Why a Max Out Your Credit Card Spending Spree Might Be the Best Money Decision You Ever Make

Consider the upside of carelessly throwing money away

We’re cognitive and emotional prisoners of our social environments.

Socialization influences, if not wholly dictates, the choices we make, particularly in the most intimate areas of our lives. Certain subjects become taboo. We don’t freely talk about them with strangers, neighbors, friends, family, and even lovers.

In my experience, this most often happens in two areas — sex and money.

Sadly, this article focuses on the latter.

However, in both areas, we do things behind closed doors we’d never discuss publicly. There’s significant stigma associated with myriad sexual practices and preferences. Something similar holds true with money.

Most of us have done or are currently doing things with money others would judge as reckless, irresponsible, or, at the very least, financially imprudent. This sucks because it’s these very things that can ultimately make us not only better with money but more comfortable talking about it. We learn a lot about ourselves when we take the so-called deviant route with our finances.

Try everything once. If you don’t like it, don’t do it again. If you do, take what you learned the first time and adapt it to future performances. This is one of my go-to mottoes in life. It colors the seeming insanity I’m about to spew with respect to credit cards and how they mediate your relationship with money.

I’m a proponent of not using credit cards at all. Like literally at all.

However, it’s unrealistic to expect somebody to never touch a credit card without experiencing firsthand how they function and the effects they can have — positive and negative — on their life and personal financial situation.

A blanket Say No to Credit Cards statement will work just as well as the failed Say No to Drugs campaign or as preaching abstinence to young people. It doesn’t work.

We all need to experience things — even if they’re potentially detrimental or socially frowned upon — to understand not only how they work and make us feel, but how to eliminate them from or most safely and effectively work them into our lives.

With this in mind, it might benefit a considerable number of people to open a credit card account, secure a $5,000 limit, max it out, then deal with paying it off. On the surface, this sounds like the worst personal finance advice you’ve ever heard. Take a second to try to get past the socialization that contributes to this reaction.

Think about the costs associated with this rash decision relative to the costs associated with the slower burn of financial irresponsibility that occurs over time. Spread out across months, years, and decades of life, this slow burn of financial recklessness morphs into a series of habits so deeply embedded in our day-to-day, we hardly even recognize them as deleterious.

I spent about 10–15 years of my life misusing credit cards. It started shortly before I moved from my hometown at the ripe age of 19. As one of my favorite lyricists, Rhett Miller of Old 97’s, wrote:

19 is not the age of reason

So I made dumb decisions, born out of both being dumb and (what I thought was) necessity. But also out of what I was taught growing up— moderation and individual responsibility.

Being “dumb” generally comes down to a lack of experience and attendant knowledge. You’ve never done something before. You’re introduced to it. The messaging that comes alongside these types of introductions usually sucks. More often than not, it’s counterproductive (see, e.g., Say No to Drugs, abstinence, don’t use credit cards at all, or just use them in moderation). So you dabble, armed with all of the wrong, self-defeating information.

There’s nothing wrong with dabbling. However, I prefer to dabble with purpose. With a vision of what you want to get out of the dabbling and where it can lead you.

My early dabbling with credit cards set off a vicious cycle. All I thought I needed to do was “be responsible” with credit cards. I never considered how hard that is to do. The psychology of credit card use didn’t enter the equation when I moved from a small town to an expensive city and could barely make ends meet on my $26,500 annual salary.

So I tried to do what I thought was responsible. Running up a modest balance to get things I actually needed (e.g., food) and things I thought I needed (e.g., furniture). I’d take the interest hit and pay these balances off over time, never getting in over my head. That is until I got in over my head.

You know how this goes. You have a balance. You can manage it. You even make more than the minimum payment each month. Maybe you pay off a balance, chalking up the interest as a small price to pay for the luxury of having secured more products and services than you could have paid for with cash upfront. You’re being responsible with credit cards!

Then you get a balance transfer offer in the mail. No interest, no payments for six months. You move your existing credit card balance to this new card. It feels like the sane and logical thing to do. It feels like an extension of the smart choices you tell yourself you’ve been making. You (think you) know the system. You’re using it to your advantage. It’s an extension of your financial responsibility and moderation.

Do I even need to finish the story? We know how it ends. The worst part is it begins and ends over and over again until the day comes when you finally learn your lesson. When you realize how much money you literally threw away over the span of, say, a decade doing the credit card dance, as if it was little more than the cost of doing life.

People don’t throw money away on rent. They throw it away on credit cards.

This was me, at least.

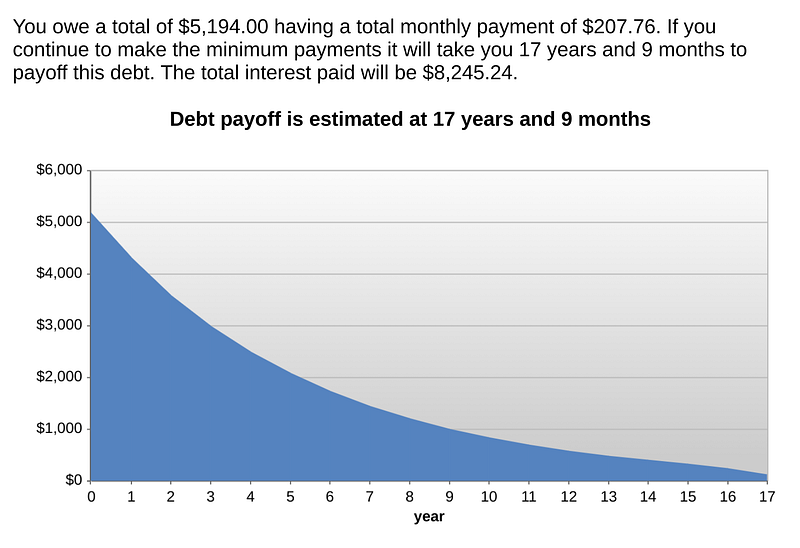

Looking back, I would have been way better off taking a credit card with a $5,000 limit and, instead of slow-burning it into the barely-noticeable-when-you’re-in-it vicious cycle, going on a massive shopping spree over like two days. Buying everything in sight then sitting with a $5,194 balance alongside an over-the-limit fee and 29.99% in unforgiving interest.

If only I would have looked at data such as this:

Going all-in on your first credit card might be better long-term guidance than thinking you can be responsible with multiple credit cards over time because so many of us are simply incapable of using credit cards responsibly as part of a broad personal financial plan.

Of course, some people can.

They Budget. Spend. Save. Invest. Pay off the credit card each month. No balance. Collect the rewards. Get a hotel upgrade. Blah, blah, blah. Sounds amazing in practice. But it’s a horrendous path to send most of us on, particularly when we’re young and relatively poor. Don’t let the people who are (so they report) good with credit cards influence you or, worse yet, make you feel capable.

Admitting you’re incapable — and finding out fast that you’re incapable — might be the best, most painless approach to credit card use.

When I do the math — and I’ll spare you the actual numbers, but, take my word for it, they’re bad — paying $8,245.24 in interest over 17 years and 9 months or scrimping to knock out the balance with out-sized monthly payments in a fraction of the time would have worked out better than “responsibly using credit cards” for ten years until I realized I actually wasn’t using them responsibly.

Paying the cost — or at least realizing the cost — when I was in my twenties and swearing off credit cards then would have been better than what I did. And what I did was, basically, the snowball effect in reverse. I let my balances snowball into something insurmountable, rather than beating them back to nothing using the same mathematical logic.

In most important areas of life, we want to protect people from themselves. We’ve been there, done that. So the easy and seemingly sensible route is to tell others:

I’ve made the mistakes. So don’t even go there. Say no to credit cards. To drugs. To sex. To anything I have gotten into trouble with.

We do this from a place of good intentions. Parents do this with their kids. And it is logical, except it tends not to work. I want my kid to make mistakes.

Unless I know it would cause serious, potentially irreparable damage — physically or mentally — I do my best to resist my parental instinct. I’m not going to protect my daughter from herself.

She needs to live. She needs to experience. She needs to feel the internal shame and unease that comes alongside failure. She needs to experience the euphoria that accompanies successfully taking an uncomfortable or uncharacteristic risk. It’s an incredibly difficult way to parent.

However, I’m convinced she’ll be better off — that most of us will be better off — when we’re given the opportunity to experience all aspects of life, even if it’s pretty certain we’re going to fuck up. Cloaking ultimately irresponsible or destructive behavior in the common and socially-accepted mantras of “just don’t do it” or “do it, but in moderation” often doesn’t end well.

Go do it. All the way. And do it hard.

It might wind up that you like it. And you keep doing it. And it works for you.

It might end up that the rush of indiscriminately charging $5,000 on a credit card over a weekend, then having to deal with the $5,000 balance for however long you’ll have to deal with it is the best fallout medicine.

Unconventional thoughts and approaches don’t always work.

It doesn’t make sense to go against the popular, mainstream grain of thought just for the sake of going against the popular, mainstream grain of thought.

However, sometimes it’s the smartest and most courageous thing to do. Sacrificing the short-term — to some degree — can bring quicker, more valuable lessons and better long-term consequences.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Consult a financial professional before making any major financial decisions.