Everyday Economics for People, Chapter 1: Credit and Interest

Mental Heuristic #1: Never pay for consumption on credit.

The most important aspect of your financial health is how much money you are bleeding away to interest payments every month. Think about it this way: do you think you are saving money if you buy something 10% off? It depends. If you bought it with a credit card and ended up paying 12% in interest, then you didn’t actually get it 10% off. For example, suppose you buy a $10.00 item for $9.00. You end up paying 12% interest on $9.00, which is $1.08. Add that to the $9.00 you spent, and you paid $10.08 for a $10.00 item. If it hadn’t been on sale, you’d have paid $11.20 for a $10 item!

If you buy something with credit and allow your debt to accrue interest, then it’s like putting negative coupons on every purchase you make. You could easily be paying 20–30% extra for everything you buy if you pay with credit and maintain a credit card balance. In many cases, if you allow your debts to build up even just for a few years, you can end up paying more than double for everything you bought.

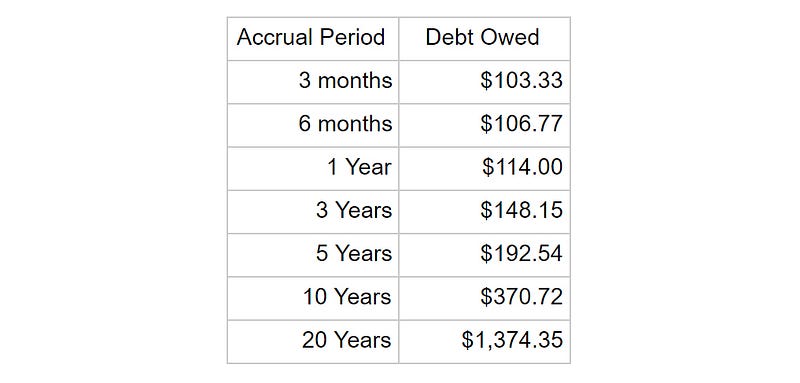

Let’s just take a quick look at the numbers. As of this writing, the average interest rate on credit cards in the U.S. is about 14%. Here’s a table showing how much you end up paying if you hold $100 of debt for different lengths of time.

Holy Grail in Constantinople! This is why usury was once considered a sin. Even just 3 months to pay off your credit card means you’re paying 3.33% extra on every single purchase. 5 years to pay off your credit card means you’re paying 92.5% extra on every single purchase. 20 years to pay off your credit card means you’re paying 13 times more money for every purchase compared with people who pay cash.

Okay, so these numbers are exaggerated, because this is only what would happen if you didn’t make any payments until the end, and it ignores inflation. Still, even if you just cover the interest payments, you add 14% to the price of every purchase you make each year. 20 x 14% is 280%, meaning you’d still pay 3.8 times as much after 20 years of interest payments compared with somebody who did not maintain a credit card balance at all.

Never buying anything on credit may sound like it takes a lot of discipline, but it actually takes much less discipline than living on credit. You see, if you choose to live on credit, then you always have the option to spend more money. That option presents you with hundreds of questions per day regarding how much debt you are willing to take on now in order to have some this or that. Making the right choice not to spend too much in each of hundreds of decisions is exhausting, and advertisers and sellers rely on you succumbing to decision-fatigue, because then your human bias is just to grab whatever thing you want and go home. So, kind of like Chinese water torture, they each tap harmlessly away at you until the persistence of their assault breaks you and you “live a little” or “spoil yourself” by stealing from future you.

If you start out with the mentality that you cannot buy things on credit unless you can instantly pay the balance (for that 1% “cash back” discount), then you don’t have to make those kinds of decisions. Instead, your decisions are based on what money you have available, and which things you want most out of what you can afford. This is a much smaller set of decisions, and it’s mostly the same decision every day that you can make automatically, and your bias is going to end up being to save up money so that you have easier choices later.

What I am telling you right now is that there is much more to this strategy than simple mathematics (which is already sufficient to make it a good idea). I assume you are a human, and humans have certain limitations and psychological weaknesses, and there is this whole gigantic corporate research and manufacturing apparatus designed to take advantage of those psychological weaknesses in order to exploit the maximum amount of profit from you, “the consumer.” The best defense against a wide array of their psychological attacks is simply to refrain from purchasing anything on credit. This helps you to keep all of your spending within rational limits, and to sidestep the innumerable lures and snares that have been laid for you all across this dystopian capitalist society.

If you ignore this advice and think simply in terms of credit instead of savings, then reality becomes blurred. The amount that you have to spend loses its connection with the amount that you actually own, making it very easy for you to spend money that you do not own, making it possible for you to buy anything that you have enough of a credit line to finance. Once this happens, you, a human, will start thinking of “saving” weirdly. “A penny saved is a penny earned,” you might chime, or “the easiest penny to earn is one that you didn’t spend.”

Instead of thinking about “saving” as putting money into your account, you will think of “saving” as any time you didn’t buy something. You “saved” money by not getting some random thing you could have. You “saved” a few dollars by not getting fries at lunch today. You “saved” by passing the chip aisle without getting as many as you normally get. You “saved” by cooking more meals this week than last week.

The problem with thinking of this as “saving” is that it has no basis in reality. You can’t “save” money by not spending. You could “not spend” 4 million times in one day and not have a single additional penny to your name. Are you starting to see the problem with calling this “saving money” whenever you didn’t spend money that you could have spent?

If you spent money, you spent money; you didn’t save money. If you bought something at a great 95% off bargain, you still didn’t save money; you spent money. The only way to save money is to increase your savings account. Period. There is a difference between smaller-negatives-than-usual and positives, even though it seems like they have the same effect. They only have the same effect as long as you were in the negatives anyway. That is, you can never start accumulating savings if you only “save” money through bargains and discounts and refraining from arbitrary purchases. It’s not really saving money unless you combine it with actually saving up money, such that your total wealth increases. “I was able to add $100 more to my bank account this month by cutting down on [thing] and not buying more of anything else.”

Again, avoiding spending on credit will help you to avoid this kind of psychological trap. If you are running on credit, then anything that results in a lower balance owed seems like saving, but it is just lower spending. In contrast, if you have to take money directly out of your savings for everything that you spend, it is much easier to feel the impact of each dollar that you spend, and you will weigh your dollars and your “savings” more rationally.

So, the long and the short of it is that you should make a habit of never paying for consumption on credit, as credit makes everything more expensive, and will eat into your future consumption by more than the amount that it is adding to your present consumption, resulting in a net loss for you overall. Additionally, avoiding debt spending entirely will insulate you from the majority of consumerist psychological prodding that corrals most Americans into credit card debt, and encourage you to be automatically more informed and thoughtful about the trajectory of your personal net worth.

Suppose that you are already barely making ends meet juggling credit cards, and this advice sounds somewhat useless to you. I am truly sorry for the state of our society, and I am doing what I know how to do to decrease the incidence of that type of situation for as many people as possible. Meanwhile, you are probably a prime candidate for honest bankruptcy, after which you’ll definitely want to read chapter three as it will help guide you through the easy and hard choices that you will probably have to make to become financially solvent.

As an aside, financing an investment is a different matter entirely, and you must instead consider the probability of the investment appreciating in value faster than the rate of interest minus the rate of inflation. That is to say, if you are taking out a loan to start a business or buy a house or increase your earning potential, it is possible that your investment could pay off more than the interest on the loan, so it could be worth it. In contrast, for consumption, there is usually a 0% chance that having your consumption a little early will pay off more than the interest on the loan, so it is almost never worth it.

Section I: Building Wealth Through Financial Habits

Chapter 1: Credit and Interest Chapter 2: Rent and Ownership Chapter 3: Budgeting & Reducing Expenses Chapter 4: Bargain Shopping Chapter 5: Optimizing How You Allocate Your Productive Time Section I Conclusion

Section II: Taking Advantage of Factors Bigger Than Oneself

Chapter 6: Crash Course In Microeconomics Chapter 7: Crash Couse in Macroeconomics Chapter 8: Why Businesses Sometimes Sell At A Loss Chapter 9: You, The Savvy Consumer Chapter 10: You, The Savvy Producer