securities. MBS are tradable securities (an instrument) that are made up of pools of underlying mortgages.

The simplest form of MBS are known as ‘Pass Throughs’; that is, they pass any payments to the underlying mortgages to the MBS’ investors (interest, principal, pre-payment).

The servicer of the MBS (the SPV) will facilitate the payments from the mortgages to the MBS security holders for a small fee. The servicer will also facilitate payment from the guarantor in case of any mortgage defaults.

MBS were also split into tranches, as we saw in the introductory article. The top installment was known as the ‘Senior Tranch’ and was most likely AAA-rated, corresponding to a large percentage of the overall underlying principal. Then came the ‘Mezzanine Tranch, ’ which was likely BBB rated, and finally came the ‘Equity Tranch,’ which was not rated.

How did MBS play a role in the financial meltdown of 2008?

In 2008 there was a vast number of subprime mortgages due to a relaxation of the lending standards. Most of these subprime mortgages were on a variable rate, most of which started with a ‘taster’ rate that was very low but quickly increased significantly after 2 or 3 years.

Mortgage-Backed Securities were built on top of these subprime mortgage pools, adding a new layer of complexity that hid the state of the subprime mortgage borrowers’ credit quality. Often, investors assumed that knowing the loan-to-value (LTV) and FICO score of the mortgages would be sufficient to asses the quality of the MBS. However, real estate asset values were inflated due to the high demand driven by the low lending standards driving the LTV down, and FICO scores were of questionable quality.

In the case of borrower default, one theorized that the real estate asset could have been sold as collateral to cover the cost of the loan. However, due to the falling market at the burst of the bubble, the real estate assets would no longer cover the value of the loans.

To make matters worse, the senior tranches of the MBS would have AAA ratings even though the underlying mortgages were subprime, meaning that there was a massive discrepancy in how they were priced and what they were worth.

In the Series

This post is part of a series of articles I wrote regarding securitizations. If you have enjoyed it, you might find the following articles also interesting:

and the aftermath regulation: