Blockchain retrospective

A look at the cognitive biases that led me here

Introduction

My name is Joshua Davis. In 2016 I took a multi-year leave of absence from a salaried position in order to research peer-to-peer architecture. My intent was to build an app for decentralized insurance. Progress has been slow. Mostly I’ve waited for Ethereum infrastructure to be built to support my app and while waiting I’ve applied for patents.

The most important thing I did the past five years was to become convinced that communities can insure themselves. To understand the problem I’m trying to solve start with this blog post. This architecture sidesteps regulation which has prevented communities from forming these types of self-insured collectives in the past.

Mistakes, I’ve had a few. But then again…

Taking a step back and seeing our mistakes can sometimes be awkward but may also prove to be profitable. My start was misguided. But after I persisted the result was valuable.

I made progress toward building a blockchain app. My start lacked a lot of rational judgement but I continued to evaluate architectures that were flawed until I found one that was good. The result was a new type of insurance architecture that eliminates the need for a centralized entity to hold reserves.

In a previous post, I explained why I started this journey. In this post, I provide perspective as to what I’ve gained up till now.

Without cognitive biases I wouldn’t have been foolish enough to even bother to try

Fake Internet Money

The ICO craze was fueled by intense speculation. The blockchain minted several virtual millionaires within the span of a few months in the first half of 2017. All that money may have gone to people’s heads. Many realized that if they could predict the next Ethereum they were a heartbeat away from becoming multi-millionaires. Being an early investor in cryptocurrency definitely strengthened my own delusional views 📈🤑. Gaining hundreds of thousands or even millions of dollars within a year without having earned it felt like a vindication of my intuitive prowess 🤣😂.

No harm in the memes

Now that I look back, I can clearly see how the integration of memes into the discussion of cryptocurrency played a role. Changing an idea into a meme makes it much easier to change a person’s inner narrative.

“Bitcoin and things like it are the equivalent of the red pill.” — Chamath Palihapitiya

This is speculation on my part, perhaps future researchers will become convinced that cryptocurrency communities on Reddit circa 2016–2017 entered into a type of group perceptive psychosis. People are being told that they are the equivalent of Neo from the matrix. If you are the star of your own inner narrative, the hero of the world, the one that has “taken the red pill,” how can you then go back to your life prior to crypto? That would be like saying, “you know what, I just realized I was never really that special, and all these ‘newfound friends’ are not really my friends.” This is the power of groupthink (collective self-deception). If you ever tried waking up from the dream then your friends would immediately gaslight you into thinking that you were crazy for wanting to “plug yourself back into the matrix.” I suspect that this is the real power of memes, they change our inner working narrative. When memes are integrated into Reddit alongside scholarly whitepapers they have all the more authority to keep people down the rabbit hole (authority bias).

Dunning-Kruger Effect

My plan was simple. First I needed to create a stylish website to host my whitepaper. Then I would publish my brilliant insights on the Ethereum Reddit forum. Finally, it would be relatively trivial for me to build a team of developers and crowdfund a few million dollars of capital. By some conservative estimates, my app could then go mainstream by the summer of 2018. What could possibly go wrong?

This was how Ethereum started, if Vitalik Buterin could do it then why not me? Forget taking a few years to work for another successful startup to gain valuable experience or perspective. This step was unnecessary for the founders of other apps on Ethereum such as Augur or MakerDAO. Forget trying to publish in a peer-reviewed journal, what would be the point of that? Sure, occasionally I might doubt myself, who doesn’t. From time to time I might wonder if failing to publish in a reputable journal made my ideas seem more fringe. Then I’d immediately invoke the Bitcoin whitepaper as if that was the ultimate vindication of publishing to an obscure internet forum 🤣(anchoring bias).

I’m reminded of the Dunning–Kruger effect. Developed by social psychologists David Dunning and Justin Kruger, their poster child was a man who, after learning that lemon juice could be used as a type of invisible ink, decided to rob a bank using this insight. “(he) robbed banks while his face was covered with lemon juice because he believed it would make him invisible to the surveillance cameras.” People can talk themselves into believing anything I suppose.

“Obviously everyone’s terrible when they start (doing something) … you need to have a certain amount of self-delusion to persist despite all evidence to the contrary … If you haven’t got enough self-delusion you won’t persist, you’ll give up. But, if you got too much and you never get any good you just get stuck in this loop of doing terrible gigs. Thankfully I was delusional enough, or you know adamant enough, (to say) I’m gonna do this and so I think I would have definitely persisted.” — Matt Parker

Is it really impossible that someone without formal training in insurance markets would ever develop a viable model for peer-to-peer insurance? It’s certainly unlikely but not impossible.

You have to convince people. Conviction and confidence go hand in hand. Although I might have been publishing my research on Medium and Reddit that doesn’t mean I couldn’t publish in a peer-reviewed journal if I really wanted to. To overcome the fact that I was not working at a major university or affiliated institution, I just needed to express an even stronger conviction. Whatever authority I lacked I could simply make up for by sheer confidence and force of will. Is it impossible that some significant insight might be published on these platforms by somebody who was previously unknown? Unlikely but not impossible.

The outcome of four years

I have written over 150,000 words on the topic of peer-to-peer insurance and I’m still writing because it’s an important topic. I learn more as I continue to research and write. I wouldn’t continue if I wasn’t convinced that there was value in doing so.

Traditional Insurance is flawed

TandaPay’s approach was developed in response to a fundamental flaw in markets for healthcare insurance..

The most obvious flaw in healthcare insurance markets

Traditional insurance is flawed in that it uses one premium to both pay claims, and provide profit for the insurer. In healthcare this has led to a volume-based payment system. Such a system incentivizes insurers to focus on the total number of tests, operations, surgeries and treatments administered to patients. This focus on volume seems to confuse patient outcomes with the volume of services required to reach those outcomes.

If you are an insurer and you want to increase your profits what do you do? Insurers cannot make their slice of the pie bigger by increasing the share of a premium that is used for administrative costs. The Affordable Care Act places specific limits on what percentage of a premium becomes an insurer’s profits. Insurers can only make the entire pie bigger which gives all of the providers in the system (the insurer included) more pie. This requires an insurer to increase the total volume of services consumed by policyholders.

When the ACA fixed the percentage of a premium which could be used for administrative costs it didn’t lower the total cost of insurance. On the contrary it resulted in an increase in consumption of healthcare services. After the ACA passed the only way an insurer could increase their profit was if the total spent on healthcare increased.

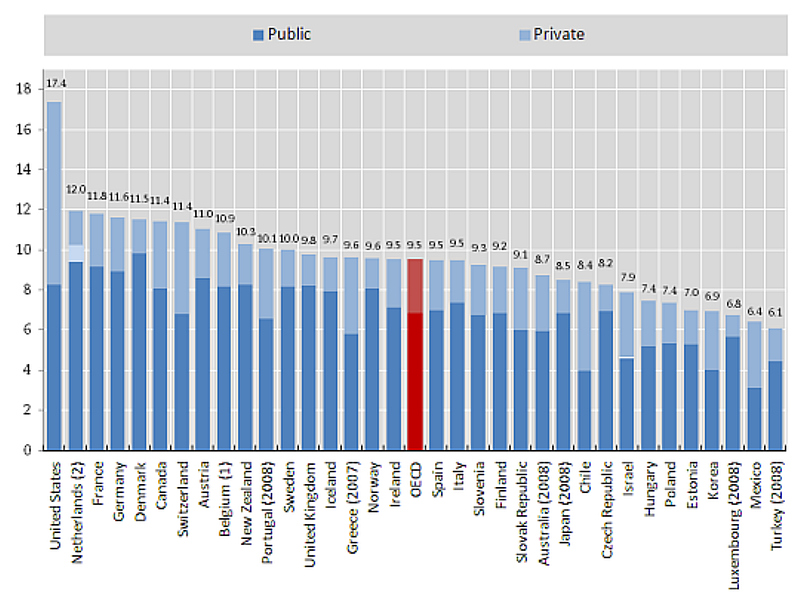

The chart below gives you a clear visualization of this effect and you can watch this video if you need further explanation. If you want to watch a great documentary on this subject I highly recommend Money and Medicine and the associated viewer’s guide.

The most obvious solution

It’s clear that we need to decouple premiums used to pay claims from administrative fees paid to providers. This change would require that 100% of every premium dollar must be used to pay claims and rebates to policyholders. It means that an insurer can’t make more profit simply by increasing the volume of services consumed.

What would happen if we built a system where 100% of the premiums were used to pay claims and rebates?

This was the starting point of all of my research into peer-to-peer insurance. What would happen if we built a system where 100% of the premiums were used to pay claims and rebates? Once I started down this path, however, the results led me in a totally unexpected direction.That direction became TandaPay.

An unexpected result

If you are curious to see what makes TandaPay a really unique protocol you should start with this post:

Once you finish that post you are primed to read the most important thing I’ve ever written:

The post I wrote on sexual harassment data was a completely unexpected result. The significant limitations which constrained the protocol likely helped to produce this finding.

These are just a few of the constraints which limit the protocol:

- Insurance pools must be small groups of 50 to 100 policyholders.

- Policyholders should be local to each other or part of the same social network.

- The value of a claim should be relatively low, for the US market this is less than $1000.

- All claims submitted to the group for approval need to be paid an identical amount.

As a result of these limitations the protocol isn’t very good at providing coverage which is comparable to a traditional insurer. This forced me to research other use cases. The use case which holds the most promise is completely unrelated to insurance.

Given our recent political turmoil most people are familiar with the term “whistleblower.” What people may find unfamiliar is that some companies use software solutions to protect the anonymity of individuals who attempt to file complaints. The TandaPay protocol is a special variant of a whistleblower complaint system. It uses financial incentives to guarantee that the content of complaints submitted by whistleblowers are true. It requires that participants, within the group from which the whistleblower complaint originated, verify the facts of the complaint.

There are no publications on the internet which I have found that provide a description of a software system like TandaPay. TandaPay functions by combining a system for complaint validation with a system of financial incentives. I believe that if this type of system could be deployed, it would represent a new innovation which has never previously existed. My final conclusion is that the TandaPay protocol would provide more value when integrated into whistleblower software than it would as a protocol for insurance.

If you can understand what I wrote and reach the same conclusions about what the protocol does then the value of my research is self-evident. One only needs to read what I wrote to understand why this is true. More information regarding my research into TandaPay can be found in this post.

My name is Joshua Davis. In 2016 I took a multi-year leave of absence from a salaried position in order to research peer-to-peer architecture. My intent was to build an app for decentralized insurance. It’s a work in progress. Well, it may be a bit of an overstatement to say that it’s is a work in progress; but, the statement is inaccurate in a good way. It’s the kind of inaccuracy that aims to show consideration for how other people might judge me in the midst of a crisis. I shouldn’t say crisis, this isn’t a crisis really it’s a situation. It’s the kind of inaccuracy you want to hear from your kid’s school superintendent when they tell you that the pandemic has been “challenging.” The last thing anyone wants to hear from their kid’s superintendent are words like “catastrophic” or “terrifying.” A challenge can be overcome, but terror is completely different. Terror is realizing that your car has careened off the edge of a cliff. No one wants that, that’s alarmist.

In other words, it isn’t an overstatement to say I am working on an app for peer-to-peer insurance, rather, it’s a “forward-looking statement.” Nevertheless, my ambition to develop peer-to-peer insurance has only progressed since I started. I have applied for several patents, attempted a few prototypes, and wrote a bunch of blog posts that no one will ever read (no seriously stop). Despite everything both good and bad, I remain steadfast in my decision to build the first decentralized insurance app. Not that there aren’t already insurance apps running on the blockchain, just none that are designed to solve real-world problems.

Mistakes, I’ve had a few. But then again…

TL;DR: Taking a step back and seeing our mistakes can sometimes be awkward but may also prove to be profitable. Getting the most from this exercise will require me to admit that I was wrong about a number of things that I previously believed. Well, maybe not wrong, but misguided perhaps. If I’m honest and willing to laugh at myself I might even find some humor in my own cognitive biases.

I think it was the most interesting man in the world who once said, “I don’t always make mistakes, but when I do I prefer to learn from them.” This post is a record of the progress I made toward building a blockchain app in the absence of rational judgment. Hopefully, my fallibility proves to be both educational and entertaining.

In a previous post, I explained why I started this journey. In this post, I provide perspective as to what I’ve gained up till now.

- Part 1: Cognitive biases which shaped my decisions from 2016–2017.

- Part 2: What I gained by researching and writing for several years.

Part 1: Although hindsight has 20/20 vision, cognitive biases remain blind as ****

Cognitive biases

The ICO craze was fueled by intense speculation. The blockchain minted several virtual millionaires within the span of a few months in the early half of 2017. All that money may have gone to people’s heads. Many realized that if they could predict the next Ethereum they were a heartbeat away from becoming multi-millionaires. Being an early investor in cryptocurrency definitely strengthened my own delusional views 📈🤑. Gaining hundreds of thousands or even millions of dollars within a year without having earned it felt like a vindication of my intuitive prowess 🤣😂. (illusory correlation)

No harm in the memes

Now that I look back, I can clearly see how the integration of memes into the discussion of cryptocurrency played a role. Changing an idea into a meme makes it much easier to change a person’s inner narrative.

“Bitcoin and things like it are the equivalent of the red pill.” — Chamath Palihapitiya

This is speculation on my part, perhaps future researchers will become convinced that cryptocurrency communities on Reddit circa 2016–2017 entered into a type of shared psychosis. People are being told that they are the equivalent of Neo from the matrix. If you are the star of your own inner narrative, the hero of the world, the one that has “taken the red pill,” how can you then go back to your life prior to crypto? That would be like saying, “you know what, I just realized I was never really that special, and all these ‘newfound friends’ are not really my friends.” This is the power of groupthink (collective self-deception). If you ever tried waking up from the dream then your friends would immediately gaslight you into thinking that you were crazy for wanting to “plug yourself back into the matrix.” I suspect that this is the real power of memes, they change our inner working narrative. When memes are integrated into Reddit alongside scholarly whitepapers they have all the more authority to keep people down the rabbit hole (authority bias).

The value of confirmation

I somehow deluded myself into thinking that I just needed to publish a my brilliant insights on an obscure internet forum. This was how Bitcoin and Ethereum started! I never even seriously considered the value of publishing in a peer-reviewed journal. I used to wonder if failing to publish in a reputable journal made my ideas seem more crackpotty. Then I’d immediately invoke the Bitcoin whitepaper as if that was the ultimate vindication of publishing to an obscure internet forum 🤣😂(anchoring bias). I’m laughing as I write this because I’m reminded of the Dunning–Kruger effect. Developed by social psychologists David Dunning and Justin Kruger; their poster child was a man who “robbed banks while his face was covered with lemon juice, because he believed it would make him invisible to the surveillance cameras🤪.” People can make themselves believe anything and I’m definitely no exception.

Calling someone a crackpot may not be very nice, but we’ve all had the feeling that some teaching or some person is crackpotty. The term is used to describe a person who emphatically promotes an idea that most people would likely believe is false. Is it impossible that someone without formal training in insurance markets would ever develop a viable model for peer-to-peer insurance? No, it’s not literally impossible. But, we shouldn’t place a very high credence in the likelihood that such a person exists either.

You have to convince people as to the validity of the your work. This is where the value of a peer-reviewed publication comes in. The platform on which you publish adds to or subtracts from the credence that what you are writing is of significant value. Publishing one’s “research” on Medium and Reddit doesn’t exactly lend a great deal of authority to the author. Someone who has only published on these platforms should be viewed skeptically. What are the odds that their publication will someday advance the development of the field in which they are studying?

Is it impossible that some significant insight might be published on these platforms by somebody who was previously unknown? Although it’s not impossible, it’s just so unlikely that no one should believe it’s true.

Satoshi Nakamoto (the creator of Bitcoin), and Vitalik Buterin (the creator of Ethereum) are truly brilliant individuals who have contributed to their respective fields. But 99.99% of people (myself included) are not like them. The funny part is how long it has taken (plus the financial cost) for me to figure this out. I still hear a little voice inside saying,

“what’s hundreds of thousands of dollars compared to the opportunity to pursue your dream? It’s only money.”

🤣😂 I’m gonna kill that voice someday🔪.

Visionary or crackpot

The difference between a crackpot and a visionary is largely based on the perceptions of other people. Some people are initially labeled as crackpots and later generations relabel them as visionaries. I know that people will usually cite someone like Galileo who was convicted of heresy for teaching that,

I personally find the story of Georg Cantor to be more interesting because it highlights how drastically public opinion about someone’s work can change. Cantor after being labeled a crackpot came under severe emotional distress, he later died in a sanatorium. His theories however were later vindicated, to the degree that set theory has become a fundamental theory in mathematics. There cannot be a better archetype for the misunderstood visionary. Here was a man whose ideas were so strongly rejected that he lost his sanity, but after his death his ideas avenged him by tormenting his critics😏.

From the Wikipedia entry:

Leopold Kronecker’s public opposition and personal attacks included describing Cantor as a “scientific charlatan”, a “renegade” and a “corrupter of youth”. Kronecker objected to Cantor’s proofs that the algebraic numbers are countable, and that the transcendental numbers are uncountable, results now included in a standard mathematics curriculum. Writing decades after Cantor’s death, Wittgenstein lamented that mathematics is “ridden through and through with the pernicious idioms of set theory”, which he dismissed as “utter nonsense” that is “laughable” and “wrong”.

No one working on a startup thinks, “this is going to fail”

“Obviously everyone’s terrible when they start (doing something) … you need to have a certain amount of self-delusion to persist despite all evidence to the contrary … If you haven’t got enough self-delusion you won’t persist, you’ll give up. But, if you got too much and you never get any good you just get stuck in this loop of doing terrible gigs. Thankfully I was delusional enough, or you know adamant enough, (to say) I’m gonna do this and so I think I would have definitely persisted.” — Matt Parker

When it comes to working on one’s own startup, one rarely make choices based upon the rational odds of success (optimism bias). The media we consume internalizes a very strong survivorship bias. We only hear about those founders who made it and were successful. This is why most founders internalize that their project will also be a success. It goes without saying that no one wants to hear about the various startups which have failed. That’s why I’m so glad you’re here🤣😂! If you’re working on a startup let me be the first to pat you on the back and tell you, “when you wake up it’s going to be OK, we’re still here for you.”

Part 2: The outcome of four years

This post is not an exercise in choice-supportive bias. I have written over 150,000 words on the topic of peer-to-peer insurance and I’m still writing because it’s still an important topic. Although my findings have yet to be confirmed by a reputable authority, I don’t think it’s hard for someone to reach the same conclusions I have.

Traditional Insurance is flawed

TandaPay’s approach was developed in response to a fundamental flaw in markets for healthcare insurance.

The most obvious flaw in healthcare insurance markets

Traditional insurance is flawed in that it uses one premium to both pay claims, and provide profit for the insurer. In healthcare this has led to a volume-based payment system. Such a system incentivizes insurers to focus on the total number of tests, operations, surgeries and treatments administered to patients. This focus on volume seems to confuse patient outcomes with the volume of services required to reach those outcomes.

If you are an insurer and you want to increase your profits what do you do? Insurers cannot make their slice of the pie bigger by increasing the share of a premium that is used for administrative costs. The Affordable Care Act places specific limits on what percentage of a premium goes to administrative costs. Insurers can only make the entire pie bigger which gives all of the providers in the system (the insurer included) more pie. This requires an insurer to increase the total volume of services consumed by policyholders.

When the ACA fixed the percentage of a premium which could be used for administrative costs it didn’t lower the total cost of insurance. On the contrary it resulted in an increase in consumption of healthcare services. After the ACA passed the only way an insurer could increase their profit was if the total spent on healthcare increased.

The chart below gives you a clear visualization of this effect and you can watch this video if you need further explanation. If you want to watch a great documentary on this subject I highly recommend Money and Medicine and the associated viewer’s guide.

The most obvious solution

It’s clear that we need to decouple premiums used to pay claims from administrative fees paid to providers. This change would require that 100% of every premium dollar must be used to pay claims and rebates to policyholders. It means that an insurer can’t make more profit simply by increasing the volume of services consumed.

What would happen if we built a system where 100% of the premiums were used to pay claims and rebates?

This was the starting point of all of my research into peer-to-peer insurance. What would happen if we built a system where 100% of the premiums were used to pay claims and rebates? Once I started down this path, however, the results led me in a totally unexpected direction.That direction became TandaPay.

An unexpected result

If you are curious to see what makes TandaPay a really unique protocol you should start with this post:

Once you finish that post you are primed to read the most important thing I’ve ever written:

The post I wrote on sexual harassment data was a completely unexpected result. The significant limitations which constrained the protocol likely helped to produce this finding.

These are just a few of the constraints which limit the protocol:

- Insurance pools must be small groups of 50 to 100 policyholders.

- Policyholders should be local to each other or part of the same social network.

- The value of a claim should be relatively low, for the US market this is less than $1000.

- All claims submitted to the group for approval need to be paid an identical amount.

As a result of these limitations the protocol isn’t very good at providing coverage which is comparable to a traditional insurer. This forced me to research other use cases. The use case which holds the most promise is completely unrelated to insurance.

Given our recent political turmoil most people are familiar with the term “whistleblower.” What people may find unfamiliar is that some companies use software solutions to protect the anonymity of individuals who attempt to file complaints. The TandaPay protocol is a special variant of a whistleblower complaint system. It uses financial incentives to guarantee that the content of complaints submitted by whistleblowers are true. It requires that participants, within the group from which the whistleblower complaint originated, verify the facts of the complaint.

There are no publications on the internet which I have found that provide a description of a software system like TandaPay. TandaPay functions by combining a system for complaint validation with a system of financial incentives. I believe that if this type of system could be deployed, it would represent a new innovation which has never previously existed. My final conclusion is that the TandaPay protocol would provide more value when integrated into whistleblower software than it would as a protocol for insurance.

If you can understand what I wrote and reach the same conclusions about what the protocol does then the value of my research is self-evident. One only needs to read what I wrote to understand why this is true. More information regarding my research into TandaPay can be found in this post.