Everyday Economics For People, Chapter 7: Macro Economics

“Macro” is just the complement to “micro,” so as you would expect, macroeconomics is a discussion of factors that have influence throughout the entire economy. Before we proceed, though, let’s define “the economy.” This is a very slippery subject, and confoundingly hard to measure clearly.

One way of measuring “The Economy” is the dynamic duo “aggregate demand,” which is the total amount consumers in an economy could potentially spend in all markets combined, and “aggregate supply,” which is the total amount producers in an economy could potentially produce in all markets combined. We sort of have to guestimate the potential curves, but the actual present level is often measured by something called Gross Domestic Product (GDP), which is measured as the total amount of money paid for all goods and services. Note, this tells us only where we are on the aggregate supply curve; not necessarily where we could be if we change various conditions.

Another present-level measure, Gross National Produce (GNP), sums the total income of every person in the nation, and can include income generated internationally. This measure is neglected given its relevance in the age of global corporations, but has its limitations anyway, especially from a public policy perspective, since much of GNP is determined by laws outside of direct U.S. jurisdiction. GNP and GDP usually are pretty similar to each other, each missing some information from the larger picture.

Yet another measure, and one to which I will refer as “the stock market,” is the combined present market value of all the publicly traded stocks in the nation. This provides a more predictive measure of national production, as it bakes in estimates for aggregate supply and demand, investments, debts, and other assets, and is therefore often able to forecast future up and down trends in GDP. However, the stock market only includes the values of publicly traded firms, so it has that and other limitations as well, such as incomplete information, speculation, and gaming. Also, if you know about liquidity, you know that spot prices are limited at best. I don’t want to get into it, but basically the price of stocks falls as you sell them, so their present valuations are not accurate. They could only be sold for half as much as they are valued at, on a good day, typically, but it depends on many things.

Then there is the matter of the underground economy, which includes goods and services that are hidden from account because they would face legal consequences, as well as self-produced goods and services that people do for one another as part of family, community, etc., and these must be estimated and tacked on to the GDP and GNP estimates (but are typically ignored, instead).

Okay, I know I said I was going to define “the economy” but as you can see, we got only sort of a blurry outline of what it is. However, that’s definitely enough for our purposes.

So, let’s talk about the macroeconomic factors that have the biggest impact on aggregate supply and aggregate demand, and thus on “the economy” as a whole. As you will recall from our earlier discussion, the most important factors of demand for every good are the size of the population and the spending power of that population. This means that anything which indicates an increase or decrease in the size or spending power of the population will have a corresponding impact increasing or decreasing demand for every single product in the entire economy. Every single product in the entire economy. Every single product. Holy moly.

These days, populations are fairly predictable, as most people die in their old age, and so future demographics are largely known many decades in advance of when they occur. It must be emphasized that this does not mean demographics are stable. Indeed, the uneven distribution of population caused by the oddly large Baby Boomer generation has resulted in dramatic changes in the age composition of the consumer market over the last 40 years, and will continue for the next 20–40 years, after which the large Millennial generation will have a similar trajectory. Despite being known decades in advance, these demographic shifts can have dramatic impacts on both aggregate supply and aggregate demand.

In contrast to population dynamics, consumer wealth, income, and spending dynamics are extremely volatile and variable. There are many factors which can affect consumer spending power. Basically, anything that increases or decreases how much people have to spend. The most obvious are:

- Rates of labor force participation (not unemployment), as this determines the size of the market of people with income;

- Total income and liquid wealth of all consumers, as this determines the amount that they can spend without consuming investments;

- Sufficient distributions of income and wealth among lower percentiles to allow discretionary spending, as 1,000 people with $1,000 each will spend more than 10 people with $100,000 each;

- Marginal propensity to consume at each income level, which is the number of cents from every dollar a person spends instead of saving. A high rate of spending means higher demand. This is related to the one above, but distinct.

- Government subsidies, as this is effectively additional purchasing power potentially borrowed from the future;

- Taxation, as this reduces the amount of money people have available to spend or raises the prices of things they would like to buy; and

- The general availability and cost of credit, as these determine how much extra purchasing power consumers may borrow from the future, and how much they are deterred from doing so by interest payments.

Changes in any of these above-listed factors will have predictable results on aggregate demand in a given economy. There may be other factors I have not listed, but you get the idea. If it increases the size or spending power of the population, it increases aggregate demand. I have emboldened the three bottom ones, as these represent fiscal and monetary policy, which are arbitrarily determined by government institutions, and can easily change at a whim. Although governments can influence the upper four, they can only do so indirectly.

There are similarly many factors which can affect aggregate supply. The most obvious, though not a comprehensive list, include:

- The amounts of liquid wealth available for investment, as this will determine how much supply could expand to capitalize on opportunities;

- The cost and availability of credit, again, because this will determine how much supply could expand to capitalize on opportunities;

- The number of potential producers available, because this will determine how much supply could expand to capitalize on opportunities;

- The barriers to entry throughout the economy, because this will determine limits on potential producers entering and affect opportunity cost analysis for existing producers;

- Taxes, because these cut into profit margins and discourage would-be producers from participating;

- The prices of the factors of production, because these determine the minimum prices at which producers would be willing to produce;

- The distribution of wealth among people, as higher concentrations of wealth among a few people result in a higher percentage of saving and investment, allowing greater capacity for supply to expand to capitalize on opportunities; and

- The productive skills of the population, because the greater productive skill the population has, the more cheaply they can take advantage of opportunities that arise.

Once again, I have emboldened aspects which the government itself can set directly. Changes in any of these factors will have predictable results on aggregate supply in a given economy. Usually, there are so many factors moving in different directions and with different magnitude that predicting short term equilibrium changes in the price of any specific stock or asset is difficult. However, if enough of these factors line up in the same direction together over a sustained period, the long-term direction of the overall economy becomes quite easy to predict. Furthermore, there are systemic inevitabilities that cause these factors to align with each other over the long run!

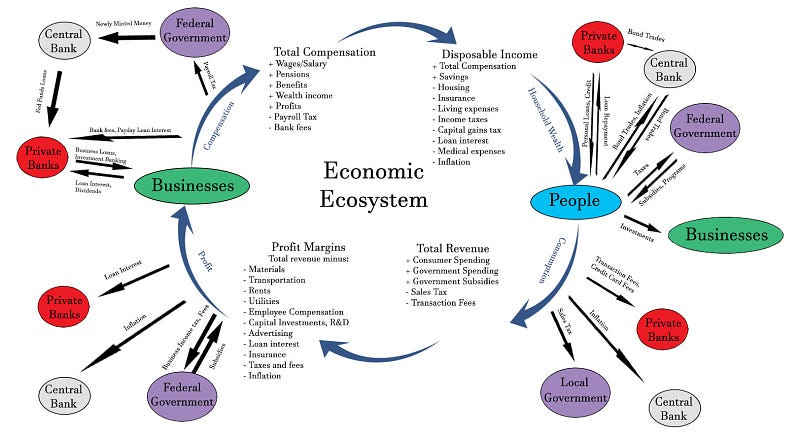

The overall system looks like this:

As you can see, there are a whole lot of different moving parts, but when it is broken down visually like this, it’s fairly easy to see how a change in one of these would impact the overall flow in the long run.

For example, businesses stop receiving investment funding from people, banks, and the government, then they will stop paying out as much in wages. That will reduce disposable income of people, which will reduce consumption, which will reduce revenue, which will reduce profits, which will further reduce the ability of businesses to hire and pay employees.

As another example, If the central bank lowers interest rates at which it lends to private banks, those banks may choose to lower rates or standards at which they lend to consumers and businesses, increasing employment and wages as well as consumer credit, which will both increase consumption, increasing profits, increasing employment, etc.

Note that the effect of these cyclical impacts is reduced with each turn around the circle, so they don’t go infinitely. They eventually fizzle out. Okay, now we can talk about economic boom and bust / expansion and recession cycles!

Due to the financial liability involved in predicting asset prices, professionals in the field of Economics tend to understate publicly the level of confidence with which they are able to predict macroeconomic events. As a consequence, there is a systemic misrepresentation of “the economy” as being unpredictable, because nobody wants to risk financial responsibility for being wrong and thereafter sued or otherwise attacked by very wealthy investors who lost money listening to them. On that note, please recognize that this book is purely for entertainment and informational purposes and does not constitute financial advice.

What is an economic cycle? Well, take a look back at that economic ecosystem. Put simply, businesses require that people spend money to hire anyone, and people require that businesses hire them to spend money. This creates something of a Catch-22 if businesses ever stop hiring or people ever stop spending. The market tends to have “cycles” during which employment or consumer spending recedes, causing the other to recede as well, causing the first to recede further, etc., causing a cascade of decline in employment and spending. This phenomenon is commonly called a “recession” or a “bust.”

The reverse is also possible; if businesses start to increase employment, or consumers get more money from somewhere, that increases consumer spending, which increases profits, which increases employment, etc., causing a cascade of economic growth. This is called an “expansion” or a “boom.”

Screenshot from Google.com

Those are some examples of major geopolitical and/or economic events that caused mass declines in economic growth for sustained periods. As of this writing, it appears that we are in the very, very early stages of a deep recession.

Anyway, basically, economic cycles work like this: employment and investment push each other in the same direction in a positive feedback loop, and external pressures that rein them in (e.g. competitive rise in costs of rent, workers, finance, materials) accumulate too slowly behind to prevent large swings of momentum from being generated. The details are as follows.

When somebody wants to engage in a business venture, they need to have starting capital. That means that either they need to have a lot of wealth sitting around, or they need to convince wealthy investors to front their initial costs, or they need a loan from a bank. Thus, new business investments occur when people have money to invest on their own, or when credit is cheap and available.

Almost all investing is done by very wealthy people. This is because anyone who is not very wealthy will probably buy a home first, and then maybe another home, and then they will be fairly wealthy. Point is, “little people” rarely invest, and even if they did they don’t have much and they don’t think about timing, so they are easily dwarfed by conglomerate investors.

In order for wealthy investors who own many businesses already to be interested in opening new ventures, they would need to perceive that consumer spending power is not currently being served or is on an upward trajectory, in order to support additional production. Otherwise, they would simply end up competing against their own existing productive apparatus.

Credit prices are determined arbitrarily by the Federal Reserve Board of Directors, although they do attempt to justify their decisions using market data and research.

Okay, so now that we have the major players, we can talk about why the market cycle occurs. First, we’ll talk about the cycle before the existence of central banks, and then we can talk about the role the central banks play.

It works like this: imagine we are at the bottom of a recession, wherein unemployment is high, wages are low, peoples’ savings are depleted, and banks are very cautious about lending money. In this situation, it is hard for new businesses to get going, because so many potential customers already can’t even afford all of their basic needs. This discourages investors from putting money into anything, because there is little reason to expect a profit. As a result, no new job positions open, and so unemployment remains high and demand remains low, keeping unemployment high, keeping demand low, etc.

This may appear to be an infinite death-spiral, but it is not. A few things happen during this time that eventually turn the tide. The most important thing to happen is probably that the last person from the wave of mass defaults finally defaults, and the banks stop hemorrhaging money and stabilize. Once this process of default and bankruptcy is complete and banks start to reaccumulate spare funds from reliable debtors, they can once again loosen up their requirements for new loan applicants.

Another important thing is happening is the total depletion of the wealth and income of the population in general. Yes, of course this is important in terms of the dramatic human cost (a crucial social discussion very far outside the scope of this particular book), but it is also very important for macroeconomic calculations. Firstly, economic desperation among the population creates a labor market that is very favorable to employers. Additionally, as normal people lose all of their spending power, investors gain more and more. For example, when a landlord has evicted half of their tenants, they will eventually have to drop rents, which lowers the market value of the property. For an investor looking to buy a property, this is an ideal moment. The same applies to commercial properties: because there aren’t many customers, each store produces relatively low revenue, which drives down rents and property values, creating ideal conditions for an investor to swoop in at low start-up costs.

It doesn’t stop there. All of the costs of production are very low during this period, because there aren’t many businesses competing for them. In many cases, factories are not producing at capacity, and can easily expand to fill new large orders without raising prices. Raw materials are not being purchased, and sit in silos and warehouses waiting for buyers to put in orders. Equipment is being liquidated by bankrupt failures at bargain basement prices. An army of truckers is sitting by the road waiting for something to ship.

At a certain point, the very bleakest moment of all for the general population, when everything appears that it will never improve and that capitalism has failed — at that moment, the biggest risk-taking capitalists will finally buy up all the liquidated productive capital again and start hiring desperate, discouraged workers to operate it for them at low wages.

As they do so, more cautious investors take note. They realize that the earlier actors have taken out loans and invested large sums of money, much of which will go toward wages, which of course means that there are about to be new customers with money to burn. So, additional investors begin putting money into starting and expanding business ventures. And banks, noticing the same trend of low risk and high reward, loosen their lending standards to ensure that they get a nice cut of the coming expansion.

As more and more investors pour money back into employment, they create the conditions of rising demand that draw more investors in, driving up employment, driving up consumer demand, increasing the incentives for further investment and employment, etc. Once again, we have a situation in which investment and employment create a positive feedback loop with one another, this time pointing toward economic growth forever. As you have guessed, there will eventually have to be some kind of external pressure to stop the feedback loop. Let’s talk about those pressures.

One of the most important is the general average increase in the costs of production as production expands. As more and more businesses start trying to take advantage of the increasing consumer demand, they run into a wall: there aren’t enough employees to go around. At a certain point, basically everybody looking for a job has a job already. Now, because consumer demand is so high at the time, it is very important to have workers in order to take advantage of that demand. So, businesses have to compete with each other for employees, which means that they start paying higher wages. Additionally, eventually every storefront is occupied, and they need to compete with each other for physical space, meaning that rents and property values rise. Additionally, they need to compete with each other for raw materials and intermediate goods, and cleaning services, and equipment, and utilities, and advertising space, credit from banks, and basically everything. Each new entrant to the economy increases average costs for everyone who was already there before them, reducing average profits, for some perhaps below the point of financial solvency.

Because the potential revenues are so high during this boom in wages and employment, businesses are willing to take big risks to try to carve out a chunk of the pie. That risk translates in the real world into high interest loans. As the upward “bull” phase of the market cycle reaches final maturity, smart investors notice consumer demand peaking, and start selling everything rather than putting more money in, forcing businesses to seek loans exclusively from banks. Simultaneously, banks begin to recognize the precariousness of new loans, and the reluctance of private investors, and so demand higher and higher interest payments and collateral insurance to offset the risk of loaning to such speculative ventures. Smaller entrepreneurs, emboldened by the recent successes of others, continue taking bold risks, but in increasingly overcrowded economic conditions and with expensively borrowed money.

The predictable result is that a lot of start-ups poached workers with wages far too high on the expectation of continually increasing consumer demand, and instead end up competing against one another for razor-thin profit margins as new investments largely stop, and employment stops rising, and consumer demand stagnates. If they are lucky, these new, super-hyped businesses may have a flash of glory before collapsing in on themselves, unable to make debt payments. And, as they shut down, the banks and investors who funded their gamble take a big hit, and are forced to be much more cautious about lending money.

Once the first major wave of businesses fails, there is a sudden collapse in consumer demand, because so many people just lost very high paying jobs, and are unable to find new work. As their wages disappear, they stop buying all the stuff they had been buying, and there will be a second wave of businesses failing, with another corresponding collapse in consumer demand, and another corresponding hit to banks, who will again have to tighten their credit requirements, stifling business investments and consumption even further.

Once this second wave has broken, it becomes clear to the vast majority of investors that the market is now entering the downward “bear” mode, in which prices of goods and thus values of stocks and property are likely to continue to drop, so investors start unloading all of their market-based assets in favor of financial or other assets which are unlikely to depreciate in the same way. This has the effect of closing down even more businesses, reducing employment even further, reducing consumer demand further, cementing the downward spiral once again.

And, once again, this spiral will continue until banks are refusing to loan money to anybody, the typical worker has been drained of almost all of their wealth and is desperate for a job, commercial landlords are desperate for tenants to fill their empty storefronts, and factories and mines and farms and truckers are desperate for orders to fill, at which point the most confident and informed capitalists will once again “save the day” and become fabulously wealthy in the process as they put all the money they made selling assets at the top of the market back into assets now at the bottom of the market.

As you can see, this is really not that complex or mysterious. It is, quite simply, the result of misguided, jubilant overinvestment and overspending during boom years and overly cautious underinvestment during bust years. That is, unless it’s a conspiracy! Ha. Investment decisions have self-reinforcing medium-term feedbacks, and long-term negative feedbacks from external factors, inevitably resulting in wild swings to the extent that external pressures lag behind the positive feedback loop of investment and employment. You will also notice that this is a very lucrative arrangement for wealthy capitalists, and a lousy arrangement for working people. Working people noticed this, too, and they attempt to use the federal government and the central bank in order to stimulate the economy during recessions. The problem, generally described, is that working people do not demand that these institutions attempt to use those same tools to restrict the economy during booms.

I won’t spend too long talking about the federal government, but I will summarize their actions generally as being far too optimistic about each upward economic swing and far too pessimistic about each minor downward swing. Thus, they raise taxes far too late and too little to take advantage of economic booms, and they waste funds on stimulus for minor downward corrections. When major downward corrections occur, they have to borrow large amounts of money to stimulate growth again, and when growth does occur, they are again too slow to raise taxes to pay off the debts they accrued. The federal debt now stands at a record $26 trillion dollars — significantly higher than total GDP — and we are already likely at the end of this growth cycle, and so likely to increase deficit spending dramatically in the coming recession years. Rather than raise taxes during the moment of highest revenue the last few years, we cut them in 2017 in a vain attempt to continue growth indefinitely. It’s like using up your rocket fuel to propel yourself up over a cliff instead of saving it to counter gravity as you inevitably fall. That was before the Coronavirus pandemic shutdown.

Now we can discuss the role of the central bank: in our case, the Federal Reserve. The Fed has a dual mandate: to maintain low unemployment, and to maintain low inflation. As it happens, inflation and unemployment typically move in opposite directions from each other. That is, when there is lots of funding available, entrepreneurs are more likely to take out loans and hire people, reducing unemployment, whereas when money is tightly controlled, entrepreneurs cannot qualify or choose to avoid paying for loans, so they don’t hire anybody, so unemployment tends to increase. So the job of the Fed in practice is to increase inflation when employment is down and to decrease inflation when employment is up. It achieves this by changing the rate at which it loans to banks (lower rates = more investment = more employment), and by changing the yield on treasury bonds which it sells (higher yields = less investment = less employment). Important note: the Fed is attempting to change employment indirectly by influencing potential investors through potential financiers. If either the investors or financiers do not behave as planned, then the Fed’s actions will not have the intended impact.

Okay, so imagine that we are in a recession. The goal of the central bank, if it were run rationally by long-term focused economists, would be to cushion the descent and encourage an early recovery from the bottom before having to wait for the costs of investing to reach rock bottom. They would achieve this by buying bonds and decreasing the interest rate, increasing the money supply and hopefully therefore increasing employment.

Importantly, after the recession has clearly ended, the central bank should immediately begin reducing the money supply in order to discourage over-investment, as well as to give the bank greater leverage to reduce rates during the next recession.

When the bull market is clearly moving into a range where a downward correction is likely (i.e. it has moved too far above its long term moving averages), the central bank should encourage the correction by increasing rates even further, stifling exuberant growth and building up additional leverage to protect against calamitous bear market conditions should prices fall below long-term averages. This would decrease volatility by preventing the peak from growing as far out of rationality, and it would also prevent the collapse from being too deep, as the Fed would then have vast leverage to increase the money supply without inflicting massive inflation.

Now that we’ve talked about the ideal version of how central banks could operate, let’s talk about how they actually do operate. The first thing to understand is that although the central bank is run by a board who are appointed, not elected, they do ultimately have to answer to Congress, who can impeach them at a whim with a majority. Thus, the central bank is, to a large extent, bound by political considerations.

Starting in the 80’s, this has manifested as the Fed overreacting to medium-term corrections, when politicians are panicking ignorantly about this potentially being the next Great Depression. Rather than allow the market to correct for overexuberance with medium-sized movements, the Fed ends up trying to stimulate growth while stock prices are still above their long-term moving averages.

The predictable result is that the central bank ends up depleting all of its leverage attempting to “correct” each downward swing to maintain infinite upward growth, which is obviously impossible. Naturally, this means that when the real long-term downward correction finally arrives, it has been pushed back repeatedly already by misguided attempts at stimulus, building pressure, and now both the federal government and the central bank have no more stimulus to give when the crash actually begins in earnest.

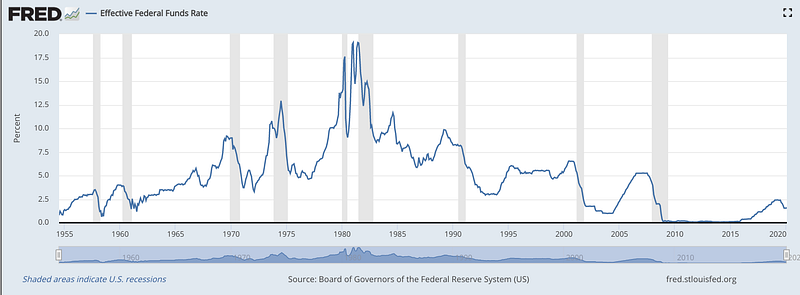

In the 2008 recession, for example, rates were already so low that the Fed had to begin experimenting with a new concept obfuscatingly named “quantitative easing,” which is a fancy way to say that they pay banks money to borrow from them, instead of charging them interest. That is, they began “charging” negative interest, allowing them to reduce interest rates below 0% to continue increasing the money supply in a way they felt they could control. Amazingly, the experiment was a success and the banking system was preserved and recovered from the housing bubble burst of 2008.

As of this writing, the interest rate is at a mere 2.5%. Oops, it was lowered between drafts of this book, and now stands at 2.25%, despite stock values being still at record high levels. Although 2.25% is much higher than it has been over the last few years, this means that they can only lower it by 2.25% before they start moving into murky, uncharted financial territory of negative interest loans. If they had increased rates more along the way up to record high stock price levels, where we currently sit, then they would be in much better standing to address the impending market correction. They are not in good standing, nor is the federal government, which already stands 22 trillion dollars in debt. Oops, again between drafts of this book, things changed, and because of the pandemic response, we are already at 0% interest, with a historically large Fed balance sheet, and the federal government is now 26 trillion in debt.

So, that’s sort of a long way of saying that central banks and central governments both focus on the medium-term, which causes them ironically to exacerbate rather than ameliorate long-term stock market volatility. There is no reason to expect that stock market volatility is going to disappear any time soon. Indeed, it might be approaching its most volatile moments in history! Who knows what will happen to stock values of international, U.S.-based firms when the dollar starts shedding value? (I say “when” because the only way for the dollar not to lose its value would be for the U.S. to pay down its debt to a manageable level prior to the next major recession. If we are unable to achieve this, then either taxes will need to be raised during the recession to make interest payments, reducing the spending power of each income earner and U.S. production — resulting in a weaker dollar — or money will need to be printed — resulting in a weaker dollar — or the U.S. would default on its debts, destroying its access to future lines of credit, forcing it to print money to cover deficits — resulting in a weaker dollar.) Okay, once again, that topic is beyond the scope of this book, but the point is that the federal government and the federal reserve are each not operating in ways that are solvent in the long-term, and each of them encourages the long-term boom and bust cycle.

This book is not about how we should change those institutions so that they think more appropriately in the long-term, because that would take collective action of probably about 100 million people or more. I’ll write that one later. This book is about how you, the individual with no real money worth mentioning, can minimize the amount you personally are taken advantage of in the dystopian capitalist environment we find ourselves living in. You know the waves are coming, and there’s nothing you can do by yourself to stop them; here’s how to surf.

Section I: Building Wealth Through Financial Habits

Chapter 1: Credit and Interest Chapter 2: Rent and Ownership Chapter 3: Budgeting & Reducing Expenses Chapter 4: Bargain Shopping Chapter 5: Optimizing How You Allocate Your Productive Time Section I Conclusion

Section II: Taking Advantage of Factors Bigger Than Oneself

Chapter 6: Crash Course In Microeconomics Chapter 7: Crash Couse in Macroeconomics Chapter 8: Why Businesses Sometimes Sell At A Loss Chapter 9: You, The Savvy Consumer Chapter 10: You, The Savvy Producer