PSLF Update — April 2021

There have been a lot of changes the past six months.

It’s been a whirlwind year for the PSLF program, from student loan payments being paused to updated application forms. Here are the highlights:

- The separate PSLF and TEPSLF were combined into a single form..

- DOE upgraded their PSLF Help Tool.

- The pause on student loans means “free money” for PSLF borrowers

- The effect of (possible) mass forgiveness on the PSLF program

Let’s dive right in.

(Note 1: For explanations of the data and corresponding calculations, please see the original article about parsing the PSLF reports.)

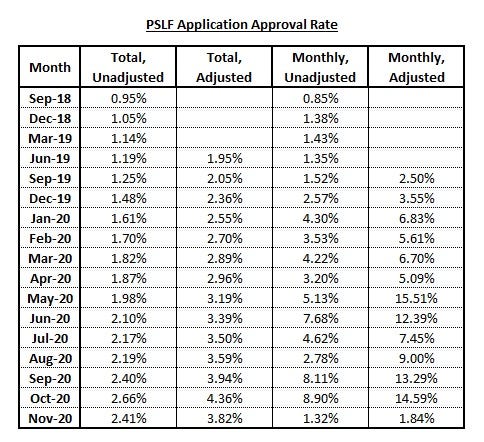

Approval Rate

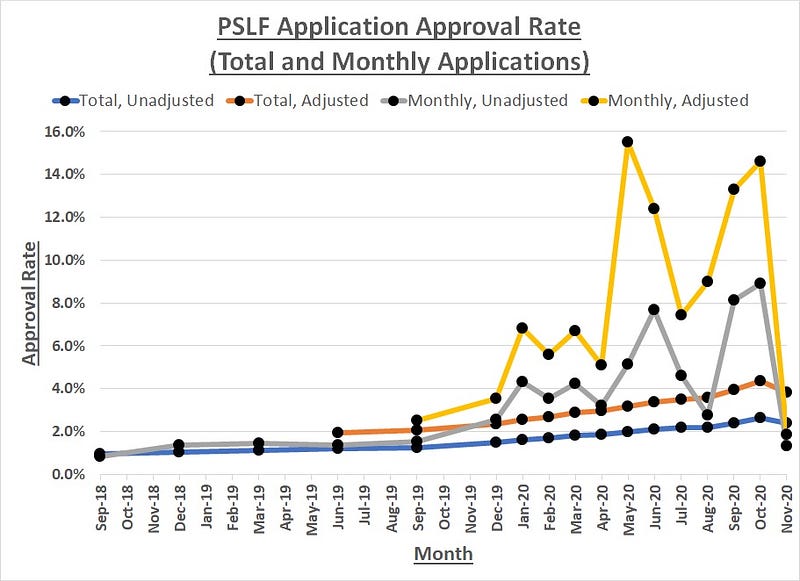

After taking a little dip this summer, adjusted approval rates have jumped back up into the mid-teens again. I’ll address the nose-dive in November in a minute, but I want to center your attention on the increasing approval rates.

We are now no longer in the dog days of PSLF. There is a definite upward trend, even when using the unadjusted data.

This upward trend is only going to keep rising.

PSLF started with the graduating class of 2007, with the earliest forgiveness available in fall of 2017. That first cohort (graduates from 2007 to 2011-ish) got royally screwed by the DOE’s disaster of a rollout.

However, the years following saw more marketing, more (and accurate) information from the DOE, more borrowers taking DOE and FedLoan to talk, and more discussion among borrowers about earlier mistakes.

It is no surprise to see the approval rates increasing, and this is just the tip of the iceburg.

November Dip

The big downward swing in November can be chalked up to two things.

- Updating the application form

- A flood of applications

First, the last time the DOE released PSLF data was in December 2020, with the information only through November 2020. The main reason is that the applications forms for the PSLF and TEPSLF programs were combined, which means the old reporting format is moot.

Switching in the middle of November also had the unfortunate side effect of tanking November’s numbers, making it look like there was

I’m guessing that this messed up their data (why they didn’t prepare for this, I’ll never know, but am not really surprised at their ineptitude at this point), and they haven’t reported on it since.

Second, the past 12 months have seen just under 10,000 application reviews being completed. For some reason, in November there were just over 50,000 application reviews completed, with no similar increase in approvals.

I’m not sure what happened there, but it might be because of the application switch, the end of the former administration shoving paperwork through, or unqualified borrowers flooding the system in false hope of approval.

Regardless of the reason, the data set is an outlier, so ignore the November number and let’s celebrate the almost 15% approval rate in October 2020.

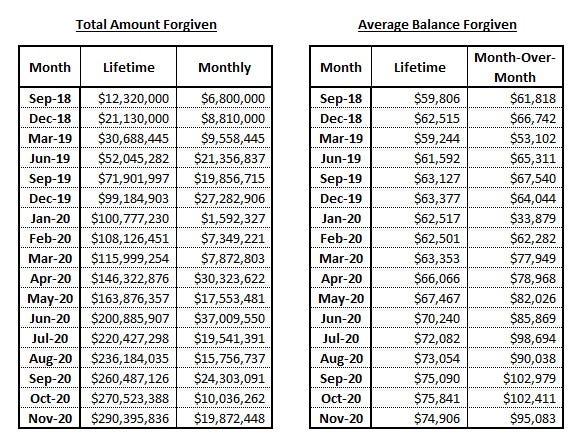

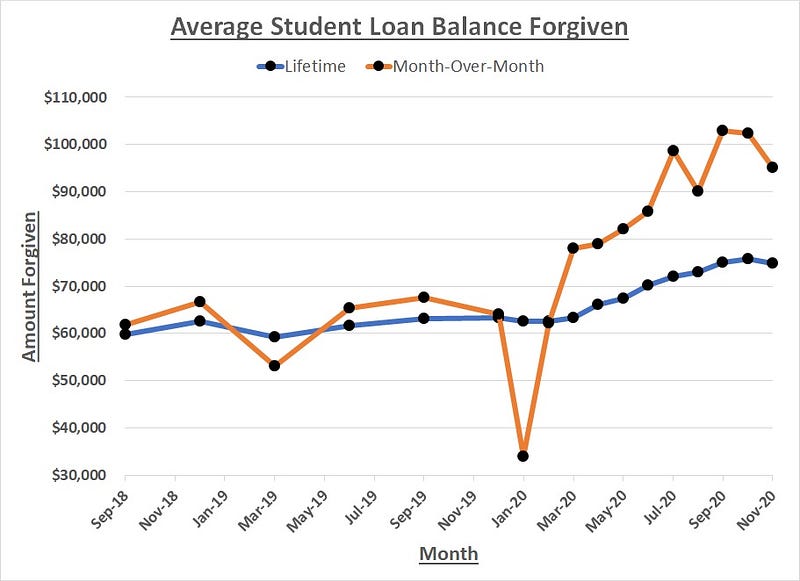

Student Loan Amount Forgiven

Through November 2020, the PSLF program has forgiven close to $300 million.

That’s small compared to the overall $1.7 trillion in current outstanding student loans, but it’s not nothing, especially to the 3,776 people who have received full forgiveness so far.

What other program has reached a similar milestone and gotten called a failure?

None!

In the past two months alone, 1,424 borrowers have received an average of $95,000 in forgiveness.

And these are people who started paying in August 2009 or earlier. Can you imagine what the average loan forgiveness will be given the past 10 years of tuition inflation?

Other PSLF News

New Application Form

As I mentioned above, starting in November of 2020, a new form was rolled out that combined both the PSLF and TEPSLF applications. It was created to help reduce the number of errors seen with people aubmittting the wrong form to the wrong program.

The problem here is that now the data is all messed up, so there is no way to publicly know if it’s working. Part of me is hoping that the DOE is just waiting until they have the kinks worked out to release solid data. But another part of me worries that it’s been a colossal mistake and the DOE is trying to hide it as long as possible.

This new combined form came along right in the middle of an administration change, so I’m sure that is further exacerbating the delay in data releases.

New Online Help Tool

One bit of good news is that the DOE rolled out a new PSLF online help tool. It is much more robust and user friendly than the old calculator. You actually have to log in to your FSA account, and it can use your exact data.

Payments on Hold

PSLF borrowers are getting a hell of a deal right now with the pause in student loan payments. As of this writing, loan payments will have been paused until September 2021, which is 19 months total.

That’s 19 months of no payments, but still counting towards PSLF.

Given that the PSLF program requires 120 payments, we are getting almost 1/6 of that payback time for free. For those who qualified at the very beginning, we’re now getting 100% forgiveness while only paying 83% of the cost.

Out-freaking-standing.

Impact of Blanket Forgiveness

There has been much discussion about the Biden administration possibly forgiving up to $50,000 in federal student loan debt for everyone. If this goes through, there will be two main effects on PSLF.

- People will have their full loans forgiven

- People with super-high loans will stay in their current jobs

The borrowers who get their loans totally forgiven will now have no barriers to pursuing the, on average, higher paying private sector jobs. The downside is that competition for those jobs becomes higher, reducing their chances of getting that better salary.

The borrowers who have six figures of student loan debt (like me) will keep on keeping on, plugging away every month until they get their 120 payments, then wait until their loans are forgiven.

The overall impact will be a massive streamlining of the PSLF program, with the most earnest and dedicated borrowers sticking with the program and within the rules.

Success Stories

Every month I like to highlight a few PSLF success stories, showing just how big of an impact this program has on people.

PSLF

$90,000 — $57,000 — $125,000 — $46,000 — $170,000 — $57,000

TEPSLF

And some of my favorite advice from Reddit is below:

- Keep filing paperwork every year and make your payments.

- Keep track of your total payments (not amount, number of monthly payments).

The process is pretty straightforward:

1. File your annual paperwork, including application for forgiveness. (Wet signatures on things!)

2. If you get rejected for PSLF forgiveness, note how many payments they show you have made.

3. File for TEPSLF

4. When/If TEPSLF rejects you, note how many extra payments you may pick up from them.

5. The month those two numbers would add up to 120, file for PSLF forgiveness again. When you get rejected, file for TEPSLF.

Turnaround for the whole process for me this time was ~5 weeks.

PSLF is a wonderful program that has finally started working the way it was originally planned.

Even if you aren’t banking on forgiveness, if you are working in at a qualifying employer, then I suggest you submit an Employment Certification Form (ECF) to get your loans in the system.

If you change jobs, oh well. PSLF just wasn’t in the cards for you.

But if you stay and make 120 payments, then by golly, you just got your loans forgiven!

Related Articles/Resources

- PSLF Update — September 2020

- PSLF Update — August 2020

- PSLF Update — July 2020

- The Basics of Public Service Loan Forgiveness

- The Truth About PSLF

- Is PLSF Right for Me?

- In Defense of Public Service Loan Forgiveness

- How to Hack the Secretly Successful PSLF Program

- How I Still Have $135,000 in Student Loan Debt (Even After 21 Years)

Most Recent Stories

- Will Student Loan Forgiveness Actually Work?

- My Worst Financial Mistake

- The Anti-Debt Fanatics Are Wrong

- 3 Reasons to Buy a House Right Now

- What’s Going On With Inflation?

This article is for informational purposes only and should not be considered Financial or Legal Advice. Not all information may be accurate. Consult a financial professional before making any major financial decisions.

{kind=link}