Try This Move in Your Checking Account to Save and Invest More Money

I’m taking the Tim Ferriss approach to personal finance

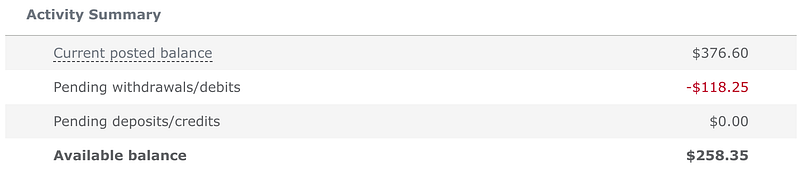

I have $258.35 in my checking account.

This might lead you to conclude I’m in financial trouble. However, the opposite holds true. I’ve never been financially more healthy than I am today.

I’m just running an experiment on myself.

In this article, I detail this experiment and illustrate how you can conduct it on yourself.

“…self-experimentation need not be extreme (I do the extremes so you don’t have to), and you can make significant discoveries with a sample size of one.”

I like Tim Ferriss’s approach. He advocates self-experimentation, within reason, but tries out the extreme stuff on himself. So you don’t have to.

While Ferriss does things to and with his body I’d never try, I am willing to apply his extreme strategy to my personal finance.

Because it’s the only way to truly make personal finance personal.

If I adhere to the things I’m doing now — and only the things I’m doing now — they risk becoming dogma. Then these articles function like most everyone else’s. I can only advance the conversation — and my own relationship with money — if I challenge my tried and trues.

This doesn’t mean there aren’t things I do that I’ll do forever. Strong conviction and adherence to the practices it spawns can be good. But it can also put you in a rut. I never want to go through the motions, because there’s always another way to, at the very least, consider, if not out and out live by.

Running on a well-calculated empty in your checking account

I advocate and practice an income allocation strategy that keeps ample cash on hand to meet all of your immediate and short- to mid-term money needs before you invest a dime. You can read about it in detail here and here.

However, I recently started questioning the wisdom of a two times expenses cushion in my checking account. Not due to inflation fears or anything like that. But because (a) I have my emergency fund satisfactorily stocked and (b) I have regular income flowing. Income I’m confident (knock on wood) will continue to flow for the foreseeable future.

Because I pay all of my bills first — before I save and invest — I divert income to obligatory and discretionary expenses as I receive money throughout the month. I save and invest the monthly surplus. An extra couple to a few thousand sitting in my checking account serves little purpose. It’s not security. That’s why you keep emergency and rainy day funds.

That cushion does nothing, other than, potentially, encourage unneeded spending. There’s a strong psychological pull to seeing a large checking account balance amid consistent cash flow and knowing you will pay your bills with relative ease.

So I decided to take the following steps:

- Remove the two times expenses cash cushion from my checking account.

- Make precise weekly estimates of upcoming outflows to ensure a satisfactory account balance.

- Invest the $3,900 cash cushion in dividend-paying stocks.

So, at the moment, I’m running a checking account balance of $258.35.

Before the end of the month, I’ll receive an income that pays my rent. In the first week of November, I take in cash that will meet my other expenses and then some.

After running the numbers in the last week of October and first week of November, I’ll move the surplus to the appropriate savings and investments accounts, leaving only what I need to pay bills and other discretionary expenses (i.e., coffee, a stop at the plant store, etc.) in my checking account.

While there’s something psychologically unsettling about running with such a low checking account balance, I want to push myself into relatively uncomfortable territory. It’s a worthy experiment. However, it’s one I’m okay guinea pigging with only because:

- I have my savings accounts adequately stocked.

- I feel confident in my present and future cash flow.

I’m already seeing other attendant, positive effects.

For example, my investment portfolio — full of dividend-paying stocks — yields roughly 4.5%. This means the dividend income I receive from my stock holdings generates annual cash equal to about 4.5% of my account balance. Therefore, I increased the dividend income my portfolio produces by $175.50 per year.

However, I reinvest this money into new shares of stock so I experience the power of compounding:

I made super modest assumptions in this model — no share price appreciation, meager 1% annual dividend growth, and no additional contributions other than dividend reinvestment. The reality is I’ll probably take what used to be my checking account cushion and invest it on the regular, in addition to the money I already invest on a regular basis.

With this in mind, look at what adding a monthly contribution of $1,000 in new money does to this 10-year projection:

Mind. Blown.

A $3,900 initial investment, followed by $1,000 monthly investments and quarterly dividend reinvestment over ten years without any consideration of growth, yields a balance of $156,286.58.

You can learn all about how dividends function here and here.

As with most things in life, you gotta be willing to experiment.

Like Tim Ferriss says, you can learn quite a bit via a sample size of one. While this doesn’t work in the aggregate as social science research, it’s significant in personal finance, particularly if you — and you alone — comprise the sample.

Broad applications of commonly-spewed, money-related tenets can’t possibly take into account individual circumstances and, most importantly, the psycho-emotional states they create. So we tinker within the context of our own lives.

I tinker in the hope that you can pull something — even a sliver — from my experience and use it to help inform and enhance your own.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.