We Ignore the Most Critical Part of the Rent Versus Own Debate

Renting isn’t throwing money away if it keeps you cash secure

I’m in the middle of redecorating my small studio apartment in Melrose Hill, Los Angeles, California.

I pay $1,342.72 per month to live in this 1924 building that looks — inside and out — like it could be in New York City. I almost moved. But I’m glad I didn’t. I love my apartment. And the price is right.

Paying rent keeps me sane.

It’s not that I’m excited about paying rent. I don’t look at it this way. However, I am passionate about the comprehensive personal finance plan paying rent plays a role in.

In this article, I aim to partially put to rest the rent versus own debate that, all too often, turns into an argument.

This is not something we should be arguing about.

Consider a handful of typical scenarios.

#1 Your dream is to own a home (A)

I hate it when people shit on other people’s dreams. You see it all of the time in personal finance articles.

A self-proclaimed money guru prescribes a rigid vision and tells followers there’s no other way around it — this is how you must handle your money. Bull. You can do absolutely anything you want to do with your money. That’s not the part we should be writing about. If I advocate anything, it’s to fold your dreams into a sane, logical, and sound strategy. And to empower people on their journey.

Millions of people dream to own a home. This doesn’t resonate much with me, but I get it. A subset of these people want it so badly, they’re willing to compromise on things like neighborhood quality to attain home ownership.

You see it all of the time on House Hunters (lol!). If you want something you can afford, I’m going to have to take you to neighborhoods outside of the one you brought me to as your first choice.

This might not work for you. Doesn’t work for me. But it works for countless others.

#2 Your dream is to own a home (B)

Simple. You want to own a home in your dream neighborhood. Full stop. You save every dime until you can do it. For many people, finally signing that real estate contract marks one of life’s greatest achievements.

#3 You move a lot

I know some people who move a lot. If you know you’re probably not going to be in a city for more than a couple to a few years, you might opt to rent. It’s just easier.

You make the rent or buy decision on the basis of your prevailing lifestyle — dictated by things such as work and personal preference.

#4 You’re me (or something like me)

Then you have people like me.

I live in an ultra-expensive real estate market. I’m not willing to compromise much, if at all, on neighborhood or housing style. There’s no way I could find a home in Los Angeles within this context for much less than $1 million.

Because I would refuse to take a creative mortgage product, let’s put my down payment — and related upfront costs — at somewhere between $100,000 and $200,000. For the sake of argument, let’s call it $100,000.

The thought of saving that much money, then turning around and spending it absolutely, unequivocally terrifies me.

I know. I’m not spending it. I’m investing it. But I don’t look at it this way.

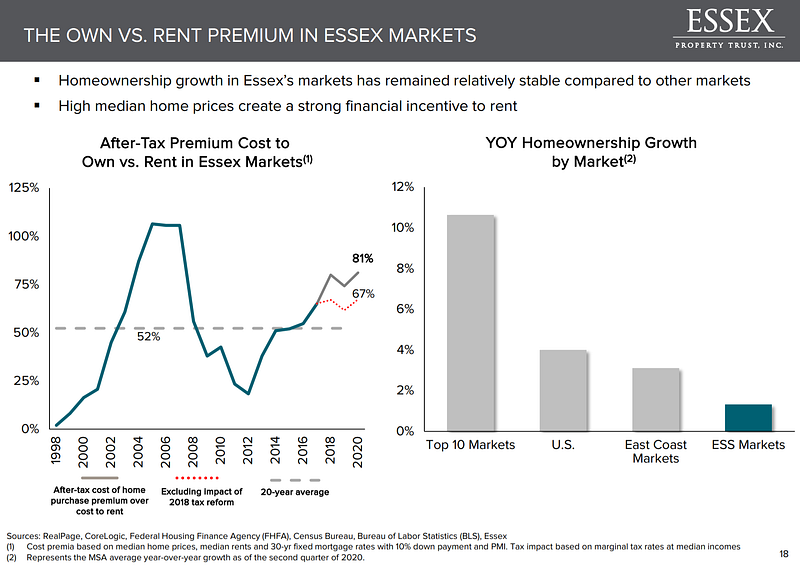

This is the part of the conversation personal finance writing tends to leave out. The psycho-emotional component of the money decisions we make or choose not to make. Sometimes they’re irrational. In my case, the choice to rent might make perfect sense, especially if you believe Essex Property Trust, a company with a vested interest in renting high-end apartments:

You pay a premium to own in Southern California, Northern California, and Seattle. As Essex says, there’s “a strong financial incentive to rent.”

However, I don’t present this data to “make my point” that renting trumps (ugh!) owning in Los Angeles and other expensive places. Remember — we shouldn’t be arguing over this! I present it for the opposite reason.

If it was my dream to own a home, I would not let this stop me. I’d save my money. I’d find the perfect house in my dream neighborhood, and I’d buy it. And, just as I do while renting today, I’d fit the apparently less attractive option (according to a company that rents apartments!) into a sensible personal finance strategy.

In other words, I’d make it work. More importantly, I would make choices in other areas to compensate for the apparent premium I would be paying to own a home in Los Angeles over rent an apartment. This is exactly what I do now in the opposite direction.

I maintain a low rent payment — in a rent-controlled apartment — so I don’t have to worry about having this out-sized monthly obligation hanging over my head for the rest of my life. I do this amid an insanely low cost of living, which tops out at around $2,500 a month. I’m working to lower this number.

I keep more than ample cash on hand in an emergency and other funds, so I feel cash secure. I would never spend — or invest — this money on a mortgage down payment. Money sitting in home equity would feel so far away from me. And, practically, it is. If I needed the cash, I couldn’t access it because I need a place to live. (Don’t tell me to take out a home equity loan!).

I’d rather take the money I have left — after ensuring I’m cash secure — and invest it in dividend-paying stocks. This is where I choose to invest a bulk of my money. Not in a house. I’ll forgo the appreciation we see in frothy housing markets in favor of the aforementioned cash security. I’ll opt for the power of compounding and the exponentially growing income stream this style of stock market investing brings.

It’ll take me a while to reap the fruits of this income stream (i.e., live off of it, all or in part), but it would also take me a while (probably much longer) to see the benefits of real estate price appreciation. Because, again, I need someplace to live. Being house rich would not work for me.

If I had a $500,000 or $1,000,000 fixed annual salary, I might view the math differently.

But I don’t.

I don’t think like an economist. But I know how to think like an economist.

I’m presently obsessed with economic psychology. The branch of psychology that “deals with decisions (individual or interactive), preferences, judgments, and factors influencing these, as well as the consequences of judgments and decisions for economics and society.”

This is the direction personal finance needs to head. Looking at what motivates people to make money decisions others simply can’t make sense of.

The rent versus buy argument is a good place to start. However, the ideal introduction to this line of inquiry would be to stop arguing about it.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.