Examining My Income Over the Last 30 Years to Help You Become Better With Money

An era-by-era look at my earnings, money mistakes, and what you can learn from them

I live in constant conflict.

This isn’t a bad thing. It produces a sort of productive, even therapeutic unease. The conflict over exactly what and how much of my personal life to share in my writing.

In this article, I go about as deep as a personal finance writer can go into the personal details of their personal finance. (I like the word “personal).

While I have always written from a decidedly personal perspective, I made the choice to go as all-in as I possibly can early on in the pandemic. I hope sharing intimate details of my personal life, particularly my personal financial life, can help others.

Sometimes this feels self-indulgent. But it’s something I need to get past. I just don’t want to come across as an opportunistic guru (you know the type). I’m anti-guru and tread carefully to empower over preach.

Too much personal finance writing on the internet is devoid of personal experience. This is probably because most writers in the space fear not being taken seriously if they reveal their financial history, complete with the less than stellar parts. But they miss the point.

It doesn’t help to only hear from experts who operate under the guise of having never made mistakes or being millionaires. In fact, hearing from “experts” has become so lame it might not help much at all.

Writing on money works better if the source:

- Does a lot with little.

- Makes mistakes — and has flat out failed — but learned from those mistakes and is brutally and embarrassingly honest in articulating these experiences.

These are my superpowers.

I suck at a lot of things. But I’m good at doing a lot with little and blowing shit up. I used to blow stuff up and, as Elliott Smith wrote, fight problems with bigger problems. In recent years, I have come to acknowledge and isolate my mistakes, truly learn from them, and find ways to relate them to an audience hungry for actionable and empowering content about money.

All of this to say, I recently pulled up my earnings record with the Social Security Administration. It’s great and instructive fun to look back on how much money you made (or, at least, how much you made that had Social Security tax deducted from it). It’s also sort of scary to share this information in a society where talking about how much you earn is, by and large, taboo.

But screw it. I’m doing it. Hopefully, this breakdown of how much money I have made — and not made — over the last 30 years can help inform your personal financial situation, particularly if you’re younger than me.

A couple notes. In most years, I made more money than listed on my Social Security report.

For example, in a handful of years, I made considerably more money than the Social Security Wage Base. This is basically an income cap — that increases annually — where you stop paying into Social Security. Case in point — in 1998, Social Security lists my income as $68,400. This number was also the Social Security Wage Base for 1998. So, anything I made in excess of that doesn’t show up on my Social Security earnings report.

And, of course, not all money you earn as a freelancer shows up on these types of reports for a variety of reasons. I’ll leave that at that.

Stock market gains also boosted my income, particularly between 2010 and 2019.

1990–1994 / The Teen Years

For the record, all of these screenshots come from the My Social Security Account section of the Social Security Administration’s online portal. If you pay into Social Security, you should create an account. It also shows you how much Social Security you’re on track to receive at various “retirement” ages.

I turned 15 in July of 1990. I think I spent pretty much everything I earned in these years. It’s easy to criticize the choices your teenager you made. Too easy. It’s essentially revisionist history — or merely being too rear view mirror hard on yourself.

I mean, had I just taken 10% of my earnings in each of those five years ($3,028.40) and invested them in the S&P 500 starting in 1995, I would have had $15,885 by the end of 2019.

Doesn’t sound like much. And, while I can’t hold my teenager self to such a high standard amid the benefit of hindsight, that sixteen grand would have come in handy during the next era of my life.

1995–1999 / Just Starting Out / The Radio Years

I made most of my money between 1990 and 1999 working in radio. I had one of my best years ever in 1998 (when I was 23), surpassing the stated $68,400, which was 1998’s Social Security Wage Base.

A few lessons from this period of my life.

I took my first full-time radio job in Miami, Florida, when I was 19 about to turn 20. My salary — a whopping $26,500 a year. To do nighttime talk radio in one of the nation’s largest media markets. Short story — I got ripped off. They took advantage of my youth, enthusiasm, and paid me in sunshine.

Bottom line — don’t let anybody push you around or underpay you for being in your 20s. No matter what they offer, ask for more. Aim high. Only settle for slightly less. You don’t have to be older than 30 to negotiate. Thankfully, financial opportunity presents itself differently for a 20-year old in 2020 than it did in 1995.

Back to that $16,000. It would have been nice to have had that amount of money, or something close to it, socked away as a 20-year old living in an ultra-expensive city on a relatively meager $26,500 salary. Never underestimate the power of saving just a little bit of money. It can save you from a world of hurt.

Because we could also refer to this era as The Credit Card Years. When I moved away from home, with virtually no money saved and a crappy salary, I entered the toxic environment of financing my lifestyle with credit cards. I tell part of this story here.

Simply put, I started life on my own from an awful personal financial place on almost every level.

- I thought I was a big shot. Full-time gig. Radio personality. I felt entitled to live — and portray — a lifestyle I could not afford.

- I had no savings. Even a little bit of cash behind me — like, um, $15,885 — would have helped fill the gap between income and out-sized monthly expenses.

- I turned to credit cards. This triggered a decade’s worth of personal financial trouble.

- Because I had no savings and was in over my head, I couldn’t save during prime earning years.

This is where it starts to hurt.

Had I saved just 10% of my earnings in each of those five years ($23,680.50) and invested them in the S&P 500 starting in 2000, I would have had $57,947 by the end of 2019. Had I done this alongside the incremental and methodical investing I have done in subsequent years, I’d be in a better position today.

Here’s the math — investing $2,000 a month for 20 years at an 8% annual return with a $23,680.50 head start would have yielded roughly $1,255,694 between 2000 and 2019. Investing $2,000 a month without the $23,680.50 head start leaves you with $1,145,320.

The difference — $110,374 — doesn’t sound like a lot of money once you get past a million. However, it’s significant when you think about it in terms of paying your annual expenses. If you’re frugal, you can squeeze four years of a great life out of $110,000.

But, digress I do.

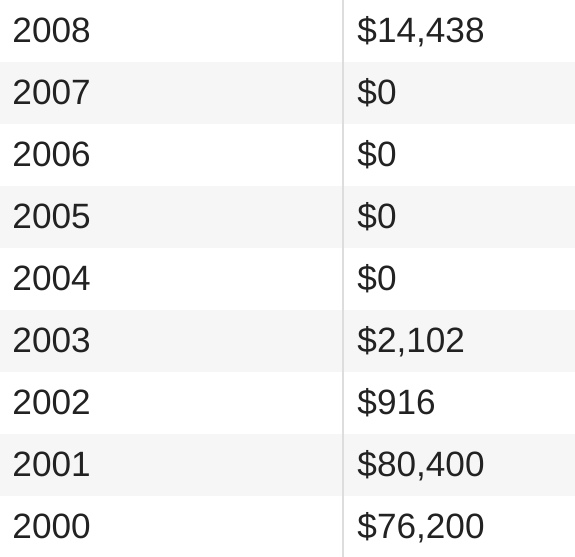

2000–2008 / The College Years

I spent four-and-a-half years as an undergraduate (2002–2006) and two years in graduate school (2007–2008). I also took out student loan debt during this time. Bad idea. I’ll leave that at that.

However, I also made smart moves, which helped mitigate the effect of taking on debt. I got out of radio in 1999–2000 and took a somewhat random sales job in San Francisco, just as Silicon Valley was booming (and about to bust). I eclipsed six figures easily in 2000 and 2001. I had ample cash saved, which allowed me to make the decision to quit working (for the most part) and attend college.

This period also represents the early stages of my thought process on not having a traditional retirement. It shaped my thinking that, instead of saving and investing for a linear trajectory into retirement, I will have a better life if I allocate income into various pots of money to fund expenses, wants, and different stages of life. You can read about that, in part, here and here.

From here on out, I came to fully understand it’s not about much money you make, it’s about what you do with the money you do make. I started to formulate my thinking and eventually became obsessed with an insanely low cost of living.

I started doing a lot with a relative little. And, at the same and right time, I kicked my investing into high gear.

2009-Present / Frugality at Its Finest

For the record, this applies quite a bit during these years:

And, of course, not all money you earn as a freelancer shows up on these types of reports for a variety of reasons. I’ll leave that at that.

I have never been more financially flexible in my entire life than I have been over the last few years. And it all comes down to an insanely low cost of living, the way I allocate my income, and the benefits of a seemingly endless bullish stock market.

I save/invest a vast majority of the money I make. Some months, I’m able to save/invest close to 80% of my income. It’s more powerful to do this on relatively light earnings than to save nothing or “just” 10% on larger sums of money.

For example, I’m on track to earn close to $100,000 in 2020. And I’m saving/investing at a consistent 35–40% clip, with some months approaching 80%.

I hesitated to post all of this personal information. I cringed a lot as I wrote this. However, without even knowing the reaction I’ll get, I’m glad I did.

We need to remove the cloak of secrecy around how much money we make. We need to shed the insecurity over the fear that somebody will look at what we made in a given year and think, “What a loser! That’s nothing. How can they be writing about money!?” This is, no doubt, one of my insecurities.

However, I’m also quite secure in the reality that it really isn’t about how much you make. It truly is about how you allocate what you do make. Even more important, every penny I take in above the annual figures you see here (from income above the Social Security contribution threshold, other income, investment profits, unexpected financial windfalls), goes to savings and investing.

It’s important to point out the role luck plays. I have been able to do what I do on what I make — and don’t make — each year, in large part, because of the stock market. With a couple retrospective radar screen blips, we have spent the last twenty years with a stock market that only goes up.

This fact shouldn’t make you overconfident going forward. It should make you (particularly me!) realize that you (me!) may have reaped the benefits of the bull market.

If the stock market hadn’t performed quite as well as it has, I’d be telling a different story than I am today. There might not be a story to tell. I might not even be doing what I’m doing — freelance writing — and living the way I’m living — a relatively financially flexible lifestyle — without stock market returns.

I more lucky — and privileged — than good.

I wish I made smarter choices in my teens and twenties, but I don’t regret not making all the right choices. The path I set out in those days afforded a whole host of experiences that made me the person I am today. I don’t think I would have been able to have had these experiences had I not made less than ideal financial decisions.

You can’t cherry-pick life events — discarding poor choices and leaving only the consequences of the good ones:

It’s our human tendency to want to grow, evolve, and experience all of the good things at the same time as undoing the “bad.” This is not realistic. And the “bad” isn’t necessarily “bad,” particularly if it basically had to happen to lead to the good.

Basically, if you want it all, you can’t have it all.

I blew money in my teens. I ran up credit cards in my twenties. I got my shit together in my thirties, thanks, in large part, to a raging stock market and a more prudent income allocation strategy. The first two sentences had to “happen” for me to be able to write the third. You get the drift.

I hope this journey through my earnings history helps. If there’s one thing to take away from it, it’s don’t listen to convention. Forge your own trajectory through life.

If you can manage to save/invest a little (or a lot) more than you spend, you’ll soon realize you don’t need to make as much as you think you do, particularly from traditional work. This alone — working less in the traditional sense alongside an insanely low cost of living — might be the number one facilitator of a great, financially flexible life, at least from my personal perspective.

The Mini Post-Grad Survival Guide

A 5-day email course with tips on budgeting, investing, and productivity for 20-somethings. Sign up for free.