My Startup Journey

The Quixotic Quest for Blockchain Insurance Applications

Tilting at windmills

Obviously everyone’s terrible when they start (doing something) … you need to have a certain amount of self-delusion to persist despite all evidence to the contrary … If you haven’t got enough self-delusion you won’t persist, you’ll give up. But, if you got too much and you never get any good you just get stuck in this loop of doing terrible gigs. Thankfully I was delusional enough, or you know adamant enough, (to say) I’m gonna do this and so I think I would have definitely persisted. — Matt Parker

Dynamis was going to be the “401(k) of severance” or so I thought. In the same way that the 401(k) had revolutionized retirement, personalized individual severance accounts could revolutionize employment. If you have time, click on the link to watch the video. Dynamis was going to be, “the sensible choice for severance,” it was one of those great ideas that made perfect sense on paper. In 2015, so many things came together at just the right time in just the right way to make it seem as if I had stumbled across, “the opportunity of a lifetime,” or as Don Quixote might say, “Fortune is guiding our affairs better than we ourselves could have wished.”

The Story of Dynamis

Looking back now it’s clear that the driving force behind my actions wasn’t some great market insight. Pensions would still dominate today as the main way American’s save for retirement had it not been for a change in the tax code. The name 401(k) comes from the tax code. No one would have thought that when executives at Kodak originally asked congress for this exemption it would one day lead to an entirely new market of financial products focused on retirement. If you change the tax code you change a lot. It would be unwise to assume that if the tax code had not been changed anything like the 401(k) would even exist today to compete with the pension. With humility, I now admit what drove me to waste so much of my time and money on my initial startup was my own hubris and a personal offense.

Summary: About 20 years ago International Paper (IP) had decided to outsource their IT staff to EDS which was later acquired by Hewlett-Packard (HP) to become HP-EDS enterprise solutions. After HP shed many of their IT consulting clients 5 years ago, IP was forced to rehire these workers.

Bob was one of those outsourced / rehired workers. I remember him as a dedicated, tireless network engineer who was super friendly and always helpful. To me he was just Bob. He had worked out of the same Memphis office which was the headquarters for International Paper for nearly 25 years when I left the company in 2016. I imagine that when he was transferred from IP to EDS nearly 20 years ago he had to accept some sort of reduction in his years of service but what choice did Bob really have?

Is he going to say, “no I worked hard for my PTO so I’m going to walk away if you take it from me.” So he signs the paper which basically formalizes something equivalent to “you were fired, then immediately you were hired, welcome to your new job Bob!” Except it’s the same office, same team, same everything minus the years of service.

A little over a decade later in 2014 HP-EDS decides they are going to shed as many jobs as possible since the IT outsourcing business was no longer profitable for them. Times are tough for HP but everyone is going to keep their jobs once they are transferred to IP. They make it seem like everything’s ok outwardly, but we are going through all the same motions a new hire would go through. We are being severed and not everyone is getting the same severance package (more on that later).

Bob and I are sitting on a bunch of conference calls to, “help us with the transition,” there’s a lot of paperwork but buried in all the fine print was the matter of our years of service and our benefits package.

I’m on this one call multi-tasking and someone is mad, really mad. I’ve never seen George lose his temper. What’s going on, what happened?

George: So basically you’re telling me that even for employees like Bob whose been serving IP faithfully for over 20 years he can only keep the years of service he’s had with IP?

Bill: Now hold on, I can see people are getting fired up about this but I want you to know that we negotiated the best possible deal for our people. We talked about this issue at length but the problem was that IP’s human resources has a formal policy. They’d need a vote by their board of directors …

Bill gives a talk about how the decision to “negotiate” away a combined total of more than 300 years of service was because HR was unwilling to budge on their policies and procedures. This was because it would be unfair given how many other acquisitions and mergers IP participates in. Over the past five years IP has acquired more than 5,000 employees through acquisitions and should they really be “on the hook” for all of their years of service?

How could they treat Bob like this? I wish I would have said:

This isn’t some stranger in some paper mill you will never visit. This is someone who has a cubicle down the hall from yours but travels a lot more than you do. Bob has co-labored with you in the Memphis office for more than 20 years. Now all of a sudden he’s a new hire with benefits equivalent to 8 years of service? If you treat Bob this way whom you’ve known and trusted for more than 20 years I can’t imagine how you’d treat someone with whom you’ve established no relationship of trust and mutual respect.

Inside I snapped. my inner Greta Thunberg was awakened. Outwardly I was the same person but inwardly my skin was green. I was going to *Hulk Smash* the system. The more excuses I heard them give the more determined I became to change the way corporations treat their employees.

“You see,” they said, “it’s all perfectly reasonable, HR just needs to have one standardized policy. Given how often IP acquires workers through acquisitions, you can’t expect them to assume the costly liability of perfectly compensating everyone’s benefits. That would be an unreasonable competitive handicap. But don’t worry they intend to make up for it by giving you a modified severance package (just don’t discuss this with anyone else at HP or anyone else at IP or anyone else period).”

Bribe me, bribe me go on and bribe me

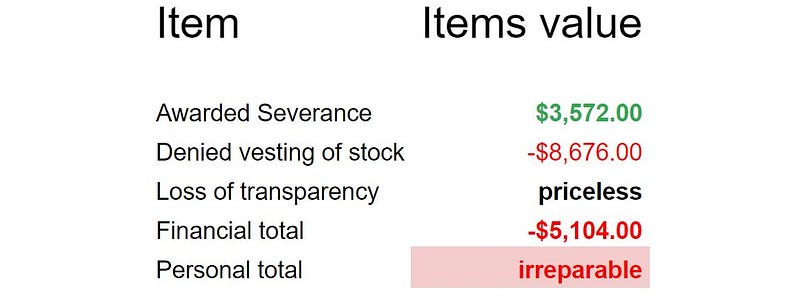

Summary: In my case my severance package amounted to a really lame bribe. When it was all said and done, I felt like I had lost more than $5,000 although on paper they gave me $3,500. For some people this is a lot of money but in severance terms this is peanuts. The math worked out like this:

For the sake of budgeting when large companies do moves like this, it may involve stages. Different employees may make the transfer at different times. I was included in the small initial “good” group that was receiving the “best” severance package. The difference I would receive was an additional $6,300 which was a lot. It was so good we really needed to keep quiet about it and not tell anyone because the people coming after us were getting substantially less.

Why this split up was done, I still to this day don’t know. I don’t believe this was some biased expression of favoritism. I think there are only so many ways you can slice a group of 65 people. HP was changing the rules on how they would award severance and you had to be officially severed by some date to receive a payment under the old formula. Not everyone could be severed by that date. So you could say that our managers were actually doing something really good by getting some of us a better package. Rather than criticize the managers I’d like to fix the system which is broken. It was the system which was treating people unfairly and it was the system that needed to be fixed.

I really didn’t like how people were being treated, but most importantly I didn’t want to feel like I was being forced to become an accessory to their deceit. It’s not like I was going to start asking everyone, “so how much did you get,” anyways. If you’re planning on not discussing something is it a big deal to sign away your rights to talk openly about it? I didn’t want to rock the boat and expose the others in the “good” group so I thought “why not sign?” This might have happened if it were not for the timing of the offer.

I had worked at HP for almost 2 years and 10 months when I received the offer. They wanted us to transfer in 30 days. I was less than 3 months away from vesting so signing meant I’d be out $8,600. Most importantly my health benefits would terminate and my providers would change. This meant my previously scheduled medical surgery would not be covered, which would result in medical bills exceeding $10,000. I wanted them to accommodate me and I said I was considering saying with HP-EDS to keep my insurance.

I insisted I couldn’t reschedule my surgery when in reality I probably could have. This meant they had to accommodate me by moving me from the “good” group to the “bad” group. This was me expressing my vote of no confidence in their s****y system. I thought that the switch from the “good” group to the “bad” group would not result in a financial penalty for me since being in the “good” group would mean I would be out my vesting in my 401(k). The difference was between $9,800 (good) and $3,500 (bad) given my years of service. But for some in the good group who had been with HP-EDS for 10 years or longer the difference was substantial.

So actually being in the “bad” group I thought I was going to get $2,300 more because I would keep my vesting:

- $9,800 + $0 = $9,800 (good group no vesting)

- $3,500 + $8,600 = $12,100 (bad group with vesting)

- $12,100 - $9,800 = $2,300 (difference made if I keep my vesting)

- $3,500 - $8,600 = -$5,100 (what actually happened)

What ended up happening was something I didn’t expect, the worst possible outcome. Our group ended up moving to IP when I was less than 1 week from my vesting date (see proof here). This meant no vesting and no good severance package. This caused an irrational mental split given how much time I had spent trying to see if there was any way I could save my vesting. I had come so close to actually keeping it, not having it felt like it had been taken from me. This is why being paid $3,500 felt like -$5,100. I kept thinking one of the following two things should have been true:

- Didn’t I earn at least a prorated portion of my vested 401(k) since I didn’t quit or get fired? Wouldn’t this be nearly all of the $8,600?

- If HP just treated us all equally wouldn't I had been paid $9,800 instead of $3,500? (I might have been convinced this would have compensated for the loss of the 401(k) money).

Bob didn’t choose to forfeit his years of service and I didn’t choose to forfeit my 401(k) vesting. So starting with the system mistreating Bob and ending with my experience this is how I came to hate the system known as severance.

But why blockchain?

Employers have employees over a barrel when it comes to employment negotiations. The only way we can effectively change how corporations treat their employees is to give them more leverage. The easiest way to give existing employees more leverage in these types of situations is to make it easier for them to walk away from their jobs. The most straightforward way of enabling employees to walk away from their jobs is to provide them with personalized individual severance accounts. These accounts would accrue with severance funds in the same way a workers 401(k) accrues with retirement funds.

You don’t need blockchain to provide this type of product. But, the thinking was that most employers wouldn’t be eager to offer this type of financial product to their employees. Why would an employer want to offer their employees a financial product that would give them less leverage in employment negotiations?

In 2015, before anyone really knew what blockchain was, it was the secret sauce that would allow you to circumvent the existing infrastructure of financial institutions. It would allow you to provide financial products directly to consumers that sought to buck the system. If powerful institutions tried to conspire to block workers from gaining more leverage then they could sidestep them. Blockchain would allow developers to build a financial product on a network that would be freed from the control and influence of those institutions. And most importantly it was “easy to code” a platform where anyone can just “hack something together.”

Did some people think we were crazy in believing this? Sure, of course they did. But, you also had Chamath Palihapitiya, a former vice president of AOL that later became an early executive of Facebook, saying emphatic things like this in late 2013:

Bitcoin and things like it are the equivalent of the red pill. We are entering a world of completely uncharted waters.

I own Bitcoin in my hedge fund, I own Bitcoin in my fund, I own Bitcoin in my private account. It is a huge deal, it’s a huge huge huge deal. What you’re talking about right now is for the next three to five years an unbelievably better store value. (Bitcoin) is gold 2.0 right … I can do the same thing with Bitcoin except now it’s outside the purview of every single government. It’s being used everywhere where you would think it would be used: Russia, Iran, Iraq, Egypt, Venezuela, Argentina everywhere where you have currency pressure. Everywhere where you want to basically shield your assets. And, then after that it’ll probably become a payment mechanism … you’re talking about trillions of dollars up for grabs, up for grabs right! And it’s just about trying something! I’m taking a few months to understand what the opportunity is and then hit the scene … the cool thing is it’s easier to know how to code. It’s actually useful in a way where you know you can probably hack something together yourself you can find folks and so this is the time where people should be trying really big crazy things.

Most importantly, the blockchain space had a visionary leader who was respected by the traditional financial system while he simultaneously defied the traditional financial system. He was a young kid wearing t-shirts with llamas and rainbows to events where everyone else comes dressed in suits. Charismatic influencers such as Vitalik stood as bridges between these two worlds and the way people treated him seemed to signal that a shift was taking place. Who wouldn’t want to be a part of this shift?

What blockchain felt like in 2015–2017

Blockchain felt like it was about regaining control. It felt like it was about redirecting power from the center to the fringes. When I wrote my first whitepaper, no one knew how difficult blockchain would be to build upon or how impractical it was to use. No one knew how expensive blockchain development would be or how long it would take to build a real consumer product.

Dynamis failed because I hadn’t carefully considered the complexity of the problem. After a year and several $$$$$ I learned my lesson. You cannot solve severance inequality without changing corporate culture. You cannot change corporate culture if you are an outsider. This wasn’t a technology problem.

If the problems related to severance were largely entrenched in corporate culture then what role could blockchain really play? But if you only have one tool in your toolkit with which to solve problems, your perspective as to the available solutions is going to be warped (Maslow’s hammer bias). Additionally, trying to get blockchain to DO something both new and useful for the average consumer was not something 99% of developers achieved in 2016, 2017, 2018 or 2019.

If I had known in 2015 that these amazing applications were several years instead of several months away, maybe I would have stopped to think more carefully about the consequences. Remember, we were told by smart people that it was, “easy to hack something together, anyone could do it (authority bias).” It took a few years for us to reevaluate these claims, but by then it was too late, we had “taken the red pill.” How many people, who had read the bitcoin whitepaper, would decide in the future to give up on cryptocurrency? Is it possible that innocent memes like this actually have an insidious effect? Who wants a return to normalcy if it means “plugging yourself back into the matrix?”

The entire blockchain community was an incredibly powerful echo chamber that was always offering up strong confirmation bias. The list of cognitive biases on wikipedia exceeds 50 in number, but one in particular seems to aptly describe many of us when we initially began our journey. Blockchain in 2016 was a Dunning–Kruger community. The effect is so well known, it has even appeared in popular culture, having inspired an opera song:

“Some people’s own incompetence somehow gives them a stupid sense that anything they do is first rate. They think it’s great. But… No, it’s not.”

Some people in the blockchain community were actual geniuses but most (myself included) were not. However this didn’t stop us from thinking we were geniuses especially after we made 100 fold or more returns from our initial cryptocurrency investments by the end of 2017. And so it was #hodlgang, #hodlgang, #hodlgang for investors and #BUIDLGANG, #BUIDLGANG, #BUIDLGANG for developers. Well, we were a gang until we reached the bottom in 2019. We couldn’t be bothered by people who warned us. They were just haters who failed to see the vision early like we did.

In terms of visionary ideas and energy, the blockchain community was clearly a better place to be than traditional fintech incubators. Outsiders such as myself had no way to participate in creating new financial products. Every fintech team needed at least one founder who had come from the financial sector. But if my goal was to build a tangible financial product for a consumer market I would have been better off avoiding blockchain entirely.

What blockchain feels like in 2019

Reality hits you hard bro. But blockchain is still here and ironically since the bubble burst over a year ago Ethereum has seen more powerful upgrades. With applications such as MakerDAO’s DAI and wallets such as Fortmatic, Ethereum has more potential than it did in 2015. I wouldn’t say that mainstream consumer apps are just around the corner but they are not more than 3 years away either.

Why I continued with blockchain even after Dynamis failed

The primary reason why it is difficult to innovate in the financial space is due to regulation. The reason why this regulation exists is to protect people from third parties who hold customer funds. The simplest way to innovate without breaking the law is to circumvent the banking system. This is because our modern banking and financial system is composed entirely of third parties who hold funds that do not belong to them (see graphics in this post). Blockchain is the only financial system that allows for direct custody of digital assets.

All you’ve ever known your entire life is the banking system. Trying to imagine another type of financial network is like trying to imagine living in another parallel world (hence the Matrix meme). Can you imagine a world as modern as ours but without banks? Go ahead and give it a good try. Give up yet? There is no way a cash based economy could ever reach the level of human development we see in the first world today. But what about digital cash? Digital cash operates separately from traditional banking. Could blockchain payment technology reduce our reliance on the banking system and change our relationship with the banks?

I’m not here to convince you that windmills are giants. CEO’s can walk away from failed companies with “golden parachutes” and workers can find that their job has been “downsized” with nothing to show for it. Severance inequality in America is not an imaginary enemy. Proposing a blockchain based insurance product for consumers in 2015 however was certainly a ridiculous solution. Many laughed as we labored for a mature ecosystem of products and services because they believed that our efforts were as vain as Don Quixote’s knight-errant adventures. Blockchain was after all, “a solution in search of a problem,” they said.

With every passing year however blockchain seems more like a solution to some very relevant problems. If Facebook launches Libra, is it conceivable that new insurance solutions will appear on Facebook’s platform? Could these solutions eliminate third party custodians? Do such solutions have the potential of having far less regulatory overhead? Will this reduced overhead and lower operating costs allow for new products to come to market? The answer to all of these questions today is a firm “maybe.” This is an improvement over the definitive “are you kidding me,” which is where most people believed the technology was in 2015.

Many believe that this technology opens up a parallel world of new financial products and services with lower total cost both in terms of regulatory and accounting overhead. All who’ve been convinced of this fact have decided to invest something of their time or money into blockchain. It’s just a matter of degree.

And that is how I ended up here, where I’m still working developing use cases that I believe are compelling.

{kind=link}