My Son’s Daycare Will Cost $65,886

Counting down the days until free, public kindergarten!

Daycare is one of the biggest expenses for young children. Even before the pandemic, families were struggling.

COVID turned everything upside down, to the point that many parents, mostly women, have given up on their jobs and decided to stay home with their kids.

And that got me to rethinking the cost of daycare.

The cost of watching your child during the day has to be paid one of two ways.

- You stay home and pay with your time.

- You work and pay with your money.

Regardless, until the child reaches kindergarten, that cost is required to be paid. In that way, the cost of childcare is much like a debt (okay, more like a personal unfunded mandate), which spawned the title of this article.

My wife and I both kept our jobs through the pandemic and both earn more than the cost of child care, so we’re choosing the second option. How much is that exactly?

Let’s break it down.

Breaking Down Child Care Expenses

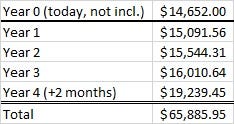

Let’s detail the assumptions then do the math.

- Our son is currently 17 months, which means we still have 4 years and 2 months of childcare until he starts public kindergarten in the fall of 2025.

- We send him to the local Goddard School year-round, and tuition is $1,221 per month.

- The current “transitory” inflation aside, let’s assume a 3% inflation rate until kindergarten.

Given all that, here are the annual and total costs.

That’s a significant amount of money.

Comparing Child Care of Other Expenses

Here’s the fun (or sad) part: comparing the cost of sending your kid to daycare to your other regular expenses.

Housing

I just moved from an apartment to a house, so I have two numbers to compare.

For the apartment, our monthly expenses were the rent, pet fee, two carports, washer/dryer rental, and a small storage unit for a total of $1,495

For the house, our monthly expenses are the full PITI payment for a total of $1,641.

- The total amount of $65,000 could easily allow us to make the acre our house is on a workable mini-farm, replacing a most of our groceries.

- The monthly amount of $1,221 is 82% of rent and 75% of our mortgage.

Transportation

We have two car loans of $330 and $344, for a total of $674/month. (Fun fact, both of the loans will drop off before our daycare obligation.)

We have a Subaru Outback and a Subaru Impreza, the latter we bought thinking we were only going to be a family of three. Not one year later, our son came along.

The thought of getting a larger vehicle to accommodate everyone is tempting, but the thought of getting another full loan for another five years for probably a higher amount is just…yuck.

- The total amount of $65,000 could get a brand new Chevy Suburban, with only a few bells and whistles.

- The monthly amount of $1,221 is 181% of our car loans.

Education

My wife and both have student loans, with our combined payments averaging $450/month, depending on the annual REPAYE calculation.

We’re also both on PSLF, which means we’ll only pay about half of the original value of our loans.

- The total amount of $65,000 could pay for more than two years of in-state tuition, room and board, and other fees at Indiana University. Scholarships and grants could make up the rest, resulting in no student loans!

- The monthly amount of $1,221 is 271% of our student loan payments.

The Takeaway

Child care is a huge expense for the first years of life is a huge expense, but one that normally gets relegated to the back burner of personal finance until it’s right up in your face.

If you are thinking about having kids, you need to include child care into your financial plan. It’s the cost of a shiny new car, your kid’s college tuition, or a large chunk of your mortgage.

What it is not is something to ignore.

Work it into your plan and avoid the sticker shock of daycare before your parental leave is up.

Related Stories

- COVID Destroyed Women’s Finances

- How I Still Have $135,000 in Student Loan Debt (Even After 21 Years)

- Falling Birth Rates Will (Probably) Destroy the Economy

Most Recent Stories

- Measuring Inflation is Damn Hard

- This is What Happens When You Irrigate a Desert.

- Parents: How to Add a COVID Career Gap on Your Resume.

- The K-Shaped Student Loan Story

- Breaking Down the Jobs Report — May 2021

Don’t miss my next article! Click here to get notified when I publish new material.

If you love the articles published in Money. Daily., then become a member of the Medium community and get full access to our full archives.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.