Everyday Economics For People, Chapter 6: Crash Course In Micro Economics

Economics is somewhat technical and may perhaps be intimidating to those who are not at least a little familiar with this type of reasoning. Do not despair! You don’t need to understand every detail. Just try to pick up the broad strokes, and the practical instructions for money management at the end will make sense.

Before we can dive into our discussion of macroeconomics — the study of the wider economy — we require a foundational explanation of microeconomics, which is the study of how individuals interact with a specific market for one good or service at a time. There are two main branches to consider; we’ll start with demand.

Market demand for a good or service is the sum total of all of everyone’s willingness to buy that good or service at various prices. In order to talk about the sum total, however, first we will zoom in on a single individual, whose demand for a good or service is determined by these questions:

How much a person desires a thing depends on many factors, including human biology, personal biology, cultural and family upbringing, complementary goods, personal circumstances, and more. Whether or not they would spend money on the thing that they want depends on how much money they have available to spend, and what else they want to buy with that money.

For example, one person might have a cultural upbringing that makes them value very highly a particular brand of shoes. They could want those shoes very much. However, if that person has many other things to pay for, like food, rent, utilities, and transportation, they may not have enough left to purchase their favorite brand of shoes. They may be stuck buying a cheaper alternative.

That person would, of course, have some level of income which if they reached, they would finally buy the shoes they wanted. What level of income that would be is different for each and every individual customer! It also depends on how expensive the shoes are.

It can be very complicated to describe even just one single person’s total range of purchasing possibilities in different universes where they have different amounts of money or different access to complementary or substitute goods, or different cultural inputs, but if you hold most things constant and look at them one by one, you can see how they affect demand.

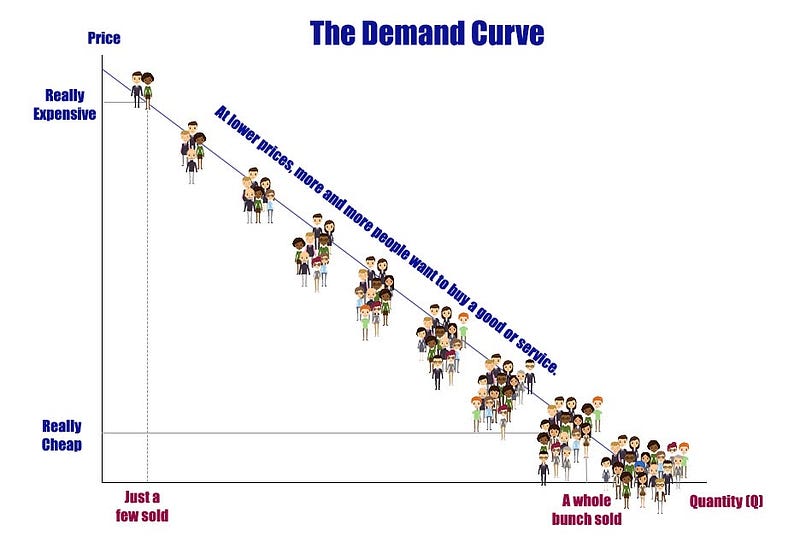

We are going to go further than that, and instead describe the sum total of a whole bunch of individuals’ preferences stacked together into one big graph called a demand curve.

Some people have more money than others, some have greater inherent desire for things, some have more needs and spread their income more thinly across them all. As a consequence, not everyone responds to a price level the same way. In short, some people will see “a bargain” where others see “overpriced.”

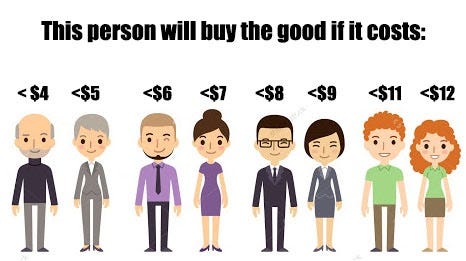

The demand curve is a graphical representation of how the total of all potential customers will respond to every possible price for a given good or service, if price changed and nothing else changed. For instance, if it costs $7.50, only the four people on the right will buy it. If it costs only $3, everyone will buy it.

When you put all of those people’s price requirements together into a graph, it shows you how many customers there would be at every price level, holding everything else constant.

There are many factors that affect demand for a good or service, i.e. increase or decrease the total number of customers willing to buy at every price level. The most important factors are the size and purchasing power of the potential consumer market. The more potential buyers there are, the more units a producer can sell at each price if the same proportion of them are willing to spend the same proportion of their money on the good. The more spending power each buyer has available, the higher the price they would be willing to pay for any given thing.

The next most important question is what need the good or service is meeting. If it doesn’t meet any or many needs compared to how much it costs, then it will have very low demand. Meanwhile, if it is something that is very useful for the price, there will likely be high demand for it.

However, another crucially important factor is the comparative price of any substitute good, which is something else that can meet the same need. Substitute goods come in two categories. There are the kinds that can be substituted directly for each other, like cotton vs. linen clothing, for example, or chicken and beef. Because we can substitute these things for each other, the price of one can never rise much beyond its substitutes or demand will simply shift to the substitute.

The other kind of substitution is between categories based on a hierarchy of needs. For example, rice and eggs can easily become substitutes for every other kind of consumption like entertainment if a person only has barely enough money to afford to eat. Because everything costs the same money, anything can be substituted for anything else, and basic needs can easily end up being “substituted” for everything that is optional. Thus, demand for a good is limited both by what other goods or services can meet the same needs, and also separately limited by its price relative to all other goods and services that a person could pay for instead to meet other needs, which may take priority to a certain threshold. Once a person is fed, then they suddenly demand other things besides food.

Another relevant factor is the cultural importance of the good or service within the population being considered. Some things are seen as indispensable in some populations, but are basically unheard of in others. Most things are somewhere in between. Sometimes this is because a good is “complementary” to another. For instance, hotdog buns would have almost no demand at all if hotdogs and sausages generally were not also in demand. Cultural prevalence of certain goods encourages demand for other related goods. Culture is one of the most difficult measures on which to collect data, but that does not prevent massive sums from being poured into advertising to build a culture of relevance for a product or brand.

In summary, the demand for a good or service can be affected by changes in the size of the consumer population, the spending power of each consumer, consumer attitudes about the product, general price indices, and the prices of direct substitutes. Increases in demand shift the curve outward, decreases shift it inward. Important note: demand is not affected by changes in price, because it is by definition a list of how consumers will respond to each price level. How much exactly is demand affected by various changes? Figure it out and you’ll receive tenure at Harvard! Still, the general trends are pretty clearly apparent.

Now we can talk about supply.

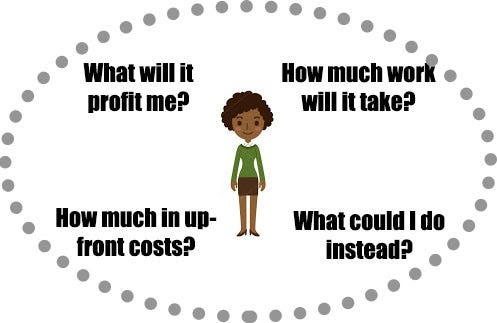

As with demand, supply is made up of a whole bunch of individuals. When an individual is thinking about becoming a producer of a good or service, they will ask the following questions:

As with demand, different people will have different situations that determine what their answers to these questions will be. The first question sounds like it is about money, but not everyone thinks about profit strictly in terms of money. There are other goals a person may have when choosing to be a producer of something, and that will be entirely personal but based on human biology, personal biology, family and cultural upbringing, social context, personal circumstances, personal priorities, and more.

The second question, regarding how much work something will take, has multiple dimensions as well. For some, certain kinds of labor are difficult for them to perform even for short periods, whereas others would happily do the task for hours on end. Not everyone must put in the same amount of work to complete the same number of hours or tasks. Individual decisions to become producers will vary for these reasons.

The third question is much more straightforward, although it could refer to time costs as well as monetary costs. For example, a person may need to complete 8 years of school to become qualified for certain kinds of labor. Even if it is fully paid for, that is a serious cost to consider.

The final question is the most important, but usually gets the least attention because it is so broad that a complete answer is often impossible to arrive at. What could a person substitute instead of working one job, or starting one business? The potential answers number in the thousands, if they have a limit at all. The “right” path for each person is entirely personal and subjective. Most people choose between the most obviously apparent choices and stop thinking about it, at that. You, and everyone, should think about it more than most people currently do.

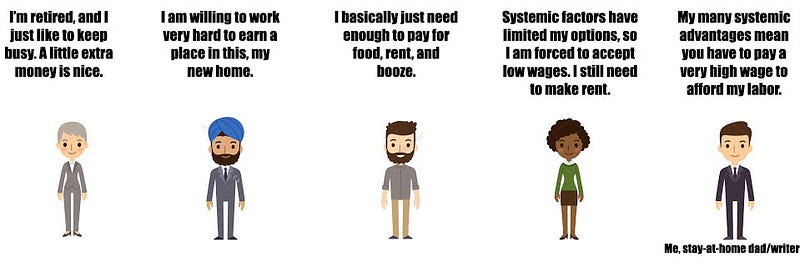

A quick note about privilege. You’ll notice that I put an image of a black woman, because I didn’t want to be accused of promoting the idea that white men are the main producers. Take a look at the bottom two questions: do you think black women have the money to put up or equal sets of options for being productive as compared with other statistical groupings of people — for example, white men? The answer to that question is, “What are you smoking? Obviously not,” but it is also beyond the scope of this book. I do recommend that you think about the nature of the system and what could possibly be changed to improve it for all of its members even as you think about how to work within it for your own benefit.

Okay, so again, it can be very complex to describe even just a single individual’s total set of responses to various price levels for producing various kinds of goods and services, because that individual is affected by dozens (at least) of factors that influence their decisions. However, when we stack all of the different people’s individual curves together and hold everything constant, we can get some useful information about how many people will sign up to produce something depending on how much others are willing to pay for that thing.

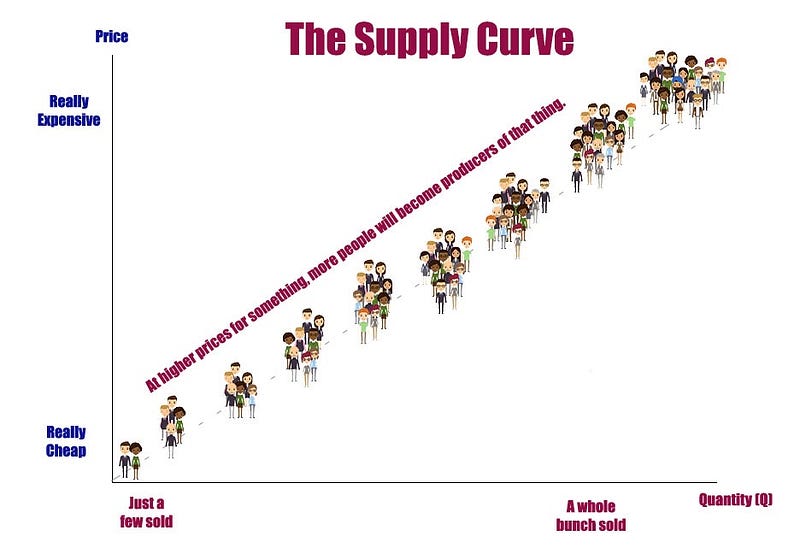

Simply put, the more it is worth to sell something, the more people will produce it.

The supply curve is a representation of how many people will put their resources and efforts into producing and selling something at a given price. It is typically depicted like this to demonstrate that more and more people would be willing to become producers of something if it sold for enough money.

For example, if pork suddenly somehow became worth its weight in gold, then everyone who was able would suddenly start buying up land and piglets to cash in on the incredible bonanza. Meanwhile, if beef and cow’s milk were suddenly too culturally unpopular to eat, then everyone raising cattle would suddenly exit the industry and produce something else. Note, this would not change the supply curve, but just move along it to a point with more people working it.

There are many factors that move the supply curve. The most important factors are the number of potential producers and how much money they have to invest in production. The more potential producers there are, the greater the capacity for supply to be filled. The more money potential producers have for investing, the greater a supply they can actually generate to meet demand.

The next most important question is how much each of the factors of production costs. Factors of production vary by product, but generally can be said to include labor, taxes, raw materials, intermediate goods, rent, utilities, and anything else a business has to pay to operate. Note that the costs of each of these things goes up the more of them you use. For example, if you rent one building, you can rent the cheapest one, whereas if you rent five buildings, you would have to get the five cheapest at best, which will have a higher average cost than the cheapest one had. This principle applies to virtually all factors of production.

Another sneaky note about systemic barriers to some peoples’ success: an economic caste system, maintained racially or otherwise, allows for businesses to operate with very cheap labor for the least expensive goods, bringing down prices for certain things at the expense of the laborers producing those inexpensive goods. These low prices create more available wealth to be spent on other, expensive goods, to the benefit of those workers creating the expensive things. This works cyclically to preserve itself across time, as the “expensive workers” continue to live in luxury and plenty, which allows their children to afford the training to become “expensive workers,” whereas the “inexpensive workers” continue to live in poverty and want, and their children don’t have the resources to afford the training to become “expensive workers.” The caste system allows for the creation of very advanced production at the expensive end, subsidized secretly by the inadequate financial health of the lower castes. Keeping a segment of the population very poor actually improves the profitability of businesses. Understatement: profitability of businesses can be overrated.

The next most important question is how much it costs a producer in order to begin production. In most cases, there are substantial startup costs associated with developing productive capacity. The greater the initial barriers to entry, the less supply will be able to increase in reaction to higher prices. Those barriers could be government requirements, or they could be “naturally occurring” economies of scale, or other. On an individual level, barriers could include differential schooling received in youth, lack of geographic access to lucrative opportunities, having to be a misfit of some type, lack of access to affordable finance, and more.

Finally, perhaps most importantly, just as consumers can substitute one product for another, so producers also can substitute one type of production for another. Therefore, the supply for a good or service is impacted by all of the other opportunities potentially available to a producer. Some products may potentially be profitable, but never get produced because other opportunities crowd them out. Note: this is often due to ignorance/uncertainty about their potential rather than a lack of potential, although it is also often because they would barely be profitable at all.

So, in summary, supply of a good or service is impacted by changes in the availability of investment funding, the number of potential producers/investors, the number of opportunities available to producers/investors, the costs of the factors of production, and even the cultural appropriateness of producers participating in the market. In many cases, it takes a very high market price to entice any producers into participating with all the costs for them (for example, dealing in kidneys, legally with medical debt or otherwise with the feds after them!).

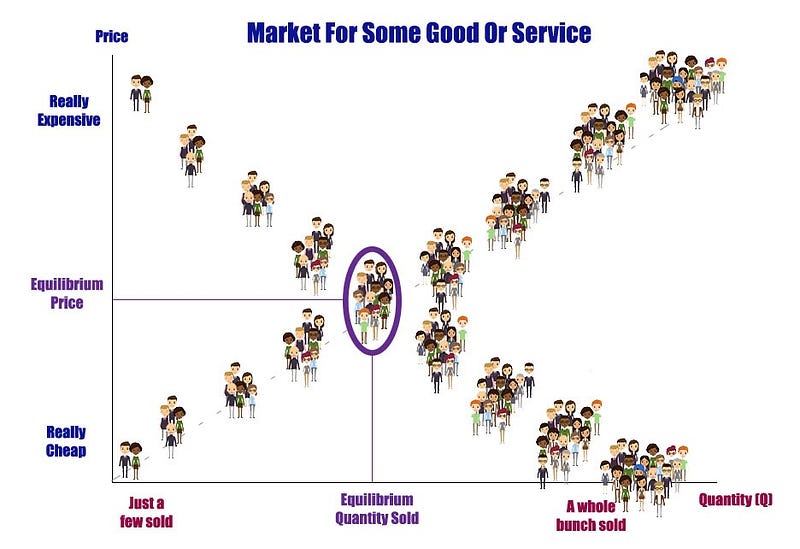

Now, as you may have already noticed, the demand curve pairs higher quantities with lower prices, whereas the supply curve pairs higher quantities with higher prices. Thus, because they start at opposite places and move in opposite directions, the market equilibrium occurs where the two curves can agree on a price and quantity.

This equilibrium can easily be adjusted by anything that impacts either curve, as well as arbitrary government limitations, and should be recognized as circumstantial rather than “natural,” even though it emerges “naturally” in any given situation.

For example, anything that limits the supply would shift the demand curve to the left, moving the “natural” equilibrium to a higher price and lower quantity sold. Anything that expands supply would move the supply curve to the right, making it meet demand at a higher quantity and decreased price. Same principle: anything that limits demand would decrease quantity and decrease price. Anything that increases demand would increase quantity and increase price.

Boom. That’s it! You’ve got, like, most of an Econ 101A credit right there. What? Elasticity? Comparative advantage? Consumer and producer surplus? Government interventions? Some other stuff? Okay, so it’s not a full credit. We don’t need those right now.

Section I: Building Wealth Through Financial Habits

Chapter 1: Credit and Interest Chapter 2: Rent and Ownership Chapter 3: Budgeting & Reducing Expenses Chapter 4: Bargain Shopping Chapter 5: Optimizing How You Allocate Your Productive Time Section I Conclusion

Section II: Taking Advantage of Factors Bigger Than Oneself

Chapter 6: Crash Course In Microeconomics Chapter 7: Crash Couse in Macroeconomics Chapter 8: Why Businesses Sometimes Sell At A Loss Chapter 9: You, The Savvy Consumer Chapter 10: You, The Savvy Producer