About the Dumbest Money Mistake You Can Make

Emotion rocks unless it dominates your life and risks your livelihood

You can’t remove emotion from most money equations. You can only hope to contain it. To properly channel the bits and pieces that bubble to the surface.

This sane, logical, and sound strategy has a dark side. That’s what this article is about. The dark side that can render you insolvent or close to it.

Emotion influences most aspects of life. We can’t pick and choose where emotion impacts and helps direct our trajectories. Sometimes emotion makes us uncomfortable. Like at the beginning of a relationship with someone we really like. Or in a conflict, you‘d prefer to avoid. Tense as it may be, this discomfort helps situate our stories. All these feels give the world soul.

Emotion belongs in personal finance and investing. The gurus say you must remove emotion from the equation, especially when investing your money. There might not be worse advice. It’s like telling a teenager not to drink or have sex.

You can’t suppress psycho-emotionally fueled behaviors. But you can learn how to recognize the way you feel and how you might respond. This gives you the opportunity to pause, collect your thoughts, adjust, and act accordingly.

In a recent Making of a Millionaire article, I lamented successful Tesla investors who — despite becoming, in some cases, millionaires thanks to the stock — remain all-in. Some stay fully invested in Tesla. To make matters worse, they’re doubling down using leverage in margin accounts.

This scares the heck out of me.

Full disclosure: I’m long Tesla stock. I bought one share. It goes against my policy of only purchasing stocks that pay dividends. I bought the stock on December 22, 2020, for $630. As of this writing, on New Year’s Eve 2020, it trades for $705.67. Not bad.

I bought Tesla for two reasons: One, I think it will continue to fly. Two, I want to experiment with buying a small number of shares of high-priced stocks to see how they perform against my relatively conservative but larger positions in dividend-paying stocks.

So there’s that. A far cry from turning $23,000 into $2 million or whatever. However, if I was lucky enough — stress the word, lucky — to have done that, I would have taken a vast majority of the money and run. Fast. Because the bottom can fall out at any time.

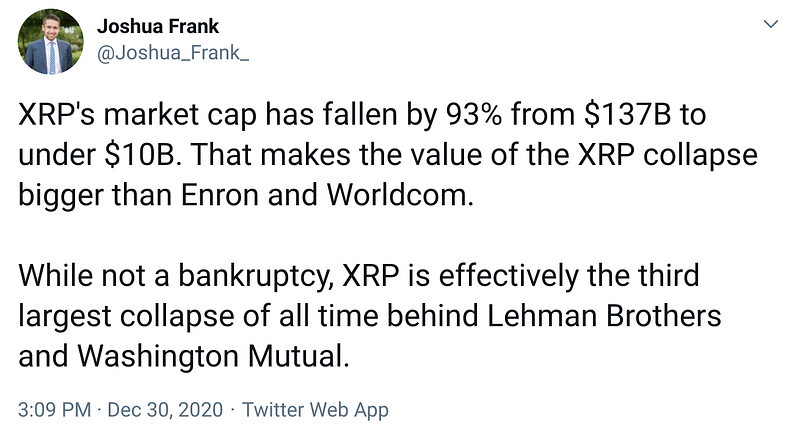

Case in point — the cryptocurrency Ripple (XRP). You might have read about what’s happening with it. Not so long story short, the U.S. Securities and Exchange Commission is after Ripple for the way it brought its token to market. Cryptocurrency exchanges continue to drop Ripple’s XRP from their platforms. Apparently, XRP’s demise is the third biggest collapse in history.

I bring this up not to get into the specific merits of investing in any one stock or cryptocurrency — we don’t do that here at Making of a Millionaire — but to highlight how terrifyingly dangerous it is to put all of your eggs in one basket even if you throw a super cute and adorable cat in the basket along with your eggs.

A few years ago, I successfully traded Ripple. There’s a Ripple cult out there. Gaggles of people emotionally attached to the token. They even sell Ripple t-shirts. I bought one. But that marked the extent of my fandom. I took a cold approach, methodically trading in and out, abiding by my predetermined price targets.

A few weeks ago, I looked at Ripple again. I almost bought some. Thank goodness I didn’t. While I would have invested only a small fraction of my cash, it still would have sucked to be stuck in this thing. Not only has it crashed, but I assume I would have had difficulty trading out of it. In any event, it would have been a stressful situation.

Take my scenario a step further. There are certainly large swaths of people all-in Ripple. As in, the token comprises a vast majority, if not all, of their invested assets. Imagine what they’re going through right now.

No matter how you rationalize it, this isn’t all that different from being all-in Tesla — or any other stock for that matter. One false move from Elon Musk — love the guy, but he’s known to make false moves — and we could see something similar happen with Tesla stock.

Don’t believe me?

2020. Enough said.

The dumbest money move you can make — ever — is going all-in. If Enron, Worldcom, Lehman Brothers, and Washington Mutual didn’t make this clear, let Ripple be the present-day example. There’s no doubt in my mind — just read the message boards — that the people who go all-in on a Ripple or Tesla let emotion take control.

They become emotionally attached to a token or stock. They allow the battleground that exists around the investment to get inside their head. Being invested in something that generates so much passion flips the context — at least in your mind — from being in an investment to rooting for a sports team.

But it’s more than rooting. It’s like you have to prove loyalty to your team. It’s one thing to shave your head or get a tattoo. It’s entirely another to invest all of your savings in something, obsess over it all day online, try to get your friends to buy it, and say you’re going to hold it to the death.

You can extend this logic. (I hope you’re reading this as a logical thought process!). You can extend this logic into plain personal finance. Just as you can and probably should diversify your investment portfolio, you can and probably should diversify what we’ll call your personal finance portfolio.

It makes no sense to keep all of your cash in a checking account.

It makes no sense to keep all of your cash in an emergency fund.

It makes no sense to keep all of your cash in a rainy day fund.

It makes no sense to keep all of your cash in all of the above if you’re generating enough cash flow to fully stock a checking account, emergency fund, and rainy day fund.

You gotta branch out. Create pots of money to satisfy short- and long-term needs, wants, desires, passions, and goals. Spread your cash across accounts. By efficiently allocating your income, you’ll probably do a better job keeping track of it, hanging on to it, and saving/spending it wisely.

Be thoughtfully comprehensive. Aim for healthy diversity. Craft a targeted series of personal finance and investing elements to comprise a purposeful and wider approach to managing your money.

This isn’t necessarily the opposite of dumb. It’s merely in the ballpark of not making the dumb decision of marrying yourself to one position while ignoring the risk inherent in this approach. Hopefully, we’re all in the same ballpark. Operating within a common, general framework, each of us will organize our personal finance and investing activities in a way that works for us.

Ideally, we’ll welcome and do the work to recognize our emotions. We’ll divert this emotional energy to make the choices that will take care of our immediate needs, mid-range goals, and far-off futures while ensuring we have more good sleeps than restless nights.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.